Contemporary Accounting Theory: Crown Resort Sustainability Report

VerifiedAdded on 2022/09/29

|21

|4641

|27

Report

AI Summary

This report delves into the sustainability reporting practices of Crown Resort Limited, examining the company's approach to corporate social responsibility (CSR) within the framework of contemporary accounting theory. The analysis begins with an exploration of why CSR is increasingly vital for financial firms, the holistic nature of sustainability reporting, and relevant theoretical underpinnings, including legitimacy and institutional theories. The report then applies this theoretical knowledge to Crown Resort Limited, providing a company overview, assessing its sustainability performance using GRI guidelines, and evaluating the extent and quality of its sustainability reporting. The report highlights the importance of sustainability reporting in addressing stakeholder needs and its role in enhancing a company's public image and long-term viability. It concludes with an assessment of the company's performance and recommendations for future improvements in its sustainability reporting practices. The report aims to provide a comprehensive understanding of the subject matter, integrating theoretical concepts with practical application and evaluation.

Running head: CONTEMPORARY ACCOUNTING THEORY

Report on the sustainability reporting of crown resort limited

Student’s name

Name of the university

Authors note

Report on the sustainability reporting of crown resort limited

Student’s name

Name of the university

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 2

Table of Contents

Executive summary.............................................................................................................3

Introduction..........................................................................................................................3

PART A: THEORETICAL UNDERSTANDING OF THE CONCEPTS..........................4

i). Why CSR is increasing among financial firms...........................................................4

ii). whether sustainability reporting represents a holistic view of CSR...........................6

iii). Theories that explain the essence of sustainability reporting....................................7

PART B: APPLICATION OF THEORETICAL KNOWLEDGE......................................9

iv). Company overview....................................................................................................9

v). sustainability scoring index according to the GRI guidelines..................................11

vi). Extent and quality of Crown Resort limited sustainability reporting......................14

Conclusions........................................................................................................................16

References..........................................................................................................................17

Table of Contents

Executive summary.............................................................................................................3

Introduction..........................................................................................................................3

PART A: THEORETICAL UNDERSTANDING OF THE CONCEPTS..........................4

i). Why CSR is increasing among financial firms...........................................................4

ii). whether sustainability reporting represents a holistic view of CSR...........................6

iii). Theories that explain the essence of sustainability reporting....................................7

PART B: APPLICATION OF THEORETICAL KNOWLEDGE......................................9

iv). Company overview....................................................................................................9

v). sustainability scoring index according to the GRI guidelines..................................11

vi). Extent and quality of Crown Resort limited sustainability reporting......................14

Conclusions........................................................................................................................16

References..........................................................................................................................17

CONTEMPORARY ACCOUNTING THEORY 3

Executive summary

This report contains information regarding the different aspects of sustainability reporting

and contemporary accounting in general. Crown Resort Company limited was used as the major

company and therefore part of the information that was used was obtained from the company’s

annual reports. This report is however presented in about two subsections and these include part

one (A) and part two (B). The first part mainly provides explanations relating to the theoretical

understanding of the GRI framework of accounting. The second part (B) of the report, on the

other hand, emphasizes the practical concerns of the framework. Therefore, in this particular part

of the report, the relevant company information is used to make the required sustainability

company assessments.

Introduction

This report will contain an analysis regarding the various concepts of sustainability

reporting framework of accounting. Therefore, information such as that which is related to the

sustainability reporting standards will be highly vital and required. To obtain al such

information, a review of the existing literature will be carried out. This will be done to gain an

understanding of the different benefits that are associated with sustainability reporting. A

contrast between sustainability reporting and other conventional accounting methods will also be

conducted. At the same time, a few theories regarding sustainability reporting will be explained

to provide a better understanding of the concepts.

In the second part of the report however, the focus will be drawn towards assessing the

historical background of the chosen company of interest. Additionally, the report will also

Executive summary

This report contains information regarding the different aspects of sustainability reporting

and contemporary accounting in general. Crown Resort Company limited was used as the major

company and therefore part of the information that was used was obtained from the company’s

annual reports. This report is however presented in about two subsections and these include part

one (A) and part two (B). The first part mainly provides explanations relating to the theoretical

understanding of the GRI framework of accounting. The second part (B) of the report, on the

other hand, emphasizes the practical concerns of the framework. Therefore, in this particular part

of the report, the relevant company information is used to make the required sustainability

company assessments.

Introduction

This report will contain an analysis regarding the various concepts of sustainability

reporting framework of accounting. Therefore, information such as that which is related to the

sustainability reporting standards will be highly vital and required. To obtain al such

information, a review of the existing literature will be carried out. This will be done to gain an

understanding of the different benefits that are associated with sustainability reporting. A

contrast between sustainability reporting and other conventional accounting methods will also be

conducted. At the same time, a few theories regarding sustainability reporting will be explained

to provide a better understanding of the concepts.

