Financial Audit and Ethics Report: CSL Limited (2018) Analysis

VerifiedAdded on 2022/12/29

|13

|3472

|93

Report

AI Summary

This report provides a comprehensive analysis of the audit and ethics of CSL Limited, a leading global biotech company. It begins by determining the level of materiality, considering factors such as profit before tax and relevant benchmarks. The report then reviews draft notes and disclosures, specifically addressing contingent liabilities and inventory valuation. A significant portion of the report is dedicated to ratio analysis, comparing CSL Limited with Sonic Healthcare to identify potential manipulation and areas of concern. Key ratios, including operating profit margin, net profit margin, current ratio, quick ratio, accounts receivable turnover, debt-to-equity ratio, and debt ratio, are examined. The report also analyzes the statement of cash flows, highlighting the importance of managing cash positions. Finally, the report outlines the audit procedures necessary to address the identified risks and concerns, including testing sales, current assets and liabilities, cash transactions, and debt instruments. The report concludes with recommendations for ensuring the accuracy and reliability of CSL Limited's financial statements.

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Determination of the Level of Materiality.............................................................................2

Review of Draft Notes and Disclosures.................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................8

Statement of Cash Flows........................................................................................................8

Audit Report...........................................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Determination of the Level of Materiality.............................................................................2

Review of Draft Notes and Disclosures.................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................8

Statement of Cash Flows........................................................................................................8

Audit Report...........................................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

2AUDITING AND ETHICS

Introduction

The main aim of the audit profession is to inspect and examine the financial records

and financial reports of the audit clients with the aim of find any kind of material

misstatement in them. It is important for the auditors to determine the level of materiality for

the audit of the group accounts as this materiality level assists the auditors in identifying the

materially misstated accounts in the financial statements (Griffiths, 2016). This needs to be

done by the auditors after taking into consideration the analysis of the financial statements

and associated draft notes. After the determination of level of materiality, the auditors are

needed to apply preliminary analytical review for the identification of the areas of higher risk

in final audit. Ratio analysis is considered as a major preliminary analytical process that

needs to be undertaken. The auditors are also required to undertake the analysis of the cash

flows with the aim to assess the going concern risk of the business. The main aim of this

report is analyse the above-discussed aspects of CSL Limited. CSL Limited is one of the

leading global biotech companies involves in researching, developing, manufacturing and

marketing of products for treating as well as preventing serious medical conditions of

humans. More specifically, the company develops and delivers innovative biotherapies and

influenza vaccines which save lives and help people from life-threating medical conditions.

This report also considers Sonic Healthcare as the similar company for comparing ratios.

Section 1

Determination of the Level of Materiality

Materiality is a fundamental concept of auditing and its application can be seen in the

audit planning stage and the stage when the auditors determine the impact of identified

material misstatements. Three steps needs to be followed by the auditors in materiality

determination and they are as follows:

Introduction

The main aim of the audit profession is to inspect and examine the financial records

and financial reports of the audit clients with the aim of find any kind of material

misstatement in them. It is important for the auditors to determine the level of materiality for

the audit of the group accounts as this materiality level assists the auditors in identifying the

materially misstated accounts in the financial statements (Griffiths, 2016). This needs to be

done by the auditors after taking into consideration the analysis of the financial statements

and associated draft notes. After the determination of level of materiality, the auditors are

needed to apply preliminary analytical review for the identification of the areas of higher risk

in final audit. Ratio analysis is considered as a major preliminary analytical process that

needs to be undertaken. The auditors are also required to undertake the analysis of the cash

flows with the aim to assess the going concern risk of the business. The main aim of this

report is analyse the above-discussed aspects of CSL Limited. CSL Limited is one of the

leading global biotech companies involves in researching, developing, manufacturing and

marketing of products for treating as well as preventing serious medical conditions of

humans. More specifically, the company develops and delivers innovative biotherapies and

influenza vaccines which save lives and help people from life-threating medical conditions.

This report also considers Sonic Healthcare as the similar company for comparing ratios.

Section 1

Determination of the Level of Materiality

Materiality is a fundamental concept of auditing and its application can be seen in the

audit planning stage and the stage when the auditors determine the impact of identified

material misstatements. Three steps needs to be followed by the auditors in materiality

determination and they are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

1. Relevant and appropriate benchmark or base selection.

2. Level of percentage selection.

3. Providing appropriate justification behind the above selections (Sunderland &

Trompeter, 2017).

These three steps need to be followed when determining the level of materiality of CSL

Limited for the year 2018; and the process is shown below.

