Comprehensive Equity Analysis Report: CSL Ltd Stock Valuation

VerifiedAdded on 2020/07/22

|21

|4595

|456

Report

AI Summary

This report provides a comprehensive equity analysis of CSL Ltd, a leading biotechnology company. It includes an executive summary, introduction outlining objectives and the rationale for selecting CSL Ltd, and a detailed fundamental analysis covering basic information, operational and competitive status, and a SWOT analysis. The valuation section details the methodology, assumptions, historical data, beta analysis, dividend growth rate estimation, and valuation models, culminating in a final valuation and risk analysis. The report concludes with a recommendation based on the findings, aiming to assist investors and portfolio managers in making informed decisions regarding CSL Ltd's stock. The analysis considers both fundamental and intrinsic value perspectives to assess the stock's potential for middle and long-term investment returns, highlighting key financial ratios, profitability, liquidity, and solvency metrics, as well as an assessment of the company's strengths, weaknesses, opportunities, and threats.

Equity Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. Executive Summary.....................................................................................................................1

2. Introduction..................................................................................................................................1

2.1 Objectives of the report.........................................................................................................1

2.2 Reasons for selecting CSL Ltd..............................................................................................1

3.0 Fundamental analysis.................................................................................................................2

3.1 Basic information...................................................................................................................2

3.2 Operation and competitive status analysis.............................................................................2

3.3 SWOT analysis....................................................................................................................10

4 Valuation.....................................................................................................................................11

4.1Analysis methodology..........................................................................................................12

4.2Assumptions.........................................................................................................................12

4.3 Historical data......................................................................................................................12

4.4.1 Beta analysis.....................................................................................................................14

4.3 Dividend growth rate estimation.........................................................................................15

4.4.2 Valuation model...............................................................................................................16

4.4.3 Valuation...........................................................................................................................17

4.4.5 Risk analysis and assumptions..........................................................................................17

5 Recommendation........................................................................................................................17

1. Executive Summary.....................................................................................................................1

2. Introduction..................................................................................................................................1

2.1 Objectives of the report.........................................................................................................1

2.2 Reasons for selecting CSL Ltd..............................................................................................1

3.0 Fundamental analysis.................................................................................................................2

3.1 Basic information...................................................................................................................2

3.2 Operation and competitive status analysis.............................................................................2

3.3 SWOT analysis....................................................................................................................10

4 Valuation.....................................................................................................................................11

4.1Analysis methodology..........................................................................................................12

4.2Assumptions.........................................................................................................................12

4.3 Historical data......................................................................................................................12

4.4.1 Beta analysis.....................................................................................................................14

4.3 Dividend growth rate estimation.........................................................................................15

4.4.2 Valuation model...............................................................................................................16

4.4.3 Valuation...........................................................................................................................17

4.4.5 Risk analysis and assumptions..........................................................................................17

5 Recommendation........................................................................................................................17

1. Executive Summary

In the present era, investors prefer to take risk with the motive to generate high returns

from the amount invested. In this regard, equity valuation and beta assessment becomes the

priority which in turn helps in ascertaining the level of investment risk and stock’s volatility. The

main objectives of CBB investment company is to provide investors with higher returns. Hence,

for enhancing the middle and long term investment return equity analysis of CSL Ltd’s stock is

conducted by taking into account the fundamental and intrinsic value perspectives.

For this report, CSL Ltd has been selected which one of the leading biotechnology

company operating at global level. It is involved in the varied activities such as research,

development, manufacturing and marketing of products or services that helps in treating as well

as preventing serious human medical conditions. Products which are offered by CSL Ltd include

blood plasma derivatives, vaccines, research and manufacturing applications etc. It can be

concluded from the evaluation that financial position and performance of CSL is good. However,

it needs to make focus on ideal debt-equity ratio such as .5:1 which in turn helps in creating

optimal structure. Further, it can be summarized from the evaluation that beta of CSL’s stock

is .51 respectively which is not higher as compared to the market trend as whole.

2. Introduction

2.1 Objectives of the report

The main objectives of the present report are to assess intrinsic value of stock, beta and

returns that are associated with the stock of CSL Ltd. Hence, findings of the report will provide

potential investors as well as portfolio manager with the input for decision making. The present

report will provide investment management team with the strategies for effectual portfolio

management.

2.2 Reasons for selecting CSL Ltd

At the time of stock selection, high level of emphasis is placed on middle-long term

investment. In addition to this, aspect of risk minimization has also been considered while

making selection of stock for portfolio. Current portfolio of CBB does not include any

biotechnology company. Along with this, Australian Biotechnology Company has attained

leading position in the world and it is continuously growing. Thus, to strengthen the portfolio

and enhancing the associated returns CSL Ltd has been selected by analyst. Inclusion of such

company in portfolio may result into diversity and minimization of portfolio’s risk.

1 | P a g e

In the present era, investors prefer to take risk with the motive to generate high returns

from the amount invested. In this regard, equity valuation and beta assessment becomes the

priority which in turn helps in ascertaining the level of investment risk and stock’s volatility. The

main objectives of CBB investment company is to provide investors with higher returns. Hence,

for enhancing the middle and long term investment return equity analysis of CSL Ltd’s stock is

conducted by taking into account the fundamental and intrinsic value perspectives.

For this report, CSL Ltd has been selected which one of the leading biotechnology

company operating at global level. It is involved in the varied activities such as research,

development, manufacturing and marketing of products or services that helps in treating as well

as preventing serious human medical conditions. Products which are offered by CSL Ltd include

blood plasma derivatives, vaccines, research and manufacturing applications etc. It can be

concluded from the evaluation that financial position and performance of CSL is good. However,

it needs to make focus on ideal debt-equity ratio such as .5:1 which in turn helps in creating

optimal structure. Further, it can be summarized from the evaluation that beta of CSL’s stock

is .51 respectively which is not higher as compared to the market trend as whole.

2. Introduction

2.1 Objectives of the report

The main objectives of the present report are to assess intrinsic value of stock, beta and

returns that are associated with the stock of CSL Ltd. Hence, findings of the report will provide

potential investors as well as portfolio manager with the input for decision making. The present

report will provide investment management team with the strategies for effectual portfolio

management.

2.2 Reasons for selecting CSL Ltd

At the time of stock selection, high level of emphasis is placed on middle-long term

investment. In addition to this, aspect of risk minimization has also been considered while

making selection of stock for portfolio. Current portfolio of CBB does not include any

biotechnology company. Along with this, Australian Biotechnology Company has attained

leading position in the world and it is continuously growing. Thus, to strengthen the portfolio

and enhancing the associated returns CSL Ltd has been selected by analyst. Inclusion of such

company in portfolio may result into diversity and minimization of portfolio’s risk.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.0 Fundamental analysis

3.1 Basic information

CSL is one of largest company of Australia and is operating in biotherapeutics industry.

Firm is currently operating multiple projects under which it is developing innovative biotherapies

that save life of million of peoople. Firm have manufacturing plant in Australia, USA and some

of European nations (Corporate profile, 2017). Mentioned company is specifically focusing on

R&D so that more therapies can be developed. In current time period firm is leading producer of

plasma protein therapeutics. Firm is consistently expanding its market and have aggreive

investment plans. Thus, there is positive optimism about growth of business firm.

