Auditing and Assurance: A Detailed Analysis of CSL Limited's Audit

VerifiedAdded on 2023/06/04

|15

|3356

|429

Report

AI Summary

This report provides an analysis of CSL Limited's audit and assurance practices, focusing on key audit matters as per ASA 701 and the Audit Committee's reporting requirements. It examines the auditor's independence declaration, independent auditor's report, and non-audit services provided. A comparative analysis of auditor remuneration from 2016 to 2017 highlights changes in payments for audit and non-audit services. The report also discusses audit procedures performed for key audit matters, the structure and functions of the Audit and Risk Management Committee, and the roles and responsibilities of auditors. Furthermore, it addresses material subsequent events and the differing responsibilities of directors, management, and auditors in relation to financial reporting. The report concludes with potential follow-up questions for the auditor at the company's Annual General Meeting, offering a comprehensive overview of CSL Limited's auditing environment.

AUDITING & ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The CBL Limited attempts to feature new audit functions as per the new reporting of Audit

committee, 2016. ASA 701 is concerned to communicate key audit matters as per the

independent auditor’s report. The responsibility of an auditor has more focused to

communicate the key audit committee explained in the report especially after 2016. The aim

of communicating the key matters is to increase the communication among the shareholders.

The CBL Limited attempts to feature new audit functions as per the new reporting of Audit

committee, 2016. ASA 701 is concerned to communicate key audit matters as per the

independent auditor’s report. The responsibility of an auditor has more focused to

communicate the key audit committee explained in the report especially after 2016. The aim

of communicating the key matters is to increase the communication among the shareholders.

Contents

Executive summary....................................................................................................................1

Introduction................................................................................................................................3

Introduction of the company......................................................................................................3

Auditor’s Independence Declaration..........................................................................................4

Independent auditor’s report......................................................................................................4

Non-audit services provided by auditor.....................................................................................4

Analysis of the each Auditor remuneration as compared to the previous year..........................5

A comparative analysis of total remuneration of auditors as compared to the previous year. . .6

Audit Procedures Performed For Key Audit Matters................................................................7

Structure of Audit and risk management committee..................................................................8

Functions of Auditor..................................................................................................................8

Roles and Responsibilities of the Audit Committee..................................................................9

Material subsequent events by the CSL limited.........................................................................9

The Directors and Management’s responsibilities differ from the Auditor’s responsibilities in

relation to the financial report..................................................................................................10

Follow-up questions would you ask the Auditor at the company’s Annual General Meeting 10

Conclusion................................................................................................................................10

References................................................................................................................................12

Executive summary....................................................................................................................1

Introduction................................................................................................................................3

Introduction of the company......................................................................................................3

Auditor’s Independence Declaration..........................................................................................4

Independent auditor’s report......................................................................................................4

Non-audit services provided by auditor.....................................................................................4

Analysis of the each Auditor remuneration as compared to the previous year..........................5

A comparative analysis of total remuneration of auditors as compared to the previous year. . .6

Audit Procedures Performed For Key Audit Matters................................................................7

Structure of Audit and risk management committee..................................................................8

Functions of Auditor..................................................................................................................8

Roles and Responsibilities of the Audit Committee..................................................................9

Material subsequent events by the CSL limited.........................................................................9

The Directors and Management’s responsibilities differ from the Auditor’s responsibilities in

relation to the financial report..................................................................................................10

Follow-up questions would you ask the Auditor at the company’s Annual General Meeting 10

Conclusion................................................................................................................................10

References................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

In the current changing business environment, organisations use fraudulent measures to

achieve more profit and attract more public to invest in their company. To overcome the

problem of fraud in business, auditors are appointed to check and review the financial

accounts of a company. The company, which is chosen to, analyses the effect of auditors and

non-audit services is CSL limited. CSL limited is a biotherapeuitics company, which deals in

manufacturing of medicines and other curing products such as vaccination products. The

report brings out the brief description of Auditor`s independence declaration, Independent

auditor’s report especially for shareholders. Moreover, the annual reports analysed the

remuneration of auditors for both audit as well as non-audit services. After the modification

in the duties of auditors, the responsibilities of auditors has been changed in Australia. The

report discusses the audit Procedures Performed for Key Audit Matters (Deumeset al., 2012).