Certain factors need to be considered at the time of the selection of the suitable

benchmark; nature of the business entity and the nature of the industry in which it operates

are two of the most crucial factors for the selection of benchmark. Expensive use of certain

benchmarks can be seen due to their suitability; they are profit before tax, gross profit, net

assets, total assets and others. It is suitable to take Profit before Tax (PBT) ($2281.1 million)

as the benchmark for the determination of level of materiality because it is a widely

acceptable benchmark in the industry in which the firm operates. After the determination of

suitable benchmark, it is needed for the auditor of CSL Limited to determine the suitable

percentage for materiality determination that needs to be charged on the selected base. It

needs to be mentioned that AASB 1031 Materiality is a crucial document that provides the

auditors with the necessary guidelines for the determination of materiality (Sarwoko &

Agoes, 2014). In case of the selection of the percentage, the auditor of CSL Limited can

select from the below options:

The auditor can chose an amount which is equal to or greater than 10 percent of the

appropriate base amount as material unless there is any contrary; and

The auditor can chose an amount which is equal to or less than 5 percent of the

appropriate base amount as material unless there is any contrary (aasb.gov.au, 2019).

1. Relevant and appropriate benchmark or base selection.

2. Level of percentage selection.

3. Providing appropriate justification behind the above selections (Sunderland &

Trompeter, 2017).

These three steps need to be followed when determining the level of materiality of CSL

Limited for the year 2018; and the process is shown below.

Certain factors need to be considered at the time of the selection of the suitable

benchmark; nature of the business entity and the nature of the industry in which it operates

are two of the most crucial factors for the selection of benchmark. Expensive use of certain

benchmarks can be seen due to their suitability; they are profit before tax, gross profit, net

assets, total assets and others. It is suitable to take Profit before Tax (PBT) ($2281.1 million)

as the benchmark for the determination of level of materiality because it is a widely

acceptable benchmark in the industry in which the firm operates. After the determination of

suitable benchmark, it is needed for the auditor of CSL Limited to determine the suitable

percentage for materiality determination that needs to be charged on the selected base. It

needs to be mentioned that AASB 1031 Materiality is a crucial document that provides the

auditors with the necessary guidelines for the determination of materiality (Sarwoko &

Agoes, 2014). In case of the selection of the percentage, the auditor of CSL Limited can

select from the below options:

The auditor can chose an amount which is equal to or greater than 10 percent of the

appropriate base amount as material unless there is any contrary; and

The auditor can chose an amount which is equal to or less than 5 percent of the

appropriate base amount as material unless there is any contrary (aasb.gov.au, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

The selection of the one item from the above largely depends on the professional

judgments of the auditors and the second option that is 5 percent is selected for the

materiality determination of CSL Limited which needs to be charged on the selected

benchmark that is PBT (Wee et al., 2016). Therefore, based on the above whole discussion,

determination of the level of materiality is illustrated below.

Overall Materiality = PBT × 5%

= $2281.1 × 5%

= $114 million (Approximately)

Review of Draft Notes and Disclosures

1. As per Note No. 13 (b), CSL Limited has been involved in litigation in the ordinary

courses of business due to a breach of contract. In order to tackle this, the company

has recognized a legal provision that would be utilized for settling the matter

(csl.com, 2019). Therefore, in case this contingent liability of CSL Limited becomes

due, there would be significant impact on the company’s financial outcome; and thus,

this matter needs to be considered for the final audit of CSL Limited. The audit

procedure for this would be to examine the legal documents of this liability for

determining the likelihood of becoming a major liability.

2. As per Note 4 Inventories, there are different factors that affect the recoverability of

the carrying value of inventory that includes regulatory approvals and future demands

of goods and products (csl.com, 2019). This makes the accounting treatment of

inventories in CSL Limited complex and it needs to be tested in the final audit. The

procedures that would be needed to undertake are assessment of the carrying value of

the inventories, conducting regular cycle count for testing the existence of the

The selection of the one item from the above largely depends on the professional

judgments of the auditors and the second option that is 5 percent is selected for the

materiality determination of CSL Limited which needs to be charged on the selected

benchmark that is PBT (Wee et al., 2016). Therefore, based on the above whole discussion,

determination of the level of materiality is illustrated below.

Overall Materiality = PBT × 5%

= $2281.1 × 5%

= $114 million (Approximately)

Review of Draft Notes and Disclosures

1. As per Note No. 13 (b), CSL Limited has been involved in litigation in the ordinary

courses of business due to a breach of contract. In order to tackle this, the company

has recognized a legal provision that would be utilized for settling the matter

(csl.com, 2019). Therefore, in case this contingent liability of CSL Limited becomes

due, there would be significant impact on the company’s financial outcome; and thus,

this matter needs to be considered for the final audit of CSL Limited. The audit

procedure for this would be to examine the legal documents of this liability for

determining the likelihood of becoming a major liability.

2. As per Note 4 Inventories, there are different factors that affect the recoverability of

the carrying value of inventory that includes regulatory approvals and future demands

of goods and products (csl.com, 2019). This makes the accounting treatment of

inventories in CSL Limited complex and it needs to be tested in the final audit. The

procedures that would be needed to undertake are assessment of the carrying value of

the inventories, conducting regular cycle count for testing the existence of the

5AUDITING AND ETHICS

inventory, assessment of the accuracy of the standards costing system that CSL

Limited used and others (Sarwoko & Agoes, 2014).

