HI6026 Audit, Assurance, and Compliance: CSR Limited Report Analysis

VerifiedAdded on 2023/06/04

|15

|3469

|479

Report

AI Summary

This report provides an in-depth analysis of the audit, assurance, and compliance practices of CSR Limited. It examines the auditor's compliance with independence requirements, non-audit services provided by Deloitte, and the auditor's remuneration. The report delves into key audit matters, including product liability provisions and asset valuation, outlining the audit procedures performed. It also reviews the role and composition of the audit committee, including its members and functions. The report explores the auditor's opinion, contrasting the responsibilities of auditors and managers. The analysis is based on the annual reports of CSR Limited, providing a comprehensive overview of the company's auditing practices and adherence to relevant regulations, including the Corporations Act 2001 and Australian Auditing Standards.

Running head: AUDITING, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Student Name

University Name

Audit, Assurance and Compliance

Student Name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDITING, ASSURANCE AND COMPLIANCE

Executive Summary

Auditing helps to manage the financial aspects of the organization and also determine the risk

of investment which is one of the principal factors. When an investor in cause a huge risk that

person will demand a great amount of Return of Investment. Auditing helps to make sure that

each of the investment of the company is done in a proper and right place there is no financial

or non-financial loss. This thereby ensures where is proper financial security in an organization

investing in the same sure that their money is in the safe hands and there will be no laws for

them. The given report will highlight and analyze the audit procedures undertaken by the

auditors of the firm CSR Limited based on different aspects like auditor’s independence, non-

audit services, remuneration report, role of audit committee and reviewing all key audit

matters.

Executive Summary

Auditing helps to manage the financial aspects of the organization and also determine the risk

of investment which is one of the principal factors. When an investor in cause a huge risk that

person will demand a great amount of Return of Investment. Auditing helps to make sure that

each of the investment of the company is done in a proper and right place there is no financial

or non-financial loss. This thereby ensures where is proper financial security in an organization

investing in the same sure that their money is in the safe hands and there will be no laws for

them. The given report will highlight and analyze the audit procedures undertaken by the

auditors of the firm CSR Limited based on different aspects like auditor’s independence, non-

audit services, remuneration report, role of audit committee and reviewing all key audit

matters.

3AUDITING, ASSURANCE AND COMPLIANCE

Table of Contents

Introduction.....................................................................................................................................4

Whether the auditor complied with Independence requirements or not......................................4

Non-audit services...........................................................................................................................5

Auditor’s remuneration analysis.....................................................................................................6

Key Audit matters: Audit procedures performed............................................................................7

Audit committee and its members..................................................................................................9

Follow-up questions......................................................................................................................12

Conclusion......................................................................................................................................13

References.....................................................................................................................................14

Table of Contents

Introduction.....................................................................................................................................4

Whether the auditor complied with Independence requirements or not......................................4

Non-audit services...........................................................................................................................5

Auditor’s remuneration analysis.....................................................................................................6

Key Audit matters: Audit procedures performed............................................................................7

Audit committee and its members..................................................................................................9

Follow-up questions......................................................................................................................12

Conclusion......................................................................................................................................13

References.....................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDITING, ASSURANCE AND COMPLIANCE

Introduction

Audit is defined as the way in which the company adopt a particular system to evaluate

and establish a financial security within the internal controls of the company. The auditing

system enables the company to know perspective the financial and the internal systems of the

company and also helps the company to enable the possibility of better functioning in future.

Auditing is mainly concerned with the financial aspects of an organization, however in the

Modern Times, the system of auditing has expanded and spread its wings into the development

and parents of the other systems of the organization as well (Cannon and Bedard 2016).

Modern business organizations have witnessed several changes in audit procedures while

evaluating the preparation of their financial statements. The organizations have recognized the

value and importance of auditing to identify any kind of error in the financial statements. There

are different kinds of errors that can be found in financial statements (Hayes, Gortemaker and

Wallage 2014). These are in the form of error of commission, error of omission and error of

principle. It is the responsibility of an auditor to identify all form of errors (Knechel and Salterio

2016). Due to this reason, many organizations have taken several positive steps in order to

enhance audit quality in their financial statements. In this report, the various aspects of annual

report of the firm CSR limited will be analyzed in terms of auditing.