Introduction of the company

CSL limited is a biotherapeutics entity who undertakes the manufacturing of allied products

and delivers biotherapies. CSL limited is a world specialty biotechnical organisation that

finds, develops, manufactures, and advertise the products to treat serious human health

problems. The company operate segments named CSL Behring, CSL intellectual property,

and Seqirus. All the segments perform different operation such as CSL Behring produces and

distributes plasma products and recombinants. Seqirus segment produces and delivers non-

plasma biotechnical products. Moreover, this segment also produces a wide range of

antivenoms, vaccination products, and pharmaceutical products in New Zealand and

Australia. The intellectual segments of CSL is involved in licensing the intellectual property

created by the organisation to the third unrelated party. The company operates its facility in

Germany, U.K., U.S., Switzerland, and Australia.

In the current changing business environment, organisations use fraudulent measures to

achieve more profit and attract more public to invest in their company. To overcome the

problem of fraud in business, auditors are appointed to check and review the financial

accounts of a company. The company, which is chosen to, analyses the effect of auditors and

non-audit services is CSL limited. CSL limited is a biotherapeuitics company, which deals in

manufacturing of medicines and other curing products such as vaccination products. The

report brings out the brief description of Auditor`s independence declaration, Independent

auditor’s report especially for shareholders. Moreover, the annual reports analysed the

remuneration of auditors for both audit as well as non-audit services. After the modification

in the duties of auditors, the responsibilities of auditors has been changed in Australia. The

report discusses the audit Procedures Performed for Key Audit Matters (Deumeset al., 2012).

Introduction of the company

CSL limited is a biotherapeutics entity who undertakes the manufacturing of allied products

and delivers biotherapies. CSL limited is a world specialty biotechnical organisation that

finds, develops, manufactures, and advertise the products to treat serious human health

problems. The company operate segments named CSL Behring, CSL intellectual property,

and Seqirus. All the segments perform different operation such as CSL Behring produces and

distributes plasma products and recombinants. Seqirus segment produces and delivers non-

plasma biotechnical products. Moreover, this segment also produces a wide range of

antivenoms, vaccination products, and pharmaceutical products in New Zealand and

Australia. The intellectual segments of CSL is involved in licensing the intellectual property

created by the organisation to the third unrelated party. The company operates its facility in

Germany, U.K., U.S., Switzerland, and Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditor’s Independence Declaration

The company has a clear declaration of auditor`s independence declaration as per the

requirement of section 307C of the Corporation Act, 2001. Until now to the knowledge and

belief of directors, there are no contraventions by auditor for their independence or any other

applicable code of conduct based on professionals. Although, as of now no payment has been

made to E&Y as an indemnified cost during this fiscal year (CSL limited 2016).

Moreover, the CSL limited has agreed to indemnify the auditors to the extent to which it is

permitted by the law. E&Y as a part of external auditors in terms of engagement agreement

against the claims with the third party for a particular amount that has raised from the audit.

Indemnification refers to an agreement between one party where the monetary costs can be

reimbursed incurred by any second party (CSL limited 2017).

Independent auditor’s report (shareholders)

A group of external auditor attends every annual general meeting because they are available

to provide a solution to shareholders regarding audit procedures. Shareholders are allowed to

ask the relevant questions regarding the preparation and relevance to each item in the

financial statement and how far it can contribute to profit making from the report from the

auditors (Cannon and Bedard, 2016).

Non-audit services provided

Bowlin, Hobson, and Piercey, 2015)

Clikeman, 2018)Roy and Saha, 2018)Byrnes et al., 2018)decision-making. Non-audit

services include advocate for CSL or jointly sharing the risk and the rewards. Ernst & Young

and its non-audit services

CSL limited 2017

The company has a clear declaration of auditor`s independence declaration as per the

requirement of section 307C of the Corporation Act, 2001. Until now to the knowledge and

belief of directors, there are no contraventions by auditor for their independence or any other

applicable code of conduct based on professionals. Although, as of now no payment has been

made to E&Y as an indemnified cost during this fiscal year (CSL limited 2016).

Moreover, the CSL limited has agreed to indemnify the auditors to the extent to which it is

permitted by the law. E&Y as a part of external auditors in terms of engagement agreement

against the claims with the third party for a particular amount that has raised from the audit.

