Corporate Social Responsibility and Financial Distress Analysis

VerifiedAdded on 2022/09/08

|30

|15416

|23

Report

AI Summary

This study, published on Desklib, investigates the association between corporate social responsibility (CSR) performance and financial distress in publicly listed Australian firms from 2007 to 2013. The research employs regression analysis to demonstrate a significant negative relationship between positive CSR activities and financial distress, indicating that firms with strong CSR practices experience reduced financial distress. The study also examines the moderating effect of firm life cycle stages on this relationship, revealing that the negative association between CSR and financial distress is more pronounced in firms in mature life cycle stages. The findings, based on a sample of 651 firm-years, are robust to alternative measures of financial distress, CSR performance, and life cycle stages, contributing to the understanding of financial distress drivers and the economic consequences of CSR engagement. The study highlights CSR as a risk management strategy, emphasizing its role in preserving corporate financial performance and its implications for stakeholder relationships. This research provides valuable insights for investors and firms regarding the importance of CSR in financial risk management, particularly in the context of Australian listed firms.

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/315855719

Corporate Social Responsibility Performance, Financial Distre

Cycle: Evidence from Australia

Article in Accounting and Finance · April 2017

DOI: 10.1111/acfi.12277

CITATIONS

20

READS

1,108

5 authors, including:

Some of the authors of this publication are also working on these related projects:

Market Risk Disclosures and Board Gender-Diversity in Gulf Cooperation Council FirmsView project

Multiple Directorships, Family Ownership and the Board Nominiation Committee: International Evidence froView proje

Ahmed Al‐Hadi

Curtin University

24PUBLICATIONS138CITATIONS

SEE PROFILE

Ali Yaftian

Deakin University

16PUBLICATIONS42CITATIONS

SEE PROFILE

Mostafa Monzur Hasan

Macquarie University

41PUBLICATIONS288CITATIONS

SEE PROFILE

Corporate Social Responsibility Performance, Financial Distre

Cycle: Evidence from Australia

Article in Accounting and Finance · April 2017

DOI: 10.1111/acfi.12277

CITATIONS

20

READS

1,108

5 authors, including:

Some of the authors of this publication are also working on these related projects:

Market Risk Disclosures and Board Gender-Diversity in Gulf Cooperation Council FirmsView project

Multiple Directorships, Family Ownership and the Board Nominiation Committee: International Evidence froView proje

Ahmed Al‐Hadi

Curtin University

24PUBLICATIONS138CITATIONS

SEE PROFILE

Ali Yaftian

Deakin University

16PUBLICATIONS42CITATIONS

SEE PROFILE

Mostafa Monzur Hasan

Macquarie University

41PUBLICATIONS288CITATIONS

SEE PROFILE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate social responsibility performance, financial

distress and firm life cycle: evidence from Australia

Ahmed Al-Hadia, Bikram Chatterjeeb , Ali Yaftianc,

Grantley Taylora, Mostafa Monzur Hasand

aSchool of Accounting, Curtin Business School, Curtin University, Perth, WA, Australia

bDepartment of Accounting, Waikato Management School, The University of Waikato,

Hamilton, New Zealand

cDepartment of Accounting, Deakin Business School, Deakin University, Burwood, VIC,

Australia

dSchool of Economics and Finance, Curtin Business School, Curtin University, Perth, WA,

Australia

Abstract

This study examines the association between corporate socialresponsibility

(CSR) performance and financialdistressand additionally the moderating

impact of firm life cycle stages on that association. Based on a sample of 651

publicly listed Australian firm-years’ data covering the 2007–2013 period, our

regression results show that positive CSR activity significantly reduces financia

distress of the firm. In addition, the negative association between positive CSR

performance and financial distress is more pronounced for firms in mature life

cycle stages.Our results are robust to alternative proxy measures of financial

distress, CSR performance and life cycle stages.

Key words:Corporate social responsibility; Financial distress; Corporate life

cycle

JEL classification: G01, G32, H26

doi: 10.1111/acfi.12277

1. Introduction

Corporate socialresponsibility (CSR) and financialdistress are prominent

research topics, but often these constructs are considered in isolation (Deegan

2002).The rationale behind corporate CSR engagement is multidimensional

and can range from culturaland socialreasons to economic and financial

reasons.We thus adopt a broad perspective of CSR activities and reporting

following Moser and Martin (2012),which encapsulates allcorporate actions

© 2017 AFAANZ

Accounting and Finance

distress and firm life cycle: evidence from Australia

Ahmed Al-Hadia, Bikram Chatterjeeb , Ali Yaftianc,

Grantley Taylora, Mostafa Monzur Hasand

aSchool of Accounting, Curtin Business School, Curtin University, Perth, WA, Australia

bDepartment of Accounting, Waikato Management School, The University of Waikato,

Hamilton, New Zealand

cDepartment of Accounting, Deakin Business School, Deakin University, Burwood, VIC,

Australia

dSchool of Economics and Finance, Curtin Business School, Curtin University, Perth, WA,

Australia

Abstract

This study examines the association between corporate socialresponsibility

(CSR) performance and financialdistressand additionally the moderating

impact of firm life cycle stages on that association. Based on a sample of 651

publicly listed Australian firm-years’ data covering the 2007–2013 period, our

regression results show that positive CSR activity significantly reduces financia

distress of the firm. In addition, the negative association between positive CSR

performance and financial distress is more pronounced for firms in mature life

cycle stages.Our results are robust to alternative proxy measures of financial

distress, CSR performance and life cycle stages.

Key words:Corporate social responsibility; Financial distress; Corporate life

cycle

JEL classification: G01, G32, H26

doi: 10.1111/acfi.12277

1. Introduction

Corporate socialresponsibility (CSR) and financialdistress are prominent

research topics, but often these constructs are considered in isolation (Deegan

2002).The rationale behind corporate CSR engagement is multidimensional

and can range from culturaland socialreasons to economic and financial

reasons.We thus adopt a broad perspective of CSR activities and reporting

following Moser and Martin (2012),which encapsulates allcorporate actions

© 2017 AFAANZ

Accounting and Finance

that impact firms’ stakeholders. Specifically, we are motivated in this study to

empiricallyexaminethe association between financialdistressand CSR

performanceof publicly listed Australian firmsbecausefinancialdistress

impacts the risk-shifting behaviour of firm management.

CSR can be regarded as how a business takes accountof its socialand

environmentalimpacts of its operations(Deegan,2002) and generally

incorporates benefits by way of economic development to both the firm and

the society in which the firm operates (Holme and Watts,2006;Moser and

Martin, 2012). CSR is regarded as key factor in the success and survivalof a

firm (Hoi et al.,2013).However,there is generally no regulatory regime in

place mandatingdisclosureof CSR activities of a firm other than the

Australian Stock Exchange governance best practice recommendations, which

suggest that firms could consider reporting on these activities. Firms can then

voluntarilydiscloseCSR activities and a likely consequenceis that the

reporting of such activities will vary widely.

