Crunchy Chips: Analyzing Financial Viability Using CVP and Breakeven

VerifiedAdded on 2020/02/24

|4

|849

|130

Homework Assignment

AI Summary

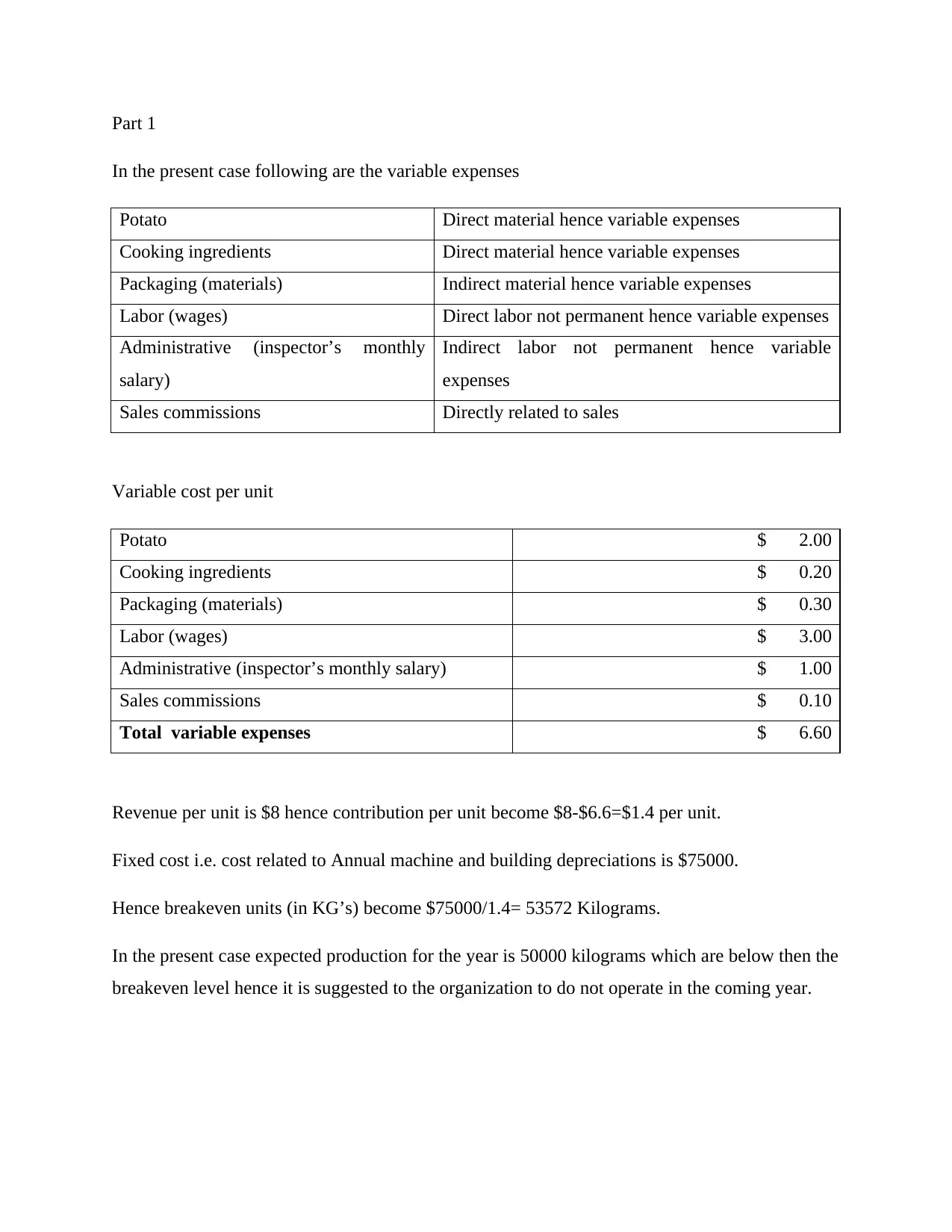

This assignment analyzes the financial viability of Crunchy Chips, focusing on breakeven and cost-volume-profit (CVP) analysis. Part 1 calculates variable and fixed costs, determines the breakeven point (53,572 kg), and recommends against operating in the coming year due to expected production being below the breakeven level. Part 2 explains CVP analysis, emphasizing the importance of sales volume exceeding the breakeven point for profitability and highlighting the assumptions of constant fixed cost, variable cost per unit, and sales price per unit. Part 3 provides a memo advising Jerahm and Angel on reducing operating losses by either reducing variable costs or increasing sales volume, as the current cost structure, with mainly variable costs, limits the ability to offset fixed costs. The analysis suggests that the company should focus on strategies to improve profitability through either cost reduction or increased sales.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.