In the second part of the report however, the focus will be drawn towards assessing the

historical background of the chosen company of interest. Additionally, the report will also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 4

contain data regarding sustainability scoring index. This type of data will, however, be collected

from a variety of published information sources.

PART A: THEORETICAL UNDERSTANDING OF THE CONCEPTS

i). Why CSR is increasing among financial firms

Whereas a universally acceptable definition of corporate social responsibility may not be

available, CSR can be defined in several ways. For instance, the concept can be referred to as

the activities and processes that a firm can undertake to achieve a positive societal image. Such

activities may include carrying out ethical activities, economic duties, and acceptable legal

behaviours and so on (Vitolla and Rubino, 2018). However, financial entities and firms have

increasingly embraced corporate social responsibility for different reasons and these are

explained below:

In this part of the report, emphasis will be drawn to specifically three aspects of

assessment. These will include relationships between CSR and employee turnover, CSR

customer satisfaction and lastly CSR contribution towards a company's public image. Therefore,

these will be the major points of discussion as to why firms are increasingly adopting CSR (Carp

et al, 2019). To begin with, almost all corporate entities consider their manpower as the most

valuable resource. Therefore, there is a need to preserve and retain such human resource for the

longest time possible. It is out of such concerns that a company's top management executives

will strive to undertake activities to ensure that there is a low labour turnover. If a company can

retain its employees and workers, it brings an impression in the general public that such a

company is effectively performing well. In summary, ensuring that low labour turnovers within

contain data regarding sustainability scoring index. This type of data will, however, be collected

from a variety of published information sources.

PART A: THEORETICAL UNDERSTANDING OF THE CONCEPTS

i). Why CSR is increasing among financial firms

Whereas a universally acceptable definition of corporate social responsibility may not be

available, CSR can be defined in several ways. For instance, the concept can be referred to as

the activities and processes that a firm can undertake to achieve a positive societal image. Such

activities may include carrying out ethical activities, economic duties, and acceptable legal

behaviours and so on (Vitolla and Rubino, 2018). However, financial entities and firms have

increasingly embraced corporate social responsibility for different reasons and these are

explained below:

In this part of the report, emphasis will be drawn to specifically three aspects of

assessment. These will include relationships between CSR and employee turnover, CSR

customer satisfaction and lastly CSR contribution towards a company's public image. Therefore,

these will be the major points of discussion as to why firms are increasingly adopting CSR (Carp

et al, 2019). To begin with, almost all corporate entities consider their manpower as the most

valuable resource. Therefore, there is a need to preserve and retain such human resource for the

longest time possible. It is out of such concerns that a company's top management executives

will strive to undertake activities to ensure that there is a low labour turnover. If a company can

retain its employees and workers, it brings an impression in the general public that such a

company is effectively performing well. In summary, ensuring that low labour turnovers within

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 5

the company is one of way facilitating organizational growth, productivity and performance in

the long run.

The second reason as to why corporate entities are turning towards social corporate

responsibility is the need for better customer satisfaction. Because customer satisfaction is a

continuous process, it plays a significant role in the past, present and future performance of the

business entity (Hahn, 2013). Therefore, to determine a company’s profitability close attention

must be paid to the number of customers served. . Therefore, to ensure that customers are fully

satisfied, corporate social responsibility is a vital tool for the firms. Corporate social

responsibility operates in a way that promotes equity for the customer. For instance, if an entity

conducts environmental duties, the surrounding community of such an entity will feel justified.

With such a close relationship benefits such as customer, royalty is some of the advantages that

the firm would obtain (Camilleri, 2017).

Lastly, the need to create a reputable societal image of the company which would imply

that a company or firm is highly recognized. Recognition on the other can be defined as the

external assessment that outsiders can attribute to any given business or corporate entity having a

positive image would imply an increase in sales, profitability and so on (Glover et al, 2014). On

the other, however, a negative public image or reputation would result in continued losses and

the worst-cases collapse. Therefore, besides the financial determinants of a company's

performance, other social aspects such as public image and reputation have a vital role in a

company's existence and success.

the company is one of way facilitating organizational growth, productivity and performance in

the long run.

The second reason as to why corporate entities are turning towards social corporate

responsibility is the need for better customer satisfaction. Because customer satisfaction is a

continuous process, it plays a significant role in the past, present and future performance of the

business entity (Hahn, 2013). Therefore, to determine a company’s profitability close attention

must be paid to the number of customers served. . Therefore, to ensure that customers are fully

satisfied, corporate social responsibility is a vital tool for the firms. Corporate social

responsibility operates in a way that promotes equity for the customer. For instance, if an entity

conducts environmental duties, the surrounding community of such an entity will feel justified.

With such a close relationship benefits such as customer, royalty is some of the advantages that

the firm would obtain (Camilleri, 2017).