Indemnification refers to an agreement between one party where the monetary costs can be

reimbursed incurred by any second party (CSL limited 2017).

Independent auditor’s report (shareholders)

A group of external auditor attends every annual general meeting because they are available

to provide a solution to shareholders regarding audit procedures. Shareholders are allowed to

ask the relevant questions regarding the preparation and relevance to each item in the

financial statement and how far it can contribute to profit making from the report from the

auditors (Cannon and Bedard, 2016).

Non-audit services provided

Bowlin, Hobson, and Piercey, 2015)

Clikeman, 2018)Roy and Saha, 2018)Byrnes et al., 2018)decision-making. Non-audit

services include advocate for CSL or jointly sharing the risk and the rewards. Ernst & Young

and its non-audit services

CSL limited 2017

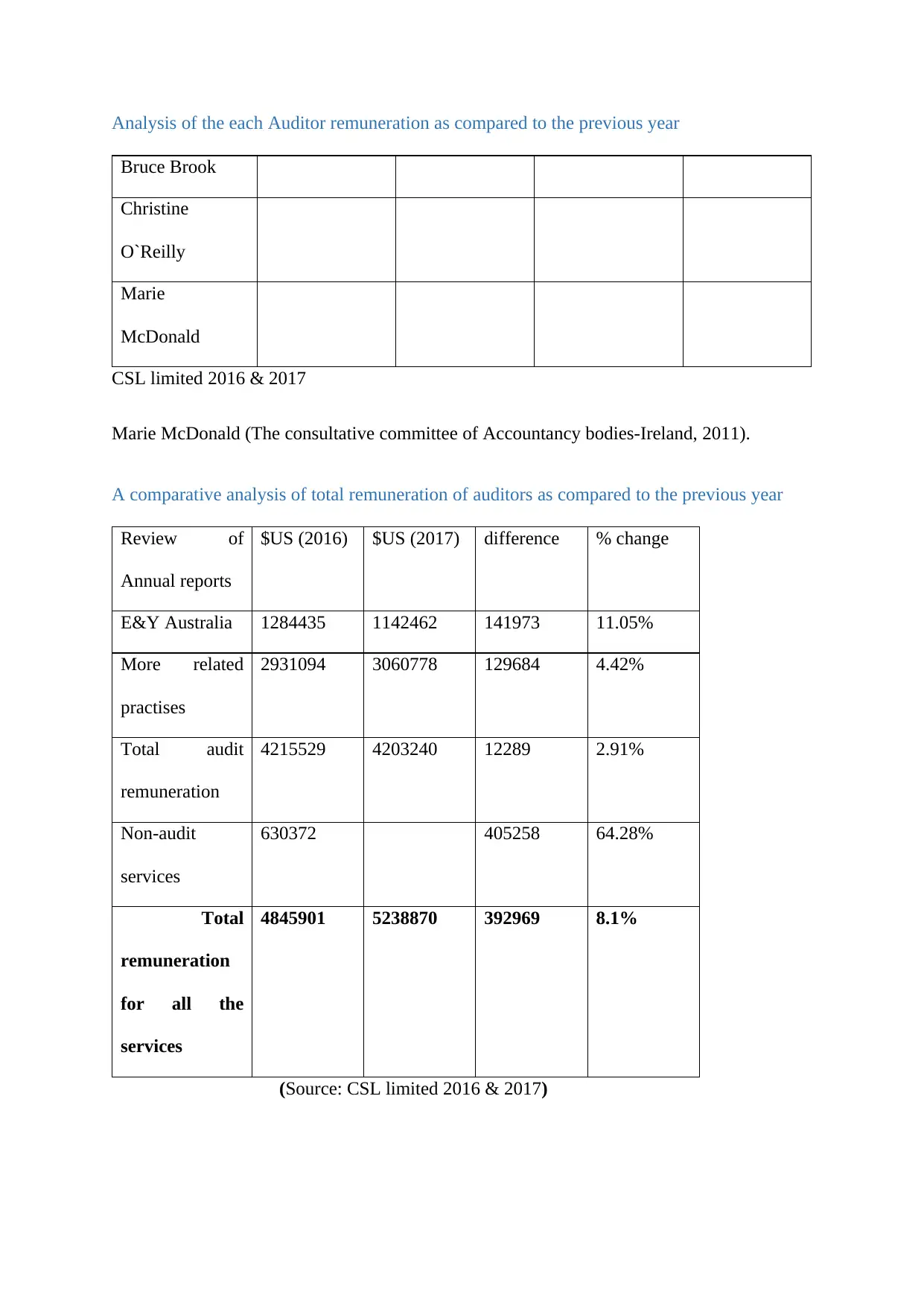

Analysis of the each Auditor remuneration as compared to the previous year

Bruce Brook

Christine

O`Reilly

Marie

McDonald

CSL limited 2016 & 2017

Marie McDonald (The consultative committee of Accountancy bodies-Ireland, 2011).

A comparative analysis of total remuneration of auditors as compared to the previous year

Review of

Annual reports

$US (2016) $US (2017) difference % change

E&Y Australia 1284435 1142462 141973 11.05%

More related

practises

2931094 3060778 129684 4.42%

Total audit

remuneration

4215529 4203240 12289 2.91%

Non-audit

services

630372 405258 64.28%

Total

remuneration

for all the

services

4845901 5238870 392969 8.1%

(Source: CSL limited 2016 & 2017)

Bruce Brook

Christine

O`Reilly

Marie

McDonald

CSL limited 2016 & 2017

Marie McDonald (The consultative committee of Accountancy bodies-Ireland, 2011).

A comparative analysis of total remuneration of auditors as compared to the previous year

Review of

Annual reports

$US (2016) $US (2017) difference % change

E&Y Australia 1284435 1142462 141973 11.05%

More related

practises

2931094 3060778 129684 4.42%

Total audit

remuneration

4215529 4203240 12289 2.91%

Non-audit

services

630372 405258 64.28%

Total

remuneration

for all the

services

4845901 5238870 392969 8.1%

(Source: CSL limited 2016 & 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

After analysing annual reports of two years 2016 and 2017, the remuneration of auditors do

not cost little to the company. Apart from production and operation cost, auditor`s cost also

