Case Study: Accounting for Decision Making at Crystal Hotel Pty Ltd

VerifiedAdded on 2020/02/19

|13

|2144

|42

Case Study

AI Summary

This case study examines Crystal Hotel Pty Ltd's financial decision-making processes, focusing on how the hotel manages expenses through budgeting, buy-or-rent decisions, and market analysis. The analysis covers two key scenarios: the Wellness Centre project and a promotional event. For the Wellness Centre, the study evaluates the cost-effectiveness of buying versus renting machinery and plants, considering factors like initial costs, ongoing expenses, and technological changes. The event analysis uses CVP analysis to determine contribution margins, break-even points, and the number of tickets needed to achieve target profits. The study highlights the importance of strategic financial planning and the use of tools like CVP analysis to optimize profitability and make informed decisions. The conclusion emphasizes the need for companies to carefully analyze various options and leverage available tools and techniques for effective financial management.

RUNNING HEAD: Accounting for decision making

1

Accounting for decision making

1

Accounting for decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for decision making 2

Contents

Case overview...................................................................................................................3

Task 1................................................................................................................................3

Task 2................................................................................................................................4

Task 3................................................................................................................................5

Task 4................................................................................................................................6

Task 1................................................................................................................................8

Task 2................................................................................................................................9

Task 3..............................................................................................................................10

Task 4..............................................................................................................................11

Conclusion......................................................................................................................12

References.......................................................................................................................13

Contents

Case overview...................................................................................................................3

Task 1................................................................................................................................3

Task 2................................................................................................................................4

Task 3................................................................................................................................5

Task 4................................................................................................................................6

Task 1................................................................................................................................8

Task 2................................................................................................................................9

Task 3..............................................................................................................................10

Task 4..............................................................................................................................11

Conclusion......................................................................................................................12

References.......................................................................................................................13

Accounting for decision making 3

Case overview:

In this case, Crystal Hotel Pty ltd has been studied and it has been found that how this

hotel manages every expense according to the budget and many cases of the company have

been resolved on the basis of budgets, buy or rent decision, market analysis etc. in this case,

many issues which has been faced by the company have been resolved and it has also been

described that which option is useful for a company at which time.

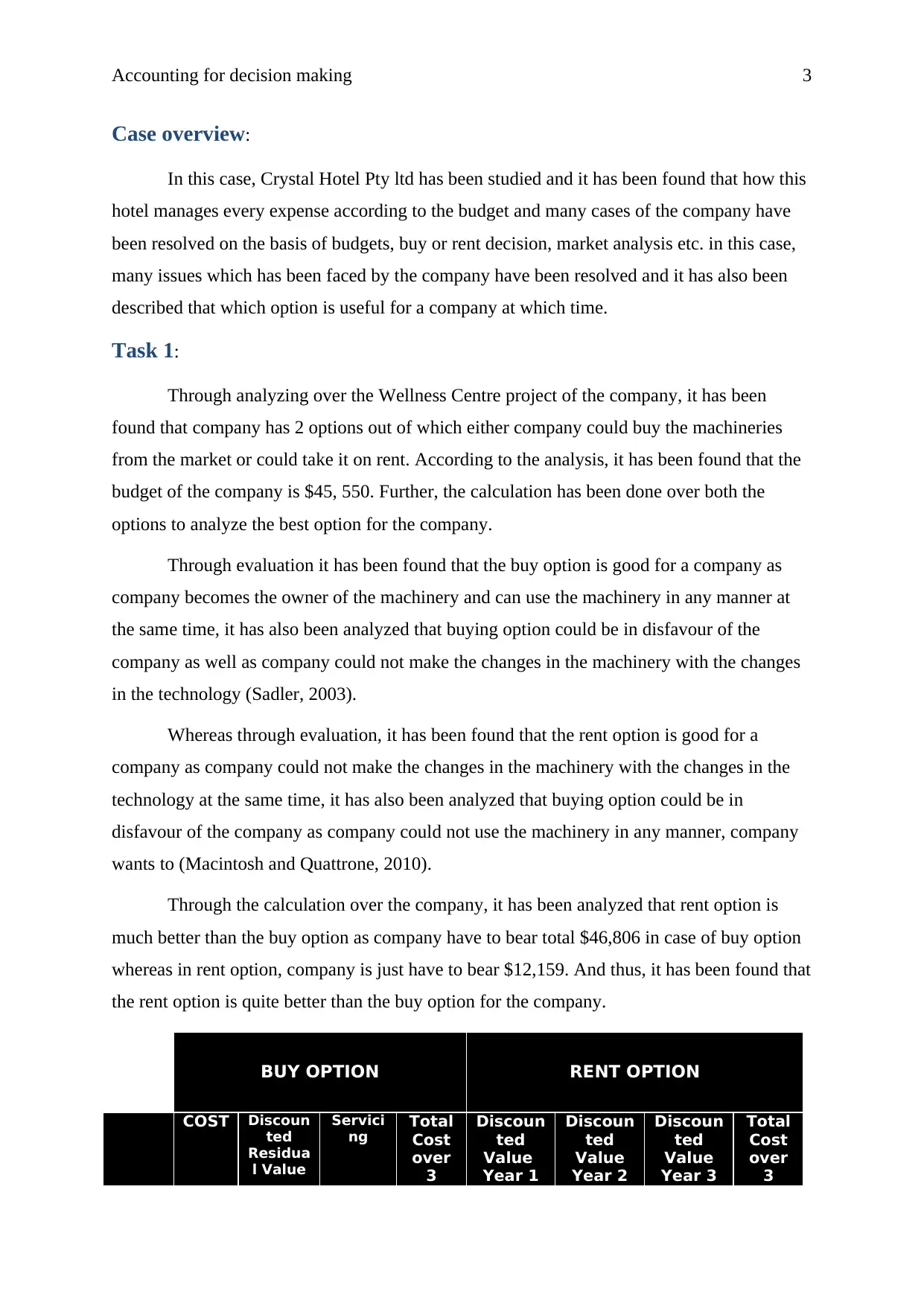

Task 1:

Through analyzing over the Wellness Centre project of the company, it has been

found that company has 2 options out of which either company could buy the machineries

from the market or could take it on rent. According to the analysis, it has been found that the

budget of the company is $45, 550. Further, the calculation has been done over both the

options to analyze the best option for the company.

Through evaluation it has been found that the buy option is good for a company as

company becomes the owner of the machinery and can use the machinery in any manner at

the same time, it has also been analyzed that buying option could be in disfavour of the

company as well as company could not make the changes in the machinery with the changes

in the technology (Sadler, 2003).

Whereas through evaluation, it has been found that the rent option is good for a

company as company could not make the changes in the machinery with the changes in the

technology at the same time, it has also been analyzed that buying option could be in

disfavour of the company as company could not use the machinery in any manner, company

wants to (Macintosh and Quattrone, 2010).

Through the calculation over the company, it has been analyzed that rent option is

much better than the buy option as company have to bear total $46,806 in case of buy option

whereas in rent option, company is just have to bear $12,159. And thus, it has been found that

the rent option is quite better than the buy option for the company.

BUY OPTION RENT OPTION

COST Discoun

ted

Residua

l Value

Servici

ng

Total

Cost

over

3

Discoun

ted

Value

Year 1

Discoun

ted

Value

Year 2

Discoun

ted

Value

Year 3

Total

Cost

over

3

Case overview:

In this case, Crystal Hotel Pty ltd has been studied and it has been found that how this

hotel manages every expense according to the budget and many cases of the company have

been resolved on the basis of budgets, buy or rent decision, market analysis etc. in this case,

many issues which has been faced by the company have been resolved and it has also been

described that which option is useful for a company at which time.

Task 1:

Through analyzing over the Wellness Centre project of the company, it has been

found that company has 2 options out of which either company could buy the machineries

from the market or could take it on rent. According to the analysis, it has been found that the

budget of the company is $45, 550. Further, the calculation has been done over both the

options to analyze the best option for the company.

Through evaluation it has been found that the buy option is good for a company as

company becomes the owner of the machinery and can use the machinery in any manner at

the same time, it has also been analyzed that buying option could be in disfavour of the

company as well as company could not make the changes in the machinery with the changes

in the technology (Sadler, 2003).