Lastly, the need to create a reputable societal image of the company which would imply

that a company or firm is highly recognized. Recognition on the other can be defined as the

external assessment that outsiders can attribute to any given business or corporate entity having a

positive image would imply an increase in sales, profitability and so on (Glover et al, 2014). On

the other, however, a negative public image or reputation would result in continued losses and

the worst-cases collapse. Therefore, besides the financial determinants of a company's

performance, other social aspects such as public image and reputation have a vital role in a

company's existence and success.

CONTEMPORARY ACCOUNTING THEORY 6

ii). whether sustainability reporting represents a holistic view of CSR

Unlike in the past trends of business operations, the present environment calls for a

variety of stakeholder requirements (Crane, Matten and Spence, 2013). The vast range of

stakeholder categories such as employees, shareholders, investors, authorities and so on demands

for a wide range of business assessment. It is notably evident that each of these of the entity

stakeholders has specific interests and desires that must be fulfilled if an organization is to be

considered socially viable. Therefore, organizations and corporate entities had to consider the

aspect of sustainability reporting if all such needs were to be effectively met. For instance,

applying sustainability reporting implies that corporate entities had to ensure transparency at the

highest level. This includes reporting for reputation, legitimacy and competitiveness.

With shifts towards a more environmentally related type of reporting, traditional western

approaches became increasingly unrepresentative. It is such a trend that facilitated the

development of frameworks such as the GRI which are considered as the de-facto global

reporting standards of sustainability reporting (Gauthier, 2013). Questions regarding

sustainability reporting and CSR can be answered through sustainability concepts such as social,

environmental, ethical and human rights among others. For instance, sustainability reporting

considers the social aspect of reporting as the duty of corporate entities to assess the impacts of

the decisions taken on the environment and the entire community. This should, however, be done

through aspects such as ethical transparency socially acceptable behaviour. Additionally, the

increasing change of reporting for corporate entities represents a holistic relationship between

CSR and sustainability reporting. This is identified through the multidimensional reporting

standards and other integrated report of organizations. These integrated reports are an

illustration of both the traditional financial information together with the sustainability

ii). whether sustainability reporting represents a holistic view of CSR

Unlike in the past trends of business operations, the present environment calls for a

variety of stakeholder requirements (Crane, Matten and Spence, 2013). The vast range of

stakeholder categories such as employees, shareholders, investors, authorities and so on demands

for a wide range of business assessment. It is notably evident that each of these of the entity

stakeholders has specific interests and desires that must be fulfilled if an organization is to be

considered socially viable. Therefore, organizations and corporate entities had to consider the

aspect of sustainability reporting if all such needs were to be effectively met. For instance,

applying sustainability reporting implies that corporate entities had to ensure transparency at the

highest level. This includes reporting for reputation, legitimacy and competitiveness.

With shifts towards a more environmentally related type of reporting, traditional western

approaches became increasingly unrepresentative. It is such a trend that facilitated the

development of frameworks such as the GRI which are considered as the de-facto global

reporting standards of sustainability reporting (Gauthier, 2013). Questions regarding

sustainability reporting and CSR can be answered through sustainability concepts such as social,

environmental, ethical and human rights among others. For instance, sustainability reporting

considers the social aspect of reporting as the duty of corporate entities to assess the impacts of

the decisions taken on the environment and the entire community. This should, however, be done

through aspects such as ethical transparency socially acceptable behaviour. Additionally, the

increasing change of reporting for corporate entities represents a holistic relationship between

CSR and sustainability reporting. This is identified through the multidimensional reporting

standards and other integrated report of organizations. These integrated reports are an

illustration of both the traditional financial information together with the sustainability

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 7

information. By undertaking such approaches of reporting, organizations reflect major

consideration towards the corporate social responsibility and the financial information

requirements. The implication in such reports is that the performance of such organizations is

entirely dependent upon the CSR factors and other financial dynamics. Therefore, sustainability

reporting by corporate entities represents a holistic view of CSR requirements (Galbreath, 2010).

iii). Theories that explain the essence of sustainability reporting

There are about three types of theories that can be used to assess the essence of

sustainability reporting by organizations. These may include the legitimacy theory, stakeholder

theory and the institutional theory of sustainability reporting. However, for this particular report,

emphasis will be laid upon the legitimacy theory and institutional theories.

The legitimacy theory of sustainability reporting specifically concentrates on the possible

relationship between corporate entities and their surrounding communities (Crane, Matten and

Spence, 2013). Therefore, successful organizations according to the legitimacy theory are

obliged to embrace social behaviours and practices of the societies in which they are located

(Crown Resort Limited, 2014). Such an adoption to the societal and social requirements is done

with the view of promoting mutual existence in the community. With this mutual relationship,

the community provides the organization with required raw materials and in return, the

community provides a reliable market for the produced commodities. This type of transaction

and co-existence ultimately result in mutually beneficial exchanges between entities and the

community (Bashatweh, 2018).

The second theory of focus in this report is the institutional theory of sustainability.