CSR activities could be directed primarily as a risk managementstrategy

used by a firm to enhance its reputation, which, in turn, protects the firm from

the risk of adverse political,regulatory and socialsanctions (Godfrey,2005;

Minor and Morgan, 2011). A lack of positive CSR orientation by the firm may

lead to negative sanctions such as loss of firm/executive reputation,increased

political/media pressure,and potentialfines and penalties and even possibly

consumer boycott. Further, positive engagement in CSR related activities may

generate a range of financial benefits to a firm. Indeed, the combined benefits

positive CSR engagement may out-weight the associated costs.Accordingly,

firms could to some degree manage their financialdisposition by increasing

positive CSR activities (Godfrey, 2005) so as to lessen the expected probabilit

of falling into a state of financial distress.

We also argue thatthe association between CSR and financialdistress is

moderated by the firms’life cycle stage.Given that managements’access to

resources and their strategy are likely to evolve across different life cycle stag

we conjecture that the relation between financial distress and CSR performan

to similarly change across life cycle stages.The reason for this is thatany

association between financialdistressand CSR performance isdynamic in

nature contingent upon variation in economic fundamentals (e.g.cash flows,

retained earnings, asset turnover and solvency-related risks) and opportunitie

available to the firm across its different life cycle stages. Thus, we assess that

relation between financialdistress and CSR performance evolves conditional

upon firm life cycle stages.

Based on a sample of651 firm-yearsof publicly listed Australian firms

covering the 2007–2013 period, our regression results show that positive CSR

performance is significantly and negatively associated with financialdistress.

Moreover,the negative association between positive CSR performance and

financialdistressis magnified forfirms in the maturestageof life cycle

development.Our results are robustto alternative proxy measures ofCSR

© 2017 AFAANZ

2 A. Al-Hadi et al./Accounting and Finance

empiricallyexaminethe association between financialdistressand CSR

performanceof publicly listed Australian firmsbecausefinancialdistress

impacts the risk-shifting behaviour of firm management.

CSR can be regarded as how a business takes accountof its socialand

environmentalimpacts of its operations(Deegan,2002) and generally

incorporates benefits by way of economic development to both the firm and

the society in which the firm operates (Holme and Watts,2006;Moser and

Martin, 2012). CSR is regarded as key factor in the success and survivalof a

firm (Hoi et al.,2013).However,there is generally no regulatory regime in

place mandatingdisclosureof CSR activities of a firm other than the

Australian Stock Exchange governance best practice recommendations, which

suggest that firms could consider reporting on these activities. Firms can then

voluntarilydiscloseCSR activities and a likely consequenceis that the

reporting of such activities will vary widely.

CSR activities could be directed primarily as a risk managementstrategy

used by a firm to enhance its reputation, which, in turn, protects the firm from

the risk of adverse political,regulatory and socialsanctions (Godfrey,2005;

Minor and Morgan, 2011). A lack of positive CSR orientation by the firm may

lead to negative sanctions such as loss of firm/executive reputation,increased

political/media pressure,and potentialfines and penalties and even possibly

consumer boycott. Further, positive engagement in CSR related activities may

generate a range of financial benefits to a firm. Indeed, the combined benefits

positive CSR engagement may out-weight the associated costs.Accordingly,

firms could to some degree manage their financialdisposition by increasing

positive CSR activities (Godfrey, 2005) so as to lessen the expected probabilit

of falling into a state of financial distress.

We also argue thatthe association between CSR and financialdistress is

moderated by the firms’life cycle stage.Given that managements’access to

resources and their strategy are likely to evolve across different life cycle stag

we conjecture that the relation between financial distress and CSR performan

to similarly change across life cycle stages.The reason for this is thatany

association between financialdistressand CSR performance isdynamic in

nature contingent upon variation in economic fundamentals (e.g.cash flows,

retained earnings, asset turnover and solvency-related risks) and opportunitie

available to the firm across its different life cycle stages. Thus, we assess that

relation between financialdistress and CSR performance evolves conditional

upon firm life cycle stages.

Based on a sample of651 firm-yearsof publicly listed Australian firms

covering the 2007–2013 period, our regression results show that positive CSR

performance is significantly and negatively associated with financialdistress.

Moreover,the negative association between positive CSR performance and

financialdistressis magnified forfirms in the maturestageof life cycle

development.Our results are robustto alternative proxy measures ofCSR

© 2017 AFAANZ

2 A. Al-Hadi et al./Accounting and Finance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance,financialdistress and life cycle stages.Our findings extend the

literature on the drivers of financial distress and the economic consequences o

engaging in certain types of CSR activity.

This study contributes to the literature in severalimportant ways.First, it

provides unique empirical evidence that assesses the association between CSR

performance and financialdistress.A negative association isevident.This

finding suggests that a firm engaging in positive CSR activities also takes into

account its financialdisposition,which confirms the view that CSR is a core

activity used by firmsto support their financialactivities.Our findings

support the view that CSR activities preserve corporate financial performance

(Godfrey et al.,2009).This study then links CSR performance with firm life

cycle stages and provides evidence that the interaction between both positive

CSR performance and life cycle progression isempirically associated with

financialdistress.In fact, our empiricalresultsshow that the negative

association between positive CSR activitiesand financialdistressis largely

magnified due to firm life cycle progression.To the bestof our knowledge,

this study is the firstto documentthis association empirically.Second,this

study extendsthe literatureby examiningthe association between CSR

performanceand financial distressgenerallyand by arguing that CSR

activities constitute a set of risk management mechanisms and strategies that

impact a whole range of stakeholders.This association is likely to be value

relevantto investorsin particular in assessing risk premiumsrelating to

future cash flows and the cost ofcapital,and in determining the likelihood

that a firm will be exposedto financial distress.This study provides

important evidence regarding the implications of CSR performance for firms’

financial risk management.This is particularly important given that

sustainability and CSR performanceconstitutecore businessactivitiesof

Australian listed firms.

The remainder proceeds as follows. Section 2 outlines the background to the

study and develops our hypotheses.Section 3 discusses the research design

including thesampleand statisticaltechniques.Section 4 summarisesthe

empirical results. Finally, Section 5 concludes the paper.

2. Background and hypotheses development

2.1. Financial distress

Corporate financial distress, according to Altman and Hotchkiss (2006), is a

rathervague term,which can be furtherattributed to fourgeneric terms

commonly used in business research: failure, insolvency, bankruptcy and defa

Failure arises when the realised rate of return on invested capital, with allowan

for risk consideration, is significantly and continually lower than prevailing rate

on similar investments or insufficient revenues to cover costs,and where the

average return on investment is constantly below the firm’s cost of capital.

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 3

literature on the drivers of financial distress and the economic consequences o

engaging in certain types of CSR activity.

This study contributes to the literature in severalimportant ways.First, it

provides unique empirical evidence that assesses the association between CSR

performance and financialdistress.A negative association isevident.This

finding suggests that a firm engaging in positive CSR activities also takes into

account its financialdisposition,which confirms the view that CSR is a core

activity used by firmsto support their financialactivities.Our findings

support the view that CSR activities preserve corporate financial performance

(Godfrey et al.,2009).This study then links CSR performance with firm life

cycle stages and provides evidence that the interaction between both positive

CSR performance and life cycle progression isempirically associated with

financialdistress.In fact, our empiricalresultsshow that the negative

association between positive CSR activitiesand financialdistressis largely

magnified due to firm life cycle progression.To the bestof our knowledge,

this study is the firstto documentthis association empirically.Second,this

study extendsthe literatureby examiningthe association between CSR

performanceand financial distressgenerallyand by arguing that CSR

activities constitute a set of risk management mechanisms and strategies that

impact a whole range of stakeholders.This association is likely to be value

relevantto investorsin particular in assessing risk premiumsrelating to

future cash flows and the cost ofcapital,and in determining the likelihood

that a firm will be exposedto financial distress.This study provides

important evidence regarding the implications of CSR performance for firms’

financial risk management.This is particularly important given that

sustainability and CSR performanceconstitutecore businessactivitiesof

Australian listed firms.