Whether the auditor complied with Independence requirements or not

It is of utmost importance for an auditor to comply with all the independence

requirements effectively (Asien 2015). An auditor is required to comply with all the rules and

Introduction

Audit is defined as the way in which the company adopt a particular system to evaluate

and establish a financial security within the internal controls of the company. The auditing

system enables the company to know perspective the financial and the internal systems of the

company and also helps the company to enable the possibility of better functioning in future.

Auditing is mainly concerned with the financial aspects of an organization, however in the

Modern Times, the system of auditing has expanded and spread its wings into the development

and parents of the other systems of the organization as well (Cannon and Bedard 2016).

Modern business organizations have witnessed several changes in audit procedures while

evaluating the preparation of their financial statements. The organizations have recognized the

value and importance of auditing to identify any kind of error in the financial statements. There

are different kinds of errors that can be found in financial statements (Hayes, Gortemaker and

Wallage 2014). These are in the form of error of commission, error of omission and error of

principle. It is the responsibility of an auditor to identify all form of errors (Knechel and Salterio

2016). Due to this reason, many organizations have taken several positive steps in order to

enhance audit quality in their financial statements. In this report, the various aspects of annual

report of the firm CSR limited will be analyzed in terms of auditing.

Whether the auditor complied with Independence requirements or not

It is of utmost importance for an auditor to comply with all the independence

requirements effectively (Asien 2015). An auditor is required to comply with all the rules and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDITING, ASSURANCE AND COMPLIANCE

regulations of Australian Auditing Standards effectively. Deloitte is the audit partner of the firm

CSR Limited. From the annual report, it has been observed that no auditor played a significant

role in the CSR group audit for the year ended 31 March 2017. However, the annual report for

the year ended 31 March 2018, the auditors of CSR limited have complied with the rules and

regulations made under section 342A of the Corporations Act 2001. Apart from this, the annual

report of the firm reflects the auditor’s independence declaration made under section 307C of

the Corporations Act 2001 (Csr.com.au 2018). Apart from this, it can be also inferred that the

directors of the firm are not involved in any kind of violation of Corporations Act 2001. In

addition to this, it has been also mentioned that there are no contraventions of code of audit

professional conduct.