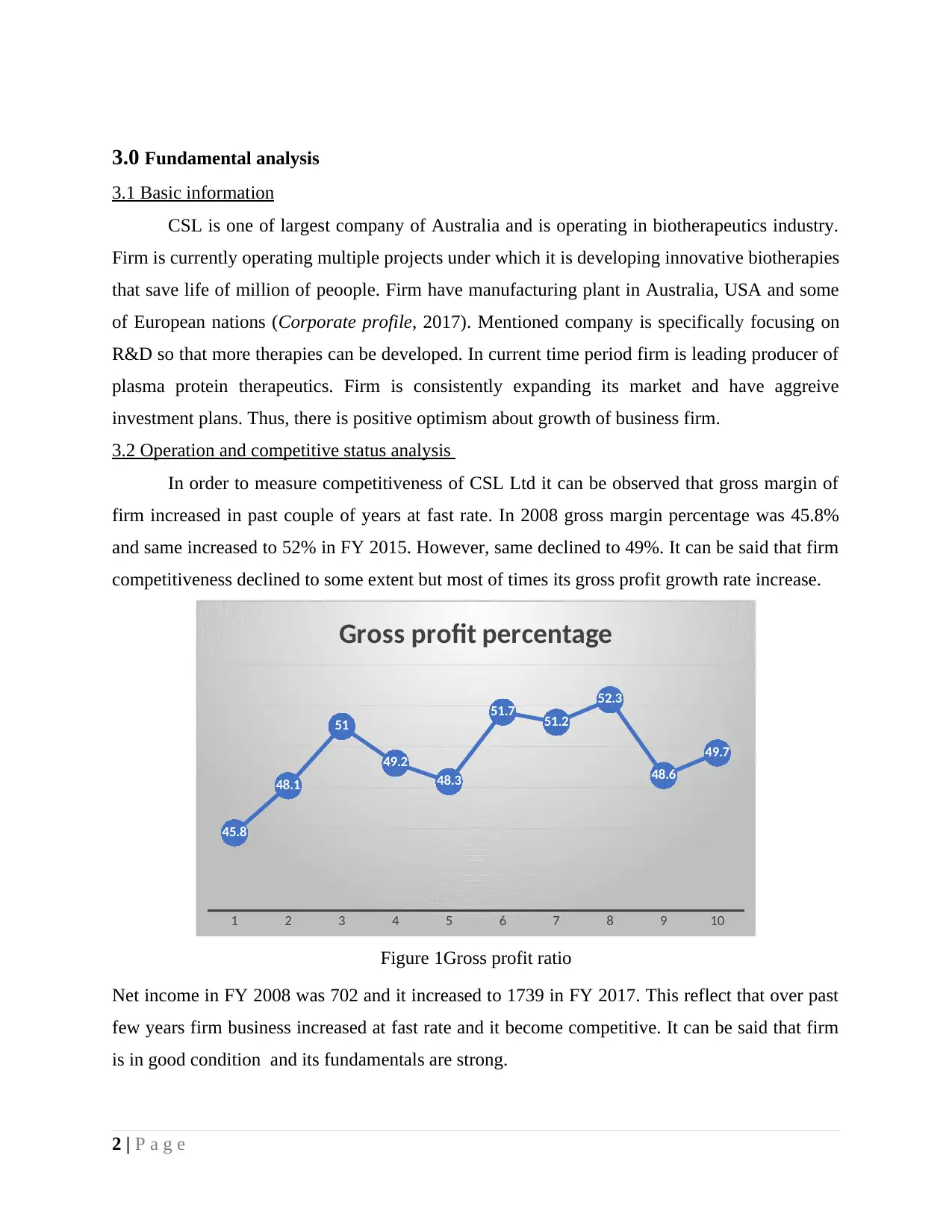

3.2 Operation and competitive status analysis

In order to measure competitiveness of CSL Ltd it can be observed that gross margin of

firm increased in past couple of years at fast rate. In 2008 gross margin percentage was 45.8%

and same increased to 52% in FY 2015. However, same declined to 49%. It can be said that firm

competitiveness declined to some extent but most of times its gross profit growth rate increase.

1 2 3 4 5 6 7 8 9 10

45.8

48.1

51

49.2

48.3

51.7 51.2

52.3

48.6

49.7

Gross profit percentage

Figure 1Gross profit ratio

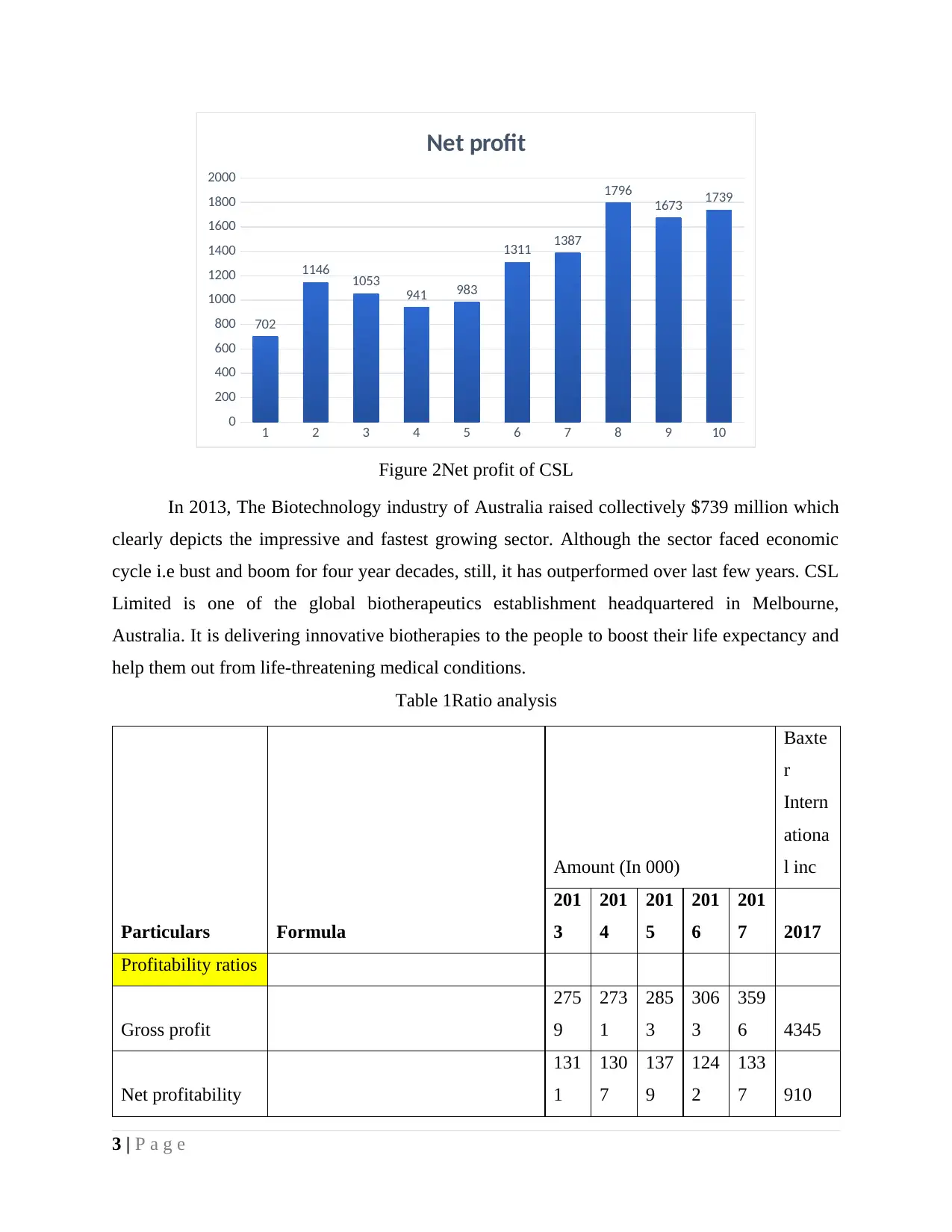

Net income in FY 2008 was 702 and it increased to 1739 in FY 2017. This reflect that over past

few years firm business increased at fast rate and it become competitive. It can be said that firm

is in good condition and its fundamentals are strong.