The remainder proceeds as follows. Section 2 outlines the background to the

study and develops our hypotheses.Section 3 discusses the research design

including thesampleand statisticaltechniques.Section 4 summarisesthe

empirical results. Finally, Section 5 concludes the paper.

2. Background and hypotheses development

2.1. Financial distress

Corporate financial distress, according to Altman and Hotchkiss (2006), is a

rathervague term,which can be furtherattributed to fourgeneric terms

commonly used in business research: failure, insolvency, bankruptcy and defa

Failure arises when the realised rate of return on invested capital, with allowan

for risk consideration, is significantly and continually lower than prevailing rate

on similar investments or insufficient revenues to cover costs,and where the

average return on investment is constantly below the firm’s cost of capital.

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Critically, financial distress increases incentives for risk-shifting to occur by

shareholders and their agents (i.e. firm management) (Maksimovic and Titma

1991;Eberhart and Senbet,1993).Indeed,in times of financialdistress,risk-

shifting behaviourincreases(Maksimovic and Titman,1991;Eberhartand

Senbet,1993;Campello et al.,2010,2011,2012).Financially distressed firms

exhibitan increase in the costof capital,a reduction in access to external

funding sources,weakercreditratingsand, in general,an increase in the

disposition of managers to take on more risk (Edwards et al., 2013). However,

credit-constrained firms focus on the need to conserve capital,to maintain

credit ratings, to meet the requirements of debt covenants and to continue as

going concern.A firm in financialdistress may also be subject to the risk of

severe negative sanctions such as loss of firm/executive reputation,increased

political/media pressure,potentialfinesand penalties,and even consumer/

creditorreprimands.In equilibrium, a firm will carry out CSR activities

provided that the marginal benefits of doing so exceeds marginal costs. A firm

strategies designed to reduce financial distress will become more appealing a

viable as the potentialcosts of financialdistressincrease.Overall, firm

managementmay be compelled to undertakerisk mitigating CSR-related

strategiesto mitigate the risksand costsassociated with financialdistress.

While there are severalmethodsto mitigate risk-shifting behaviour,more

traditionalmethods (e.g.the use of CSR) have not been evaluated tillnow,

motivating this study.

2.2. CSR performance and financial distress

Margolis and Walsh (2001)reviewed109 studiesthat examinedthe

association between CSR orientation and corporate financialperformance

and found that 54 of these studies reported a positive association between th

two. Godfrey et al. (2009) and Attig et al. (2013) find that enhanced financial

performance forstrongly CSR orientated firmsarisesthrough creation of

strongerexchangerelationshipswith key stakeholderssuch as customers,

creditors and employees, in negating the occurrence or potential impediment

of governmentintervention,and with the view to enhance future revenue

growth. Waddock and Graves (1997),purport that firms meet internal

stakeholders’expectationsthrough strategic use offinancialresourcesthat

enhances firms’reputation and competiveness.El Ghoul et al.(2011) provide

evidence thatstronger CSR engagementis associated with a lower costof

equity capitalwhile Cheng et al.(2013)find that firms with superior CSR

orientation have both better stakeholder engagement and transparency aroun

CSR performance which in turn assist in reducing capital constraints. Lee and

Faff (2009) and ElGhoul et al.(2011) assert that firms exhibiting poor CSR

practices face significantly higher idiosyncratic risk.

Minor and Morgan (2011) and Hoi et al. (2013) highlight the emerging trend

that CSR activities and reporting can be viewed as an important part of firm’s

© 2017 AFAANZ

4 A. Al-Hadi et al./Accounting and Finance

shareholders and their agents (i.e. firm management) (Maksimovic and Titma

1991;Eberhart and Senbet,1993).Indeed,in times of financialdistress,risk-

shifting behaviourincreases(Maksimovic and Titman,1991;Eberhartand

Senbet,1993;Campello et al.,2010,2011,2012).Financially distressed firms

exhibitan increase in the costof capital,a reduction in access to external

funding sources,weakercreditratingsand, in general,an increase in the

disposition of managers to take on more risk (Edwards et al., 2013). However,

credit-constrained firms focus on the need to conserve capital,to maintain

credit ratings, to meet the requirements of debt covenants and to continue as

going concern.A firm in financialdistress may also be subject to the risk of

severe negative sanctions such as loss of firm/executive reputation,increased

political/media pressure,potentialfinesand penalties,and even consumer/

creditorreprimands.In equilibrium, a firm will carry out CSR activities

provided that the marginal benefits of doing so exceeds marginal costs. A firm

strategies designed to reduce financial distress will become more appealing a

viable as the potentialcosts of financialdistressincrease.Overall, firm

managementmay be compelled to undertakerisk mitigating CSR-related

strategiesto mitigate the risksand costsassociated with financialdistress.

While there are severalmethodsto mitigate risk-shifting behaviour,more

traditionalmethods (e.g.the use of CSR) have not been evaluated tillnow,

motivating this study.

2.2. CSR performance and financial distress

Margolis and Walsh (2001)reviewed109 studiesthat examinedthe

association between CSR orientation and corporate financialperformance

and found that 54 of these studies reported a positive association between th

two. Godfrey et al. (2009) and Attig et al. (2013) find that enhanced financial

performance forstrongly CSR orientated firmsarisesthrough creation of

strongerexchangerelationshipswith key stakeholderssuch as customers,

creditors and employees, in negating the occurrence or potential impediment

of governmentintervention,and with the view to enhance future revenue

growth. Waddock and Graves (1997),purport that firms meet internal

stakeholders’expectationsthrough strategic use offinancialresourcesthat

enhances firms’reputation and competiveness.El Ghoul et al.(2011) provide

evidence thatstronger CSR engagementis associated with a lower costof

equity capitalwhile Cheng et al.(2013)find that firms with superior CSR

orientation have both better stakeholder engagement and transparency aroun

CSR performance which in turn assist in reducing capital constraints. Lee and

Faff (2009) and ElGhoul et al.(2011) assert that firms exhibiting poor CSR

practices face significantly higher idiosyncratic risk.

Minor and Morgan (2011) and Hoi et al. (2013) highlight the emerging trend

that CSR activities and reporting can be viewed as an important part of firm’s

© 2017 AFAANZ

4 A. Al-Hadi et al./Accounting and Finance

risk management.According to the risk management argument,a firm that

engages in and reports on its CSR activities would serve the interests of its

shareholders,which could potentially mitigate the risk associated with falling

into financial distress. Specifically, extensive positive CSR activities that impac

a range of stakeholdersact as a hedgeagainstfinancialimpedimentsor

constraints as the firm may be able to galvanise,and rely on its linkages and

reputation with various stakeholders to mitigate risks of financialdistress.A

firm’s action designed to ensure financial stability is legitimately influenced by

its attitude to and actions about CSR,which encapsulate broader consider-

ations regarding legality and ethics (Avi-Yonah,2008).As a result, a firm

develops CSR-related policies,strategies and activities that provide the most

favourable financial outcomes in a complex and competitive business environ-

ment.Accordingly,the risk managementperspective suggests thatincreased

positive CSR activitiesand financialdistressshould be systematically and

negativelyrelated.Godfrey et al. (2009) extendsthe risk management

perspective by asserting that when firms participate in institutionaltype CSR

activities aimed at society as a whole, this creates goodwill or moral capital fo

the firm that provides insurance-like protection when negative events occur.