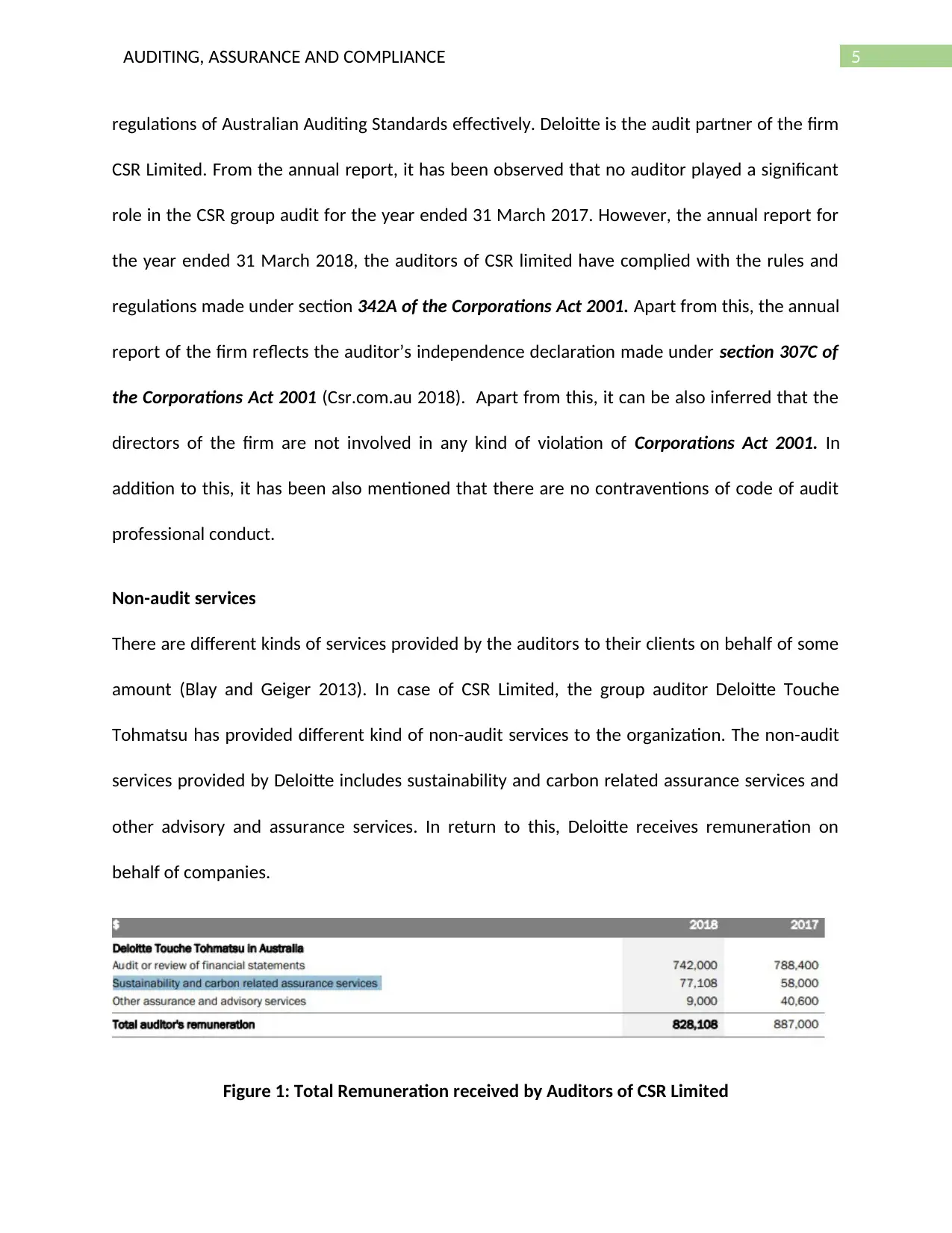

Non-audit services

There are different kinds of services provided by the auditors to their clients on behalf of some

amount (Blay and Geiger 2013). In case of CSR Limited, the group auditor Deloitte Touche

Tohmatsu has provided different kind of non-audit services to the organization. The non-audit

services provided by Deloitte includes sustainability and carbon related assurance services and

other advisory and assurance services. In return to this, Deloitte receives remuneration on

behalf of companies.

Figure 1: Total Remuneration received by Auditors of CSR Limited

regulations of Australian Auditing Standards effectively. Deloitte is the audit partner of the firm

CSR Limited. From the annual report, it has been observed that no auditor played a significant

role in the CSR group audit for the year ended 31 March 2017. However, the annual report for

the year ended 31 March 2018, the auditors of CSR limited have complied with the rules and

regulations made under section 342A of the Corporations Act 2001. Apart from this, the annual

report of the firm reflects the auditor’s independence declaration made under section 307C of

the Corporations Act 2001 (Csr.com.au 2018). Apart from this, it can be also inferred that the

directors of the firm are not involved in any kind of violation of Corporations Act 2001. In

addition to this, it has been also mentioned that there are no contraventions of code of audit

professional conduct.

Non-audit services

There are different kinds of services provided by the auditors to their clients on behalf of some

amount (Blay and Geiger 2013). In case of CSR Limited, the group auditor Deloitte Touche

Tohmatsu has provided different kind of non-audit services to the organization. The non-audit

services provided by Deloitte includes sustainability and carbon related assurance services and

other advisory and assurance services. In return to this, Deloitte receives remuneration on

behalf of companies.