Whereas through evaluation, it has been found that the rent option is good for a

company as company could not make the changes in the machinery with the changes in the

technology at the same time, it has also been analyzed that buying option could be in

disfavour of the company as company could not use the machinery in any manner, company

wants to (Macintosh and Quattrone, 2010).

Through the calculation over the company, it has been analyzed that rent option is

much better than the buy option as company have to bear total $46,806 in case of buy option

whereas in rent option, company is just have to bear $12,159. And thus, it has been found that

the rent option is quite better than the buy option for the company.

BUY OPTION RENT OPTION

COST Discoun

ted

Residua

l Value

Servici

ng

Total

Cost

over

3

Discoun

ted

Value

Year 1

Discoun

ted

Value

Year 2

Discoun

ted

Value

Year 3

Total

Cost

over

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for decision making 4

years years

Tread

mill (3

pieces

)

$18,1

71 $721 $1,546.

26

$18,9

96 $1,824 $1,740 $1,659 $5,22

3

Ellip

tical

Traine

r (2

pieces

)

$8,07

8 $321 $1,546.

26

$9,30

4 $935 $892 $851 $2,67

8

Exer

cise

Bike

(4

pieces

)

$13,3

28 $529 $1,546.

26

$14,3

45 $837 $798 $761 $2,39

7

Rowi

ng

Machi

ne (1

piece)

$2,72

3 $108 $1,546.

26

$4,16

1 $776 $740 $706 $2,22

2

TOTA

L

COST

$46,8

06

$12,5

19

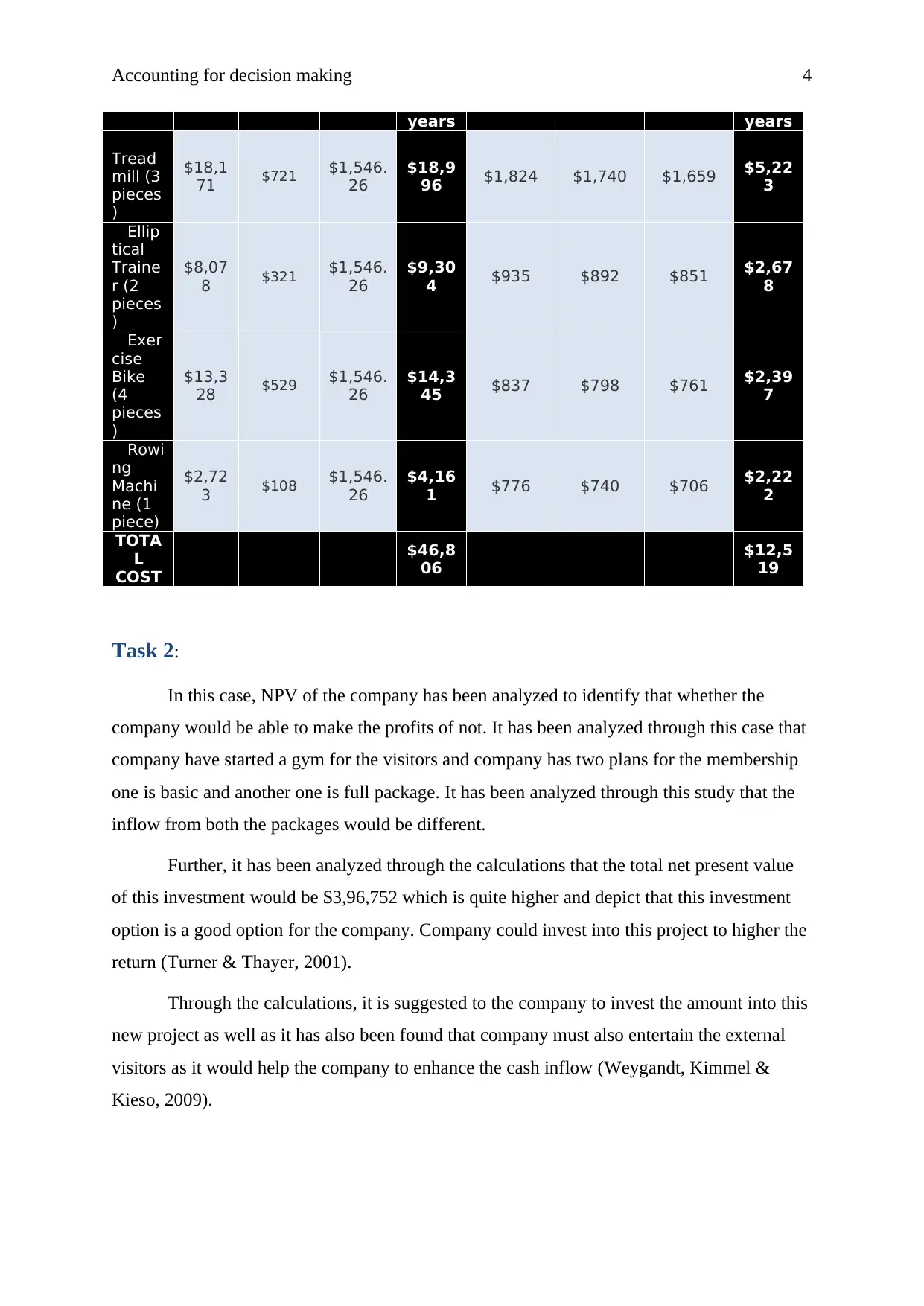

Task 2:

In this case, NPV of the company has been analyzed to identify that whether the

company would be able to make the profits of not. It has been analyzed through this case that

company have started a gym for the visitors and company has two plans for the membership

one is basic and another one is full package. It has been analyzed through this study that the

inflow from both the packages would be different.

Further, it has been analyzed through the calculations that the total net present value

of this investment would be $3,96,752 which is quite higher and depict that this investment

option is a good option for the company. Company could invest into this project to higher the

return (Turner & Thayer, 2001).

Through the calculations, it is suggested to the company to invest the amount into this

new project as well as it has also been found that company must also entertain the external

visitors as it would help the company to enhance the cash inflow (Weygandt, Kimmel &

Kieso, 2009).

years years

Tread

mill (3

pieces

)

$18,1

71 $721 $1,546.

26

$18,9

96 $1,824 $1,740 $1,659 $5,22

3

Ellip

tical

Traine

r (2

pieces

)

$8,07

8 $321 $1,546.

26

$9,30

4 $935 $892 $851 $2,67

8

Exer

cise

Bike

(4

pieces

)

$13,3

28 $529 $1,546.

26

$14,3

45 $837 $798 $761 $2,39

7

Rowi

ng

Machi

ne (1

piece)

$2,72

3 $108 $1,546.

26

$4,16

1 $776 $740 $706 $2,22

2

TOTA

L

COST

$46,8

06

$12,5

19

Task 2:

In this case, NPV of the company has been analyzed to identify that whether the

company would be able to make the profits of not. It has been analyzed through this case that

company have started a gym for the visitors and company has two plans for the membership

one is basic and another one is full package. It has been analyzed through this study that the

inflow from both the packages would be different.

Further, it has been analyzed through the calculations that the total net present value

of this investment would be $3,96,752 which is quite higher and depict that this investment

option is a good option for the company. Company could invest into this project to higher the

return (Turner & Thayer, 2001).

