CSL Limited & AASB: Analysis of Contemporary Accounting Issues

VerifiedAdded on 2023/06/14

|18

|2255

|122

Report

AI Summary

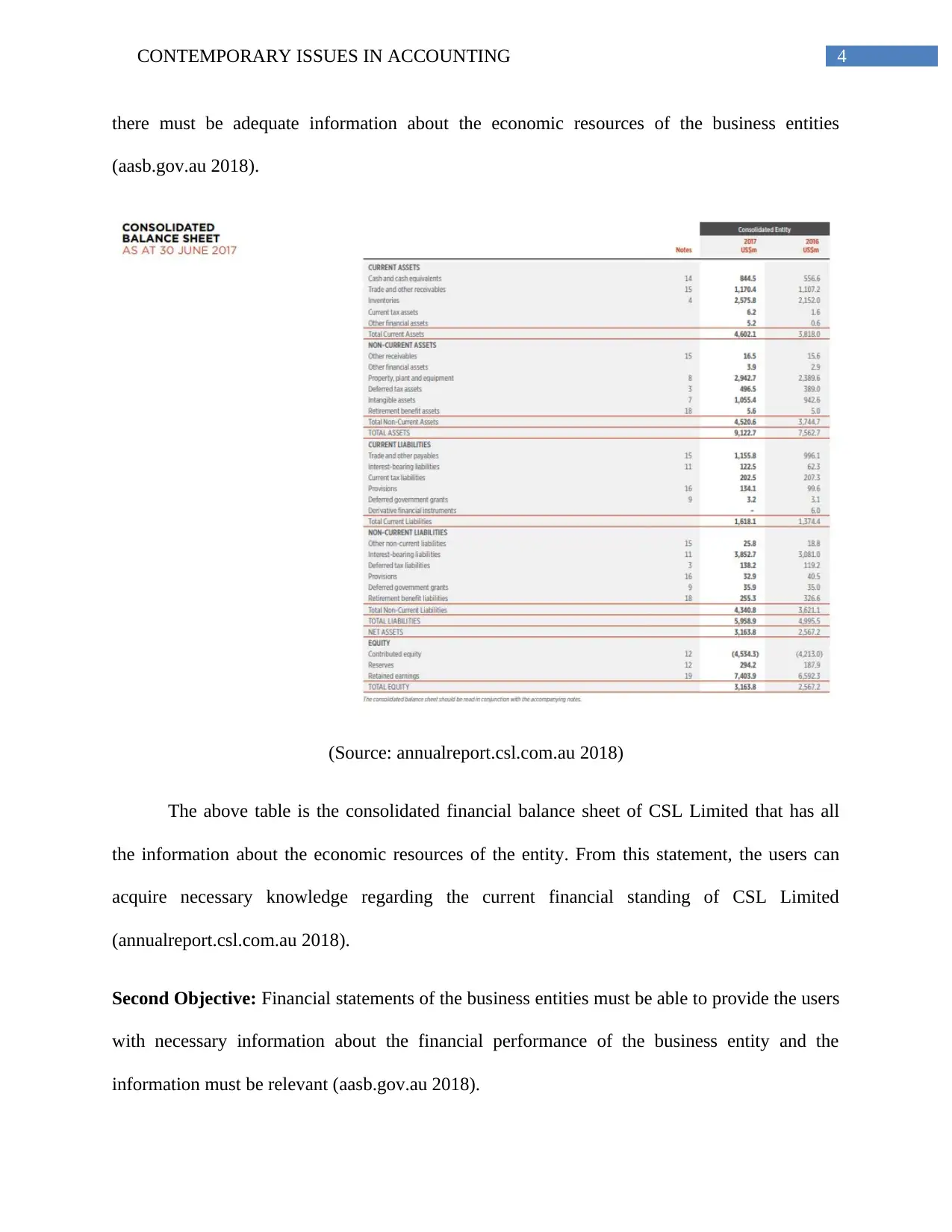

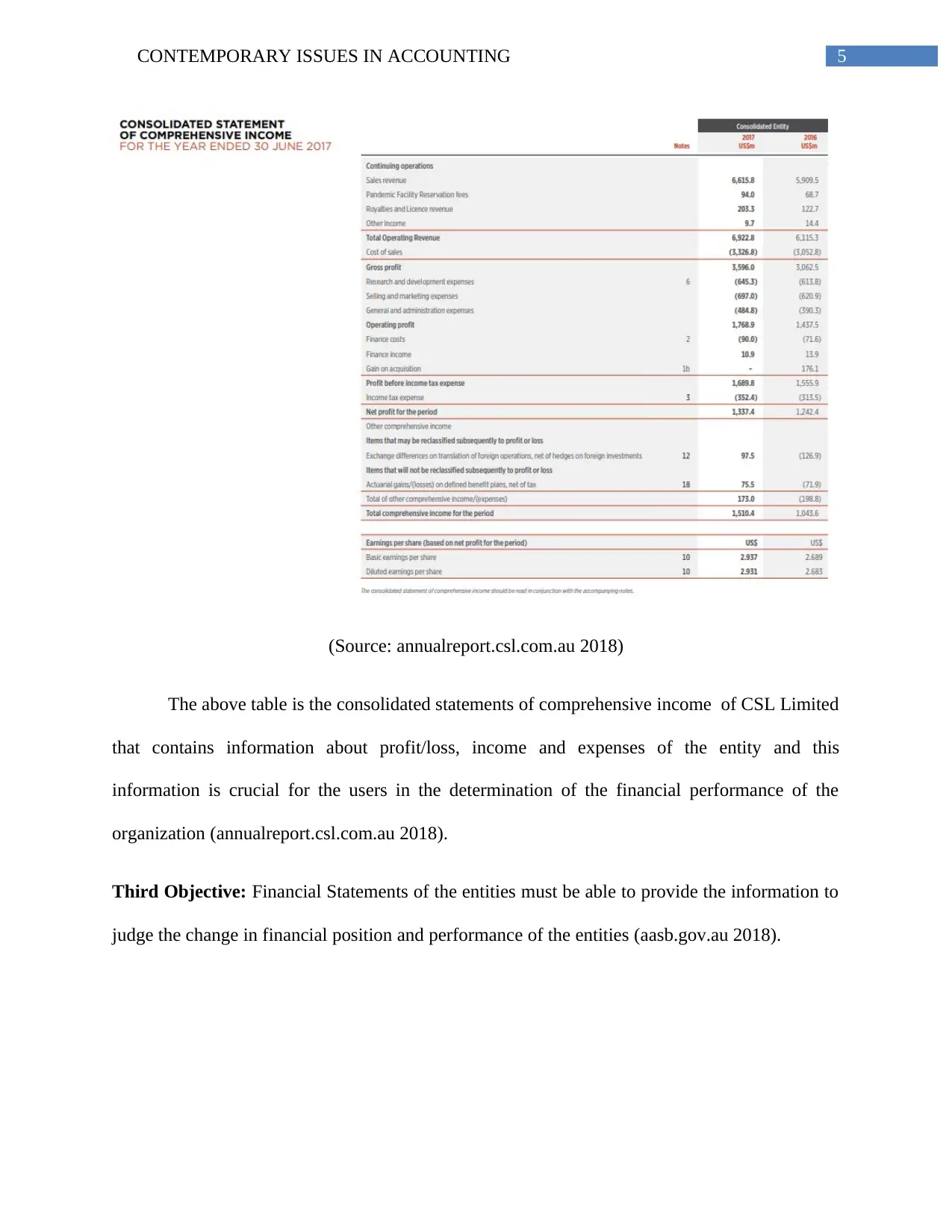