According to the institutional theory of sustainability, a firm’s operations are largely under the

information. By undertaking such approaches of reporting, organizations reflect major

consideration towards the corporate social responsibility and the financial information

requirements. The implication in such reports is that the performance of such organizations is

entirely dependent upon the CSR factors and other financial dynamics. Therefore, sustainability

reporting by corporate entities represents a holistic view of CSR requirements (Galbreath, 2010).

iii). Theories that explain the essence of sustainability reporting

There are about three types of theories that can be used to assess the essence of

sustainability reporting by organizations. These may include the legitimacy theory, stakeholder

theory and the institutional theory of sustainability reporting. However, for this particular report,

emphasis will be laid upon the legitimacy theory and institutional theories.

The legitimacy theory of sustainability reporting specifically concentrates on the possible

relationship between corporate entities and their surrounding communities (Crane, Matten and

Spence, 2013). Therefore, successful organizations according to the legitimacy theory are

obliged to embrace social behaviours and practices of the societies in which they are located

(Crown Resort Limited, 2014). Such an adoption to the societal and social requirements is done

with the view of promoting mutual existence in the community. With this mutual relationship,

the community provides the organization with required raw materials and in return, the

community provides a reliable market for the produced commodities. This type of transaction

and co-existence ultimately result in mutually beneficial exchanges between entities and the

community (Bashatweh, 2018).

The second theory of focus in this report is the institutional theory of sustainability.

According to the institutional theory of sustainability, a firm’s operations are largely under the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

influence of social factors such as culture, environment and tradition among others. Therefore,

unlike the past trends in firms had closed and independent systems, the institutional theory of

sustainability has changed this trend (Moravicikova, Stenfanikova, and Rypakova, 2015).

Pressures resulting from the social, political, economic and other forces have led to significant

changes in organizational strategies and operations. For instance, before a decision is undertaken

by an entity’s management, consideration must be given to the general environment. This takes

into account the possible effects that a particular decision will have on the entire organizational

environment. Therefore, this means that the management of an entity according to this theory

management should ensure that all stakeholders’ requirements are addressed. The failure to

undertake such an analysis would consequently jeopardize sustainability (Whitely, 2016). This

institutional theory further operates on about three drivers namely: coercive drivers, normative

and mimetic. The coercive drivers in this sense are those drivers that are as a result of influence

from powerful forces and factors. These may, however, be both internal and external depending

on the prevailing situations.

The normative drivers on the other and focus on the organizational conformity to the

social demands. Organizations that adhere to these factors or drivers benefit in the long run

through increased profitability. These drivers may include the ethical standards, ecological

perspectives and so on. With the mimetic drivers of the theory, an organization simply learns

from the activities of other competitor firms in the same industry. Therefore it involves

borrowing a leaf from what other corporate entities are doing to achieve sustainability. By

replicating the competitors' strategies and decisions, the organization assumes success and

legitimacy within the community and general society of long-run sustainability.

influence of social factors such as culture, environment and tradition among others. Therefore,

unlike the past trends in firms had closed and independent systems, the institutional theory of

sustainability has changed this trend (Moravicikova, Stenfanikova, and Rypakova, 2015).

Pressures resulting from the social, political, economic and other forces have led to significant

changes in organizational strategies and operations. For instance, before a decision is undertaken

by an entity’s management, consideration must be given to the general environment. This takes

into account the possible effects that a particular decision will have on the entire organizational

environment. Therefore, this means that the management of an entity according to this theory

management should ensure that all stakeholders’ requirements are addressed. The failure to

undertake such an analysis would consequently jeopardize sustainability (Whitely, 2016). This

institutional theory further operates on about three drivers namely: coercive drivers, normative

and mimetic. The coercive drivers in this sense are those drivers that are as a result of influence

from powerful forces and factors. These may, however, be both internal and external depending

on the prevailing situations.

The normative drivers on the other and focus on the organizational conformity to the

social demands. Organizations that adhere to these factors or drivers benefit in the long run

through increased profitability. These drivers may include the ethical standards, ecological

perspectives and so on. With the mimetic drivers of the theory, an organization simply learns

from the activities of other competitor firms in the same industry. Therefore it involves

borrowing a leaf from what other corporate entities are doing to achieve sustainability. By

replicating the competitors' strategies and decisions, the organization assumes success and

legitimacy within the community and general society of long-run sustainability.

CONTEMPORARY ACCOUNTING THEORY 9

PART B: APPLICATION OF THEORETICAL KNOWLEDGE

iv). Company overview

Established in 2007, crown Resort Company limited is an Australian gaming and

entertainment business entity. The decision to divest by the publishing and broadcasting Limited

(PBL) was a major milestone for the birth of crown Resort Company limited. Crown resort has

several investments in various countries and regions. Among such countries includes Australia,

the United Kingdom, Asia and the United States of America. Within Australia, the crown resort

operates a maximum of four segments. These include crown Melbourne, crown Perth, Aspinall's

and wagering and online. The company is a public entity that is listed on the Australian stock

exchange market under the code (CWN.AX). The company has also established headquarters at

Southbank, Melbourne, Australia (Villiers and Maroon, 2017).