Through the calculations, it is suggested to the company to invest the amount into this

new project as well as it has also been found that company must also entertain the external

visitors as it would help the company to enhance the cash inflow (Weygandt, Kimmel &

Kieso, 2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for decision making 5

Membership (Basic 40/month, Full

Package 81/month)

Member

ship

Project

Cash Outflow Cash Inflow

Net

Cash

Flow

Tax

After

Tax

CF

PV

Factor NPV

Year 0 $35,350

-

$35,3

50

-

$10,

605

-

$24,7

45

1 -

24,745

Year 1 $808 $2,22,200 $2,21,

392

$66,

418

$1,54

,974

0.9259

25926 1,43,4

95

Year 2 $808 $2,34,804 $2,33,

996

$70,

199

$1,63

,797

0.8573

3882 1,40,4

30

Year 3 $808 $2,48,382 $2,47,

574

$74,

272

$1,73

,302

0.7938

32241 1,37,5

72

NPV $3,96

,752

Task 3:

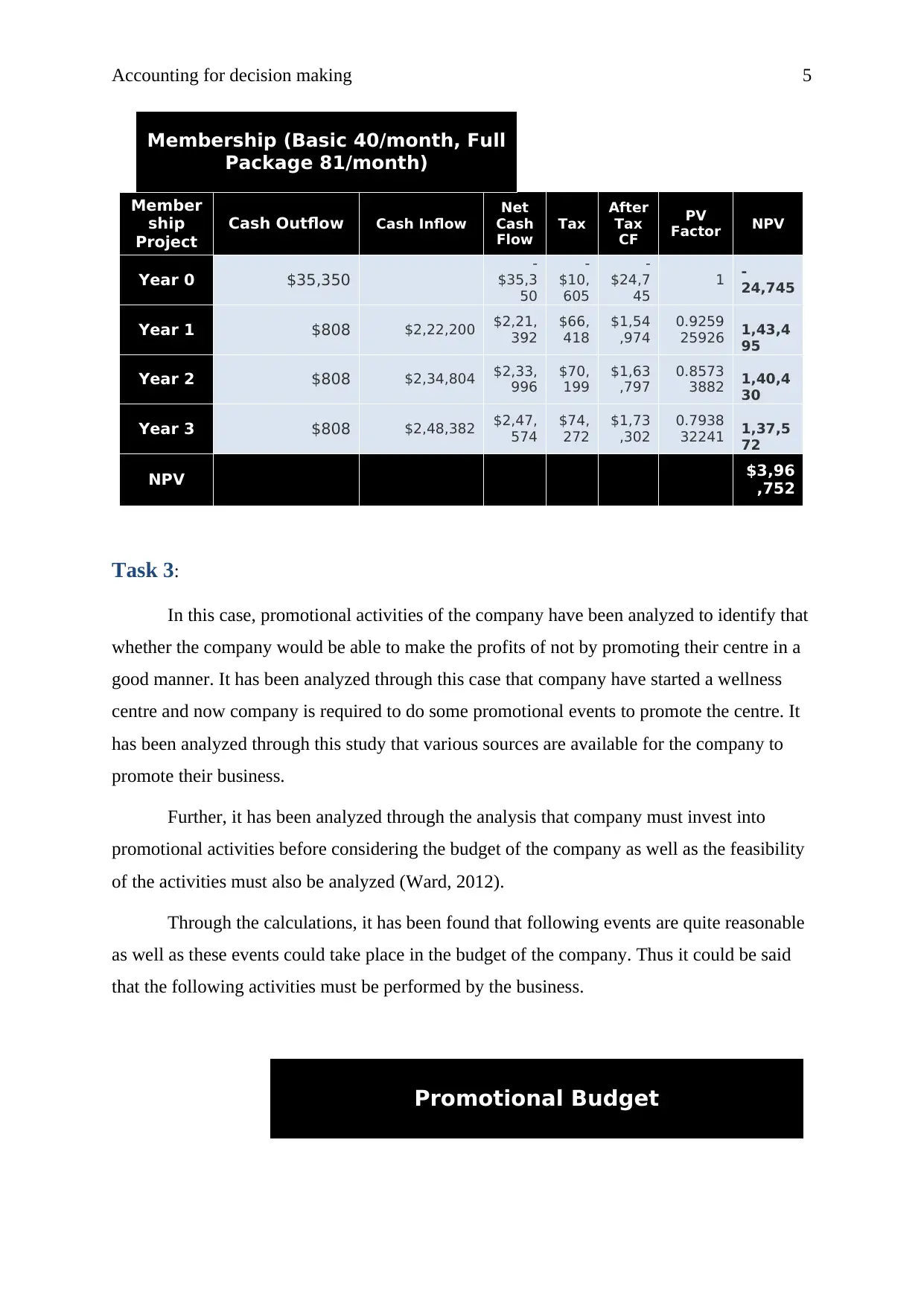

In this case, promotional activities of the company have been analyzed to identify that

whether the company would be able to make the profits of not by promoting their centre in a

good manner. It has been analyzed through this case that company have started a wellness

centre and now company is required to do some promotional events to promote the centre. It

has been analyzed through this study that various sources are available for the company to

promote their business.

Further, it has been analyzed through the analysis that company must invest into

promotional activities before considering the budget of the company as well as the feasibility

of the activities must also be analyzed (Ward, 2012).

Through the calculations, it has been found that following events are quite reasonable

as well as these events could take place in the budget of the company. Thus it could be said

that the following activities must be performed by the business.

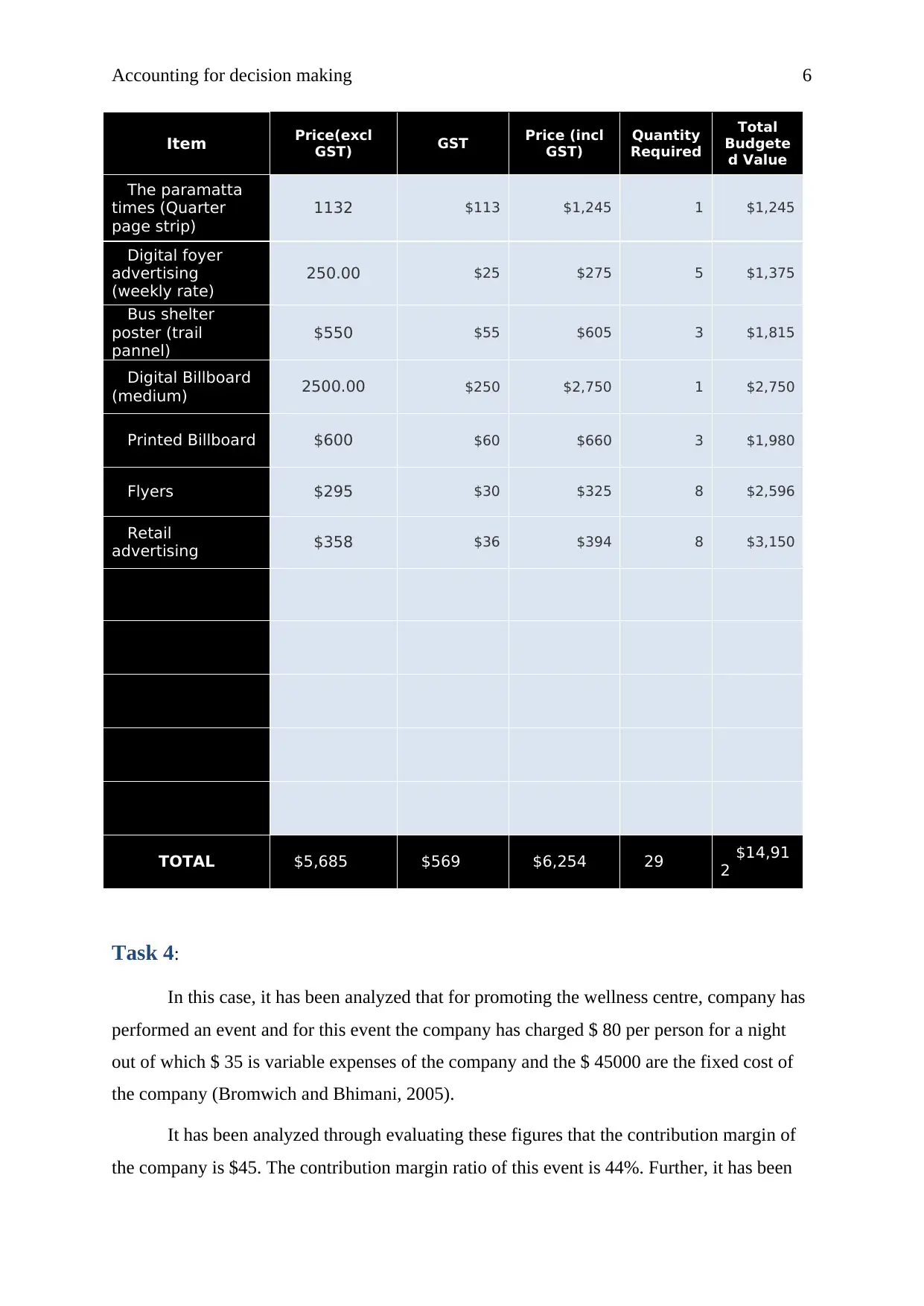

Promotional Budget

Membership (Basic 40/month, Full

Package 81/month)