influences the price of the product. In above comparison table, In Australia E&Y, the

company started paying more as compared to the previous year. The percentage increase in

paying remuneration reached 11.05 percent. However, the total audit remuneration paid to the

auditors have not shown much change 2.91 percent. The company has shown changes in the

payment of non-audit services, it increased from $US 630372 to $US 1035630. Percentage

increase in payment raised 64.28 percent. The total change in the payment of remuneration to

the auditors remain moderate 8 percent (CSL limited, 2017).

Audit Procedures Performed For Key Audit Matters

Key audit matters are not subjectively bound to Corporation Act, 2001. However, after 2016,

it has made most crucial in the audit procedure of financial reports. ASA 701 regulates that it

is important for auditors to link their independence auditor’s report to key audit matter

(Financial Reporting Council, 2015). These audit procedures is to boost greater transparency

and efficiency to execute the audit. The key audit matters relates to account for rebate and

other promotional expenses. The acknowledgment and evaluation of allowances can also

comprise of cash and accrual basis at the end of fiscal year. The motive of engaging the audit

procedure in audit matters is not to modify the financial statements of CSL limited

(Christopher, McGeachy, and McGeachy, 2017).

Various key audit matters could identify that help to evaluate the performance of auditor and

fairness of financial accounts that are shared by the organisation. The matter of measuring the

amount of goodwill is the key audit matters in evaluating the auditor’s activities (Byrnes et

al., 2018).

not cost little to the company. Apart from production and operation cost, auditor`s cost also

influences the price of the product. In above comparison table, In Australia E&Y, the

company started paying more as compared to the previous year. The percentage increase in

paying remuneration reached 11.05 percent. However, the total audit remuneration paid to the

auditors have not shown much change 2.91 percent. The company has shown changes in the

payment of non-audit services, it increased from $US 630372 to $US 1035630. Percentage

increase in payment raised 64.28 percent. The total change in the payment of remuneration to

the auditors remain moderate 8 percent (CSL limited, 2017).