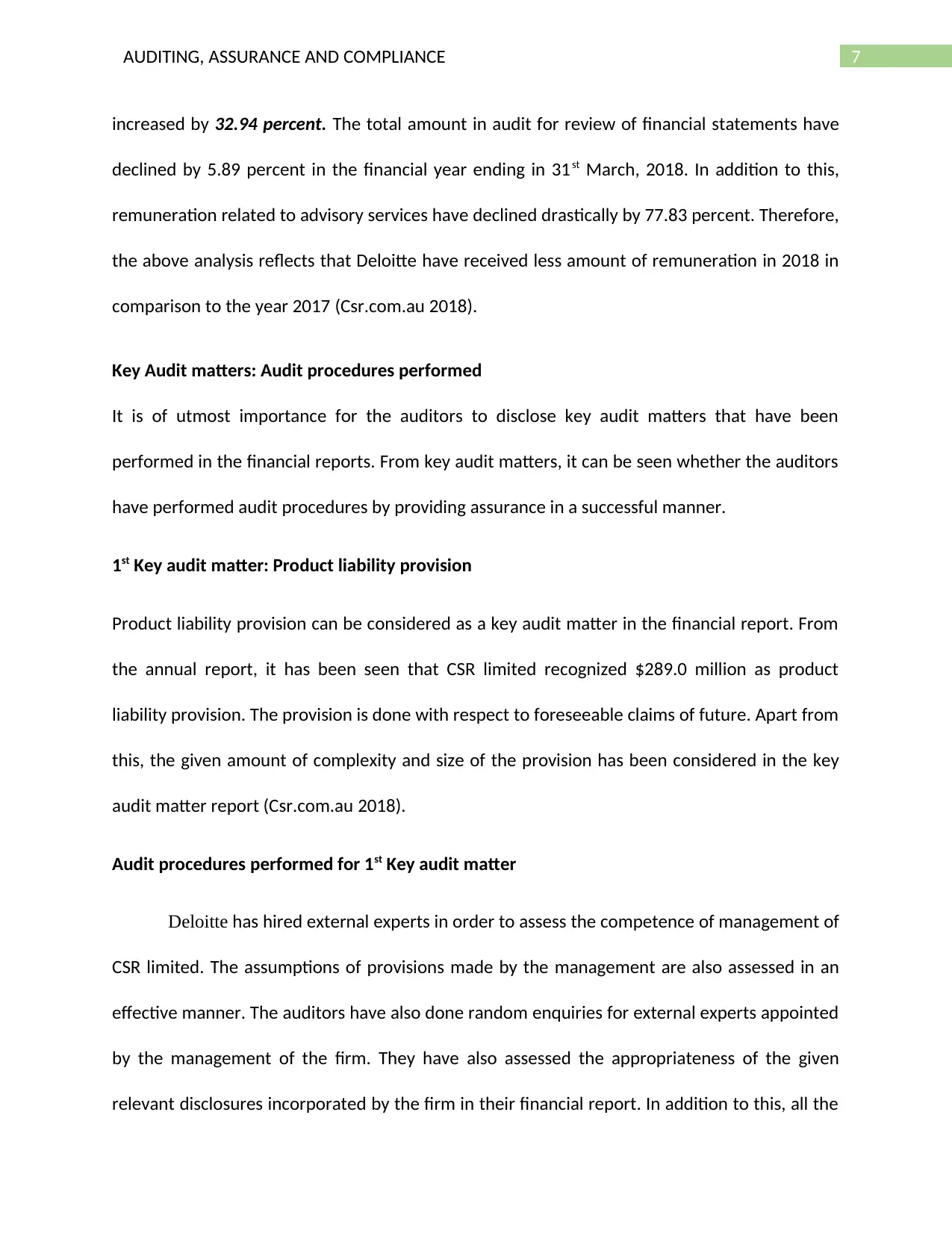

Figure 1: Total Remuneration received by Auditors of CSR Limited

6AUDITING, ASSURANCE AND COMPLIANCE

(Source: Csr.com.au 2018)

From the above figure 1, it can be inferred that Deloitte has received an amount of 58000 in the

year 2017 and 77108 in the financial year 2016. In addition to this, it can be also deduced that

the auditors of CSR Ltd have followed all the rules and regulations of Corporations Act 2001.

Apart from this, it is also stated that Deloitte has not comprise the requirements of auditor’s

independence with respect of materiality of figures in financial statements as per Corporations

Act 2001.

Auditor’s remuneration analysis

The remuneration of the auditors along with the change in percentage can be reflected with

the help of the following table:-

Figure 2: Percentage change in Remuneration of Auditors in CSR Limited

(Source: Csr.com.au 2018)

From the above figure, it can be inferred that overall remuneration of the auditor has declined

by 6.64 percent in comparison with the previous year. In addition to this, it is also reflected that

remuneration of non-audit services like assurance services of sustainability and carbon has

Particulars 2018 (in

dollars) 2017 (in dollars) Percentage Change

Deloitte Touché Tohmatsu in Australia

Audit for the review of the financial Statements 742,000 788,400 -5.89%

Assurance services for sustainability and carbon 77,108 58,000 32.94%

Services related to other assurance and advisory 9,000 40,600 -77.83%

Total Payment 828,108 887,000 -6.64%

(Source: Csr.com.au 2018)

From the above figure 1, it can be inferred that Deloitte has received an amount of 58000 in the

year 2017 and 77108 in the financial year 2016. In addition to this, it can be also deduced that

the auditors of CSR Ltd have followed all the rules and regulations of Corporations Act 2001.