Section 2

Ratio analysis is considered as a major tool used in preliminary analytical review and

the same is applicable in CSL Limited. The following discussion shows the analysis of major

ratios of CSL Limited and Sonic Healthcare which is a similar company of CSL Limited.

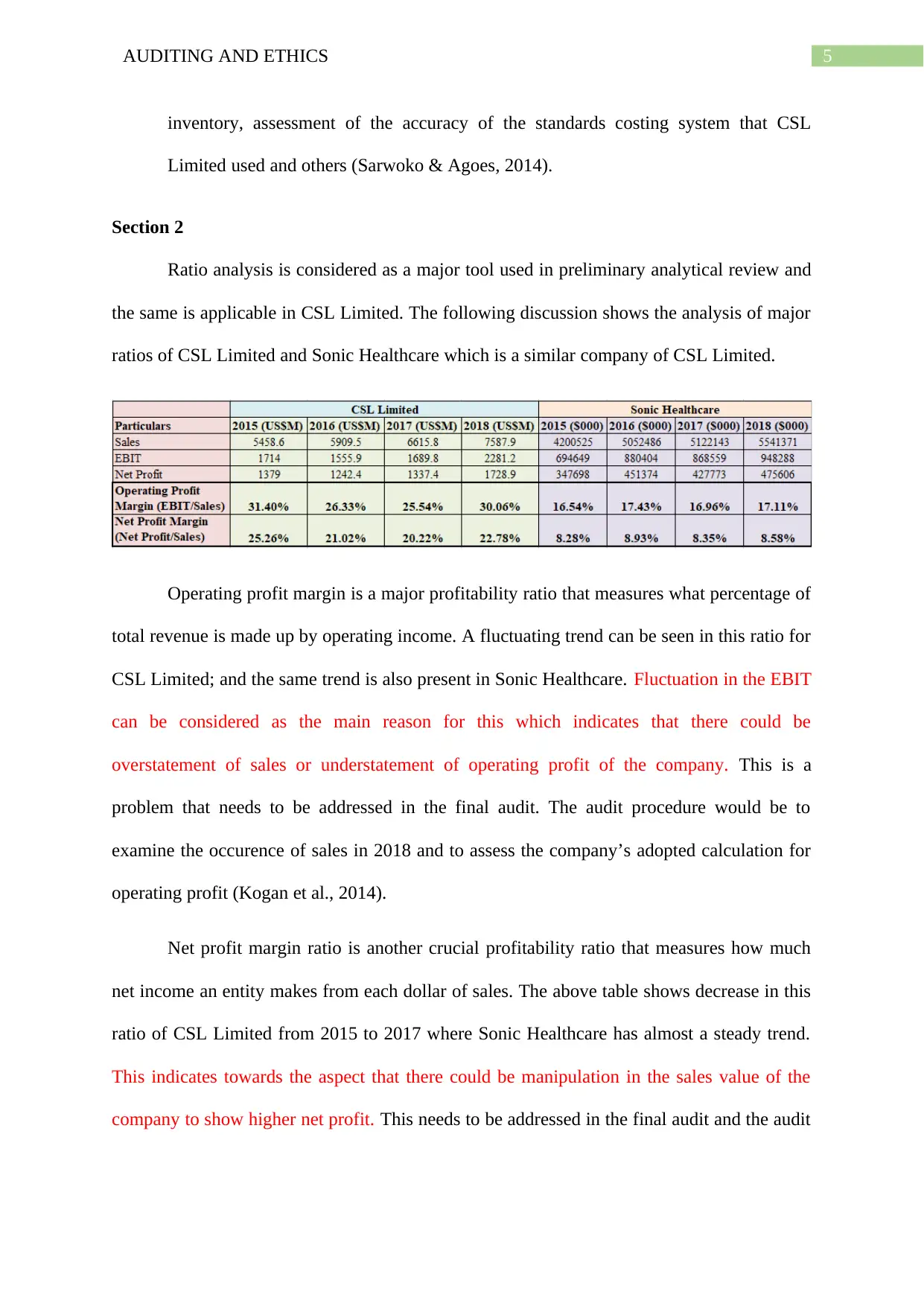

Operating profit margin is a major profitability ratio that measures what percentage of

total revenue is made up by operating income. A fluctuating trend can be seen in this ratio for

CSL Limited; and the same trend is also present in Sonic Healthcare. Fluctuation in the EBIT

can be considered as the main reason for this which indicates that there could be

overstatement of sales or understatement of operating profit of the company. This is a

problem that needs to be addressed in the final audit. The audit procedure would be to

examine the occurence of sales in 2018 and to assess the company’s adopted calculation for

operating profit (Kogan et al., 2014).

Net profit margin ratio is another crucial profitability ratio that measures how much

net income an entity makes from each dollar of sales. The above table shows decrease in this

ratio of CSL Limited from 2015 to 2017 where Sonic Healthcare has almost a steady trend.