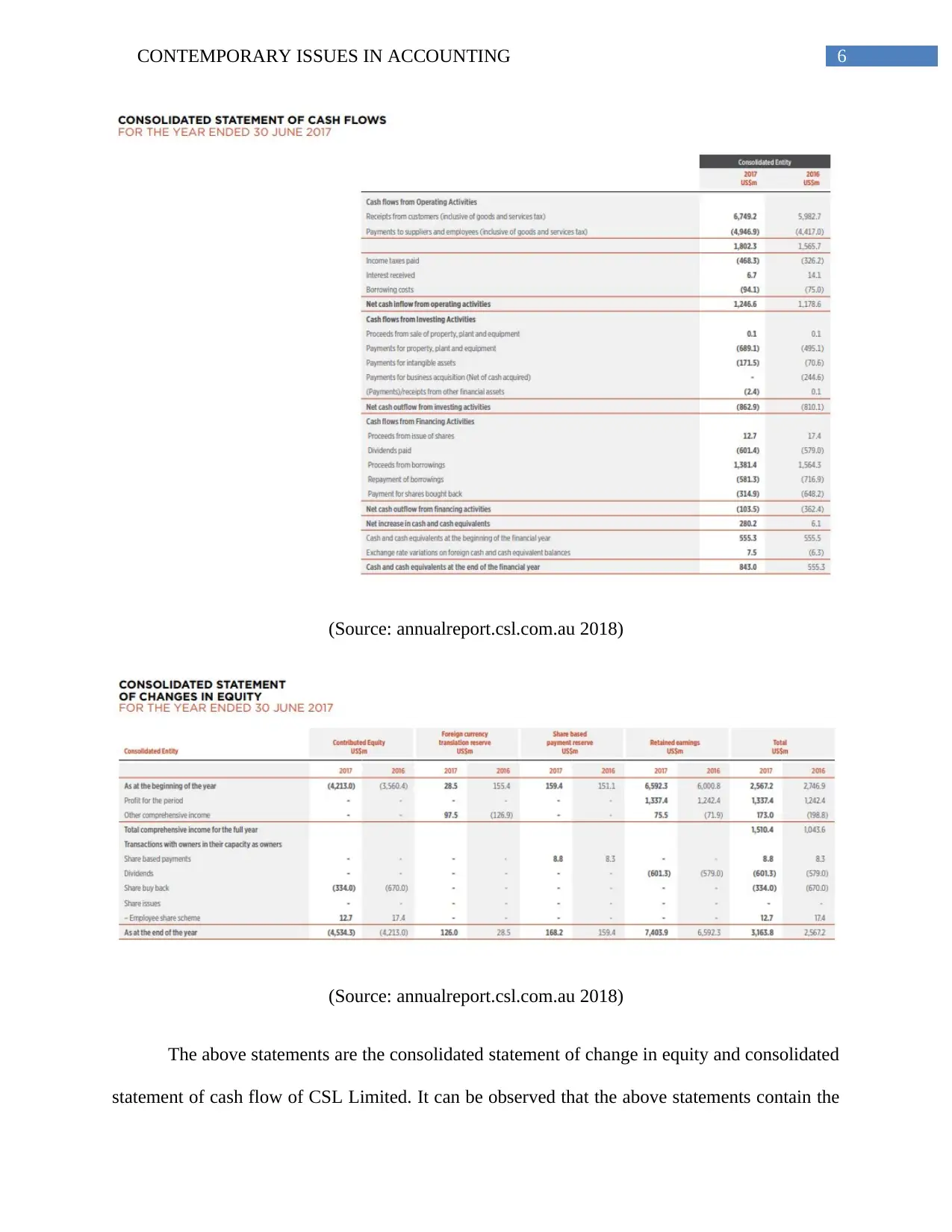

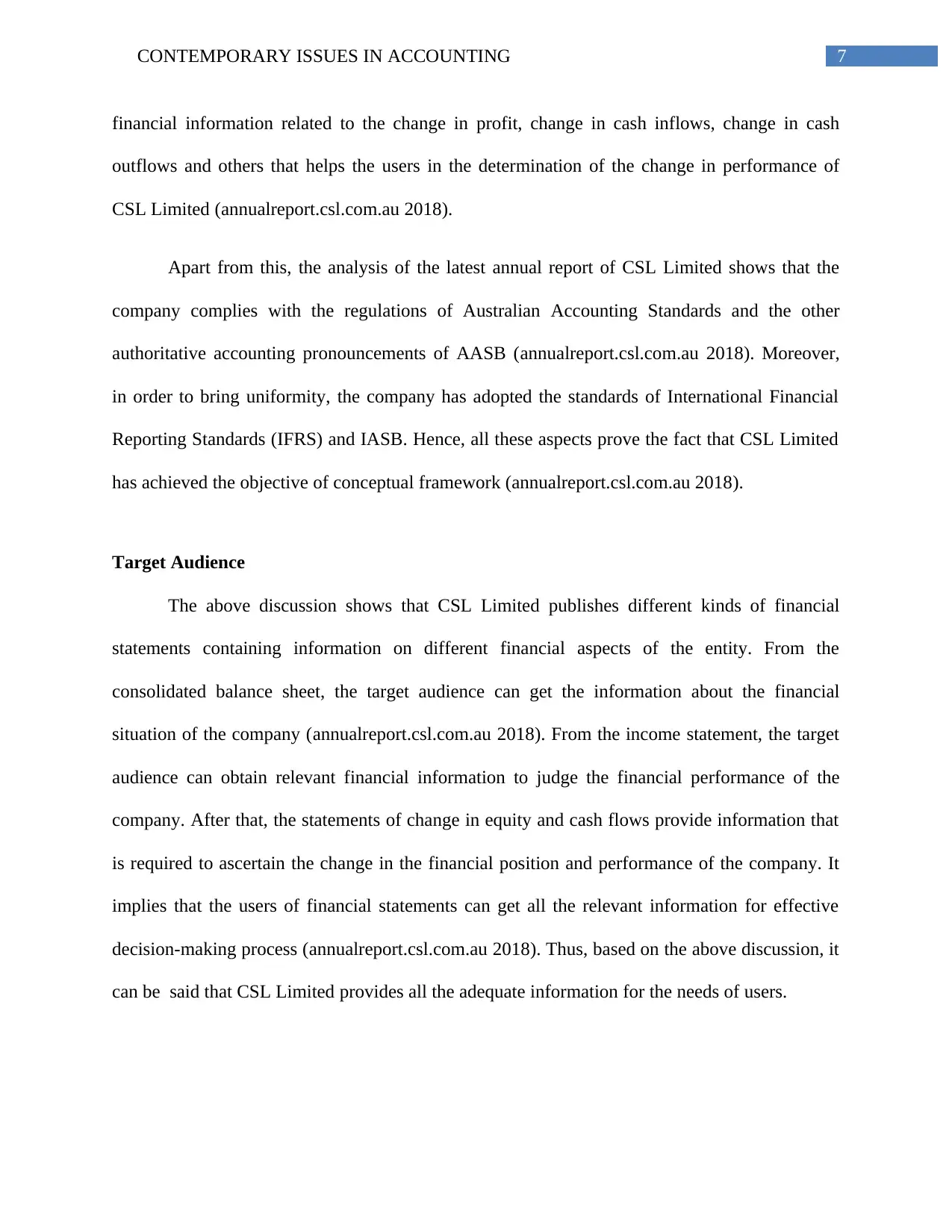

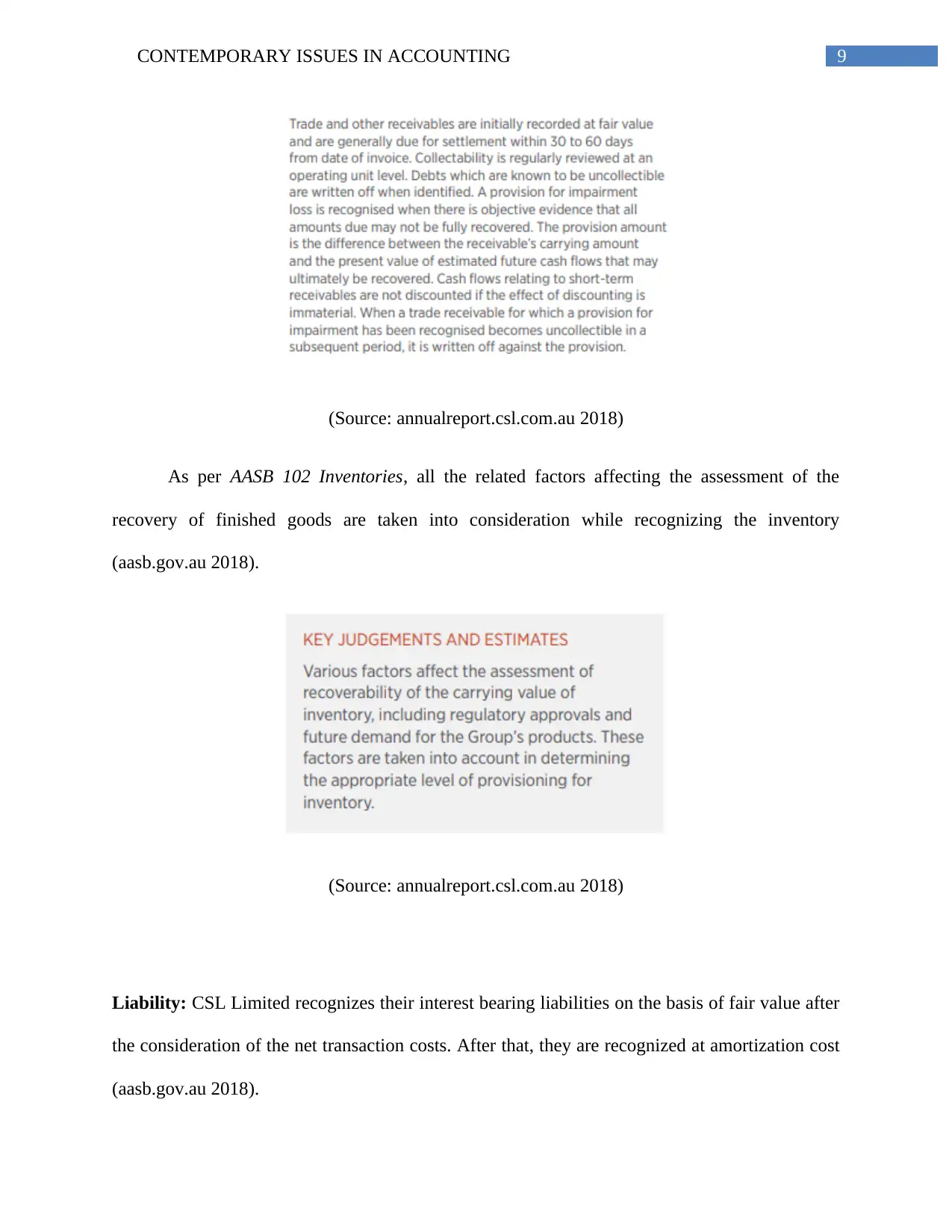

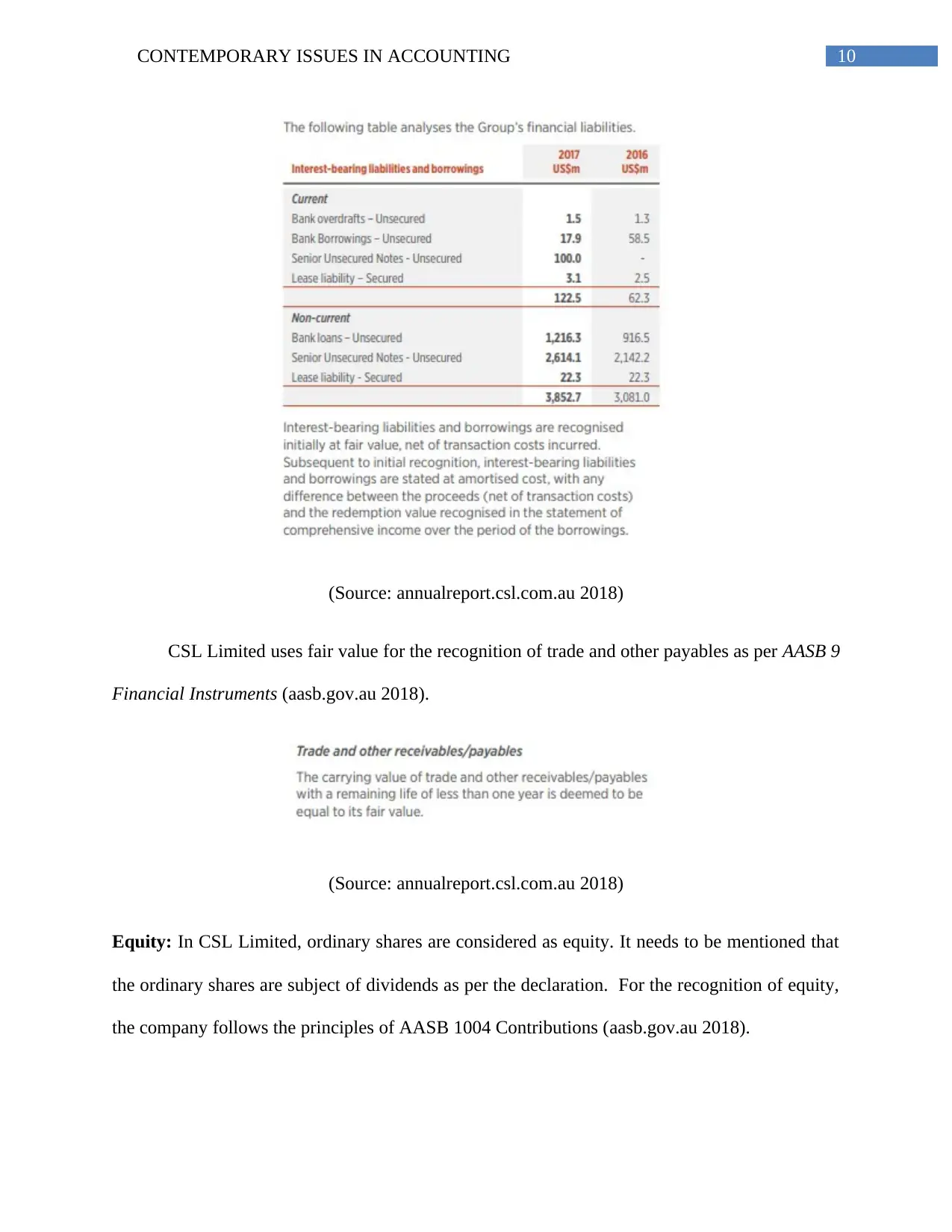

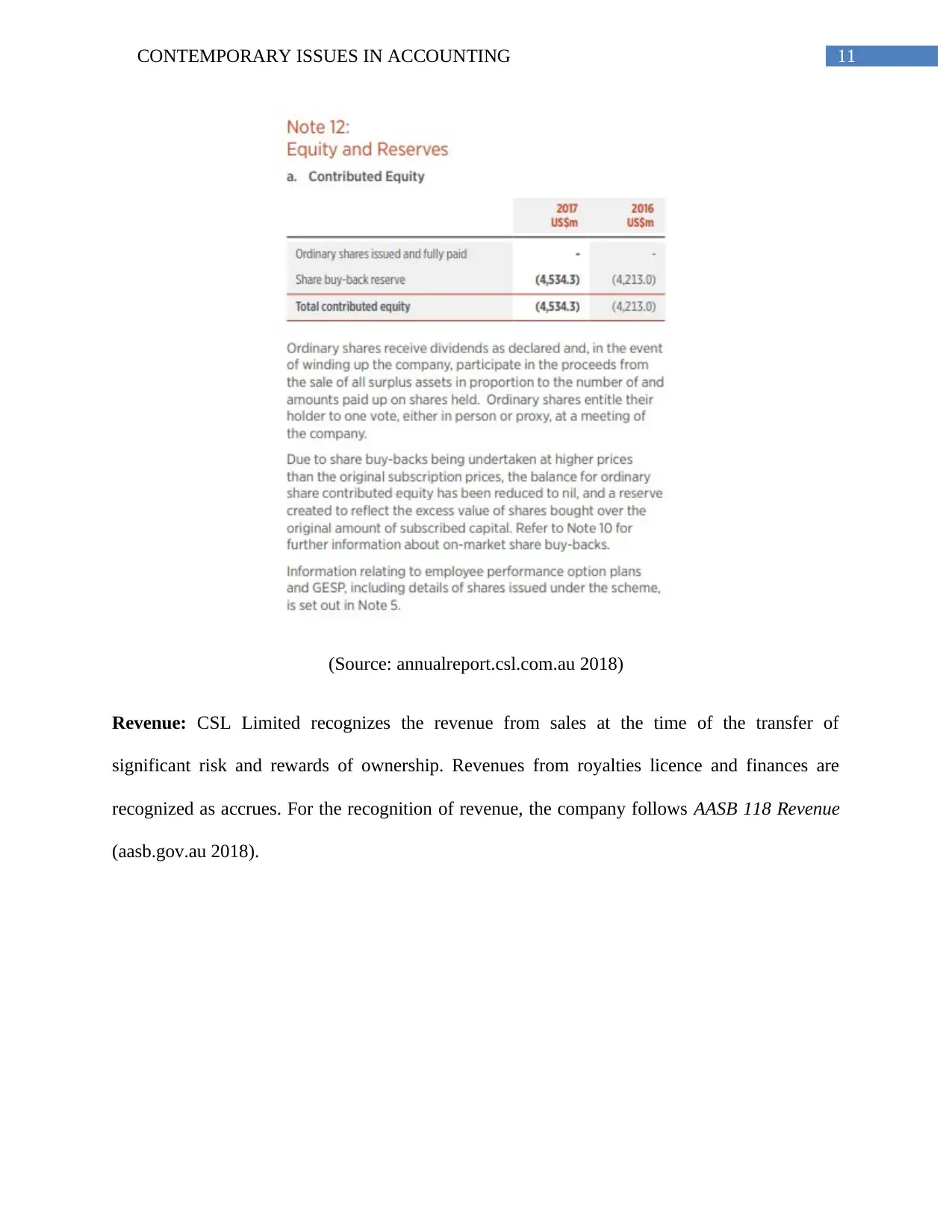

This report provides an in-depth analysis of CSL Limited's compliance with the Australian Accounting Standards Board (AASB) conceptual framework. It examines the achievement of conceptual framework objectives through a review of CSL Limited's consolidated balance sheet, income statement, statement of changes in equity, and cash flow statement, demonstrating the company's commitment to providing relevant financial information to its target audience. The report also evaluates CSL Limited's adherence to recognition criteria for assets, liabilities, equity, revenue, and expenses, referencing specific AASB standards such as AASB 116, AASB 138, AASB 9, AASB 102, AASB 1004, and AASB 118. Furthermore, the analysis extends to the fundamental qualitative characteristics (relevance and faithful representation) and enhancing qualitative characteristics (comparability, verifiability, timeliness, and understandability) of the financial information presented by CSL Limited, concluding that the company effectively complies with AASB standards, minimizing potential accounting issues.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.