Apart from this, it is also stated that Deloitte has not comprise the requirements of auditor’s

independence with respect of materiality of figures in financial statements as per Corporations

Act 2001.

Auditor’s remuneration analysis

The remuneration of the auditors along with the change in percentage can be reflected with

the help of the following table:-

Figure 2: Percentage change in Remuneration of Auditors in CSR Limited

(Source: Csr.com.au 2018)

From the above figure, it can be inferred that overall remuneration of the auditor has declined

by 6.64 percent in comparison with the previous year. In addition to this, it is also reflected that

remuneration of non-audit services like assurance services of sustainability and carbon has

Particulars 2018 (in

dollars) 2017 (in dollars) Percentage Change

Deloitte Touché Tohmatsu in Australia

Audit for the review of the financial Statements 742,000 788,400 -5.89%

Assurance services for sustainability and carbon 77,108 58,000 32.94%

Services related to other assurance and advisory 9,000 40,600 -77.83%

Total Payment 828,108 887,000 -6.64%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDITING, ASSURANCE AND COMPLIANCE

increased by 32.94 percent. The total amount in audit for review of financial statements have

declined by 5.89 percent in the financial year ending in 31st March, 2018. In addition to this,

remuneration related to advisory services have declined drastically by 77.83 percent. Therefore,

the above analysis reflects that Deloitte have received less amount of remuneration in 2018 in

comparison to the year 2017 (Csr.com.au 2018).

Key Audit matters: Audit procedures performed

It is of utmost importance for the auditors to disclose key audit matters that have been

performed in the financial reports. From key audit matters, it can be seen whether the auditors

have performed audit procedures by providing assurance in a successful manner.

1st Key audit matter: Product liability provision

Product liability provision can be considered as a key audit matter in the financial report. From

the annual report, it has been seen that CSR limited recognized $289.0 million as product

liability provision. The provision is done with respect to foreseeable claims of future. Apart from

this, the given amount of complexity and size of the provision has been considered in the key

audit matter report (Csr.com.au 2018).

Audit procedures performed for 1st Key audit matter

Deloitte has hired external experts in order to assess the competence of management of

CSR limited. The assumptions of provisions made by the management are also assessed in an

effective manner. The auditors have also done random enquiries for external experts appointed

by the management of the firm. They have also assessed the appropriateness of the given

relevant disclosures incorporated by the firm in their financial report. In addition to this, all the

increased by 32.94 percent. The total amount in audit for review of financial statements have

declined by 5.89 percent in the financial year ending in 31st March, 2018. In addition to this,

remuneration related to advisory services have declined drastically by 77.83 percent. Therefore,

the above analysis reflects that Deloitte have received less amount of remuneration in 2018 in

comparison to the year 2017 (Csr.com.au 2018).

Key Audit matters: Audit procedures performed

It is of utmost importance for the auditors to disclose key audit matters that have been

performed in the financial reports. From key audit matters, it can be seen whether the auditors

have performed audit procedures by providing assurance in a successful manner.

1st Key audit matter: Product liability provision

Product liability provision can be considered as a key audit matter in the financial report. From

the annual report, it has been seen that CSR limited recognized $289.0 million as product

liability provision. The provision is done with respect to foreseeable claims of future. Apart from

this, the given amount of complexity and size of the provision has been considered in the key

audit matter report (Csr.com.au 2018).

Audit procedures performed for 1st Key audit matter

Deloitte has hired external experts in order to assess the competence of management of

CSR limited. The assumptions of provisions made by the management are also assessed in an

effective manner. The auditors have also done random enquiries for external experts appointed

by the management of the firm. They have also assessed the appropriateness of the given

relevant disclosures incorporated by the firm in their financial report. In addition to this, all the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING, ASSURANCE AND COMPLIANCE

reports prepared by external experts are evaluated properly and effectively (Köhler, Ratzinger-

Sakel and Theis 2016).