Member

ship

Project

Cash Outflow Cash Inflow

Net

Cash

Flow

Tax

After

Tax

CF

PV

Factor NPV

Year 0 $35,350

-

$35,3

50

-

$10,

605

-

$24,7

45

1 -

24,745

Year 1 $808 $2,22,200 $2,21,

392

$66,

418

$1,54

,974

0.9259

25926 1,43,4

95

Year 2 $808 $2,34,804 $2,33,

996

$70,

199

$1,63

,797

0.8573

3882 1,40,4

30

Year 3 $808 $2,48,382 $2,47,

574

$74,

272

$1,73

,302

0.7938

32241 1,37,5

72

NPV $3,96

,752

Task 3:

In this case, promotional activities of the company have been analyzed to identify that

whether the company would be able to make the profits of not by promoting their centre in a

good manner. It has been analyzed through this case that company have started a wellness

centre and now company is required to do some promotional events to promote the centre. It

has been analyzed through this study that various sources are available for the company to

promote their business.

Further, it has been analyzed through the analysis that company must invest into

promotional activities before considering the budget of the company as well as the feasibility

of the activities must also be analyzed (Ward, 2012).

Through the calculations, it has been found that following events are quite reasonable

as well as these events could take place in the budget of the company. Thus it could be said

that the following activities must be performed by the business.

Promotional Budget

Accounting for decision making 6

Item Price(excl

GST) GST Price (incl

GST)

Quantity

Required

Total

Budgete

d Value

The paramatta

times (Quarter

page strip)

1132 $113 $1,245 1 $1,245

Digital foyer

advertising

(weekly rate)

250.00 $25 $275 5 $1,375

Bus shelter

poster (trail

pannel)

$550 $55 $605 3 $1,815

Digital Billboard

(medium) 2500.00 $250 $2,750 1 $2,750

Printed Billboard $600 $60 $660 3 $1,980

Flyers $295 $30 $325 8 $2,596

Retail

advertising $358 $36 $394 8 $3,150

TOTAL $5,685 $569 $6,254 29 $14,91

2

Task 4:

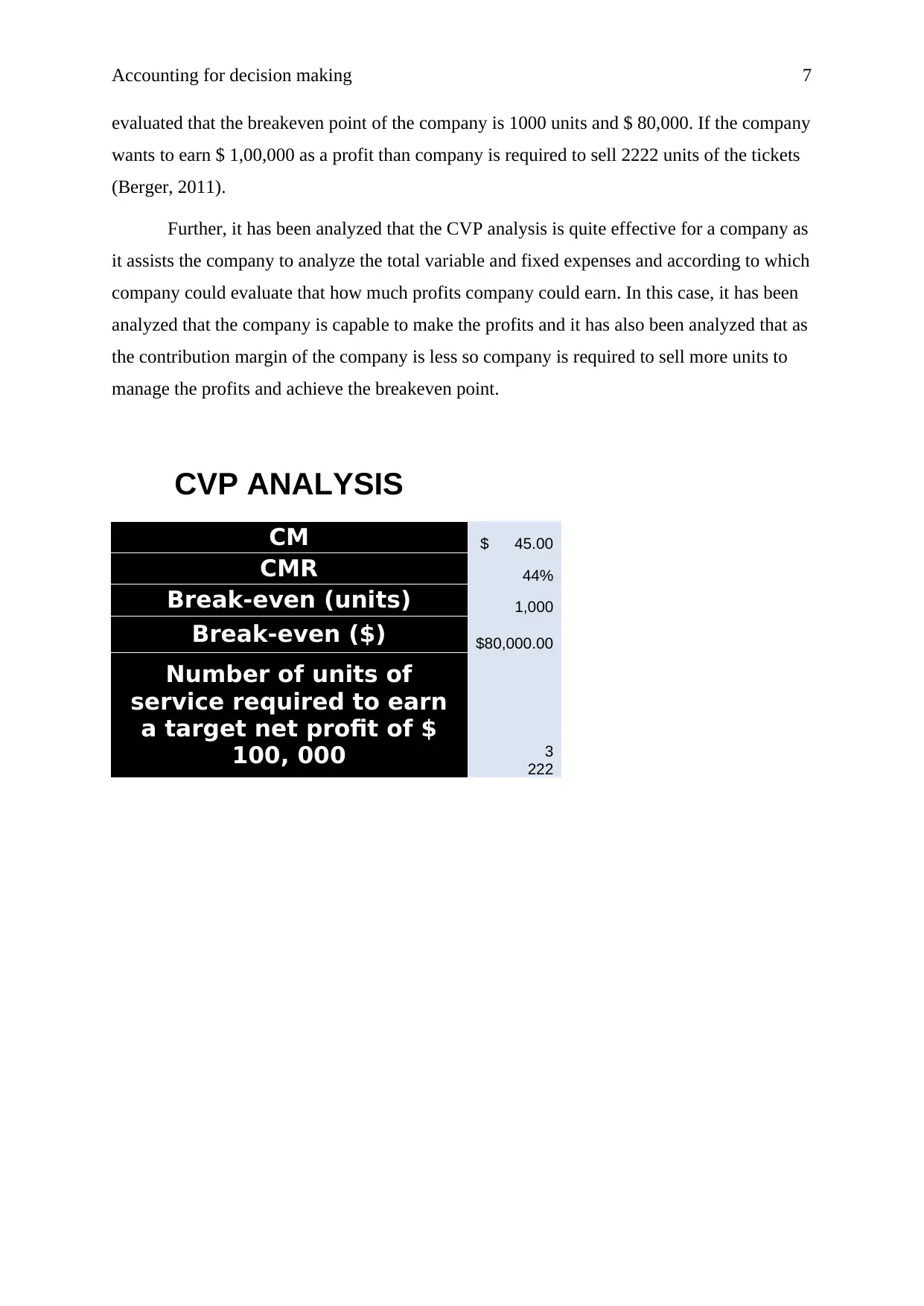

In this case, it has been analyzed that for promoting the wellness centre, company has

performed an event and for this event the company has charged $ 80 per person for a night

out of which $ 35 is variable expenses of the company and the $ 45000 are the fixed cost of

the company (Bromwich and Bhimani, 2005).

It has been analyzed through evaluating these figures that the contribution margin of

the company is $45. The contribution margin ratio of this event is 44%. Further, it has been

Item Price(excl

GST) GST Price (incl

GST)

Quantity

Required

Total

Budgete

d Value

The paramatta

times (Quarter

page strip)

1132 $113 $1,245 1 $1,245

Digital foyer

advertising

(weekly rate)

250.00 $25 $275 5 $1,375

Bus shelter

poster (trail

pannel)

$550 $55 $605 3 $1,815

Digital Billboard

(medium) 2500.00 $250 $2,750 1 $2,750

Printed Billboard $600 $60 $660 3 $1,980

Flyers $295 $30 $325 8 $2,596

Retail

advertising $358 $36 $394 8 $3,150

TOTAL $5,685 $569 $6,254 29 $14,91

2

Task 4:

In this case, it has been analyzed that for promoting the wellness centre, company has

performed an event and for this event the company has charged $ 80 per person for a night

out of which $ 35 is variable expenses of the company and the $ 45000 are the fixed cost of

the company (Bromwich and Bhimani, 2005).

It has been analyzed through evaluating these figures that the contribution margin of

the company is $45. The contribution margin ratio of this event is 44%. Further, it has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for decision making 7

evaluated that the breakeven point of the company is 1000 units and $ 80,000. If the company

wants to earn $ 1,00,000 as a profit than company is required to sell 2222 units of the tickets

(Berger, 2011).

Further, it has been analyzed that the CVP analysis is quite effective for a company as

it assists the company to analyze the total variable and fixed expenses and according to which

company could evaluate that how much profits company could earn. In this case, it has been

analyzed that the company is capable to make the profits and it has also been analyzed that as

the contribution margin of the company is less so company is required to sell more units to

manage the profits and achieve the breakeven point.