They posit that such activity leads to positive attributions from stakeholders,

who then tempertheir negativejudgementsand sanctionstowardsfirms

because of this goodwill and this serves to preserve economic value for the fir

Another perspectiverelieson stakeholdertheory whereby positiveCSR

engagementrepresents a proxy for high quality management(Gross,2009).

Altman and Hotchkiss (2006) report that a pervasive reason as to why firms fa

into financial distress is due to management incompetence. If CSR activities ar

reflective of management quality in general(Attig and Cleary,2015),then it

follows that firms engaged in those activities are less likely to fall into a state o

financial distress. Gross (2009) uses both multivariate regressions and a discre

time hazard modelto report that CSR disclosures are significantly negatively

associated with the degree of financial distress in the U.S. context. Gross (200

also shows that high disclosing firms (i.e.those in the top quartile of KLD

scores) are 11 percent less likely to experience takeover or default. In the U.S.

context,Attig et al.(2013)find a positive association between strong social

performanceand firms’ credit ratings,which they attributeto improved

stakeholder relations and an increase in firms’ long-term sustainability, a signa

of efficient resource use and sound financialperformance,and a reduction in

costs associated with socially irresponsible behaviour. In particular, Attig et al.

(2013)find that stakeholdermanagementattributessuch as community

relations,diversity,employeerelations,environmentalperformanceand

product characteristics are the most important in explaining firms’creditwor-

thiness. Overall, Attig et al. (2013) posit that credit analysts view positive CSR

activities favourably in their rating decisions because the resulting improve-

ments in long-term sustainability reduce the probability of default.Addition-

ally, disclosure of CSR information may enhance stakeholders’perception of

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 5

engages in and reports on its CSR activities would serve the interests of its

shareholders,which could potentially mitigate the risk associated with falling

into financial distress. Specifically, extensive positive CSR activities that impac

a range of stakeholdersact as a hedgeagainstfinancialimpedimentsor

constraints as the firm may be able to galvanise,and rely on its linkages and

reputation with various stakeholders to mitigate risks of financialdistress.A

firm’s action designed to ensure financial stability is legitimately influenced by

its attitude to and actions about CSR,which encapsulate broader consider-

ations regarding legality and ethics (Avi-Yonah,2008).As a result, a firm

develops CSR-related policies,strategies and activities that provide the most

favourable financial outcomes in a complex and competitive business environ-

ment.Accordingly,the risk managementperspective suggests thatincreased

positive CSR activitiesand financialdistressshould be systematically and

negativelyrelated.Godfrey et al. (2009) extendsthe risk management

perspective by asserting that when firms participate in institutionaltype CSR

activities aimed at society as a whole, this creates goodwill or moral capital fo

the firm that provides insurance-like protection when negative events occur.

They posit that such activity leads to positive attributions from stakeholders,

who then tempertheir negativejudgementsand sanctionstowardsfirms

because of this goodwill and this serves to preserve economic value for the fir

Another perspectiverelieson stakeholdertheory whereby positiveCSR

engagementrepresents a proxy for high quality management(Gross,2009).

Altman and Hotchkiss (2006) report that a pervasive reason as to why firms fa

into financial distress is due to management incompetence. If CSR activities ar

reflective of management quality in general(Attig and Cleary,2015),then it

follows that firms engaged in those activities are less likely to fall into a state o

financial distress. Gross (2009) uses both multivariate regressions and a discre

time hazard modelto report that CSR disclosures are significantly negatively

associated with the degree of financial distress in the U.S. context. Gross (200

also shows that high disclosing firms (i.e.those in the top quartile of KLD

scores) are 11 percent less likely to experience takeover or default. In the U.S.

context,Attig et al.(2013)find a positive association between strong social

performanceand firms’ credit ratings,which they attributeto improved

stakeholder relations and an increase in firms’ long-term sustainability, a signa

of efficient resource use and sound financialperformance,and a reduction in

costs associated with socially irresponsible behaviour. In particular, Attig et al.

(2013)find that stakeholdermanagementattributessuch as community

relations,diversity,employeerelations,environmentalperformanceand

product characteristics are the most important in explaining firms’creditwor-

thiness. Overall, Attig et al. (2013) posit that credit analysts view positive CSR

activities favourably in their rating decisions because the resulting improve-

ments in long-term sustainability reduce the probability of default.Addition-

ally, disclosure of CSR information may enhance stakeholders’perception of

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compliance,governance and risk management,which could in turn provide

information regarding firms’ probability distributions of its future cash flows.

We conjecture that a similar line of argument could account for a possible

negativeassociation between firms’positiveCSR disclosureand financial

distress.

Taken as a whole, we thus expect firms that exhibit a higher level of positive

CSR activities as a risk management strategy to be subject to lower levels of

financial distress. We thus hypothesise that:

H1: All else being equal, positive CSR performance is negatively associated w

financial distress.

2.3. Firm life cycle, CSR disclosure and financial distress

Life cycle theory positsthat firms are subjectto systematic changesin

operating,investing and financing activities,resource endowment,organisa-

tional capabilities,risk appetiteand strategiesas they progressthrough

different stages (Helfat and Peteraf, 2003). Extant studies show that introduc-

tion and decline firms are less profitable and more risky,while growth and

mature firms are more profitable and less risky (Dickinson,2011;Habib and

Hasan,2015).It is thus not unreasonable to expect that these differences will

impact levels of financial distress across each stage of the firm life cycle.

Investors evaluate a firm’s ability to deal with financial distress and recover

profitability primarily through itsgeneration ofcash flows and earnings

potential (Black, 1998). When firms are faced with financial constraints, as the

are more likely to do so in their early stages of growth, their management tea

may search for ways to improve capabilities and resource retention (Helfat an

Peteraf, 2003). However, in the early stages, firms may lack liquid resources a

the ability to effectively compete with their peers (Spence, 1977, 1979, 1981)

particular, according to dynamic resourced-based theory, human capital, socia

capital and cognition, and resources (e.g. financing, technological and materia

are likely to be lacking in the early stages of firms’ life cycle (Helfat and Petera

2003). In the early stages of life, firms may face a high cost of capital owing to

uncertainties about future cash flows and earnings and the potential difficulty

of raising additionalcapital(Jenkins et al.,2004;Kim and Suh,2009;Hasan

et al., 2015).

During the mature phase, the firms may have greater competitive advantag

through resource use,capability managementand maintenance (Gray and

Ariss, 1985;Helfat and Peteraf,2003).In the mature stage,firms may be

sufficiently wellresourced making them less susceptible to financialdistress.

Access to greater resources including expertise in the maturity phase may me

that firm management can focus on maintaining reputation and investments

(Javanovic, 1982; Hasan and Habib, 2017). Firms in this stage of their life cycle

© 2017 AFAANZ

6 A. Al-Hadi et al./Accounting and Finance

information regarding firms’ probability distributions of its future cash flows.