. These are the analytical procedures performed by the auditor for the first audit matter which

is Product liability provision.

Second key audit matter: Valuation of assets

The second key audit matter is related to valuation of assets of the firm CSR Limited. The

balance sheet of the firm reflects goodwill amounting to $98.1 million, plant and equipment

amounting to $834.0 million, other intangible assets amounting to $45.8 million and property

which are included in CGU’s of the organization. The management of the firm has incorporated

an impairment trigger analysis to recognize and identify the given CGU’s that needs to be

considered for calculation of impairment. The organization has considered this a key audit

matter due to its overall importance in analyzing and forecasting the future cash flows of the

firm (Csr.com.au 2018).

Audit procedures performed for 2nd Key audit matter

There are several audit procedures that have been performed by the auditor in terms of

valuation of assets. The auditor has successfully evaluated the process undertaken by the

management of CSR limited used in determination of the given CGU’s. The auditors Deloitte

have successfully evaluated and analyzed the effectiveness of impairment model used by the

firm CSR limited while incorporating their financial statements. Apart from this, the auditors

have done proper assessment of discounting rate, terminal growth rate, forecast of cash flows

and any kind of major changes in the business cycle in the near future. Therefore, due to this

reports prepared by external experts are evaluated properly and effectively (Köhler, Ratzinger-

Sakel and Theis 2016).

. These are the analytical procedures performed by the auditor for the first audit matter which

is Product liability provision.

Second key audit matter: Valuation of assets

The second key audit matter is related to valuation of assets of the firm CSR Limited. The

balance sheet of the firm reflects goodwill amounting to $98.1 million, plant and equipment

amounting to $834.0 million, other intangible assets amounting to $45.8 million and property

which are included in CGU’s of the organization. The management of the firm has incorporated

an impairment trigger analysis to recognize and identify the given CGU’s that needs to be

considered for calculation of impairment. The organization has considered this a key audit

matter due to its overall importance in analyzing and forecasting the future cash flows of the

firm (Csr.com.au 2018).

Audit procedures performed for 2nd Key audit matter

There are several audit procedures that have been performed by the auditor in terms of

valuation of assets. The auditor has successfully evaluated the process undertaken by the

management of CSR limited used in determination of the given CGU’s. The auditors Deloitte

have successfully evaluated and analyzed the effectiveness of impairment model used by the

firm CSR limited while incorporating their financial statements. Apart from this, the auditors

have done proper assessment of discounting rate, terminal growth rate, forecast of cash flows

and any kind of major changes in the business cycle in the near future. Therefore, due to this

9AUDITING, ASSURANCE AND COMPLIANCE

reason, they have also incorporated and used analytical tools to analyze the accuracy of cash

flows as given in the financial statements. The auditors Deloitte have also assessed the accuracy

of CGU’s of the firm on historical basis. In addition to this, the different forms of disclosures

have also been assessed whether they are appropriate or not. In addition to this, the auditor

have also evaluated the forecasted amounts and process followed the management of the firm

in terms of testing controls (Gimbar Hansen and Ozlanski 2015).

Audit committee and its members

There are several members in audit committee in case of the organization CSR Limited. There

are non-executive directors as well in the audit committee of the firm (Csr.com.au 2018). The

members in audit committee are as follows:-

John Gillam

Penny Winn

Matthew Quinn

Mike Ihlein

However, it can be also inferred there is no audit committee charter that have been disclosed in

the financial reports of the firm. In addition to this, it can be also deduced that the main role

and function of the audit committee is to manage and monitor internal policies and procedures

of financial reporting of the firm. In addition to this, they can also provide a written advice to

the firm in case of any non-audit services provided by the auditors.

Type of Audit Opinion:

reason, they have also incorporated and used analytical tools to analyze the accuracy of cash

flows as given in the financial statements. The auditors Deloitte have also assessed the accuracy

of CGU’s of the firm on historical basis. In addition to this, the different forms of disclosures

have also been assessed whether they are appropriate or not. In addition to this, the auditor

have also evaluated the forecasted amounts and process followed the management of the firm

in terms of testing controls (Gimbar Hansen and Ozlanski 2015).