Audit Procedures Performed For Key Audit Matters

Key audit matters are not subjectively bound to Corporation Act, 2001. However, after 2016,

it has made most crucial in the audit procedure of financial reports. ASA 701 regulates that it

is important for auditors to link their independence auditor’s report to key audit matter

(Financial Reporting Council, 2015). These audit procedures is to boost greater transparency

and efficiency to execute the audit. The key audit matters relates to account for rebate and

other promotional expenses. The acknowledgment and evaluation of allowances can also

comprise of cash and accrual basis at the end of fiscal year. The motive of engaging the audit

procedure in audit matters is not to modify the financial statements of CSL limited

(Christopher, McGeachy, and McGeachy, 2017).

Various key audit matters could identify that help to evaluate the performance of auditor and

fairness of financial accounts that are shared by the organisation. The matter of measuring the

amount of goodwill is the key audit matters in evaluating the auditor’s activities (Byrnes et

al., 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Structure of Audit and risk management committee

The composition of Audit and Risk Management committee has both executive as well as

non-executive members of the company. The committee has three to five directors but all of

them are non-executive directors named as Mr Bruce Brook, Ms Christine O`Reilly, and Ms

Marie McDonald. All of committee members are non-executive directors and all of them

have great financial expertise (Public company Accounting Oversight Board, 2018). The

committee has reported to the board of directors that the management of CSL`s material

business risks is effective in the year ended 30 June, 2016. The signing partners in the list of

external auditors are rotated in every five years (Bowlin, Hobson, and Piercey, 2015).

Moreover, the internal auditors of the company was PWC (Pricewaterhousecoopers) during

2016 fiscal year (CSL US Inc, 2005).

An auditor is required to deliver an independence declaration in a fiscal year. As per the

requirements of CSL of the Corporation Act, this year the board and the committee approved

Mr Carmody to perform as a signing partner for E&Y (Enrst & Young) for the year 2015-

2016. Further, due to some personal issues among the members the company; it directly

affected the transition plan for replacing the signing partner and approved Mr Rodney Piltz

for the year 2016-17 (Bailey, Collins, and Abbott, 2017).

Functions of Auditor

Important function of the Audit committee is to monitor the performance of internal CSL`s

auditor operations. The audit committee checks whether the company is reflecting a fair and

true view of financial position and check how far the balance data and performance of CSL is

relevant (Chan, 2015).

Both external and internal auditors is committed to ensure that financial reporting are

accomplished and integrated with managing risk and meeting compliance requirements.

The composition of Audit and Risk Management committee has both executive as well as

non-executive members of the company. The committee has three to five directors but all of

them are non-executive directors named as Mr Bruce Brook, Ms Christine O`Reilly, and Ms

Marie McDonald. All of committee members are non-executive directors and all of them

have great financial expertise (Public company Accounting Oversight Board, 2018). The

committee has reported to the board of directors that the management of CSL`s material

business risks is effective in the year ended 30 June, 2016. The signing partners in the list of

external auditors are rotated in every five years (Bowlin, Hobson, and Piercey, 2015).

Moreover, the internal auditors of the company was PWC (Pricewaterhousecoopers) during

2016 fiscal year (CSL US Inc, 2005).

An auditor is required to deliver an independence declaration in a fiscal year. As per the

requirements of CSL of the Corporation Act, this year the board and the committee approved

Mr Carmody to perform as a signing partner for E&Y (Enrst & Young) for the year 2015-

2016. Further, due to some personal issues among the members the company; it directly

affected the transition plan for replacing the signing partner and approved Mr Rodney Piltz

for the year 2016-17 (Bailey, Collins, and Abbott, 2017).

Functions of Auditor

Important function of the Audit committee is to monitor the performance of internal CSL`s

auditor operations. The audit committee checks whether the company is reflecting a fair and

true view of financial position and check how far the balance data and performance of CSL is

relevant (Chan, 2015).

Both external and internal auditors is committed to ensure that financial reporting are

accomplished and integrated with managing risk and meeting compliance requirements.

The main function of auditor committee is to check all the material aspects and

implementations of the policies that are adopted by the board (AICPA, 2017).

An auditor keeps a check whether the financial statements do comply with IFRS Accounting

standards as per the requirement in the Corporation Act, 2001 (Li et al., 2015).

Roles and Responsibilities of the Audit Committee

The role of internal auditor is to provide an independent and objective assurance to the

executive management in context to effectiveness of CSL`s risk management processes

(Sutherland, 2017).