2 | P a g e

3.1 Basic information

CSL is one of largest company of Australia and is operating in biotherapeutics industry.

Firm is currently operating multiple projects under which it is developing innovative biotherapies

that save life of million of peoople. Firm have manufacturing plant in Australia, USA and some

of European nations (Corporate profile, 2017). Mentioned company is specifically focusing on

R&D so that more therapies can be developed. In current time period firm is leading producer of

plasma protein therapeutics. Firm is consistently expanding its market and have aggreive

investment plans. Thus, there is positive optimism about growth of business firm.

3.2 Operation and competitive status analysis

In order to measure competitiveness of CSL Ltd it can be observed that gross margin of

firm increased in past couple of years at fast rate. In 2008 gross margin percentage was 45.8%

and same increased to 52% in FY 2015. However, same declined to 49%. It can be said that firm

competitiveness declined to some extent but most of times its gross profit growth rate increase.

1 2 3 4 5 6 7 8 9 10

45.8

48.1

51

49.2

48.3

51.7 51.2

52.3

48.6

49.7

Gross profit percentage

Figure 1Gross profit ratio

Net income in FY 2008 was 702 and it increased to 1739 in FY 2017. This reflect that over past

few years firm business increased at fast rate and it become competitive. It can be said that firm

is in good condition and its fundamentals are strong.

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2 3 4 5 6 7 8 9 10

0

200

400

600

800

1000

1200

1400

1600

1800

2000

702

1146 1053 941 983

1311 1387

1796

1673 1739

Net profit

Figure 2Net profit of CSL

In 2013, The Biotechnology industry of Australia raised collectively $739 million which

clearly depicts the impressive and fastest growing sector. Although the sector faced economic

cycle i.e bust and boom for four year decades, still, it has outperformed over last few years. CSL

Limited is one of the global biotherapeutics establishment headquartered in Melbourne,

Australia. It is delivering innovative biotherapies to the people to boost their life expectancy and

help them out from life-threatening medical conditions.

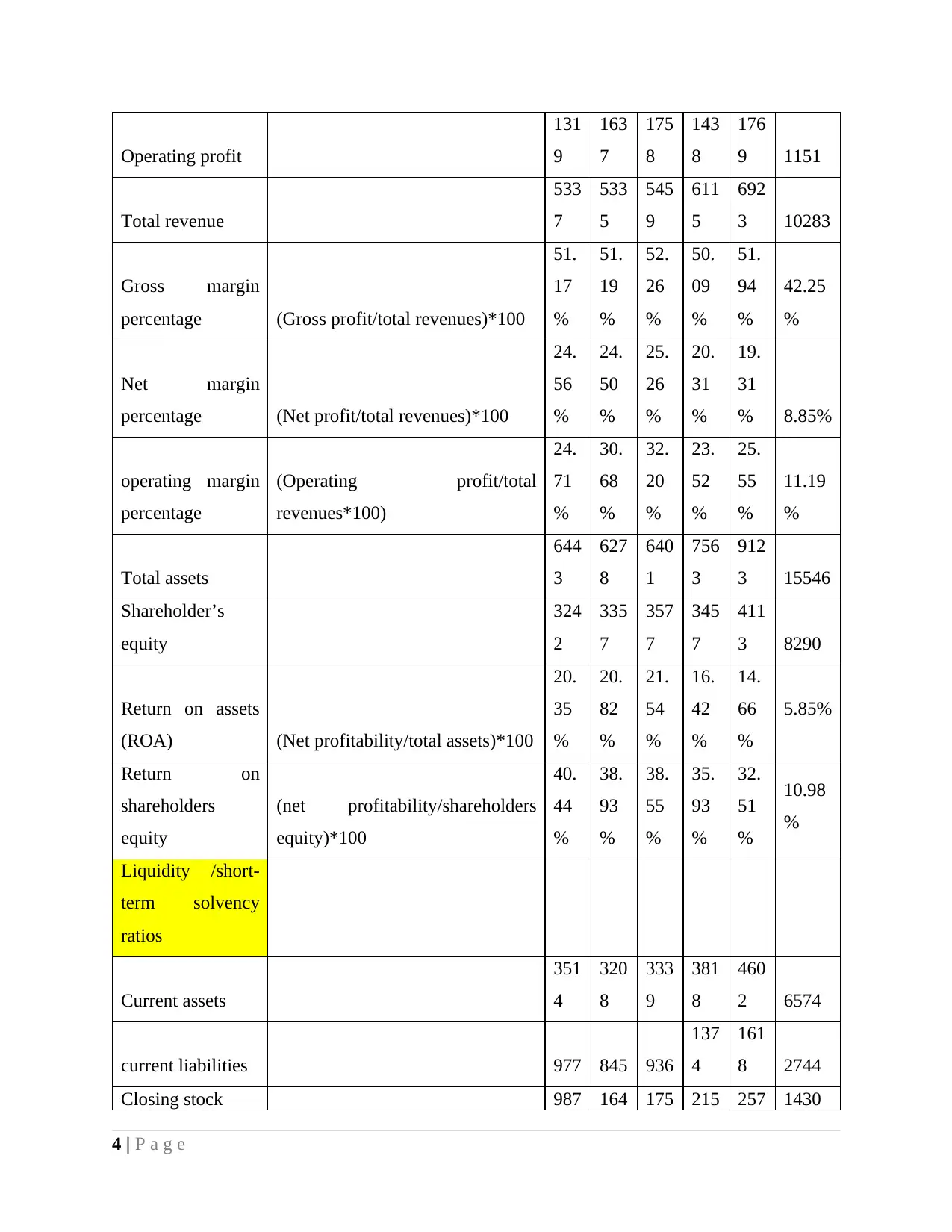

Table 1Ratio analysis

Particulars Formula

Amount (In 000)

Baxte

r

Intern

ationa

l inc

201

3

201

4

201

5

201

6

201

7 2017

Profitability ratios

Gross profit

275

9

273

1

285

3

306

3

359

6 4345

Net profitability

131

1

130

7

137

9

124

2

133

7 910

3 | P a g e

0

200

400

600

800

1000

1200

1400

1600

1800

2000

702

1146 1053 941 983

1311 1387

1796

1673 1739

Net profit

Figure 2Net profit of CSL

In 2013, The Biotechnology industry of Australia raised collectively $739 million which

clearly depicts the impressive and fastest growing sector. Although the sector faced economic

cycle i.e bust and boom for four year decades, still, it has outperformed over last few years. CSL

Limited is one of the global biotherapeutics establishment headquartered in Melbourne,

Australia. It is delivering innovative biotherapies to the people to boost their life expectancy and

help them out from life-threatening medical conditions.