CVP ANALYSIS

CM $ 45.00

CMR 44%

Break-even (units) 1,000

Break-even ($) $80,000.00

Number of units of

service required to earn

a target net profit of $

100, 000 3

222

evaluated that the breakeven point of the company is 1000 units and $ 80,000. If the company

wants to earn $ 1,00,000 as a profit than company is required to sell 2222 units of the tickets

(Berger, 2011).

Further, it has been analyzed that the CVP analysis is quite effective for a company as

it assists the company to analyze the total variable and fixed expenses and according to which

company could evaluate that how much profits company could earn. In this case, it has been

analyzed that the company is capable to make the profits and it has also been analyzed that as

the contribution margin of the company is less so company is required to sell more units to

manage the profits and achieve the breakeven point.

CVP ANALYSIS

CM $ 45.00

CMR 44%

Break-even (units) 1,000

Break-even ($) $80,000.00

Number of units of

service required to earn

a target net profit of $

100, 000 3

222

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for decision making 8

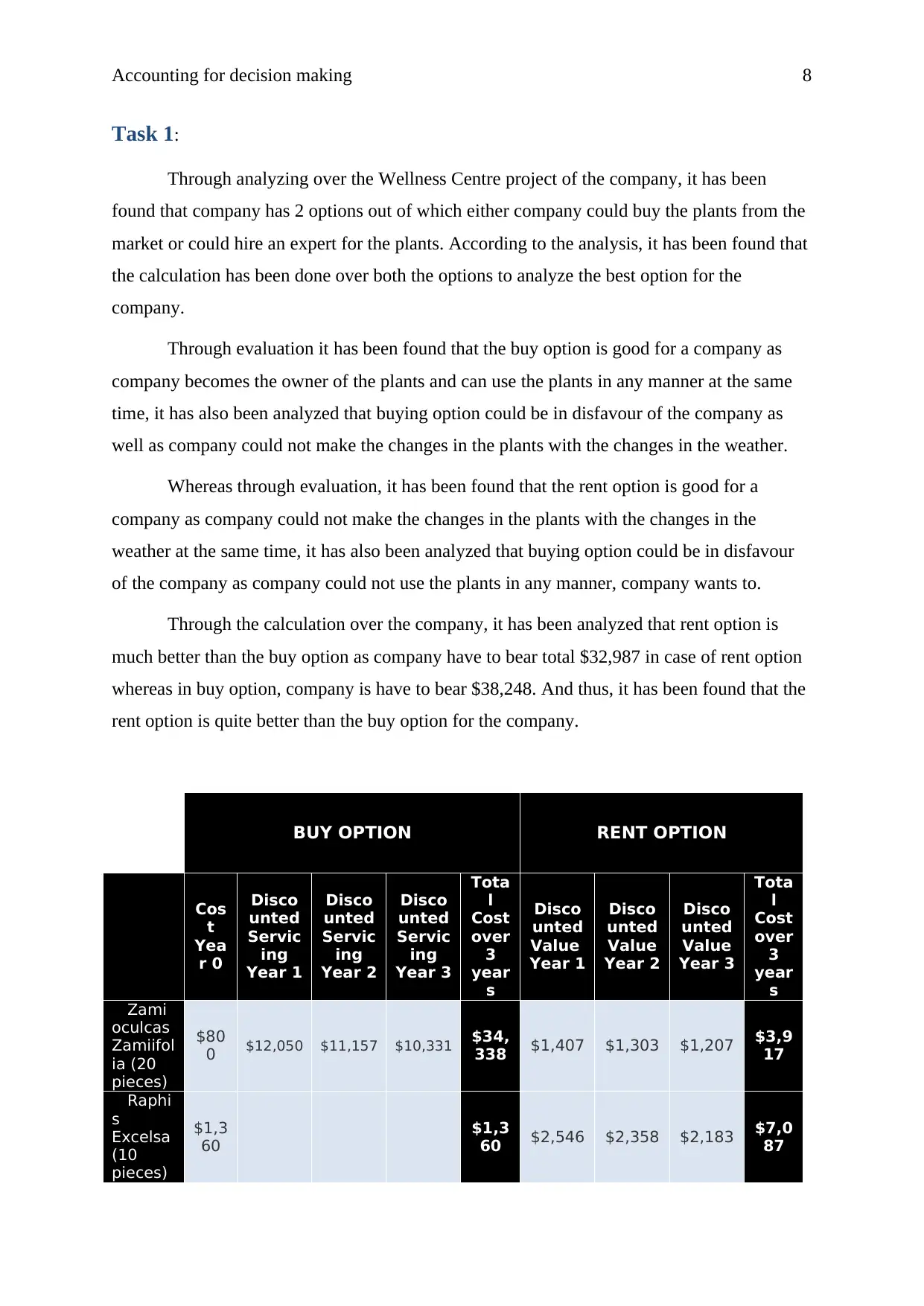

Task 1:

Through analyzing over the Wellness Centre project of the company, it has been

found that company has 2 options out of which either company could buy the plants from the

market or could hire an expert for the plants. According to the analysis, it has been found that

the calculation has been done over both the options to analyze the best option for the

company.

Through evaluation it has been found that the buy option is good for a company as

company becomes the owner of the plants and can use the plants in any manner at the same

time, it has also been analyzed that buying option could be in disfavour of the company as

well as company could not make the changes in the plants with the changes in the weather.

Whereas through evaluation, it has been found that the rent option is good for a

company as company could not make the changes in the plants with the changes in the

weather at the same time, it has also been analyzed that buying option could be in disfavour

of the company as company could not use the plants in any manner, company wants to.

Through the calculation over the company, it has been analyzed that rent option is

much better than the buy option as company have to bear total $32,987 in case of rent option

whereas in buy option, company is have to bear $38,248. And thus, it has been found that the

rent option is quite better than the buy option for the company.

BUY OPTION RENT OPTION

Cos

t

Yea

r 0

Disco

unted

Servic

ing

Year 1

Disco

unted

Servic

ing

Year 2

Disco

unted

Servic

ing

Year 3

Tota

l

Cost

over

3

year

s

Disco

unted

Value

Year 1

Disco

unted

Value

Year 2

Disco

unted

Value

Year 3

Tota

l

Cost

over

3

year

s

Zami

oculcas

Zamiifol

ia (20

pieces)

$80

0 $12,050 $11,157 $10,331 $34,

338 $1,407 $1,303 $1,207 $3,9

17

Raphi

s

Excelsa

(10

pieces)

$1,3

60

$1,3

60 $2,546 $2,358 $2,183 $7,0

87

Task 1:

Through analyzing over the Wellness Centre project of the company, it has been

found that company has 2 options out of which either company could buy the plants from the

market or could hire an expert for the plants. According to the analysis, it has been found that

the calculation has been done over both the options to analyze the best option for the

company.

Through evaluation it has been found that the buy option is good for a company as

company becomes the owner of the plants and can use the plants in any manner at the same

time, it has also been analyzed that buying option could be in disfavour of the company as

well as company could not make the changes in the plants with the changes in the weather.

Whereas through evaluation, it has been found that the rent option is good for a

company as company could not make the changes in the plants with the changes in the

weather at the same time, it has also been analyzed that buying option could be in disfavour

of the company as company could not use the plants in any manner, company wants to.

Through the calculation over the company, it has been analyzed that rent option is

much better than the buy option as company have to bear total $32,987 in case of rent option

whereas in buy option, company is have to bear $38,248. And thus, it has been found that the

rent option is quite better than the buy option for the company.