We conjecture that a similar line of argument could account for a possible

negativeassociation between firms’positiveCSR disclosureand financial

distress.

Taken as a whole, we thus expect firms that exhibit a higher level of positive

CSR activities as a risk management strategy to be subject to lower levels of

financial distress. We thus hypothesise that:

H1: All else being equal, positive CSR performance is negatively associated w

financial distress.

2.3. Firm life cycle, CSR disclosure and financial distress

Life cycle theory positsthat firms are subjectto systematic changesin

operating,investing and financing activities,resource endowment,organisa-

tional capabilities,risk appetiteand strategiesas they progressthrough

different stages (Helfat and Peteraf, 2003). Extant studies show that introduc-

tion and decline firms are less profitable and more risky,while growth and

mature firms are more profitable and less risky (Dickinson,2011;Habib and

Hasan,2015).It is thus not unreasonable to expect that these differences will

impact levels of financial distress across each stage of the firm life cycle.

Investors evaluate a firm’s ability to deal with financial distress and recover

profitability primarily through itsgeneration ofcash flows and earnings

potential (Black, 1998). When firms are faced with financial constraints, as the

are more likely to do so in their early stages of growth, their management tea

may search for ways to improve capabilities and resource retention (Helfat an

Peteraf, 2003). However, in the early stages, firms may lack liquid resources a

the ability to effectively compete with their peers (Spence, 1977, 1979, 1981)

particular, according to dynamic resourced-based theory, human capital, socia

capital and cognition, and resources (e.g. financing, technological and materia

are likely to be lacking in the early stages of firms’ life cycle (Helfat and Petera

2003). In the early stages of life, firms may face a high cost of capital owing to

uncertainties about future cash flows and earnings and the potential difficulty

of raising additionalcapital(Jenkins et al.,2004;Kim and Suh,2009;Hasan

et al., 2015).

During the mature phase, the firms may have greater competitive advantag

through resource use,capability managementand maintenance (Gray and

Ariss, 1985;Helfat and Peteraf,2003).In the mature stage,firms may be

sufficiently wellresourced making them less susceptible to financialdistress.

Access to greater resources including expertise in the maturity phase may me

that firm management can focus on maintaining reputation and investments

(Javanovic, 1982; Hasan and Habib, 2017). Firms in this stage of their life cycle

© 2017 AFAANZ

6 A. Al-Hadi et al./Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have higher earningsper share, retainedearnings/totalassets,retained

earnings/totalequity and return on netoperating assets,leading to higher

and sustained dividend payouts compared to younger stage firms (DeAngelo

et al.,2006;Dickinson,2011).Firm size and age also increase in the mature

phase.Maintenance ofoperating cash flows,ongoing certainty relating to

future cash flows, earnings, innovations and investments and profit margins in

mature stage firmsmay mean thatthese firmsare lessprone to financial

distress.

Given thatpositive CSR performance reduces financialdistress,and that

financialdistress is contingent on firm life cycle,it is also possible that both

CSR performance and life cycle stages can jointly impact financial distress of a

firm. Moreover,the association between financialdistress and CSR perfor-

mance is likely to be magnified as a consequence offirm life cycle stages.

Mature firms are concerned with thereputationalconsequencesof their

activities and how they interactwith key stakeholders,including regulatory

authorities and hence these firms are likely to engage in positive CSR activitie

more extensively as compared to younger or decline stage firms (Hasan and

Habib, 2017). In fact, in the early and decline phases of firms’ life cycle, CSR

activities and disclosure,and indirect costs including reputationaleffects and

financial reporting effects, are likely to be less important than access to badly

needed capitalfor survival,growth,innovation and sustained financing.The

reason for this is that younger firms face uncertainty concerning revenue flow

and costs (Javanovic, 1982) and these firms face risk-taking around investmen

and innovations (Gort and Klepper, 1982; Miller and Friesen, 1984; Dickinson,

2011).Younger firms are concerned largely with achieving growth objectives

and ensuring that they can adequately compete and have sufficient resources

expand into new markets and to develop new product lines, and hence are les

likely to be concerned with engaging in positive CSR activities (Ramaswamy

et al.,2008).Legitimacy with key stakeholders by way of increased positive

CSR activities is likely to be less important as compared to achieving financial

objectives. The need to conserve capital or to meet the minimum capital need

of the firm is less criticalfor mature firms,so these firms can expend greater

resources in ensuring they engage in, and adequately communicate their CSR

activities (Hasan and Habib, 2017).

Certainty and reduced risk relating to current (and possibly future) earnings

and cash flows may mean that mature stage firms have reduced risk of financ

distress and a higher propensity to pursue positive CSR arrangements includin

communication of those activities.The reason is managers of these firms are

likely to have a better understanding ofthe environmentin which the firm

operates and have more resources at their disposalwhich may allow them to

identify opportunities to engage in, and communicate positive CSR activities.

Indeed, Waddock and Graves (1997) and Elsayed and Paton (2007) argue that

the existence offunds is a key determinantof whether managers decide to

engage in positive CSR activities. Moreover, if firms have excess cash, reduced

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 7

earnings/totalequity and return on netoperating assets,leading to higher

and sustained dividend payouts compared to younger stage firms (DeAngelo

et al.,2006;Dickinson,2011).Firm size and age also increase in the mature

phase.Maintenance ofoperating cash flows,ongoing certainty relating to

future cash flows, earnings, innovations and investments and profit margins in

mature stage firmsmay mean thatthese firmsare lessprone to financial

distress.

Given thatpositive CSR performance reduces financialdistress,and that

financialdistress is contingent on firm life cycle,it is also possible that both

CSR performance and life cycle stages can jointly impact financial distress of a

firm. Moreover,the association between financialdistress and CSR perfor-

mance is likely to be magnified as a consequence offirm life cycle stages.

Mature firms are concerned with thereputationalconsequencesof their

activities and how they interactwith key stakeholders,including regulatory

authorities and hence these firms are likely to engage in positive CSR activitie

more extensively as compared to younger or decline stage firms (Hasan and

Habib, 2017). In fact, in the early and decline phases of firms’ life cycle, CSR

activities and disclosure,and indirect costs including reputationaleffects and

financial reporting effects, are likely to be less important than access to badly

needed capitalfor survival,growth,innovation and sustained financing.The

reason for this is that younger firms face uncertainty concerning revenue flow

and costs (Javanovic, 1982) and these firms face risk-taking around investmen

and innovations (Gort and Klepper, 1982; Miller and Friesen, 1984; Dickinson,

2011).Younger firms are concerned largely with achieving growth objectives

and ensuring that they can adequately compete and have sufficient resources

expand into new markets and to develop new product lines, and hence are les

likely to be concerned with engaging in positive CSR activities (Ramaswamy

et al.,2008).Legitimacy with key stakeholders by way of increased positive

CSR activities is likely to be less important as compared to achieving financial

objectives. The need to conserve capital or to meet the minimum capital need

of the firm is less criticalfor mature firms,so these firms can expend greater

resources in ensuring they engage in, and adequately communicate their CSR

activities (Hasan and Habib, 2017).