Table 1Ratio analysis

Particulars Formula

Amount (In 000)

Baxte

r

Intern

ationa

l inc

201

3

201

4

201

5

201

6

201

7 2017

Profitability ratios

Gross profit

275

9

273

1

285

3

306

3

359

6 4345

Net profitability

131

1

130

7

137

9

124

2

133

7 910

3 | P a g e

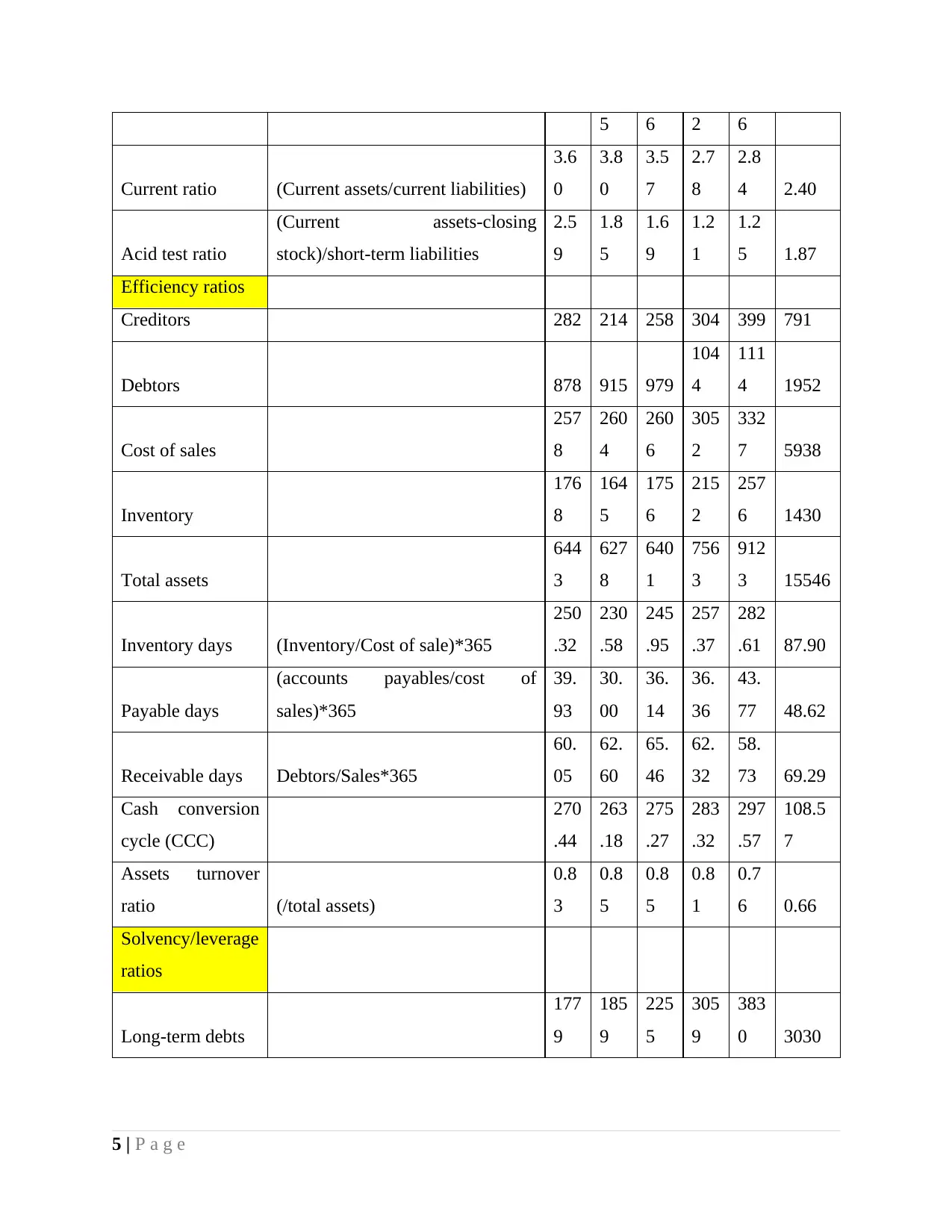

Operating profit

131

9

163

7

175

8

143

8

176

9 1151

Total revenue

533

7

533

5

545

9

611

5

692

3 10283

Gross margin

percentage (Gross profit/total revenues)*100

51.

17

%

51.

19

%

52.

26

%

50.

09

%

51.

94

%

42.25

%

Net margin

percentage (Net profit/total revenues)*100

24.

56

%

24.

50

%

25.

26

%

20.

31

%

19.

31

% 8.85%

operating margin

percentage

(Operating profit/total

revenues*100)

24.

71

%

30.

68

%

32.

20

%

23.

52

%

25.

55

%

11.19

%

Total assets

644

3

627

8

640

1

756

3

912

3 15546

Shareholder’s

equity

324

2

335

7

357

7

345

7

411

3 8290

Return on assets

(ROA) (Net profitability/total assets)*100

20.

35

%

20.

82

%

21.

54

%

16.

42

%

14.

66

%

5.85%

Return on

shareholders

equity

(net profitability/shareholders

equity)*100

40.

44

%

38.

93

%

38.

55

%

35.

93

%

32.

51

%

10.98

%

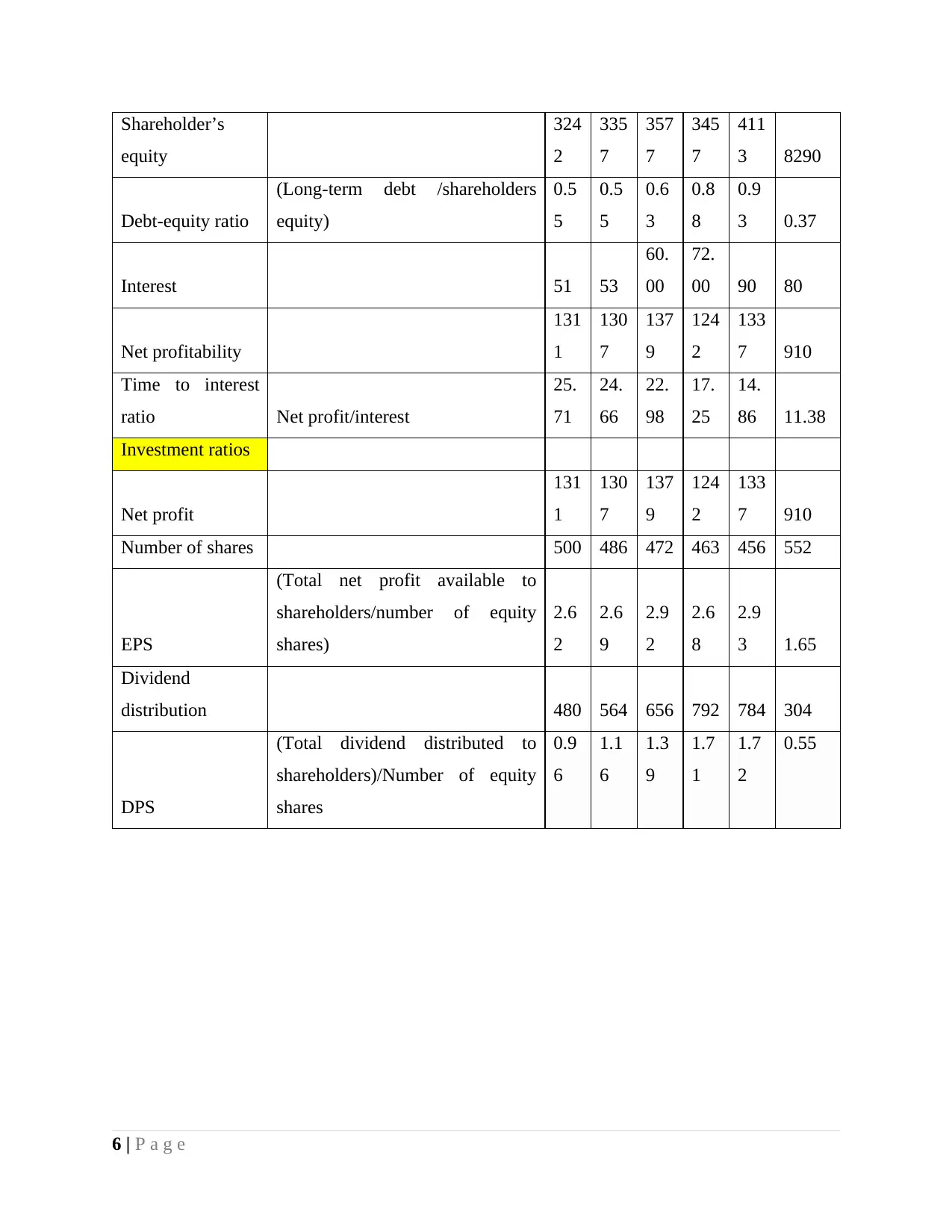

Liquidity /short-

term solvency

ratios

Current assets

351

4

320

8

333

9

381

8

460

2 6574

current liabilities 977 845 936

137

4

161

8 2744

Closing stock 987 164 175 215 257 1430

4 | P a g e

131

9

163

7

175

8

143

8

176

9 1151

Total revenue

533

7

533

5

545

9

611

5

692

3 10283

Gross margin

percentage (Gross profit/total revenues)*100

51.