BUY OPTION RENT OPTION

Cos

t

Yea

r 0

Disco

unted

Servic

ing

Year 1

Disco

unted

Servic

ing

Year 2

Disco

unted

Servic

ing

Year 3

Tota

l

Cost

over

3

year

s

Disco

unted

Value

Year 1

Disco

unted

Value

Year 2

Disco

unted

Value

Year 3

Tota

l

Cost

over

3

year

s

Zami

oculcas

Zamiifol

ia (20

pieces)

$80

0 $12,050 $11,157 $10,331 $34,

338 $1,407 $1,303 $1,207 $3,9

17

Raphi

s

Excelsa

(10

pieces)

$1,3

60

$1,3

60 $2,546 $2,358 $2,183 $7,0

87

Accounting for decision making 9

Howe

a

Forsteri

ana (10

pieces)

$57

0

$57

0 $1,843 $1,706 $1,580 $5,1

28

Cham

aedorea

Elegans

(30

pieces)

$1,9

80

$1,9

80 $5,607 $6,056 $5,192 $16,

854

TOTAL $4,

710

$12,0

50

$11,1

57

$10,3

31

$38,

248

$11,4

03

$11,4

22

$10,1

61

$32,

987

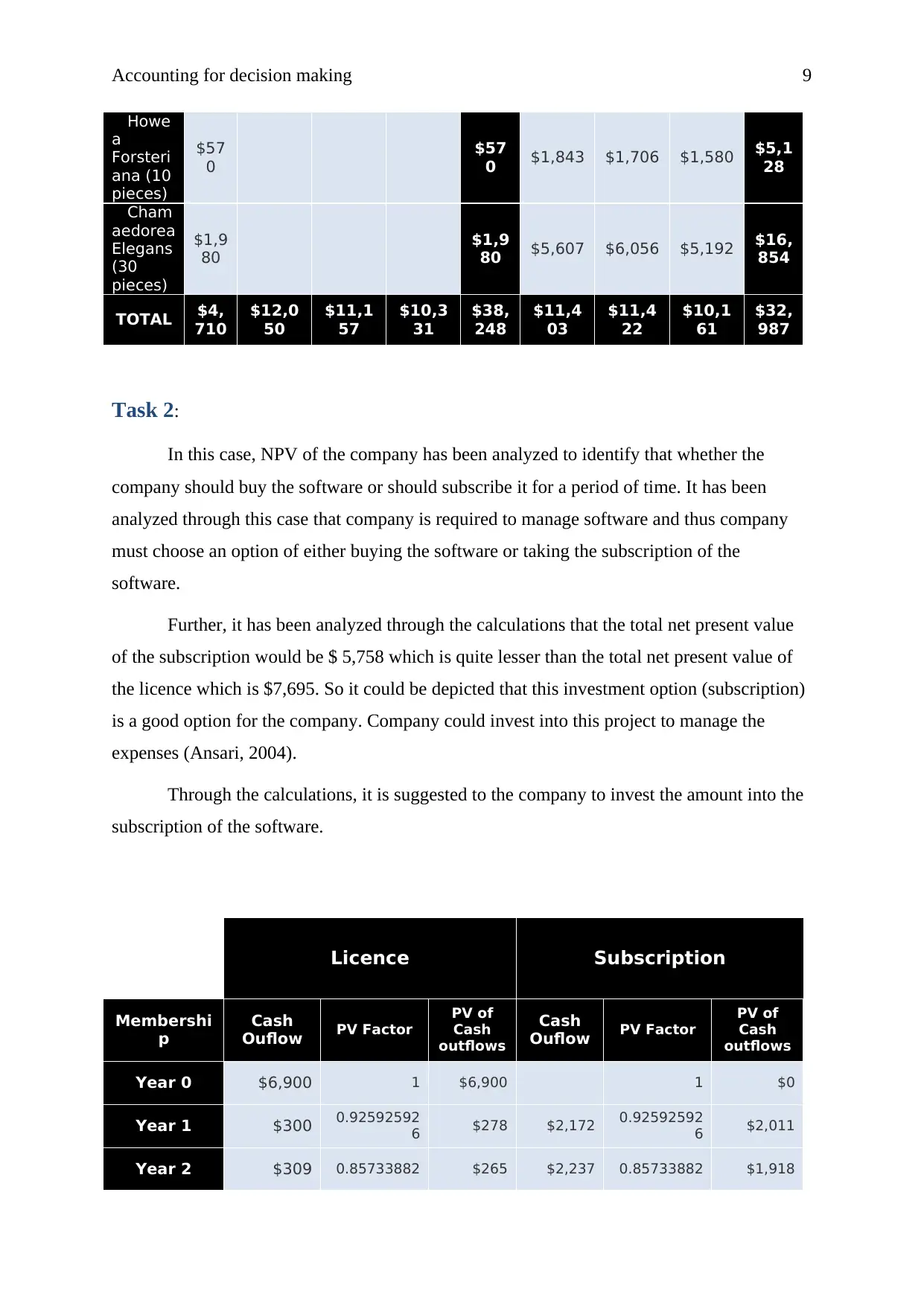

Task 2:

In this case, NPV of the company has been analyzed to identify that whether the

company should buy the software or should subscribe it for a period of time. It has been

analyzed through this case that company is required to manage software and thus company

must choose an option of either buying the software or taking the subscription of the

software.

Further, it has been analyzed through the calculations that the total net present value

of the subscription would be $ 5,758 which is quite lesser than the total net present value of

the licence which is $7,695. So it could be depicted that this investment option (subscription)

is a good option for the company. Company could invest into this project to manage the

expenses (Ansari, 2004).

Through the calculations, it is suggested to the company to invest the amount into the

subscription of the software.

Licence Subscription

Membershi

p

Cash

Ouflow PV Factor

PV of

Cash

outflows

Cash

Ouflow PV Factor

PV of

Cash

outflows

Year 0 $6,900 1 $6,900 1 $0

Year 1 $300 0.92592592

6 $278 $2,172 0.92592592

6 $2,011

Year 2 $309 0.85733882 $265 $2,237 0.85733882 $1,918

Howe

a

Forsteri

ana (10

pieces)

$57

0

$57

0 $1,843 $1,706 $1,580 $5,1

28

Cham

aedorea

Elegans

(30

pieces)

$1,9

80

$1,9

80 $5,607 $6,056 $5,192 $16,

854

TOTAL $4,

710

$12,0

50

$11,1

57

$10,3

31

$38,

248

$11,4

03

$11,4

22

$10,1

61

$32,

987

Task 2:

In this case, NPV of the company has been analyzed to identify that whether the

company should buy the software or should subscribe it for a period of time. It has been

analyzed through this case that company is required to manage software and thus company

must choose an option of either buying the software or taking the subscription of the

software.

Further, it has been analyzed through the calculations that the total net present value

of the subscription would be $ 5,758 which is quite lesser than the total net present value of

the licence which is $7,695. So it could be depicted that this investment option (subscription)

is a good option for the company. Company could invest into this project to manage the

expenses (Ansari, 2004).

Through the calculations, it is suggested to the company to invest the amount into the

subscription of the software.