This indicates towards the aspect that there could be manipulation in the sales value of the

company to show higher net profit. This needs to be addressed in the final audit and the audit

inventory, assessment of the accuracy of the standards costing system that CSL

Limited used and others (Sarwoko & Agoes, 2014).

Section 2

Ratio analysis is considered as a major tool used in preliminary analytical review and

the same is applicable in CSL Limited. The following discussion shows the analysis of major

ratios of CSL Limited and Sonic Healthcare which is a similar company of CSL Limited.

Operating profit margin is a major profitability ratio that measures what percentage of

total revenue is made up by operating income. A fluctuating trend can be seen in this ratio for

CSL Limited; and the same trend is also present in Sonic Healthcare. Fluctuation in the EBIT

can be considered as the main reason for this which indicates that there could be

overstatement of sales or understatement of operating profit of the company. This is a

problem that needs to be addressed in the final audit. The audit procedure would be to

examine the occurence of sales in 2018 and to assess the company’s adopted calculation for

operating profit (Kogan et al., 2014).

Net profit margin ratio is another crucial profitability ratio that measures how much

net income an entity makes from each dollar of sales. The above table shows decrease in this

ratio of CSL Limited from 2015 to 2017 where Sonic Healthcare has almost a steady trend.

This indicates towards the aspect that there could be manipulation in the sales value of the

company to show higher net profit. This needs to be addressed in the final audit and the audit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

procedures would be to trace the posting of individual sales invoices, reconciliation of cash

activities and others (Quadackers, Groot & Wright, 2014).

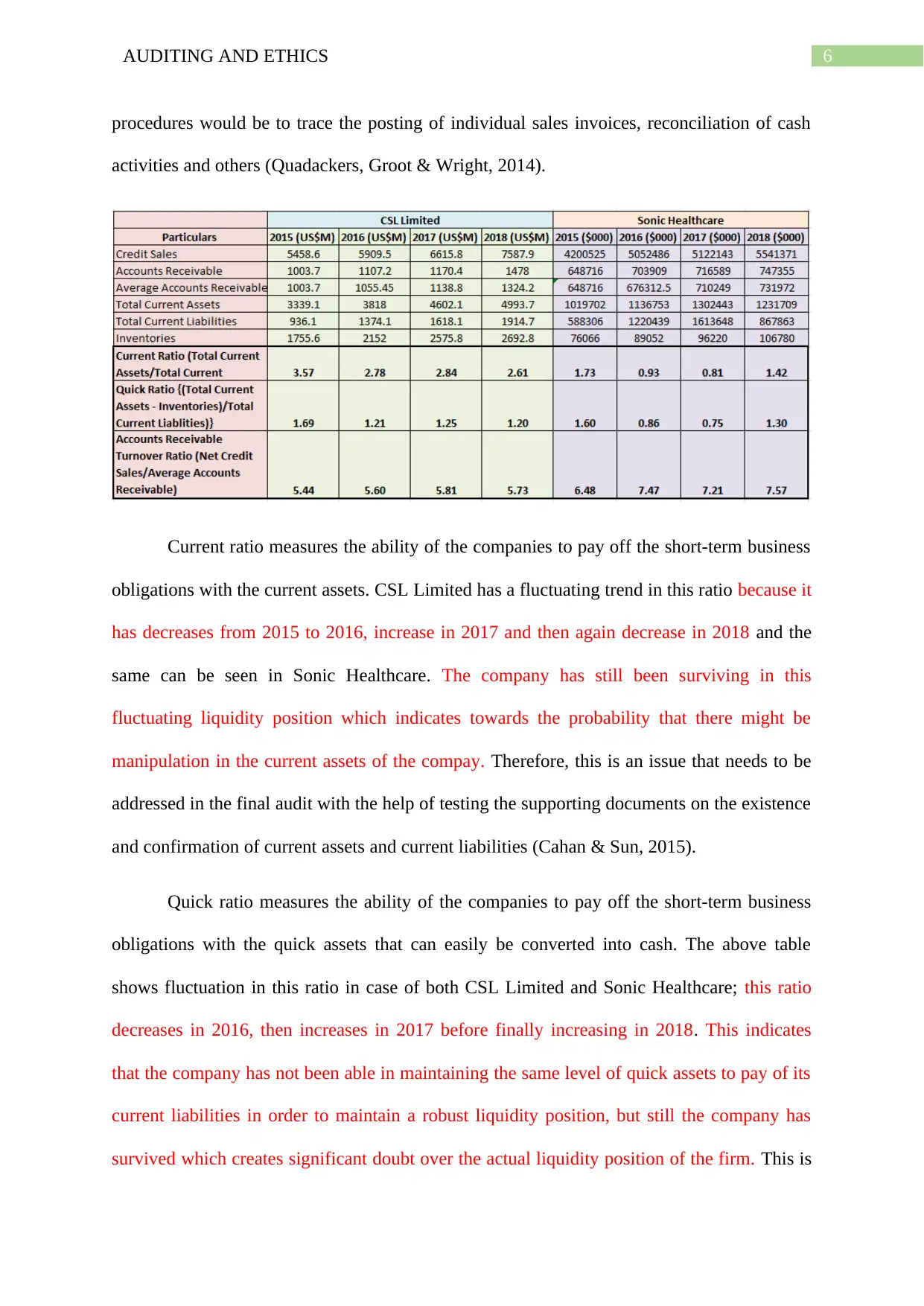

Current ratio measures the ability of the companies to pay off the short-term business