Certainty and reduced risk relating to current (and possibly future) earnings

and cash flows may mean that mature stage firms have reduced risk of financ

distress and a higher propensity to pursue positive CSR arrangements includin

communication of those activities.The reason is managers of these firms are

likely to have a better understanding ofthe environmentin which the firm

operates and have more resources at their disposalwhich may allow them to

identify opportunities to engage in, and communicate positive CSR activities.

Indeed, Waddock and Graves (1997) and Elsayed and Paton (2007) argue that

the existence offunds is a key determinantof whether managers decide to

engage in positive CSR activities. Moreover, if firms have excess cash, reduced

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 7

innovations,less competition and relatively higherlevelsof agency costs,

management of mature stage firms will be incentivised to re-invigorate the fir

by engagementin positive CSR programs (Jawahar and McLaughlin,2001;

Elsayed and Paton,2007).To do so may enhance a firm’s competitive and

reputation position in the market. In addition, managers of mature stage firms

are likely to be mindful of the potential reputational costs associated with poo

CSR engagement and communication.In essence,based on the difference in

economic fundamentals between young and older firms, the dynamic between

CSR activities and financialdistress is magnified (Miller and Friesen,1984;

Black, 1998;Helfat and Peteraf, 2003).Mature firms with steady-state

investments,combined with effective legitimacy with society through more

extensive positive CSR activities,are likely to face reduced financialdistress.

The reason is mature firms capitalise on their relations with key stakeholders,

and society as a whole, to maintain reputation and ensure that this also assist

in sustaining competitive advantage and financing opportunities.Thus, the

association between positive CSR performance and financial distress is likely t

be moderated by firm life cycle stages. Therefore, we hypothesise that:

H2: All else being equal, the association between positive CSR performance a

financial distress is magnified for firms in the mature life cycle stage.

3. Research design

3.1. Sample and data

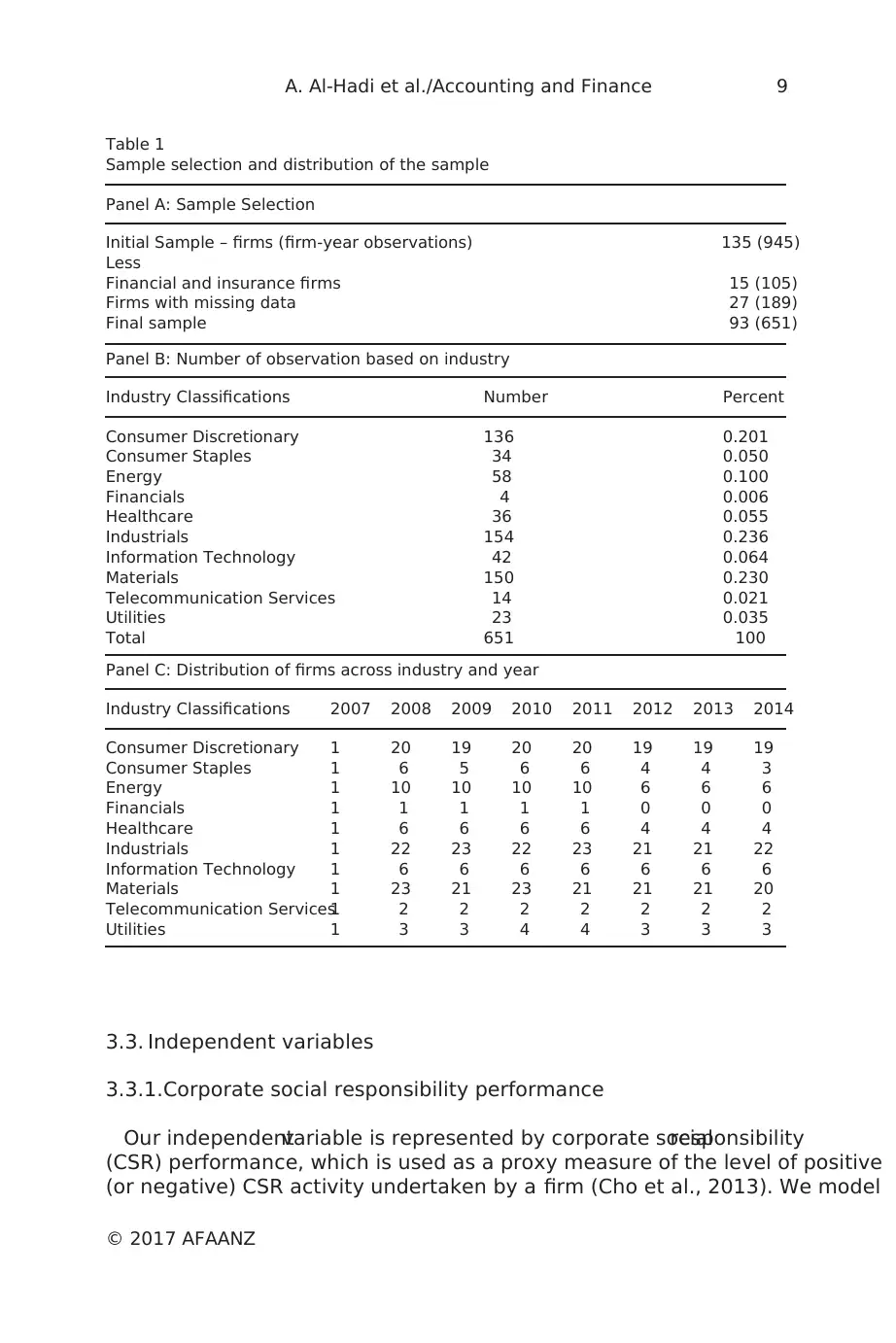

Our initial sample consists of 135 randomly selected publicly-listed Australia

firms over the period 2007–2013. The final sample consists of 93 firms (651 fi

year observations) after excluding firms with missing data (42). A summary of

sample reconciliation is presented in Table 1, panel A. The number of firm-yea

observations distributed across industry sectors is provided as Table 1, panel

and the number of firms distributed across industry sectors and years is provi

as Table 1, Panel C. Both Panel B and C show that industrials, materials and

consumer discretionary sectors dominate in our sample.

3.2. Dependent variable

Financialdistress is the dependentvariable in this study.To improve the

robustness of our results, we rely on three measures of financial distress used

the accounting and finance literature:Berger et al.(1999) model(BOS_Dis),

Altman (1968)model(AltmanZ)and Almeida and Campello (2007)model

(AC_Dis). The models are each defined in Appendix I. For all these measures,

higher values of our financial distress proxies represent lower levels of financi

distress.

© 2017 AFAANZ

8 A. Al-Hadi et al./Accounting and Finance

management of mature stage firms will be incentivised to re-invigorate the fir

by engagementin positive CSR programs (Jawahar and McLaughlin,2001;

Elsayed and Paton,2007).To do so may enhance a firm’s competitive and

reputation position in the market. In addition, managers of mature stage firms

are likely to be mindful of the potential reputational costs associated with poo

CSR engagement and communication.In essence,based on the difference in

economic fundamentals between young and older firms, the dynamic between

CSR activities and financialdistress is magnified (Miller and Friesen,1984;

Black, 1998;Helfat and Peteraf, 2003).Mature firms with steady-state

investments,combined with effective legitimacy with society through more

extensive positive CSR activities,are likely to face reduced financialdistress.