Since the company is listed on the Australian stock market, it is, therefore, run on a

shareholder ownership structure. (Tavares and Dias, 2018). More evidently, crown resort

limited is known to be owned by around eight institutional investors and other investors. Among

these shareholders, and investors include the individual investors, mutual funds, hedge funds,

institutions and so on.

The company governance is operated by the board of directors whose primary re is to

formulate strategic directions of the company (Gnanaweera and Kunori, 2017). This is in line

with the ASX corporate governance council and to further ease operations the board is also

assisted by several committees. Among such committees includes the audit and corporate

governance committee, corporate responsibility committee and many others (Crown Resorts,

2019).

PART B: APPLICATION OF THEORETICAL KNOWLEDGE

iv). Company overview

Established in 2007, crown Resort Company limited is an Australian gaming and

entertainment business entity. The decision to divest by the publishing and broadcasting Limited

(PBL) was a major milestone for the birth of crown Resort Company limited. Crown resort has

several investments in various countries and regions. Among such countries includes Australia,

the United Kingdom, Asia and the United States of America. Within Australia, the crown resort

operates a maximum of four segments. These include crown Melbourne, crown Perth, Aspinall's

and wagering and online. The company is a public entity that is listed on the Australian stock

exchange market under the code (CWN.AX). The company has also established headquarters at

Southbank, Melbourne, Australia (Villiers and Maroon, 2017).

Since the company is listed on the Australian stock market, it is, therefore, run on a

shareholder ownership structure. (Tavares and Dias, 2018). More evidently, crown resort

limited is known to be owned by around eight institutional investors and other investors. Among

these shareholders, and investors include the individual investors, mutual funds, hedge funds,

institutions and so on.

The company governance is operated by the board of directors whose primary re is to

formulate strategic directions of the company (Gnanaweera and Kunori, 2017). This is in line

with the ASX corporate governance council and to further ease operations the board is also

assisted by several committees. Among such committees includes the audit and corporate

governance committee, corporate responsibility committee and many others (Crown Resorts,