Licence Subscription

Membershi

p

Cash

Ouflow PV Factor

PV of

Cash

outflows

Cash

Ouflow PV Factor

PV of

Cash

outflows

Year 0 $6,900 1 $6,900 1 $0

Year 1 $300 0.92592592

6 $278 $2,172 0.92592592

6 $2,011

Year 2 $309 0.85733882 $265 $2,237 0.85733882 $1,918

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for decision making 10

Year 3 $318 0.79383224

1 $253 $2,304 0.79383224

1 $1,829

TOTAL $7,827 $4 $7,69

5

$6,71

3 $4 $5,758

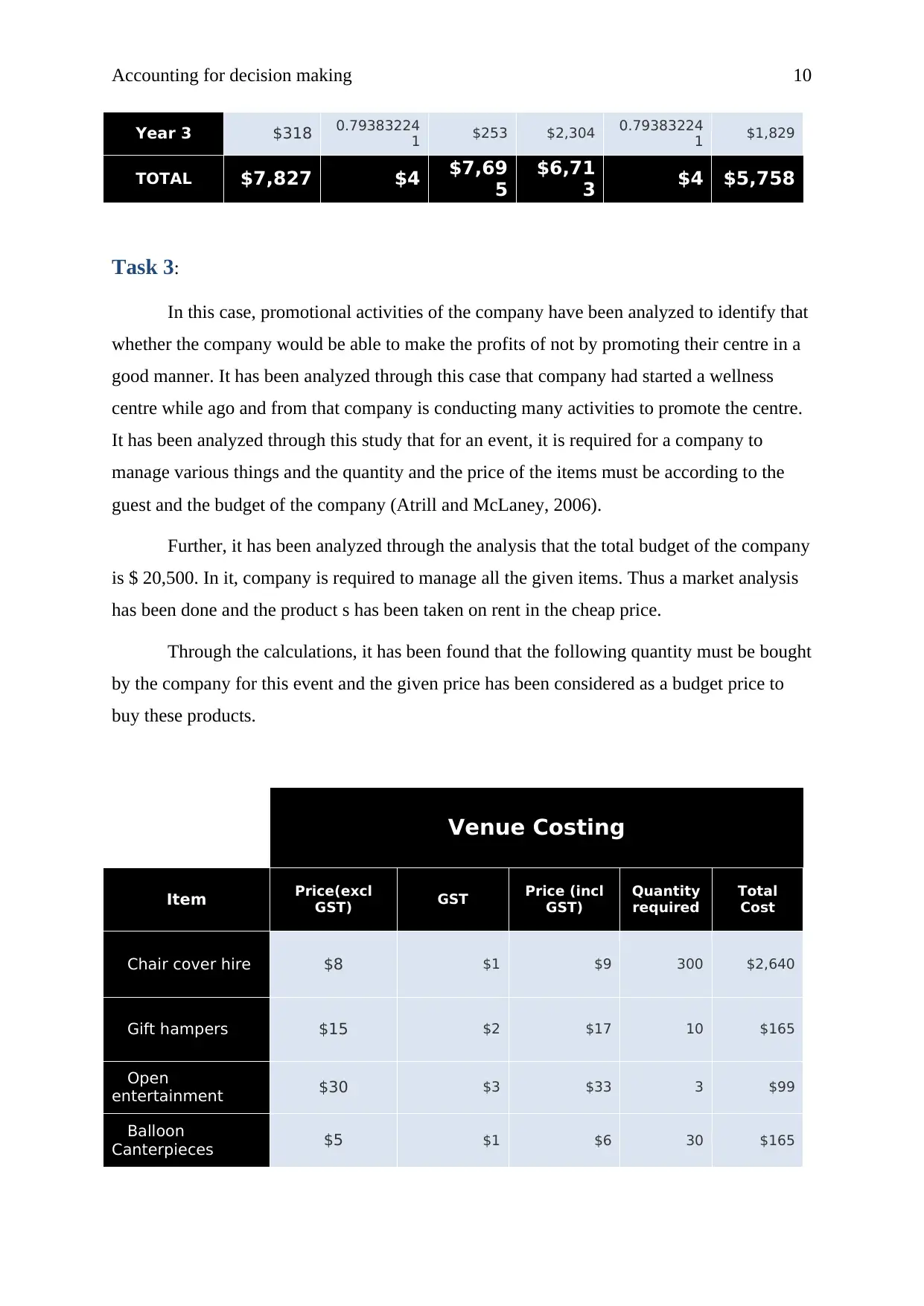

Task 3:

In this case, promotional activities of the company have been analyzed to identify that

whether the company would be able to make the profits of not by promoting their centre in a

good manner. It has been analyzed through this case that company had started a wellness

centre while ago and from that company is conducting many activities to promote the centre.

It has been analyzed through this study that for an event, it is required for a company to

manage various things and the quantity and the price of the items must be according to the

guest and the budget of the company (Atrill and McLaney, 2006).

Further, it has been analyzed through the analysis that the total budget of the company

is $ 20,500. In it, company is required to manage all the given items. Thus a market analysis

has been done and the product s has been taken on rent in the cheap price.

Through the calculations, it has been found that the following quantity must be bought

by the company for this event and the given price has been considered as a budget price to

buy these products.

Venue Costing

Item Price(excl

GST) GST Price (incl

GST)

Quantity

required

Total

Cost

Chair cover hire $8 $1 $9 300 $2,640

Gift hampers $15 $2 $17 10 $165

Open

entertainment $30 $3 $33 3 $99

Balloon

Canterpieces $5 $1 $6 30 $165

Year 3 $318 0.79383224

1 $253 $2,304 0.79383224

1 $1,829

TOTAL $7,827 $4 $7,69

5

$6,71

3 $4 $5,758

Task 3:

In this case, promotional activities of the company have been analyzed to identify that

whether the company would be able to make the profits of not by promoting their centre in a

good manner. It has been analyzed through this case that company had started a wellness

centre while ago and from that company is conducting many activities to promote the centre.

It has been analyzed through this study that for an event, it is required for a company to

manage various things and the quantity and the price of the items must be according to the

guest and the budget of the company (Atrill and McLaney, 2006).

Further, it has been analyzed through the analysis that the total budget of the company

is $ 20,500. In it, company is required to manage all the given items. Thus a market analysis

has been done and the product s has been taken on rent in the cheap price.

Through the calculations, it has been found that the following quantity must be bought

by the company for this event and the given price has been considered as a budget price to

buy these products.

Venue Costing

Item Price(excl

GST) GST Price (incl

GST)

Quantity

required

Total

Cost

Chair cover hire $8 $1 $9 300 $2,640

Gift hampers $15 $2 $17 10 $165

Open

entertainment $30 $3 $33 3 $99

Balloon

Canterpieces $5 $1 $6 30 $165

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for decision making 11

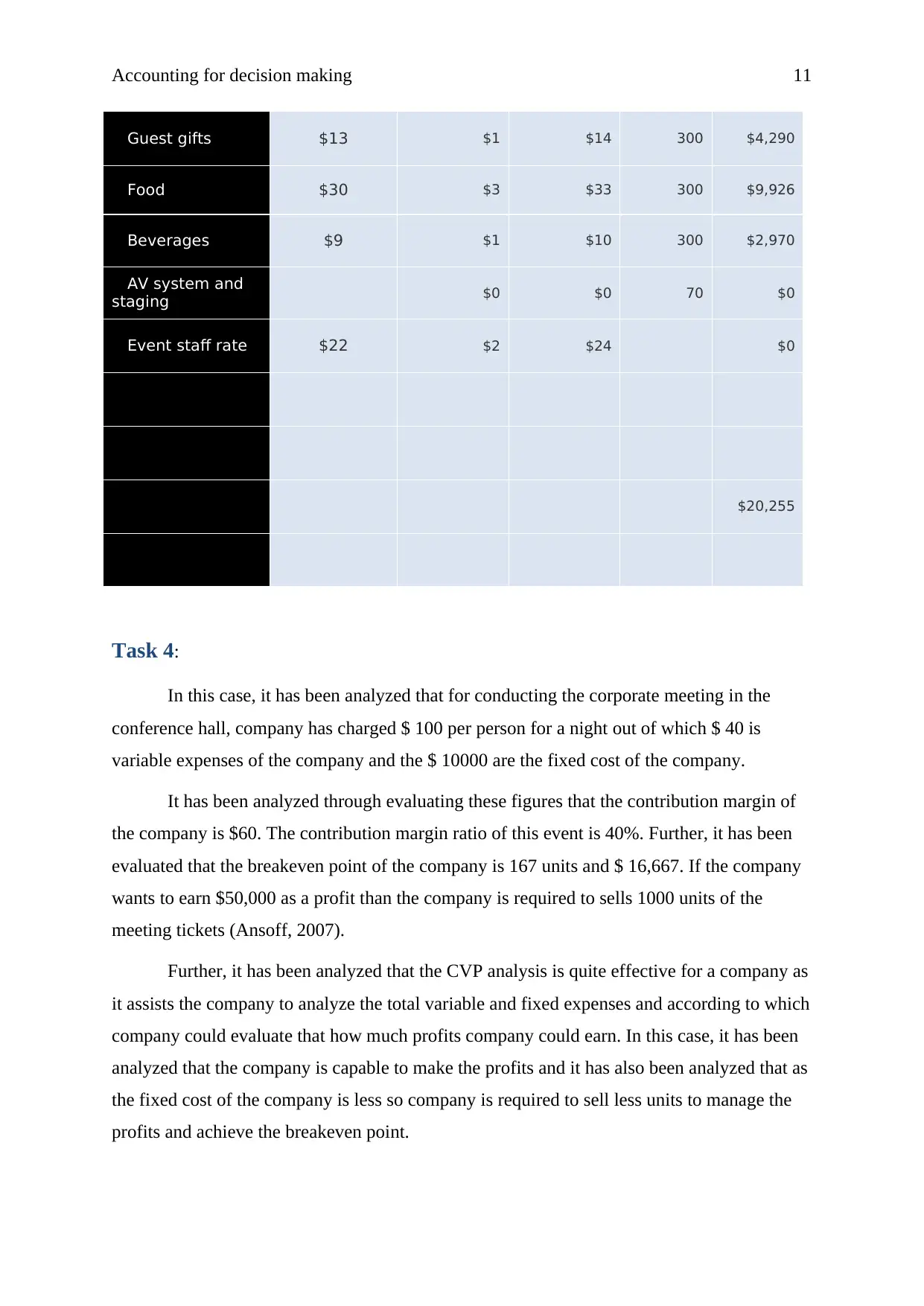

Guest gifts $13 $1 $14 300 $4,290

Food $30 $3 $33 300 $9,926

Beverages $9 $1 $10 300 $2,970

AV system and

staging $0 $0 70 $0

Event staff rate $22 $2 $24 $0

$20,255

Task 4:

In this case, it has been analyzed that for conducting the corporate meeting in the

conference hall, company has charged $ 100 per person for a night out of which $ 40 is

variable expenses of the company and the $ 10000 are the fixed cost of the company.

It has been analyzed through evaluating these figures that the contribution margin of

the company is $60. The contribution margin ratio of this event is 40%. Further, it has been

evaluated that the breakeven point of the company is 167 units and $ 16,667. If the company

wants to earn $50,000 as a profit than the company is required to sells 1000 units of the

meeting tickets (Ansoff, 2007).

Further, it has been analyzed that the CVP analysis is quite effective for a company as

it assists the company to analyze the total variable and fixed expenses and according to which

company could evaluate that how much profits company could earn. In this case, it has been

analyzed that the company is capable to make the profits and it has also been analyzed that as

the fixed cost of the company is less so company is required to sell less units to manage the

profits and achieve the breakeven point.

Guest gifts $13 $1 $14 300 $4,290

Food $30 $3 $33 300 $9,926

Beverages $9 $1 $10 300 $2,970

AV system and

staging $0 $0 70 $0

Event staff rate $22 $2 $24 $0

$20,255

Task 4:

In this case, it has been analyzed that for conducting the corporate meeting in the

conference hall, company has charged $ 100 per person for a night out of which $ 40 is

variable expenses of the company and the $ 10000 are the fixed cost of the company.

It has been analyzed through evaluating these figures that the contribution margin of

the company is $60. The contribution margin ratio of this event is 40%. Further, it has been

evaluated that the breakeven point of the company is 167 units and $ 16,667. If the company

wants to earn $50,000 as a profit than the company is required to sells 1000 units of the

meeting tickets (Ansoff, 2007).

Further, it has been analyzed that the CVP analysis is quite effective for a company as

it assists the company to analyze the total variable and fixed expenses and according to which

company could evaluate that how much profits company could earn. In this case, it has been

analyzed that the company is capable to make the profits and it has also been analyzed that as

the fixed cost of the company is less so company is required to sell less units to manage the

profits and achieve the breakeven point.

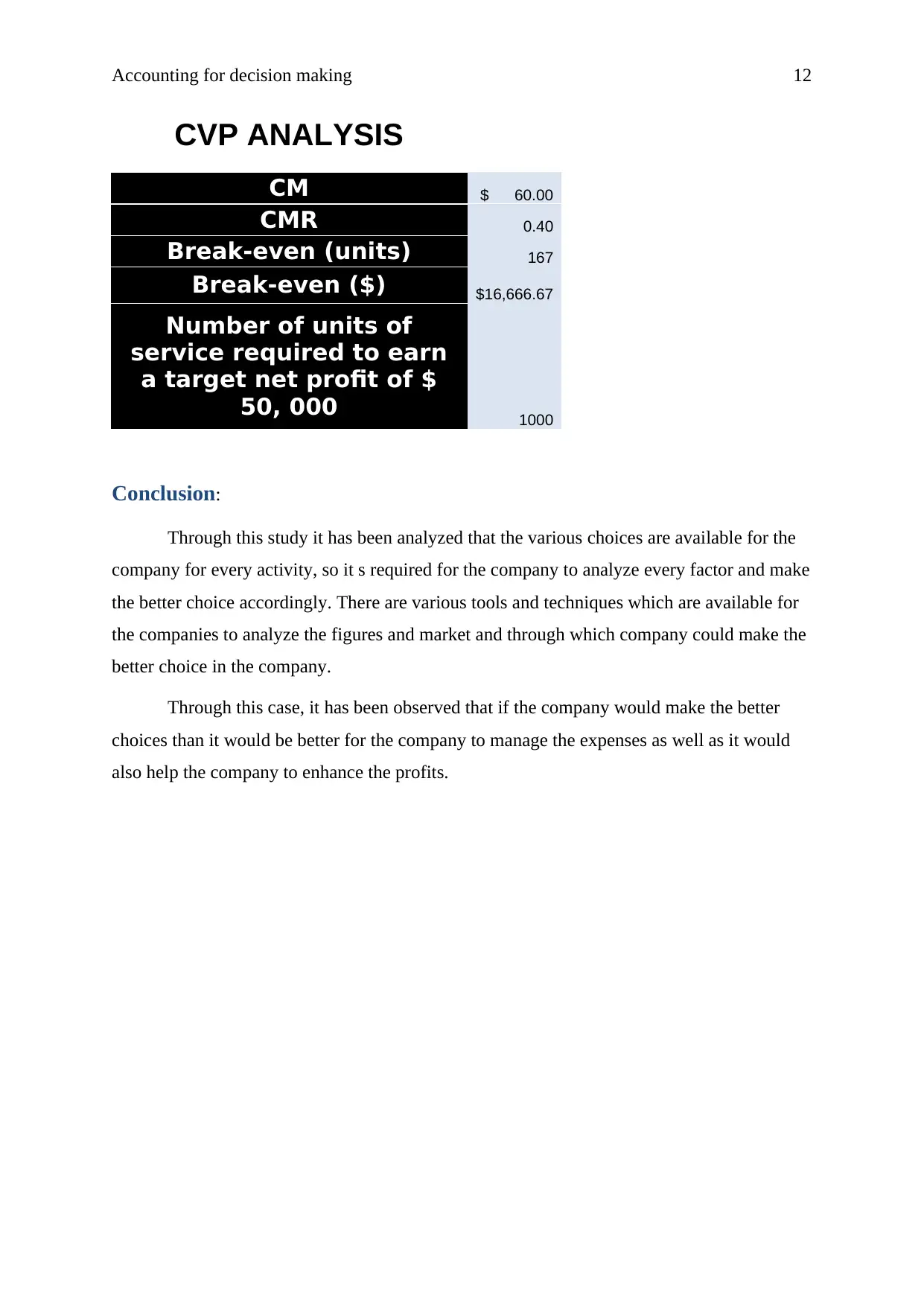

Accounting for decision making 12

CVP ANALYSIS

CM $ 60.00

CMR 0.40

Break-even (units) 167

Break-even ($) $16,666.67

Number of units of

service required to earn

a target net profit of $

50, 000 1000

Conclusion:

Through this study it has been analyzed that the various choices are available for the

company for every activity, so it s required for the company to analyze every factor and make

the better choice accordingly. There are various tools and techniques which are available for

the companies to analyze the figures and market and through which company could make the

better choice in the company.

Through this case, it has been observed that if the company would make the better

choices than it would be better for the company to manage the expenses as well as it would

also help the company to enhance the profits.

CVP ANALYSIS

CM $ 60.00

CMR 0.40

Break-even (units) 167

Break-even ($) $16,666.67

Number of units of

service required to earn

a target net profit of $

50, 000 1000

Conclusion:

Through this study it has been analyzed that the various choices are available for the

company for every activity, so it s required for the company to analyze every factor and make

the better choice accordingly. There are various tools and techniques which are available for

the companies to analyze the figures and market and through which company could make the

better choice in the company.

Through this case, it has been observed that if the company would make the better

choices than it would be better for the company to manage the expenses as well as it would

also help the company to enhance the profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.