17

%

51.

19

%

52.

26

%

50.

09

%

51.

94

%

42.25

%

Net margin

percentage (Net profit/total revenues)*100

24.

56

%

24.

50

%

25.

26

%

20.

31

%

19.

31

% 8.85%

operating margin

percentage

(Operating profit/total

revenues*100)

24.

71

%

30.

68

%

32.

20

%

23.

52

%

25.

55

%

11.19

%

Total assets

644

3

627

8

640

1

756

3

912

3 15546

Shareholder’s

equity

324

2

335

7

357

7

345

7

411

3 8290

Return on assets

(ROA) (Net profitability/total assets)*100

20.

35

%

20.

82

%

21.

54

%

16.

42

%

14.

66

%

5.85%

Return on

shareholders

equity

(net profitability/shareholders

equity)*100

40.

44

%

38.

93

%

38.

55

%

35.

93

%

32.

51

%

10.98

%

Liquidity /short-

term solvency

ratios

Current assets

351

4

320

8

333

9

381

8

460

2 6574

current liabilities 977 845 936

137

4

161

8 2744

Closing stock 987 164 175 215 257 1430

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 6 2 6

Current ratio (Current assets/current liabilities)

3.6

0

3.8

0

3.5

7

2.7

8

2.8

4 2.40

Acid test ratio

(Current assets-closing

stock)/short-term liabilities

2.5

9

1.8

5

1.6

9

1.2

1

1.2

5 1.87

Efficiency ratios

Creditors 282 214 258 304 399 791

Debtors 878 915 979

104

4

111

4 1952

Cost of sales

257

8

260

4

260

6

305

2

332

7 5938

Inventory

176

8

164

5

175

6

215

2

257

6 1430

Total assets

644

3

627

8

640

1

756

3

912

3 15546

Inventory days (Inventory/Cost of sale)*365

250

.32

230

.58

245

.95

257

.37

282

.61 87.90

Payable days

(accounts payables/cost of

sales)*365

39.

93

30.

00

36.

14

36.

36

43.

77 48.62

Receivable days Debtors/Sales*365

60.

05

62.

60

65.

46

62.

32

58.

73 69.29

Cash conversion

cycle (CCC)

270

.44

263

.18

275

.27

283

.32

297

.57

108.5

7

Assets turnover

ratio (/total assets)

0.8

3

0.8

5

0.8

5

0.8

1

0.7

6 0.66

Solvency/leverage

ratios

Long-term debts

177

9

185

9

225

5

305

9

383

0 3030

5 | P a g e

Current ratio (Current assets/current liabilities)

3.6

0

3.8

0

3.5

7

2.7

8

2.8

4 2.40

Acid test ratio

(Current assets-closing

stock)/short-term liabilities

2.5

9

1.8

5

1.6

9

1.2

1

1.2

5 1.87

Efficiency ratios

Creditors 282 214 258 304 399 791

Debtors 878 915 979

104

4

111

4 1952

Cost of sales

257

8

260

4

260

6

305

2

332

7 5938

Inventory

176

8

164

5

175

6

215

2

257

6 1430

Total assets

644

3

627

8

640

1

756

3

912

3 15546

Inventory days (Inventory/Cost of sale)*365

250

.32

230

.58

245

.95

257

.37

282

.61 87.90

Payable days

(accounts payables/cost of

sales)*365

39.

93

30.

00

36.

14

36.

36

43.

77 48.62

Receivable days Debtors/Sales*365

60.

05

62.

60

65.

46

62.

32

58.

73 69.29

Cash conversion

cycle (CCC)

270

.44

263

.18

275

.27

283

.32

297

.57

108.5

7

Assets turnover

ratio (/total assets)

0.8

3

0.8

5

0.8

5

0.8

1

0.7

6 0.66

Solvency/leverage

ratios

Long-term debts

177

9

185

9

225

5

305

9

383

0 3030

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder’s

equity

324

2

335

7

357

7

345

7

411

3 8290

Debt-equity ratio

(Long-term debt /shareholders

equity)

0.5

5

0.5

5

0.6

3

0.8

8

0.9

3 0.37

Interest 51 53

60.

00

72.

00 90 80

Net profitability

131

1

130

7

137

9

124

2

133

7 910

Time to interest

ratio Net profit/interest

25.

71

24.

66

22.

98

17.

25

14.

86 11.38

Investment ratios

Net profit

131

1

130

7

137

9

124

2

133

7 910

Number of shares 500 486 472 463 456 552

EPS

(Total net profit available to

shareholders/number of equity

shares)

2.6

2

2.6

9

2.9

2

2.6

8

2.9

3 1.65

Dividend

distribution 480 564 656 792 784 304

DPS

(Total dividend distributed to

shareholders)/Number of equity

shares

0.9

6

1.1

6

1.3

9

1.7

1

1.7

2

0.55

6 | P a g e

equity

324

2

335

7

357

7

345

7

411

3 8290

Debt-equity ratio

(Long-term debt /shareholders

equity)

0.5

5

0.5

5

0.6

3

0.8

8

0.9

3 0.37

Interest 51 53

60.

00

72.

00 90 80

Net profitability

131

1

130

7

137

9

124

2

133

7 910

Time to interest

ratio Net profit/interest

25.

71

24.

66

22.

98

17.

25

14.

86 11.38

Investment ratios

Net profit

131

1

130

7

137

9

124

2

133

7 910

Number of shares 500 486 472 463 456 552

EPS

(Total net profit available to

shareholders/number of equity

shares)

2.6

2

2.6

9

2.9

2

2.6

8

2.9

3 1.65

Dividend

distribution 480 564 656 792 784 304

DPS

(Total dividend distributed to

shareholders)/Number of equity

shares

0.9

6

1.1

6

1.3

9

1.7

1

1.7

2

0.55

6 | P a g e

2013 2014 2015 2016 2017

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

CSL's Profitability performance

Ratio (IN percentgae)