2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 10

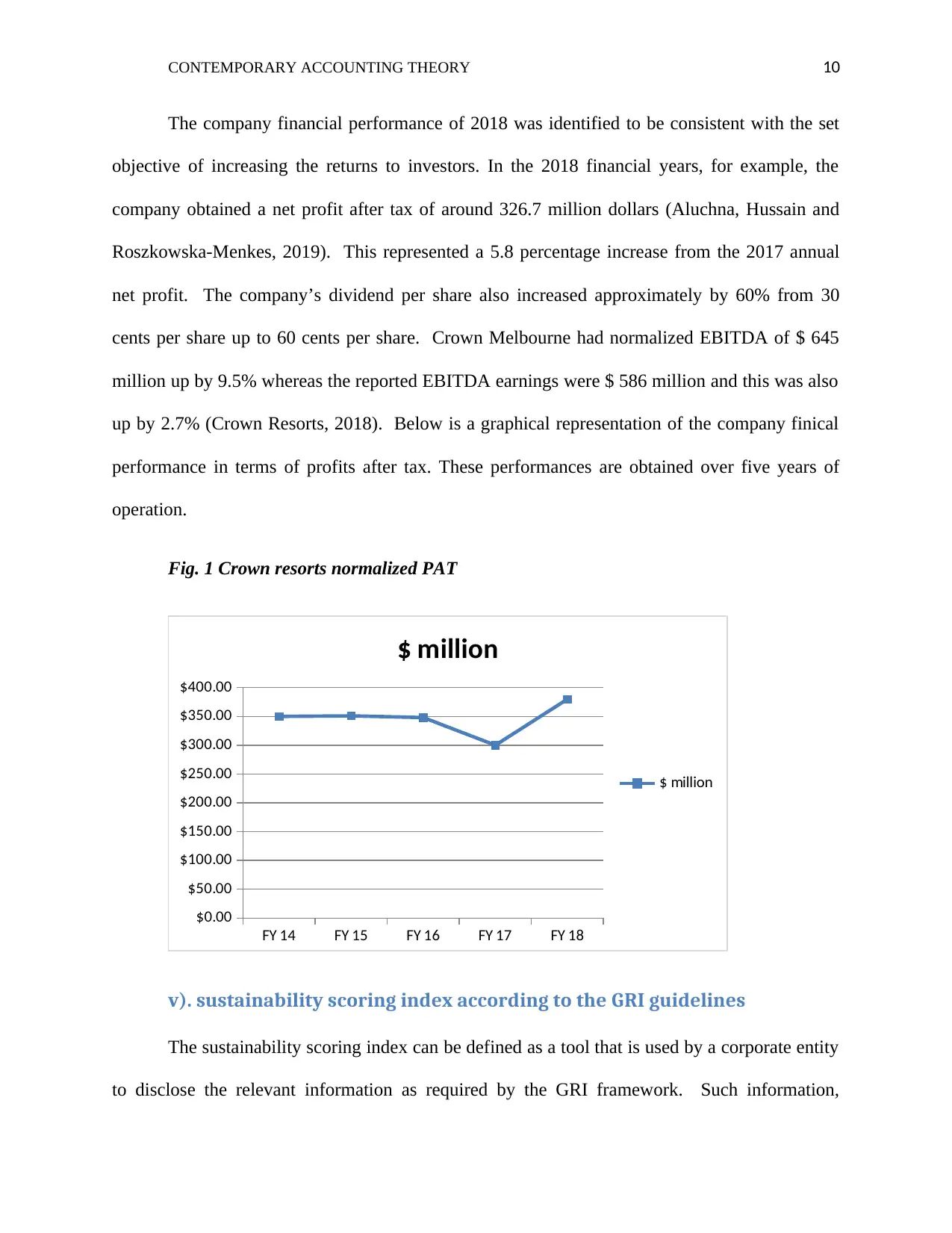

The company financial performance of 2018 was identified to be consistent with the set

objective of increasing the returns to investors. In the 2018 financial years, for example, the

company obtained a net profit after tax of around 326.7 million dollars (Aluchna, Hussain and

Roszkowska-Menkes, 2019). This represented a 5.8 percentage increase from the 2017 annual

net profit. The company’s dividend per share also increased approximately by 60% from 30

cents per share up to 60 cents per share. Crown Melbourne had normalized EBITDA of $ 645

million up by 9.5% whereas the reported EBITDA earnings were $ 586 million and this was also

up by 2.7% (Crown Resorts, 2018). Below is a graphical representation of the company finical

performance in terms of profits after tax. These performances are obtained over five years of

operation.