Audit committee and its members

There are several members in audit committee in case of the organization CSR Limited. There

are non-executive directors as well in the audit committee of the firm (Csr.com.au 2018). The

members in audit committee are as follows:-

John Gillam

Penny Winn

Matthew Quinn

Mike Ihlein

However, it can be also inferred there is no audit committee charter that have been disclosed in

the financial reports of the firm. In addition to this, it can be also deduced that the main role

and function of the audit committee is to manage and monitor internal policies and procedures

of financial reporting of the firm. In addition to this, they can also provide a written advice to

the firm in case of any non-audit services provided by the auditors.

Type of Audit Opinion:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDITING, ASSURANCE AND COMPLIANCE

The latest annual report of the CSR Limited is pretty clear in defining the opinion of the auditors

of the company, Deloitte where they claimed that the organization has prepared and published

all their financial statements in accordance to the rules and regulations of Corporations Act

2001. The auditors were accurate in justifying that the users will be able to get the correct and

impartial interpretation of the financial performances of the company CSR Limited from the

financial statements presented. The auditors of Deloitte also mentioned that the concerned

organization CSR Limited has the agreement for the financial reporting with the standards of

Corporations Act 2001 and Australian Accounting Standards in their presentation of the

financial report (Csr.com.au 2018).

Contrast in the Responsibilities of auditors and managers

The main objective or the responsibility of the directors of CSR Limited in the production

of the financial report is to formulate and present the financial statistics or the statements after

the essential agreement with the regulatory principles of Australian Accounting Standards and

Corporations Act 2001 (Christensen Glover and Wolfe 2014.) Along with that, the list of the

responsibility of the directors also includes the evaluation of the capability of the organization

in remaining operation and increasing the growth rate of the profit. The material misstatement

is one of the prime concern for the organizations conducting an audit of the assets and

liabilities of the organization and in this case the auditors need to take the responsibility of

achieving the much needed assurance of the fact that there is no presence of any material

misstatements in the financial statement of the concerned organization. Along with this the

auditors are responsible in producing the fair and exact opinion from the evaluation of the

material misstatements. Apart from this the auditors are liable for the correct evaluation of the

The latest annual report of the CSR Limited is pretty clear in defining the opinion of the auditors

of the company, Deloitte where they claimed that the organization has prepared and published

all their financial statements in accordance to the rules and regulations of Corporations Act

2001. The auditors were accurate in justifying that the users will be able to get the correct and

impartial interpretation of the financial performances of the company CSR Limited from the

financial statements presented. The auditors of Deloitte also mentioned that the concerned

organization CSR Limited has the agreement for the financial reporting with the standards of

Corporations Act 2001 and Australian Accounting Standards in their presentation of the

financial report (Csr.com.au 2018).

Contrast in the Responsibilities of auditors and managers

The main objective or the responsibility of the directors of CSR Limited in the production

of the financial report is to formulate and present the financial statistics or the statements after

the essential agreement with the regulatory principles of Australian Accounting Standards and

Corporations Act 2001 (Christensen Glover and Wolfe 2014.) Along with that, the list of the

responsibility of the directors also includes the evaluation of the capability of the organization

in remaining operation and increasing the growth rate of the profit. The material misstatement

is one of the prime concern for the organizations conducting an audit of the assets and

liabilities of the organization and in this case the auditors need to take the responsibility of

achieving the much needed assurance of the fact that there is no presence of any material

misstatements in the financial statement of the concerned organization. Along with this the

auditors are responsible in producing the fair and exact opinion from the evaluation of the

material misstatements. Apart from this the auditors are liable for the correct evaluation of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDITING, ASSURANCE AND COMPLIANCE

factors like valuation of the accounting policies, internal control mechanism along with the

analytical presentation of the going concern status and others. In addition to this, the auditor

needs to evaluate the foreseeable events of the organization and assess the historical process

of evaluation followed the firm while preparing their respective financial statements (Köhler,

Ratzinger-Sakel and Theis 2016).

Material Successive Events:

The organization CSR Limited are subjected to experience two successive events in the

year 2018 which are the payment of the dividend after the 31st of March 2018 and the sale of

the additional land at Horsley Park. In case of dividend amount, the management of CSR

Limited decided to pay 13.5 cents per share to the shareholders of the firm which will 75

percent franked. However, the total amount of final dividend has not been recognized in the

financial report as of 31st March, 2018 (Csr.com.au 2018).