obligations with the current assets. CSL Limited has a fluctuating trend in this ratio because it

has decreases from 2015 to 2016, increase in 2017 and then again decrease in 2018 and the

same can be seen in Sonic Healthcare. The company has still been surviving in this

fluctuating liquidity position which indicates towards the probability that there might be

manipulation in the current assets of the compay. Therefore, this is an issue that needs to be

addressed in the final audit with the help of testing the supporting documents on the existence

and confirmation of current assets and current liabilities (Cahan & Sun, 2015).

Quick ratio measures the ability of the companies to pay off the short-term business

obligations with the quick assets that can easily be converted into cash. The above table

shows fluctuation in this ratio in case of both CSL Limited and Sonic Healthcare; this ratio

decreases in 2016, then increases in 2017 before finally increasing in 2018. This indicates

that the company has not been able in maintaining the same level of quick assets to pay of its

current liabilities in order to maintain a robust liquidity position, but still the company has

survived which creates significant doubt over the actual liquidity position of the firm. This is

procedures would be to trace the posting of individual sales invoices, reconciliation of cash

activities and others (Quadackers, Groot & Wright, 2014).

Current ratio measures the ability of the companies to pay off the short-term business

obligations with the current assets. CSL Limited has a fluctuating trend in this ratio because it

has decreases from 2015 to 2016, increase in 2017 and then again decrease in 2018 and the

same can be seen in Sonic Healthcare. The company has still been surviving in this

fluctuating liquidity position which indicates towards the probability that there might be

manipulation in the current assets of the compay. Therefore, this is an issue that needs to be

addressed in the final audit with the help of testing the supporting documents on the existence

and confirmation of current assets and current liabilities (Cahan & Sun, 2015).

Quick ratio measures the ability of the companies to pay off the short-term business

obligations with the quick assets that can easily be converted into cash. The above table

shows fluctuation in this ratio in case of both CSL Limited and Sonic Healthcare; this ratio

decreases in 2016, then increases in 2017 before finally increasing in 2018. This indicates

that the company has not been able in maintaining the same level of quick assets to pay of its

current liabilities in order to maintain a robust liquidity position, but still the company has

survived which creates significant doubt over the actual liquidity position of the firm. This is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

a problem area that needs to be addressed in the final audit and the audit procedures would be

test of cash transaction and the test of details of the accounts balances of liquid assets.

Accounts receivable turnover ratio is a major efficiency ratio that measures how many

times a business can collect its average accounts receivable during a year. The above table

shows slight fluctuation in this ratio of CSL Limited as it increases from 2015 to 2017 before

decreasing in 2018, but the fluctuation is higher in case of Sonic Healthcare. It implies that

the ability of the company to collect its average debtors has deteriorated in the current year

when the sales of the company has an increasing trend. This indicates towards the probability

of the presence of manipulation in the debtor’s values. This issue needs to be addressed in the

final audit with the help of debtor confirmation, examining collections of the cash receipts

journals, examining ageing schedule, reviewing adequacy of doubtful accounts and

performing sales and sales return cut off tests (Frost & Choo, 2017).