CSL`s internal auditor are requested to perform investigating reviews on some suspected

fraudulent activities such as bribery, coercion or whistle blower. The risk and management

committee has the liability to keep a check on the financial statements because it is

established to maintain an adequate risk management regarding the internal compliance and

control system to enable them to prepare the reliable financial report and at the same maintain

the final accounts (Srivenkataramana, 2018).

Material subsequent events by the CSL limited

In 2014, the company has announced that it agreed to acquire Novartis global influenza

business that will combine and collaborate with bioCSL`s existing vaccine business. These

two business can become a global player if they collaborate. The fair value of net assets

overtook is anticipated to greater than the considered paid. It is anticipated that acquisition

will rise the value of assets and the liabilities (Cannon and Bedard, 2016). During 2015, CSL

conducted an internal collaboration of organisations of two bioCSL organisations. The group

has adopted certain amendments and standards as per the GAAPs (Generally Accepted

accounting principles). New standards, rules, principles, and amendments of Australian

accounting standards will be applied to coming subsequent years (Market Matters, 2018).

implementations of the policies that are adopted by the board (AICPA, 2017).

An auditor keeps a check whether the financial statements do comply with IFRS Accounting

standards as per the requirement in the Corporation Act, 2001 (Li et al., 2015).

Roles and Responsibilities of the Audit Committee

The role of internal auditor is to provide an independent and objective assurance to the

executive management in context to effectiveness of CSL`s risk management processes

(Sutherland, 2017).

CSL`s internal auditor are requested to perform investigating reviews on some suspected

fraudulent activities such as bribery, coercion or whistle blower. The risk and management

committee has the liability to keep a check on the financial statements because it is

established to maintain an adequate risk management regarding the internal compliance and

control system to enable them to prepare the reliable financial report and at the same maintain

the final accounts (Srivenkataramana, 2018).

Material subsequent events by the CSL limited

In 2014, the company has announced that it agreed to acquire Novartis global influenza

business that will combine and collaborate with bioCSL`s existing vaccine business. These

two business can become a global player if they collaborate. The fair value of net assets

overtook is anticipated to greater than the considered paid. It is anticipated that acquisition

will rise the value of assets and the liabilities (Cannon and Bedard, 2016). During 2015, CSL

conducted an internal collaboration of organisations of two bioCSL organisations. The group

has adopted certain amendments and standards as per the GAAPs (Generally Accepted

accounting principles). New standards, rules, principles, and amendments of Australian

accounting standards will be applied to coming subsequent years (Market Matters, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Directors and Management’s responsibilities differ from the Auditor’s responsibilities in

relation to the financial report

Director is responsible for making financial statements and materials in the balance sheet is

the assertion of the management. Moreover, the auditor communicate to the board whether

there exist any substantial doubt relating to entity`s ability to recognise it as going concern.

The auditor considers the undertaking of management plans while using the concept of going

concern entity basis. This accounting concept is appropriate, implication of auditor report,

and the adequacy of financial statement to disclose them in front of public (Paracini, Malsch,

and Tremblay, 2014).

The independent auditor has the liability to examine the management`s work “financial

statements” and finally expressing the opinions. The responsibility of the auditor is limited to

put a check and investigate whether the reporting of the results is accomplished with the

GAAPs (Generally accepted auditing standards). In any case, of fault on the management,

any material error and omission would be discovered if audit is performed effectively. If

there is always a sure event that the auditor`s selected evidence can fail to undercover and

uncover any material error. Then there is a need to defence the reports prepared with due care

as per the GAAPs (Generally accepted auditing standards) (Christensen et al., 2016).

Follow-up questions would you ask the Auditor at the company’s Annual General Meeting

The various follow-up questions that is to be asked by auditors at Annual General Meeting of

CSL limited (Sharma and Shekhar, 2017). What is the basis on which opinions regarding the

fair view of the financial statements in the company? Another question can be related to the

degree of assertions, which they have estimated while evaluating the books of accounts of the

company (AASB 110, 2015).

relation to the financial report

Director is responsible for making financial statements and materials in the balance sheet is

the assertion of the management. Moreover, the auditor communicate to the board whether

there exist any substantial doubt relating to entity`s ability to recognise it as going concern.

