Impact of S&P/ASX 200 on CSL Stock Price: Regression Analysis

VerifiedAdded on 2023/01/23

|4

|1120

|31

Project

AI Summary

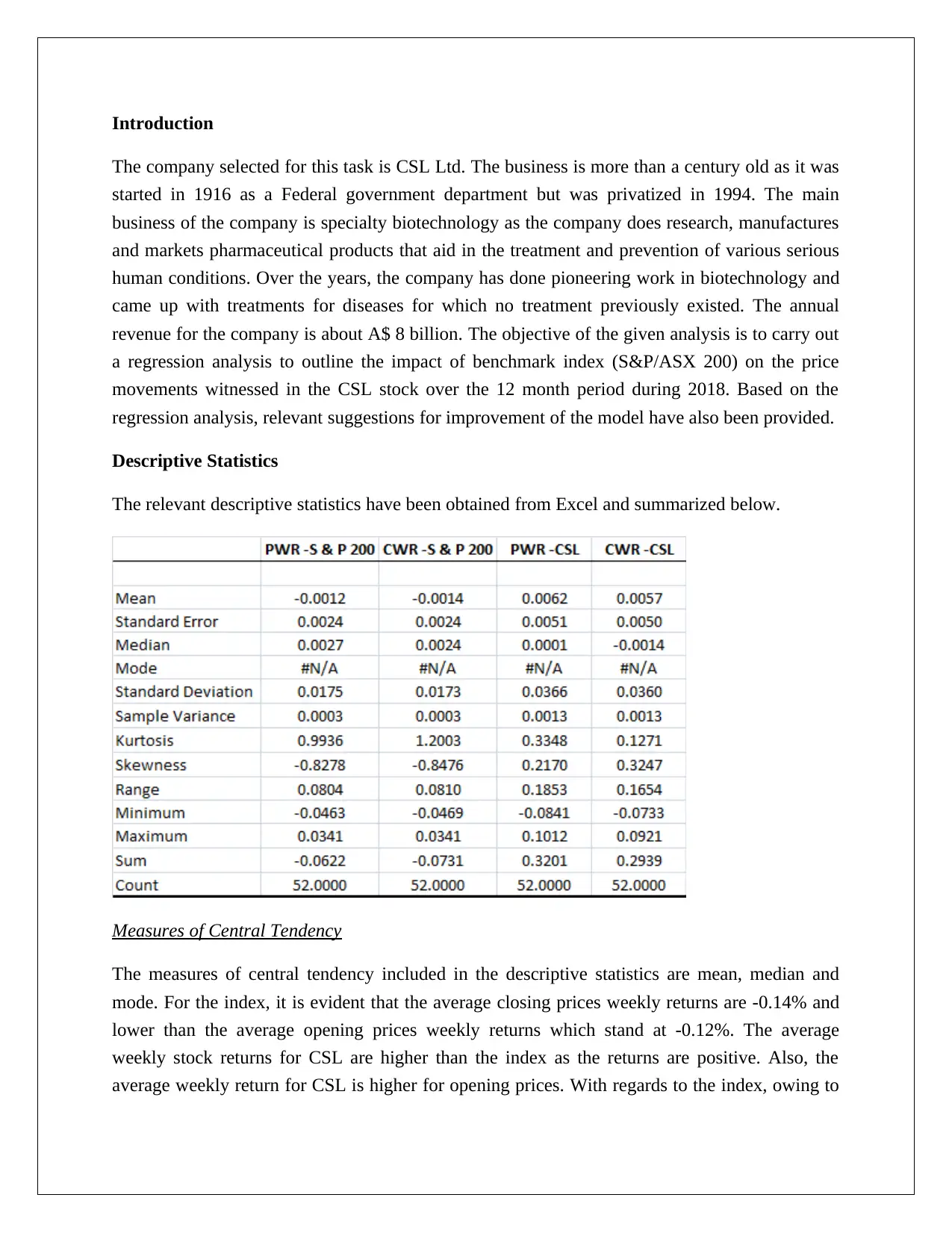

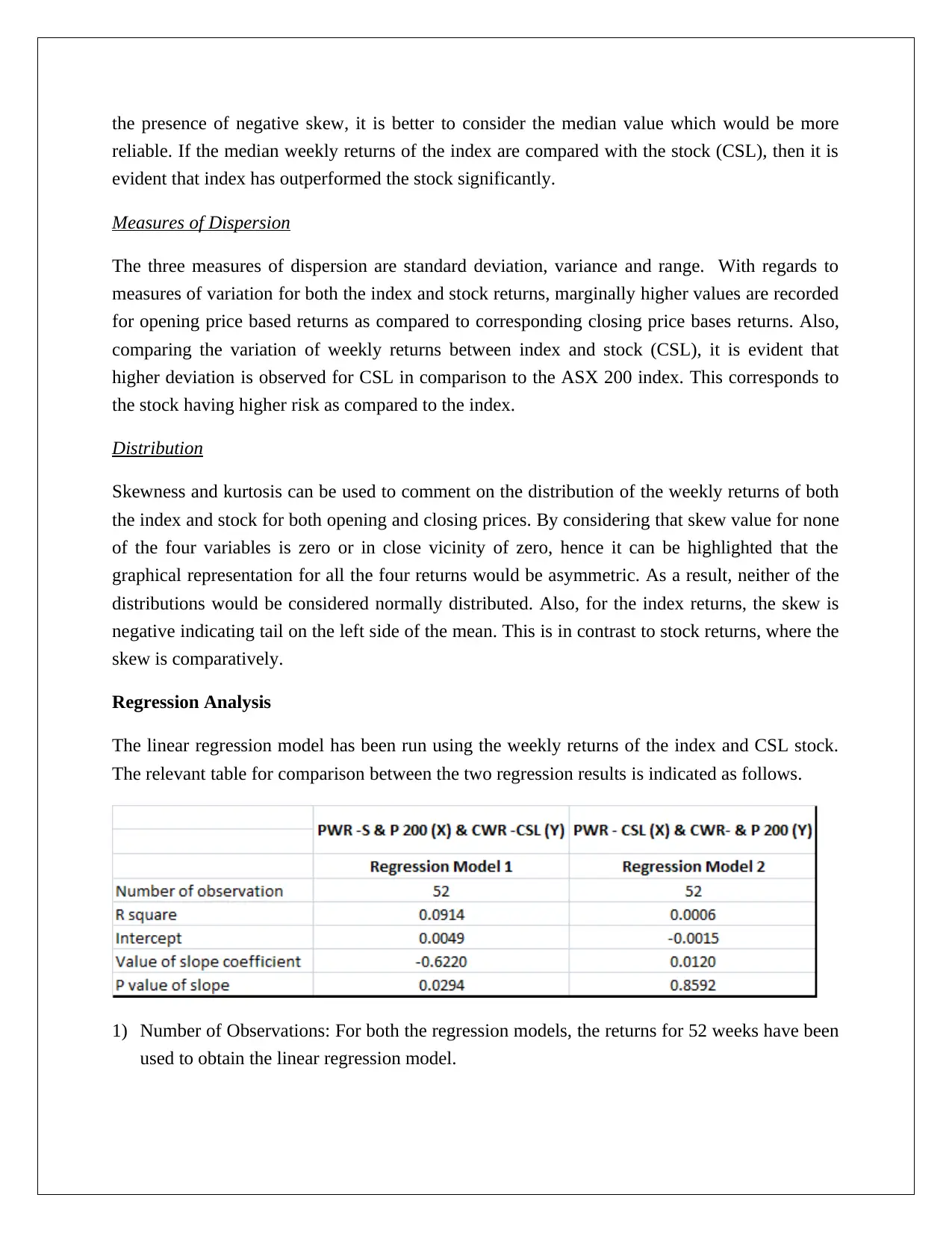

This project provides a quantitative analysis of CSL Ltd., a biotechnology company, focusing on the impact of the S&P/ASX 200 index on CSL stock price movements during 2018. The analysis employs regression models to assess the relationship between the index and the stock's weekly returns, utilizing descriptive statistics like mean, median, and measures of dispersion. The project highlights the poor fit of both regression models based on low R-squared values, though the slope is statistically significant in the first model. The findings indicate higher risk for CSL compared to the index. The conclusion suggests improvements to the models, including incorporating relevant predictor variables and, in one case, interchanging the dependent and independent variables. The project's objective is to provide insights into financial modeling and stock performance analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.