Fig. 1 Crown resorts normalized PAT

FY 14 FY 15 FY 16 FY 17 FY 18

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$ million

$ million

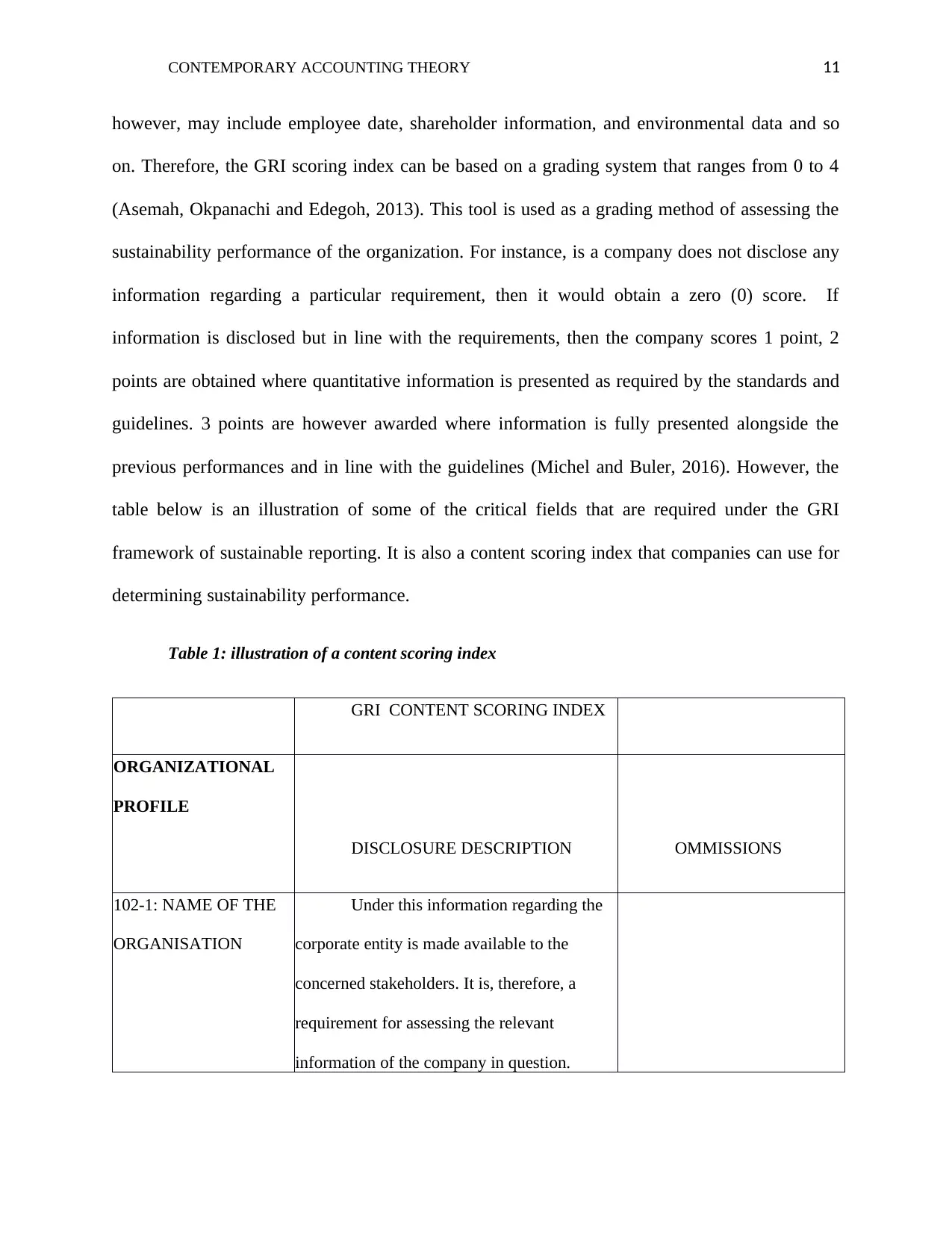

v). sustainability scoring index according to the GRI guidelines

The sustainability scoring index can be defined as a tool that is used by a corporate entity

to disclose the relevant information as required by the GRI framework. Such information,

The company financial performance of 2018 was identified to be consistent with the set

objective of increasing the returns to investors. In the 2018 financial years, for example, the

company obtained a net profit after tax of around 326.7 million dollars (Aluchna, Hussain and

Roszkowska-Menkes, 2019). This represented a 5.8 percentage increase from the 2017 annual

net profit. The company’s dividend per share also increased approximately by 60% from 30

cents per share up to 60 cents per share. Crown Melbourne had normalized EBITDA of $ 645

million up by 9.5% whereas the reported EBITDA earnings were $ 586 million and this was also

up by 2.7% (Crown Resorts, 2018). Below is a graphical representation of the company finical

performance in terms of profits after tax. These performances are obtained over five years of

operation.

Fig. 1 Crown resorts normalized PAT

FY 14 FY 15 FY 16 FY 17 FY 18

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$ million

$ million

v). sustainability scoring index according to the GRI guidelines

The sustainability scoring index can be defined as a tool that is used by a corporate entity

to disclose the relevant information as required by the GRI framework. Such information,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 11

however, may include employee date, shareholder information, and environmental data and so

on. Therefore, the GRI scoring index can be based on a grading system that ranges from 0 to 4

(Asemah, Okpanachi and Edegoh, 2013). This tool is used as a grading method of assessing the

sustainability performance of the organization. For instance, is a company does not disclose any

information regarding a particular requirement, then it would obtain a zero (0) score. If

information is disclosed but in line with the requirements, then the company scores 1 point, 2

points are obtained where quantitative information is presented as required by the standards and

guidelines. 3 points are however awarded where information is fully presented alongside the

previous performances and in line with the guidelines (Michel and Buler, 2016). However, the