The auditor considers the undertaking of management plans while using the concept of going

concern entity basis. This accounting concept is appropriate, implication of auditor report,

and the adequacy of financial statement to disclose them in front of public (Paracini, Malsch,

and Tremblay, 2014).

The independent auditor has the liability to examine the management`s work “financial

statements” and finally expressing the opinions. The responsibility of the auditor is limited to

put a check and investigate whether the reporting of the results is accomplished with the

GAAPs (Generally accepted auditing standards). In any case, of fault on the management,

any material error and omission would be discovered if audit is performed effectively. If

there is always a sure event that the auditor`s selected evidence can fail to undercover and

uncover any material error. Then there is a need to defence the reports prepared with due care

as per the GAAPs (Generally accepted auditing standards) (Christensen et al., 2016).

Follow-up questions would you ask the Auditor at the company’s Annual General Meeting

The various follow-up questions that is to be asked by auditors at Annual General Meeting of

CSL limited (Sharma and Shekhar, 2017). What is the basis on which opinions regarding the

fair view of the financial statements in the company? Another question can be related to the

degree of assertions, which they have estimated while evaluating the books of accounts of the

company (AASB 110, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

After going through such a practical implication of changes made in the responsibilities of

auditors in 2016, it can be concluded that the CSL limited has been continuously trying to

improve its audit and non-audit services by raising the contribution of profit to pay

remuneration to the auditors. The company has both internal and external audit and risk

management committee, internal as PWC and external auditor as E&Y. The company has not

paid any indemnified cost to reimburse any cost of the auditors. By going through the

comparative analysis of remuneration of both the years, it is evaluated that the company

started paying a good sum to its auditors for non-audit services that do not hamper their

independence under Corporation Act, 2001.

After going through such a practical implication of changes made in the responsibilities of

auditors in 2016, it can be concluded that the CSL limited has been continuously trying to

improve its audit and non-audit services by raising the contribution of profit to pay

remuneration to the auditors. The company has both internal and external audit and risk

management committee, internal as PWC and external auditor as E&Y. The company has not

paid any indemnified cost to reimburse any cost of the auditors. By going through the

comparative analysis of remuneration of both the years, it is evaluated that the company

started paying a good sum to its auditors for non-audit services that do not hamper their

independence under Corporation Act, 2001.

References

AASB 110, (2015) Events after the Reporting Period. [online] Available on:

https://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf [Accessed on

29/09/18]

AICPA, (2017) Statement on Auditing Standards, Number 126: The Auditor's Consideration

of an Entity's Ability to Continue as a Going Concern (No. 126). US: John Wiley & Sons.

Bailey, C., Collins, D. L., and Abbott, L. J., (2017) the Impact of Enterprise Risk

Management on the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A

Journal of Practice & Theory, 37(3), pp. 25-46.

Bowlin, K.O., Hobson, J. L. and Piercey, M. D., (2015) the effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., (2018) Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

Cannon, N. H. and Bedard, J.C. (2016) Auditing challenging fair value measurements:

Evidence from the field. The Accounting Review, 92(4), pp. 81-114.

Chan, S. (2015) is CSL Limited a good investment. [online] Available from:

https://www.fool.com.au/2015/06/22/is-csl-limited-a-good-investment/ [Accessed

14/09/2018]

AASB 110, (2015) Events after the Reporting Period. [online] Available on:

https://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf [Accessed on

29/09/18]

AICPA, (2017) Statement on Auditing Standards, Number 126: The Auditor's Consideration

of an Entity's Ability to Continue as a Going Concern (No. 126). US: John Wiley & Sons.

Bailey, C., Collins, D. L., and Abbott, L. J., (2017) the Impact of Enterprise Risk

Management on the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A

Journal of Practice & Theory, 37(3), pp. 25-46.

Bowlin, K.O., Hobson, J. L. and Piercey, M. D., (2015) the effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., (2018) Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

Cannon, N. H. and Bedard, J.C. (2016) Auditing challenging fair value measurements:

Evidence from the field. The Accounting Review, 92(4), pp. 81-114.

Chan, S. (2015) is CSL Limited a good investment. [online] Available from:

https://www.fool.com.au/2015/06/22/is-csl-limited-a-good-investment/ [Accessed

14/09/2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.