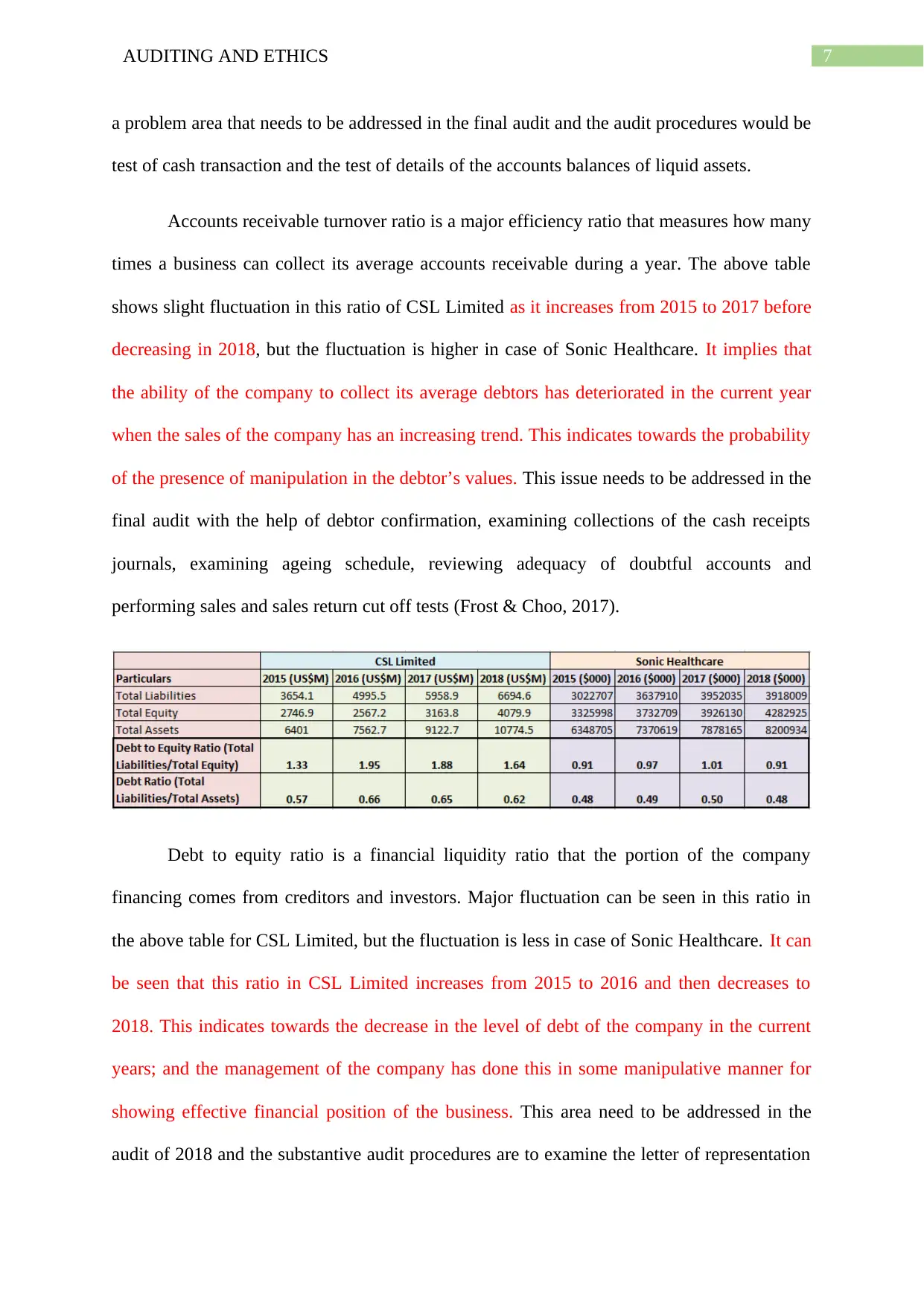

Debt to equity ratio is a financial liquidity ratio that the portion of the company

financing comes from creditors and investors. Major fluctuation can be seen in this ratio in

the above table for CSL Limited, but the fluctuation is less in case of Sonic Healthcare. It can

be seen that this ratio in CSL Limited increases from 2015 to 2016 and then decreases to

2018. This indicates towards the decrease in the level of debt of the company in the current

years; and the management of the company has done this in some manipulative manner for

showing effective financial position of the business. This area need to be addressed in the

audit of 2018 and the substantive audit procedures are to examine the letter of representation

a problem area that needs to be addressed in the final audit and the audit procedures would be

test of cash transaction and the test of details of the accounts balances of liquid assets.

Accounts receivable turnover ratio is a major efficiency ratio that measures how many

times a business can collect its average accounts receivable during a year. The above table

shows slight fluctuation in this ratio of CSL Limited as it increases from 2015 to 2017 before

decreasing in 2018, but the fluctuation is higher in case of Sonic Healthcare. It implies that

the ability of the company to collect its average debtors has deteriorated in the current year

when the sales of the company has an increasing trend. This indicates towards the probability

of the presence of manipulation in the debtor’s values. This issue needs to be addressed in the

final audit with the help of debtor confirmation, examining collections of the cash receipts

journals, examining ageing schedule, reviewing adequacy of doubtful accounts and

performing sales and sales return cut off tests (Frost & Choo, 2017).

Debt to equity ratio is a financial liquidity ratio that the portion of the company

financing comes from creditors and investors. Major fluctuation can be seen in this ratio in

the above table for CSL Limited, but the fluctuation is less in case of Sonic Healthcare. It can

be seen that this ratio in CSL Limited increases from 2015 to 2016 and then decreases to

2018. This indicates towards the decrease in the level of debt of the company in the current

years; and the management of the company has done this in some manipulative manner for

showing effective financial position of the business. This area need to be addressed in the

audit of 2018 and the substantive audit procedures are to examine the letter of representation

8AUDITING AND ETHICS

of term loans, to assess the covenant letters of the term loans, inspection with the bank

account for ensuring interest payment and others.

Debt ratio is a major solvency ratio that measures a firm’s total liabilities as a

percentage of total assets. A decreasing trend in this ratio can be seen in CSL Limited while

fluctuation can be seen in case of Sonic Healthcare. This ratio increases from 2015 to 2016,

then increases in 2017 and again decreases in 2018. It also indicates towards the reduction in

debt burden in the current year; and this could be the initiative of the management to

understate the value of long-term debts in fraud manner. This needs to be addressed in the

audit through the substantive and analytical audit procedures of testing the related documents

of the occurrence of the long-term debts (Kuenkaikaew, 2013).