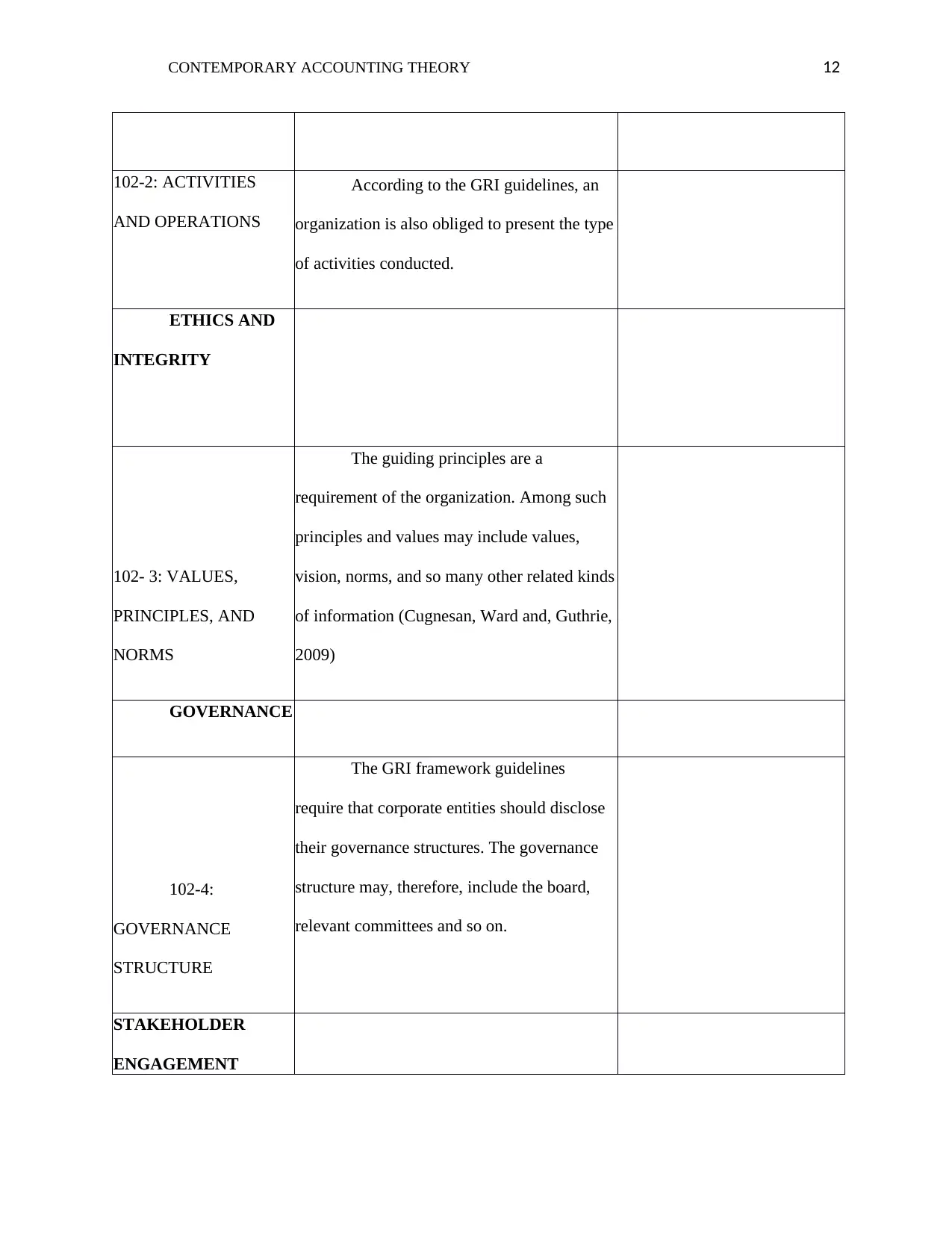

table below is an illustration of some of the critical fields that are required under the GRI

framework of sustainable reporting. It is also a content scoring index that companies can use for

determining sustainability performance.

Table 1: illustration of a content scoring index

GRI CONTENT SCORING INDEX

ORGANIZATIONAL

PROFILE

DISCLOSURE DESCRIPTION OMMISSIONS

102-1: NAME OF THE

ORGANISATION

Under this information regarding the

corporate entity is made available to the

concerned stakeholders. It is, therefore, a

requirement for assessing the relevant

information of the company in question.

however, may include employee date, shareholder information, and environmental data and so

on. Therefore, the GRI scoring index can be based on a grading system that ranges from 0 to 4

(Asemah, Okpanachi and Edegoh, 2013). This tool is used as a grading method of assessing the

sustainability performance of the organization. For instance, is a company does not disclose any

information regarding a particular requirement, then it would obtain a zero (0) score. If

information is disclosed but in line with the requirements, then the company scores 1 point, 2

points are obtained where quantitative information is presented as required by the standards and

guidelines. 3 points are however awarded where information is fully presented alongside the

previous performances and in line with the guidelines (Michel and Buler, 2016). However, the

table below is an illustration of some of the critical fields that are required under the GRI

framework of sustainable reporting. It is also a content scoring index that companies can use for

determining sustainability performance.

Table 1: illustration of a content scoring index

GRI CONTENT SCORING INDEX

ORGANIZATIONAL

PROFILE

DISCLOSURE DESCRIPTION OMMISSIONS

102-1: NAME OF THE

ORGANISATION

Under this information regarding the

corporate entity is made available to the

concerned stakeholders. It is, therefore, a

requirement for assessing the relevant

information of the company in question.

CONTEMPORARY ACCOUNTING THEORY 12

102-2: ACTIVITIES

AND OPERATIONS

According to the GRI guidelines, an

organization is also obliged to present the type

of activities conducted.

ETHICS AND

INTEGRITY

102- 3: VALUES,

PRINCIPLES, AND

NORMS

The guiding principles are a

requirement of the organization. Among such

principles and values may include values,

vision, norms, and so many other related kinds

of information (Cugnesan, Ward and, Guthrie,

2009)

GOVERNANCE

102-4:

GOVERNANCE

STRUCTURE

The GRI framework guidelines

require that corporate entities should disclose

their governance structures. The governance

structure may, therefore, include the board,

relevant committees and so on.

STAKEHOLDER

ENGAGEMENT

102-2: ACTIVITIES

AND OPERATIONS

According to the GRI guidelines, an

organization is also obliged to present the type

of activities conducted.

ETHICS AND

INTEGRITY

102- 3: VALUES,

PRINCIPLES, AND

NORMS

The guiding principles are a

requirement of the organization. Among such

principles and values may include values,

vision, norms, and so many other related kinds

of information (Cugnesan, Ward and, Guthrie,

2009)

GOVERNANCE

102-4:

GOVERNANCE

STRUCTURE

The GRI framework guidelines

require that corporate entities should disclose

their governance structures. The governance

structure may, therefore, include the board,

relevant committees and so on.

STAKEHOLDER

ENGAGEMENT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.