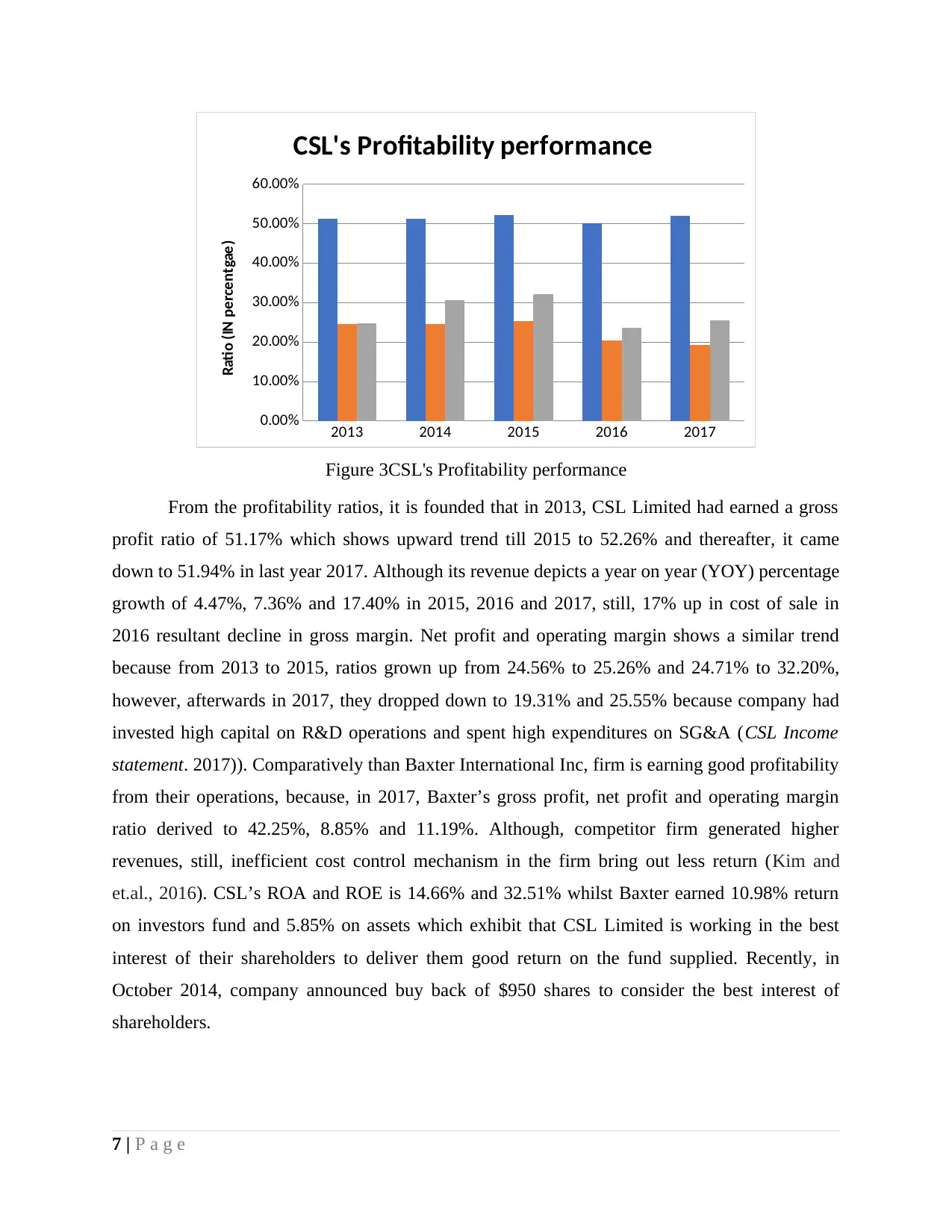

Figure 3CSL's Profitability performance

From the profitability ratios, it is founded that in 2013, CSL Limited had earned a gross

profit ratio of 51.17% which shows upward trend till 2015 to 52.26% and thereafter, it came

down to 51.94% in last year 2017. Although its revenue depicts a year on year (YOY) percentage

growth of 4.47%, 7.36% and 17.40% in 2015, 2016 and 2017, still, 17% up in cost of sale in

2016 resultant decline in gross margin. Net profit and operating margin shows a similar trend

because from 2013 to 2015, ratios grown up from 24.56% to 25.26% and 24.71% to 32.20%,

however, afterwards in 2017, they dropped down to 19.31% and 25.55% because company had

invested high capital on R&D operations and spent high expenditures on SG&A (CSL Income

statement. 2017)). Comparatively than Baxter International Inc, firm is earning good profitability

from their operations, because, in 2017, Baxter’s gross profit, net profit and operating margin

ratio derived to 42.25%, 8.85% and 11.19%. Although, competitor firm generated higher

revenues, still, inefficient cost control mechanism in the firm bring out less return (Kim and

et.al., 2016). CSL’s ROA and ROE is 14.66% and 32.51% whilst Baxter earned 10.98% return

on investors fund and 5.85% on assets which exhibit that CSL Limited is working in the best

interest of their shareholders to deliver them good return on the fund supplied. Recently, in

October 2014, company announced buy back of $950 shares to consider the best interest of

shareholders.

7 | P a g e

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

CSL's Profitability performance

Ratio (IN percentgae)

Figure 3CSL's Profitability performance

From the profitability ratios, it is founded that in 2013, CSL Limited had earned a gross

profit ratio of 51.17% which shows upward trend till 2015 to 52.26% and thereafter, it came

down to 51.94% in last year 2017. Although its revenue depicts a year on year (YOY) percentage

growth of 4.47%, 7.36% and 17.40% in 2015, 2016 and 2017, still, 17% up in cost of sale in

2016 resultant decline in gross margin. Net profit and operating margin shows a similar trend

because from 2013 to 2015, ratios grown up from 24.56% to 25.26% and 24.71% to 32.20%,

however, afterwards in 2017, they dropped down to 19.31% and 25.55% because company had

invested high capital on R&D operations and spent high expenditures on SG&A (CSL Income

statement. 2017)). Comparatively than Baxter International Inc, firm is earning good profitability

from their operations, because, in 2017, Baxter’s gross profit, net profit and operating margin

ratio derived to 42.25%, 8.85% and 11.19%. Although, competitor firm generated higher

revenues, still, inefficient cost control mechanism in the firm bring out less return (Kim and

et.al., 2016). CSL’s ROA and ROE is 14.66% and 32.51% whilst Baxter earned 10.98% return

on investors fund and 5.85% on assets which exhibit that CSL Limited is working in the best

interest of their shareholders to deliver them good return on the fund supplied. Recently, in

October 2014, company announced buy back of $950 shares to consider the best interest of

shareholders.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Liquidity ratio