Section 3

Statement of Cash Flows

The statement of cash flows or cash flows statement refers to a major financial

statement that summarizes the total amount of cash and cash equivalent inflowing and

outflowing the business. This helps in measuring the effectiveness of a company in managing

its cash position that its cash generating ability for paying its debt obligations and operating

expenses. Three categories of cash flows are there in a cash flows; they are operating

activities, investing activities and financing activities. The following discussion analyses

different aspects of the cash flow statement of CSL Limited.

The majority of cash inflows is provided by operating activities and the greatest cash

outflows are provided by investing activities (csl.com, 2019).

The primary cash receipts are receipts from customers and the primary cash payment

during the year is payment to suppliers and employees (csl.com, 2019).

of term loans, to assess the covenant letters of the term loans, inspection with the bank

account for ensuring interest payment and others.

Debt ratio is a major solvency ratio that measures a firm’s total liabilities as a

percentage of total assets. A decreasing trend in this ratio can be seen in CSL Limited while

fluctuation can be seen in case of Sonic Healthcare. This ratio increases from 2015 to 2016,

then increases in 2017 and again decreases in 2018. It also indicates towards the reduction in

debt burden in the current year; and this could be the initiative of the management to

understate the value of long-term debts in fraud manner. This needs to be addressed in the

audit through the substantive and analytical audit procedures of testing the related documents

of the occurrence of the long-term debts (Kuenkaikaew, 2013).

Section 3

Statement of Cash Flows

The statement of cash flows or cash flows statement refers to a major financial

statement that summarizes the total amount of cash and cash equivalent inflowing and

outflowing the business. This helps in measuring the effectiveness of a company in managing

its cash position that its cash generating ability for paying its debt obligations and operating

expenses. Three categories of cash flows are there in a cash flows; they are operating

activities, investing activities and financing activities. The following discussion analyses

different aspects of the cash flow statement of CSL Limited.

The majority of cash inflows is provided by operating activities and the greatest cash

outflows are provided by investing activities (csl.com, 2019).

The primary cash receipts are receipts from customers and the primary cash payment

during the year is payment to suppliers and employees (csl.com, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

There were not any non-cash financial and investing activities in the cash flow of CSL

Limited (csl.com, 2019).

As per the above analysis, positive cash inflow is a strong indicator of the fact that the

core business operations of CSL Limited have been able in fetching adequate cash

flows for the company that is a major need for any company’s survival. Investing

activities include the payments for fixed assets, intangible assets, new business

acquisition and other financial assets and liabilities which indicates CSL Limited’s

intention to invest for its future. Investing activities include issue of share, payment of

dividend, payment as well as proceeds from borrowings and others. All these aspects

show string present and future operation of CSL Limited which eliminates any going

concern risk (Sundgren & Svanström, 2014).

In order to address the going concern risk, the audit procedure would be gathering

adequate evidence on the presence of any event or incident that can create major

threat to the going concern status of the firm. In addition, adequate evidence needs to

be gathered on the fact that whether the management is appropriate using the going

concern basis of accounting (Omer, Sharp & Wang, 2018).

Audit Report

As per the independent auditor’s report, the financial statements of CSL Limited that

are in compliance with the Corporations Act 2001 provides true and fair view of the

consolidated financial position and performance of the company; and they have been

prepared in accordance with Australian Accounting Standards and the Corporations

Regulations 2001 (csl.com, 2019). Based on this, it can be said that Unqualified Audit

Opinion is suitable for CSL Limited that is issued when the financial statements of a

company are presented fairly and appropriately in the absence of any identified

exceptions and in adherence with the appropriate accounting rules and principles

There were not any non-cash financial and investing activities in the cash flow of CSL

Limited (csl.com, 2019).

As per the above analysis, positive cash inflow is a strong indicator of the fact that the

core business operations of CSL Limited have been able in fetching adequate cash

flows for the company that is a major need for any company’s survival. Investing

activities include the payments for fixed assets, intangible assets, new business

acquisition and other financial assets and liabilities which indicates CSL Limited’s

intention to invest for its future. Investing activities include issue of share, payment of

dividend, payment as well as proceeds from borrowings and others. All these aspects

show string present and future operation of CSL Limited which eliminates any going

concern risk (Sundgren & Svanström, 2014).

In order to address the going concern risk, the audit procedure would be gathering

adequate evidence on the presence of any event or incident that can create major

threat to the going concern status of the firm. In addition, adequate evidence needs to

be gathered on the fact that whether the management is appropriate using the going

concern basis of accounting (Omer, Sharp & Wang, 2018).