For the mentioned events of Horsley Park, the organization CSR Limited are in expectation of a

profit of 30 million US dollars before the tax in the financial statement on 31st March 2019. The

assessment of the mentioned events by the auditors is instrumental in describing that these

events do not contain any sort of material impact on the financial statements of the concerned

organization.

Auditor’s Evaluation of the Material Information with respect to stakeholders

The analytical description of the auditor’s report and the financial statements make it

significantly clear that the auditors have evaluated the financial events of the CSR Limited in the

most suitable manner. The conduction of the operations for the audit is observed to follow all

factors like valuation of the accounting policies, internal control mechanism along with the

analytical presentation of the going concern status and others. In addition to this, the auditor

needs to evaluate the foreseeable events of the organization and assess the historical process

of evaluation followed the firm while preparing their respective financial statements (Köhler,

Ratzinger-Sakel and Theis 2016).

Material Successive Events:

The organization CSR Limited are subjected to experience two successive events in the

year 2018 which are the payment of the dividend after the 31st of March 2018 and the sale of

the additional land at Horsley Park. In case of dividend amount, the management of CSR

Limited decided to pay 13.5 cents per share to the shareholders of the firm which will 75

percent franked. However, the total amount of final dividend has not been recognized in the

financial report as of 31st March, 2018 (Csr.com.au 2018).

For the mentioned events of Horsley Park, the organization CSR Limited are in expectation of a

profit of 30 million US dollars before the tax in the financial statement on 31st March 2019. The

assessment of the mentioned events by the auditors is instrumental in describing that these

events do not contain any sort of material impact on the financial statements of the concerned

organization.

Auditor’s Evaluation of the Material Information with respect to stakeholders

The analytical description of the auditor’s report and the financial statements make it

significantly clear that the auditors have evaluated the financial events of the CSR Limited in the

most suitable manner. The conduction of the operations for the audit is observed to follow all

12AUDITING, ASSURANCE AND COMPLIANCE

the rules and regulations of Corporations Act 2001, APES 110 and the Australian Auditing

Standards. The effective management of the events by the auditors is visible with the

communication of the crucial audit matters and the applied audit procedures in the annual

report of 2018 (Bédard, Gonthier-Besacier and Schatt 2017).

Scope of Material Information Missing:

From the evaluation of the annual report of the mentioned organization for the year

2018 that the company, it can be inferred that Deloitte have effectively assessed the important

audit matters and their assessment also provides sufficient focus on these issues with the help

of the different forms of audit procedures. It is also evident that proper communication took

place from the part of the auditors of Deloitte to the stakeholders of the CSR Limited through

the audit report informed about the crucial audit matters. The operational assessment of the

work of the auditors makes it pretty clear that they have not missed any opportunities of the

evaluation of the material information regarding the company. However, on the contrary, it can

be also inferred that an effective charter of the audit committee was missing in the report of

the firm.

Follow-up questions

There can be many follow up questions that can be evaluated for the auditors of CSR Limited

which are as follows:-

Are there any other key audit matters that can be considered?

the rules and regulations of Corporations Act 2001, APES 110 and the Australian Auditing

Standards. The effective management of the events by the auditors is visible with the

communication of the crucial audit matters and the applied audit procedures in the annual

report of 2018 (Bédard, Gonthier-Besacier and Schatt 2017).

Scope of Material Information Missing:

From the evaluation of the annual report of the mentioned organization for the year

2018 that the company, it can be inferred that Deloitte have effectively assessed the important

audit matters and their assessment also provides sufficient focus on these issues with the help

of the different forms of audit procedures. It is also evident that proper communication took

place from the part of the auditors of Deloitte to the stakeholders of the CSR Limited through

the audit report informed about the crucial audit matters. The operational assessment of the

work of the auditors makes it pretty clear that they have not missed any opportunities of the

evaluation of the material information regarding the company. However, on the contrary, it can

be also inferred that an effective charter of the audit committee was missing in the report of

the firm.

Follow-up questions

There can be many follow up questions that can be evaluated for the auditors of CSR Limited

which are as follows:-

Are there any other key audit matters that can be considered?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.