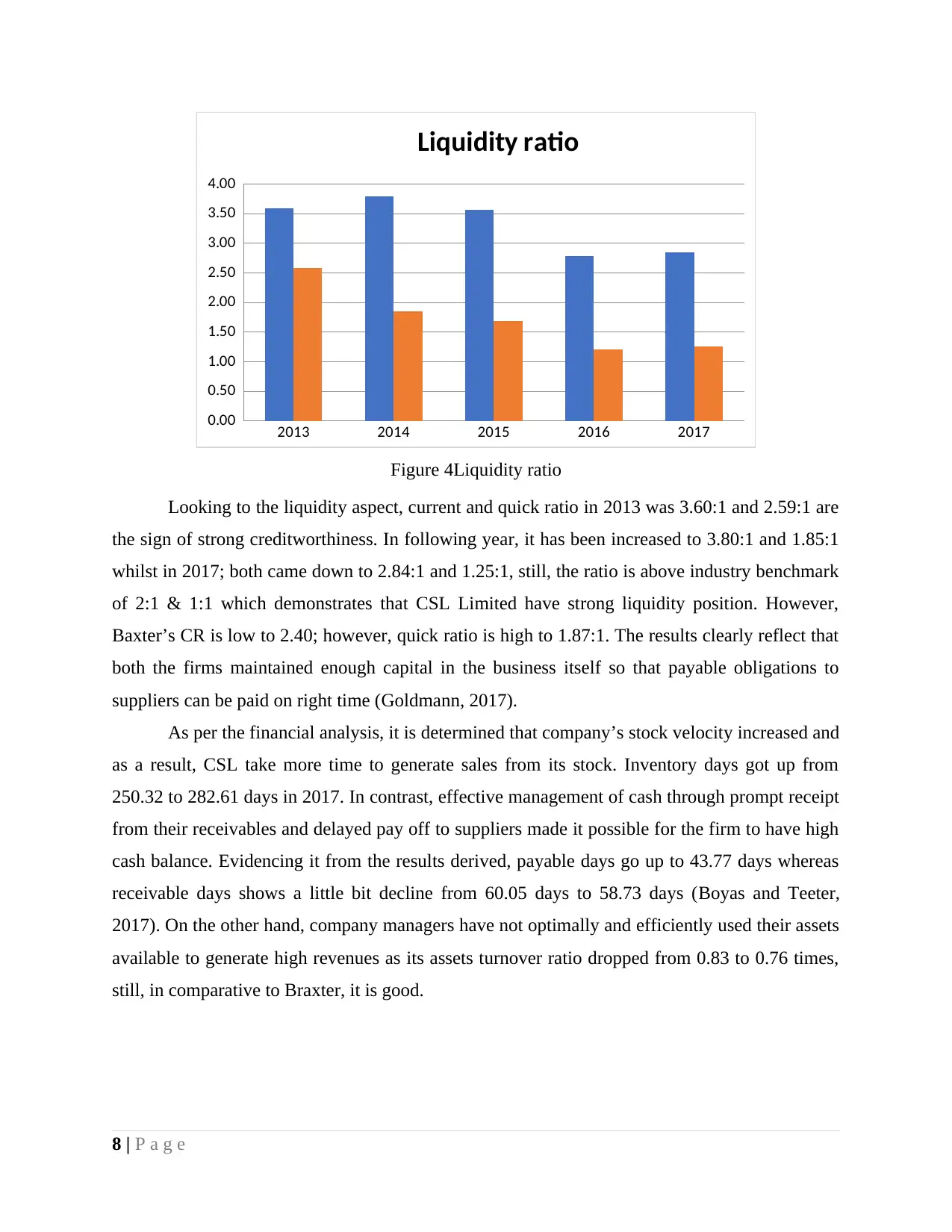

Figure 4Liquidity ratio

Looking to the liquidity aspect, current and quick ratio in 2013 was 3.60:1 and 2.59:1 are

the sign of strong creditworthiness. In following year, it has been increased to 3.80:1 and 1.85:1

whilst in 2017; both came down to 2.84:1 and 1.25:1, still, the ratio is above industry benchmark

of 2:1 & 1:1 which demonstrates that CSL Limited have strong liquidity position. However,

Baxter’s CR is low to 2.40; however, quick ratio is high to 1.87:1. The results clearly reflect that

both the firms maintained enough capital in the business itself so that payable obligations to

suppliers can be paid on right time (Goldmann, 2017).

As per the financial analysis, it is determined that company’s stock velocity increased and

as a result, CSL take more time to generate sales from its stock. Inventory days got up from

250.32 to 282.61 days in 2017. In contrast, effective management of cash through prompt receipt

from their receivables and delayed pay off to suppliers made it possible for the firm to have high

cash balance. Evidencing it from the results derived, payable days go up to 43.77 days whereas

receivable days shows a little bit decline from 60.05 days to 58.73 days (Boyas and Teeter,

2017). On the other hand, company managers have not optimally and efficiently used their assets

available to generate high revenues as its assets turnover ratio dropped from 0.83 to 0.76 times,

still, in comparative to Braxter, it is good.

8 | P a g e

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Liquidity ratio

Figure 4Liquidity ratio

Looking to the liquidity aspect, current and quick ratio in 2013 was 3.60:1 and 2.59:1 are

the sign of strong creditworthiness. In following year, it has been increased to 3.80:1 and 1.85:1

whilst in 2017; both came down to 2.84:1 and 1.25:1, still, the ratio is above industry benchmark

of 2:1 & 1:1 which demonstrates that CSL Limited have strong liquidity position. However,

Baxter’s CR is low to 2.40; however, quick ratio is high to 1.87:1. The results clearly reflect that

both the firms maintained enough capital in the business itself so that payable obligations to

suppliers can be paid on right time (Goldmann, 2017).

As per the financial analysis, it is determined that company’s stock velocity increased and

as a result, CSL take more time to generate sales from its stock. Inventory days got up from

250.32 to 282.61 days in 2017. In contrast, effective management of cash through prompt receipt

from their receivables and delayed pay off to suppliers made it possible for the firm to have high

cash balance. Evidencing it from the results derived, payable days go up to 43.77 days whereas

receivable days shows a little bit decline from 60.05 days to 58.73 days (Boyas and Teeter,

2017). On the other hand, company managers have not optimally and efficiently used their assets

available to generate high revenues as its assets turnover ratio dropped from 0.83 to 0.76 times,

still, in comparative to Braxter, it is good.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 2014 2015 2016 2017

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Debt to equity ratios

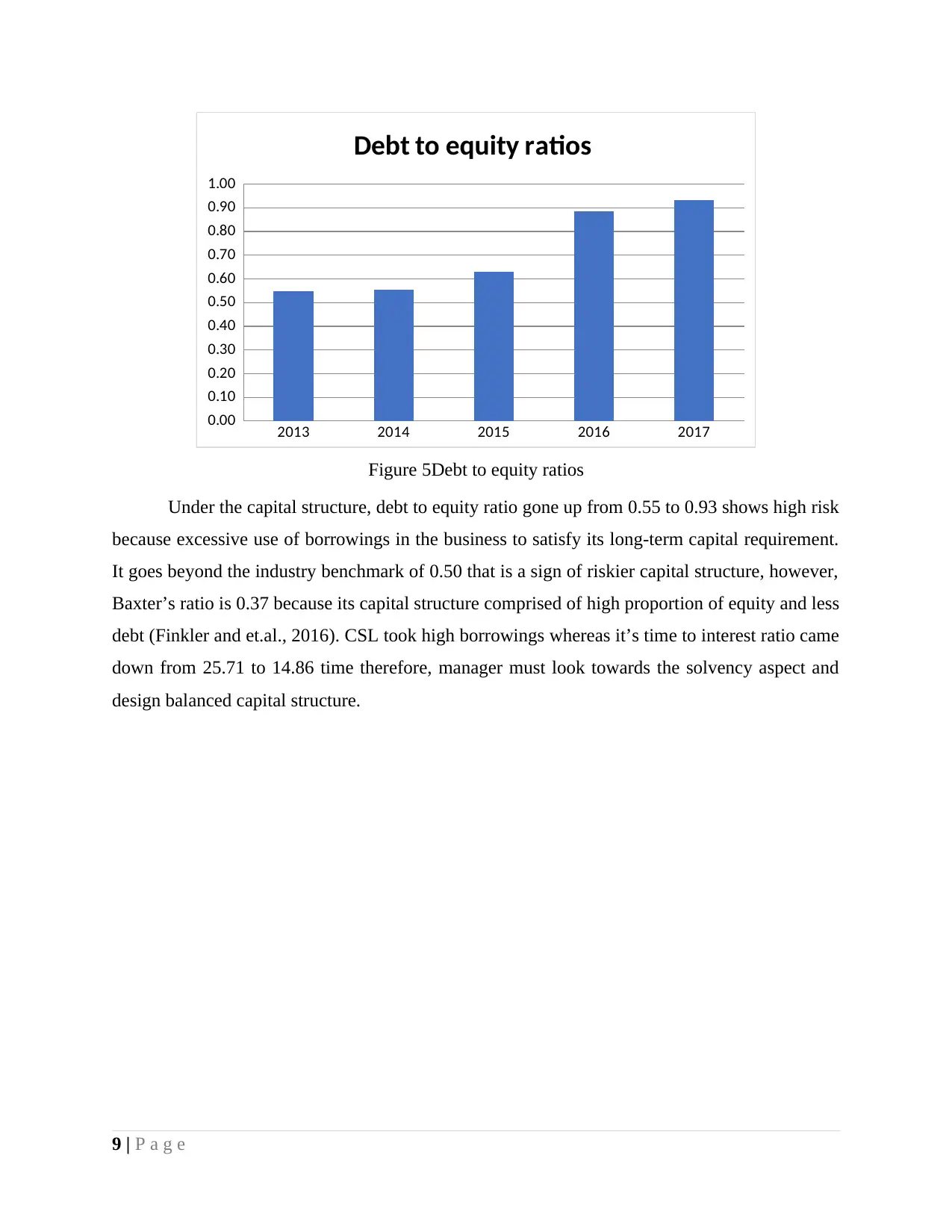

Figure 5Debt to equity ratios

Under the capital structure, debt to equity ratio gone up from 0.55 to 0.93 shows high risk

because excessive use of borrowings in the business to satisfy its long-term capital requirement.