Audit Report

As per the independent auditor’s report, the financial statements of CSL Limited that

are in compliance with the Corporations Act 2001 provides true and fair view of the

consolidated financial position and performance of the company; and they have been

prepared in accordance with Australian Accounting Standards and the Corporations

Regulations 2001 (csl.com, 2019). Based on this, it can be said that Unqualified Audit

Opinion is suitable for CSL Limited that is issued when the financial statements of a

company are presented fairly and appropriately in the absence of any identified

exceptions and in adherence with the appropriate accounting rules and principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

(Daoud et al., 2014). The same aspect can be seen in case of CSL Limited as the

auditors have mentioned that the management has complied with the required

accounting standards and they reflect true and fair view. In addition, there is not any

material misstatement in the financial statements of the company. These are the

reasons of providing unqualified audit opinion to CSL Limited.

There is a section in the audit report of CSL Limited named “Key Audit Matters” that

includes certain issues that the auditors considered most significant in the audit of the

company. These issues are related to 1) existence and valuation of inventory, 2)

accounting for acquisition for Ruide and Calimmune, and 3) complexities in taxation

(csl.com, 2019). The auditors have taken appropriate audit measures to address these

issues as a whole in the audit of CSL Limited (Cordoş & Fülöp, 2015).

Conclusion

It can be seen from the above discussion that the auditors are needed to follows

certain steps for the determination of level of materiality; such as the selection of appropriate

benchmark, appropriate percentage and providing the necessary justification. The analysis

shows that preliminary analytical review with the help of the analysis of relevant ratios which

is majorly helpful in the detection of problem areas that need to be addressed in the final

audit. Moreover, this assists in the determination of the audit procedures that need be

undertaken. The last part shows that unqualified audit report needs to be issued when the

financial statements are well complied with appropriate accounting standards and provide

true as well as fair view of financial performance and position.

(Daoud et al., 2014). The same aspect can be seen in case of CSL Limited as the

auditors have mentioned that the management has complied with the required

accounting standards and they reflect true and fair view. In addition, there is not any

material misstatement in the financial statements of the company. These are the

reasons of providing unqualified audit opinion to CSL Limited.

There is a section in the audit report of CSL Limited named “Key Audit Matters” that

includes certain issues that the auditors considered most significant in the audit of the

company. These issues are related to 1) existence and valuation of inventory, 2)

accounting for acquisition for Ruide and Calimmune, and 3) complexities in taxation

(csl.com, 2019). The auditors have taken appropriate audit measures to address these

issues as a whole in the audit of CSL Limited (Cordoş & Fülöp, 2015).

Conclusion

It can be seen from the above discussion that the auditors are needed to follows

certain steps for the determination of level of materiality; such as the selection of appropriate

benchmark, appropriate percentage and providing the necessary justification. The analysis

shows that preliminary analytical review with the help of the analysis of relevant ratios which

is majorly helpful in the detection of problem areas that need to be addressed in the final

audit. Moreover, this assists in the determination of the audit procedures that need be

undertaken. The last part shows that unqualified audit report needs to be issued when the

financial statements are well complied with appropriate accounting standards and provide

true as well as fair view of financial performance and position.

11AUDITING AND ETHICS

References

Aasb.gov.au. (2019). Materiality. Retrieved 24 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Cahan, S. F., & Sun, J. (2015). The effect of audit experience on audit fees and audit

quality. Journal of Accounting, Auditing & Finance, 30(1), 78-100.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Csl.com. (2019). CSL Limited Annual Report 2017/18. Retrieved 30 August 2019, from

https://www.csl.com/-/media/csl/documents/annual-report-docs/csl-ltd-annual-report-

2018-full.pdf

Daoud, K. A. A., Ismail, K., Izah, K. N., & Lode, N. A. (2014). The timeliness of financial

reporting among Jordanian companies: do company and board characteristics, and

audit opinion matter?. Asian Social Science, 10(13), 191-201.

Frost, R. B., & Choo, C. W. (2017). Revisiting the information audit: A systematic literature

review and synthesis. International Journal of Information Management, 37(1), 1380-

1390.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Kogan, A., Alles, M. G., Vasarhelyi, M. A., & Wu, J. (2014). Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice &

Theory, 33(4), 221-245.

References

Aasb.gov.au. (2019). Materiality. Retrieved 24 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Cahan, S. F., & Sun, J. (2015). The effect of audit experience on audit fees and audit

quality. Journal of Accounting, Auditing & Finance, 30(1), 78-100.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Csl.com. (2019). CSL Limited Annual Report 2017/18. Retrieved 30 August 2019, from

https://www.csl.com/-/media/csl/documents/annual-report-docs/csl-ltd-annual-report-

2018-full.pdf

Daoud, K. A. A., Ismail, K., Izah, K. N., & Lode, N. A. (2014). The timeliness of financial

reporting among Jordanian companies: do company and board characteristics, and

audit opinion matter?. Asian Social Science, 10(13), 191-201.

Frost, R. B., & Choo, C. W. (2017). Revisiting the information audit: A systematic literature

review and synthesis. International Journal of Information Management, 37(1), 1380-

1390.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Kogan, A., Alles, M. G., Vasarhelyi, M. A., & Wu, J. (2014). Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice &

Theory, 33(4), 221-245.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.