The reason is mature firms capitalise on their relations with key stakeholders,

and society as a whole, to maintain reputation and ensure that this also assist

in sustaining competitive advantage and financing opportunities.Thus, the

association between positive CSR performance and financial distress is likely t

be moderated by firm life cycle stages. Therefore, we hypothesise that:

H2: All else being equal, the association between positive CSR performance a

financial distress is magnified for firms in the mature life cycle stage.

3. Research design

3.1. Sample and data

Our initial sample consists of 135 randomly selected publicly-listed Australia

firms over the period 2007–2013. The final sample consists of 93 firms (651 fi

year observations) after excluding firms with missing data (42). A summary of

sample reconciliation is presented in Table 1, panel A. The number of firm-yea

observations distributed across industry sectors is provided as Table 1, panel

and the number of firms distributed across industry sectors and years is provi

as Table 1, Panel C. Both Panel B and C show that industrials, materials and

consumer discretionary sectors dominate in our sample.

3.2. Dependent variable

Financialdistress is the dependentvariable in this study.To improve the

robustness of our results, we rely on three measures of financial distress used

the accounting and finance literature:Berger et al.(1999) model(BOS_Dis),

Altman (1968)model(AltmanZ)and Almeida and Campello (2007)model

(AC_Dis). The models are each defined in Appendix I. For all these measures,

higher values of our financial distress proxies represent lower levels of financi

distress.

© 2017 AFAANZ

8 A. Al-Hadi et al./Accounting and Finance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.3. Independent variables

3.3.1.Corporate social responsibility performance

Our independentvariable is represented by corporate socialresponsibility

(CSR) performance, which is used as a proxy measure of the level of positive

(or negative) CSR activity undertaken by a firm (Cho et al., 2013). We model

Table 1

Sample selection and distribution of the sample

Panel A: Sample Selection

Initial Sample – firms (firm-year observations) 135 (945)

Less

Financial and insurance firms 15 (105)

Firms with missing data 27 (189)

Final sample 93 (651)

Panel B: Number of observation based on industry

Industry Classifications Number Percent

Consumer Discretionary 136 0.201

Consumer Staples 34 0.050

Energy 58 0.100

Financials 4 0.006

Healthcare 36 0.055

Industrials 154 0.236

Information Technology 42 0.064

Materials 150 0.230

Telecommunication Services 14 0.021

Utilities 23 0.035

Total 651 100

Panel C: Distribution of firms across industry and year

Industry Classifications 2007 2008 2009 2010 2011 2012 2013 2014

Consumer Discretionary 1 20 19 20 20 19 19 19

Consumer Staples 1 6 5 6 6 4 4 3

Energy 1 10 10 10 10 6 6 6

Financials 1 1 1 1 1 0 0 0

Healthcare 1 6 6 6 6 4 4 4

Industrials 1 22 23 22 23 21 21 22

Information Technology 1 6 6 6 6 6 6 6

Materials 1 23 21 23 21 21 21 20

Telecommunication Services1 2 2 2 2 2 2 2

Utilities 1 3 3 4 4 3 3 3

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 9

3.3.1.Corporate social responsibility performance

Our independentvariable is represented by corporate socialresponsibility

(CSR) performance, which is used as a proxy measure of the level of positive

(or negative) CSR activity undertaken by a firm (Cho et al., 2013). We model

Table 1

Sample selection and distribution of the sample

Panel A: Sample Selection

Initial Sample – firms (firm-year observations) 135 (945)

Less

Financial and insurance firms 15 (105)

Firms with missing data 27 (189)

Final sample 93 (651)

Panel B: Number of observation based on industry

Industry Classifications Number Percent

Consumer Discretionary 136 0.201

Consumer Staples 34 0.050

Energy 58 0.100

Financials 4 0.006

Healthcare 36 0.055

Industrials 154 0.236

Information Technology 42 0.064

Materials 150 0.230

Telecommunication Services 14 0.021

Utilities 23 0.035

Total 651 100

Panel C: Distribution of firms across industry and year

Industry Classifications 2007 2008 2009 2010 2011 2012 2013 2014

Consumer Discretionary 1 20 19 20 20 19 19 19

Consumer Staples 1 6 5 6 6 4 4 3

Energy 1 10 10 10 10 6 6 6

Financials 1 1 1 1 1 0 0 0

Healthcare 1 6 6 6 6 4 4 4

Industrials 1 22 23 22 23 21 21 22

Information Technology 1 6 6 6 6 6 6 6

Materials 1 23 21 23 21 21 21 20

Telecommunication Services1 2 2 2 2 2 2 2

Utilities 1 3 3 4 4 3 3 3

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CSR performanceas a set of heterogeneousactivitiesin line with most

literature (see, e.g. Godfrey et al., 2009). Our proxy measures of CSR activity

are based on GlobalReporting Initiative (GRI)G4 sustainability reporting

guidelines.Specifically,using the GRI index of 75 items of CSR activity,we

divide those items into positive areas of CSR activity (43) and negative CSR

activities(32) in a similar mannerto that of Cho et al. (2013).Both the

positiveand negativegrouping of itemsincludesthe differenttypesand

categoriesof CSR activities.Positive CSR activitiescomprise forinstance

activitiesaround improving environmentalefforts,strengthening customer

relationships,improving employmentand health and safety asevidence of

adherenceto regulations,best practice,monitoringand effectivenessof

resource usage.Negative CSR activitiesmay comprise such activities,for

instance,as the payment of fines,the existence of liabilities relating to poor

environmentalor socialpractices,and engagement in controversialactivities

or risky activities.Thus,any potentialmeasurement error arising from using

CSR disclosure as a proxy for a broad range of CSR activities is minimised in

our study.

Our first measure of CSR reporting is based on the number of positive CSR

items disclosed by a firm in a given year: POS_CSR = natural log of the numbe

of positive CSR items (43) reported in the annual report. Our second measure

of CSR reporting is the natural log of the number of negative CSR items (32)

reported by each firm (NEG_CSR).Activitiesthat comprisepositiveand

negative CSR performance are provided in Appendix II.Use of these items

ensuresthat our CSR index includesa broad range ofcategoriesof CSR

disclosure that could possibly be engaged in by a corporation.We examined

sample firms’annualreports to analyse the reporting of75 individualCSR

activity items that can be grouped into ‘environmental’ (30 items) and ‘social’

(45 items). The association between each of these CSR performance grouping

and financial distress is examined.

For each of the 75 individualCSR activity item,a firm represented was

scored either1 for disclosure ofa particularperformance attribute,or 0

otherwise.The scoring was performed by a research assistant and an author,

with both cross-checking a sample for consistency.