It goes beyond the industry benchmark of 0.50 that is a sign of riskier capital structure, however,

Baxter’s ratio is 0.37 because its capital structure comprised of high proportion of equity and less

debt (Finkler and et.al., 2016). CSL took high borrowings whereas it’s time to interest ratio came

down from 25.71 to 14.86 time therefore, manager must look towards the solvency aspect and

design balanced capital structure.

9 | P a g e

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Debt to equity ratios

Figure 5Debt to equity ratios

Under the capital structure, debt to equity ratio gone up from 0.55 to 0.93 shows high risk

because excessive use of borrowings in the business to satisfy its long-term capital requirement.

It goes beyond the industry benchmark of 0.50 that is a sign of riskier capital structure, however,

Baxter’s ratio is 0.37 because its capital structure comprised of high proportion of equity and less

debt (Finkler and et.al., 2016). CSL took high borrowings whereas it’s time to interest ratio came

down from 25.71 to 14.86 time therefore, manager must look towards the solvency aspect and

design balanced capital structure.

9 | P a g e

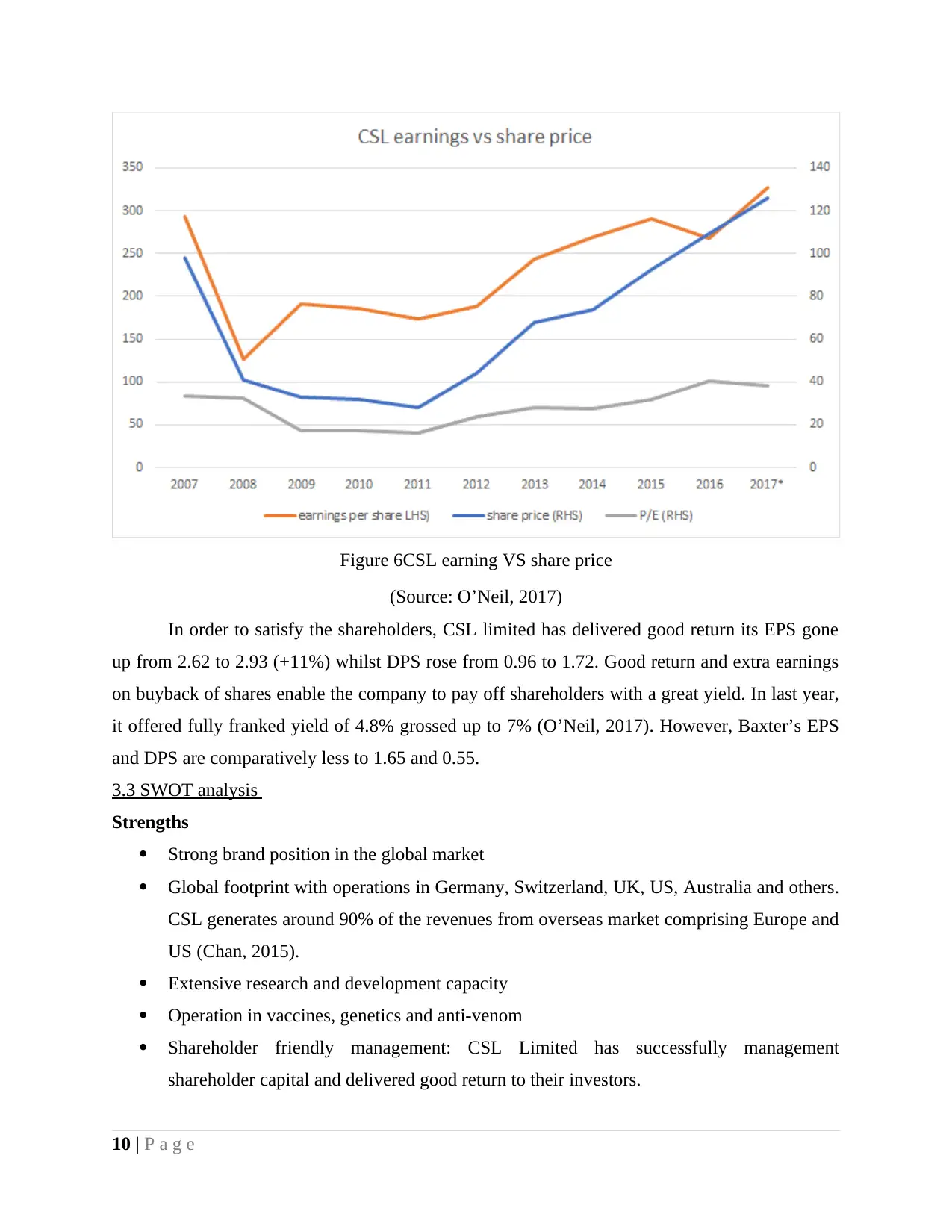

Figure 6CSL earning VS share price

(Source: O’Neil, 2017)

In order to satisfy the shareholders, CSL limited has delivered good return its EPS gone

up from 2.62 to 2.93 (+11%) whilst DPS rose from 0.96 to 1.72. Good return and extra earnings

on buyback of shares enable the company to pay off shareholders with a great yield. In last year,

it offered fully franked yield of 4.8% grossed up to 7% (O’Neil, 2017). However, Baxter’s EPS

and DPS are comparatively less to 1.65 and 0.55.

3.3 SWOT analysis

Strengths

Strong brand position in the global market

Global footprint with operations in Germany, Switzerland, UK, US, Australia and others.

CSL generates around 90% of the revenues from overseas market comprising Europe and

US (Chan, 2015).

Extensive research and development capacity

Operation in vaccines, genetics and anti-venom

Shareholder friendly management: CSL Limited has successfully management

shareholder capital and delivered good return to their investors.

10 | P a g e

(Source: O’Neil, 2017)

In order to satisfy the shareholders, CSL limited has delivered good return its EPS gone

up from 2.62 to 2.93 (+11%) whilst DPS rose from 0.96 to 1.72. Good return and extra earnings

on buyback of shares enable the company to pay off shareholders with a great yield. In last year,

it offered fully franked yield of 4.8% grossed up to 7% (O’Neil, 2017). However, Baxter’s EPS

and DPS are comparatively less to 1.65 and 0.55.

3.3 SWOT analysis

Strengths

Strong brand position in the global market

Global footprint with operations in Germany, Switzerland, UK, US, Australia and others.

CSL generates around 90% of the revenues from overseas market comprising Europe and

US (Chan, 2015).

Extensive research and development capacity

Operation in vaccines, genetics and anti-venom

Shareholder friendly management: CSL Limited has successfully management

shareholder capital and delivered good return to their investors.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.