3.3.2.Life cycle variable

Following prior studies (e.g. DeAngelo et al., 2006; Owen and Yawson, 2010

Al-Hadi et al., 2016), we employ the DeAngelo et al. (2006) model of firm life

cycle which utilises retained earnings scaled by totalassets or totalequity to

measure the stages of development in that life cycle.DeAngelo et al.(2006)

claim that the mix of earned/contributed capital(i.e.retained earnings (RE)

scaled by total assets (TA) or total equity (TE)) captures essential information

regarding corporate life cycle. Firms with high retained earnings to total asset

ratio (RE/TA) or retained earnings to total equity ratio (RE/TE) are typically

© 2017 AFAANZ

10 A. Al-Hadi et al./Accounting and Finance

literature (see, e.g. Godfrey et al., 2009). Our proxy measures of CSR activity

are based on GlobalReporting Initiative (GRI)G4 sustainability reporting

guidelines.Specifically,using the GRI index of 75 items of CSR activity,we

divide those items into positive areas of CSR activity (43) and negative CSR

activities(32) in a similar mannerto that of Cho et al. (2013).Both the

positiveand negativegrouping of itemsincludesthe differenttypesand

categoriesof CSR activities.Positive CSR activitiescomprise forinstance

activitiesaround improving environmentalefforts,strengthening customer

relationships,improving employmentand health and safety asevidence of

adherenceto regulations,best practice,monitoringand effectivenessof

resource usage.Negative CSR activitiesmay comprise such activities,for

instance,as the payment of fines,the existence of liabilities relating to poor

environmentalor socialpractices,and engagement in controversialactivities

or risky activities.Thus,any potentialmeasurement error arising from using

CSR disclosure as a proxy for a broad range of CSR activities is minimised in

our study.

Our first measure of CSR reporting is based on the number of positive CSR

items disclosed by a firm in a given year: POS_CSR = natural log of the numbe

of positive CSR items (43) reported in the annual report. Our second measure

of CSR reporting is the natural log of the number of negative CSR items (32)

reported by each firm (NEG_CSR).Activitiesthat comprisepositiveand

negative CSR performance are provided in Appendix II.Use of these items

ensuresthat our CSR index includesa broad range ofcategoriesof CSR

disclosure that could possibly be engaged in by a corporation.We examined

sample firms’annualreports to analyse the reporting of75 individualCSR

activity items that can be grouped into ‘environmental’ (30 items) and ‘social’

(45 items). The association between each of these CSR performance grouping

and financial distress is examined.

For each of the 75 individualCSR activity item,a firm represented was

scored either1 for disclosure ofa particularperformance attribute,or 0

otherwise.The scoring was performed by a research assistant and an author,

with both cross-checking a sample for consistency.

3.3.2.Life cycle variable

Following prior studies (e.g. DeAngelo et al., 2006; Owen and Yawson, 2010

Al-Hadi et al., 2016), we employ the DeAngelo et al. (2006) model of firm life

cycle which utilises retained earnings scaled by totalassets or totalequity to

measure the stages of development in that life cycle.DeAngelo et al.(2006)

claim that the mix of earned/contributed capital(i.e.retained earnings (RE)

scaled by total assets (TA) or total equity (TE)) captures essential information

regarding corporate life cycle. Firms with high retained earnings to total asset

ratio (RE/TA) or retained earnings to total equity ratio (RE/TE) are typically

© 2017 AFAANZ

10 A. Al-Hadi et al./Accounting and Finance

more mature, or old with declining investment, while firms with a low RE/TA

or RE/TE tend to be young and growing.

3.4. Control variables

We include several control variables in our regression models, including firm

size, leverage,research and development(R&D) intensity,cash holding,

liquidity, profitability, industry sector and year effects.

Firm size (SIZE),measured as the naturallog of totalassets,controls for

differencesin resourcing,ability to cope with competition and funding

opportunities.Based on prior research,we expect larger firms to be able to

cope betterin periods of financialdistressbecausethey possesssuperior

economic and political power relative to smaller firms.

Leverage (LEV), measured as short-term and long-term debt divided by total

assets, controls for the level of a firm’s indebtedness. R&D intensity (RDINT),

measured as R&D expenditure divided by total assets, controls for firms’ level

of R&D expenditure.R&D-intensive firms are more likely to be subjectto

distressthan capitalintensive firms.We include firm’scash holdingsand

liquidity position to control for firms’ ability to deal with periods of financial

constraints.Additionally,we controlfor firm’s profitability using return on

assets (ROA) and loss (LOSS). Previous literatures suggest positive association

between CSR and liquidity (e.g.Subramaniam et al.,2016).Thus, we also

include liquidity ratio (QUICK).

Finally, industry sector (IND)dummy variables,defined by the two-digit

Global Industry Classification Standard (GICS) codes, are included as control

variables in our study as it is possible for financial distress to fluctuate across

different industry sectors.We also controlfor year fixed effect to controlfor

time trend.

3.4. Regression models

Our base OLS regression modelused to examine the association between

extent of CSR performance and financial distress is estimated as follows:

DISit ¼ a0it þ b1CSRit þ b2SIZE it þ b3LEV it

þ b4CASH it þ b5ROAit þ b6R&Dit þ b7QUICK it

þ b8LOSSit þ b918 IND it þ b1924 YEAR i þ eit

ð1Þ

where i= firms 1–93;t = financialyears 2007–2013;DIS = financialdistress

(proxied by AC_Dis,BOS_Dis and AltmanZ);CSR = eitherPOS_CSR or

NEG_CSR; SIZE = the naturallogarithm of totalassets;LEV = short-term

and long-term debt divided by total assets; CASH = cash holdings by the firm

defined as cash and marketable securities scaled by total assets; ROA = retur

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 11

or RE/TE tend to be young and growing.

3.4. Control variables

We include several control variables in our regression models, including firm

size, leverage,research and development(R&D) intensity,cash holding,

liquidity, profitability, industry sector and year effects.

Firm size (SIZE),measured as the naturallog of totalassets,controls for

differencesin resourcing,ability to cope with competition and funding

opportunities.Based on prior research,we expect larger firms to be able to

cope betterin periods of financialdistressbecausethey possesssuperior

economic and political power relative to smaller firms.

Leverage (LEV), measured as short-term and long-term debt divided by total

assets, controls for the level of a firm’s indebtedness. R&D intensity (RDINT),

measured as R&D expenditure divided by total assets, controls for firms’ level

of R&D expenditure.R&D-intensive firms are more likely to be subjectto

distressthan capitalintensive firms.We include firm’scash holdingsand

liquidity position to control for firms’ ability to deal with periods of financial

constraints.Additionally,we controlfor firm’s profitability using return on

assets (ROA) and loss (LOSS). Previous literatures suggest positive association

between CSR and liquidity (e.g.Subramaniam et al.,2016).Thus, we also

include liquidity ratio (QUICK).

Finally, industry sector (IND)dummy variables,defined by the two-digit

Global Industry Classification Standard (GICS) codes, are included as control

variables in our study as it is possible for financial distress to fluctuate across

different industry sectors.We also controlfor year fixed effect to controlfor

time trend.

3.4. Regression models

Our base OLS regression modelused to examine the association between

extent of CSR performance and financial distress is estimated as follows:

DISit ¼ a0it þ b1CSRit þ b2SIZE it þ b3LEV it

þ b4CASH it þ b5ROAit þ b6R&Dit þ b7QUICK it

þ b8LOSSit þ b918 IND it þ b1924 YEAR i þ eit

ð1Þ

where i= firms 1–93;t = financialyears 2007–2013;DIS = financialdistress

(proxied by AC_Dis,BOS_Dis and AltmanZ);CSR = eitherPOS_CSR or

NEG_CSR; SIZE = the naturallogarithm of totalassets;LEV = short-term

and long-term debt divided by total assets; CASH = cash holdings by the firm

defined as cash and marketable securities scaled by total assets; ROA = retur

© 2017 AFAANZ

A. Al-Hadi et al./Accounting and Finance 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.