Analysis of CYBG Plc's CSR and Sustainability Report - ACCT20074

VerifiedAdded on 2022/10/03

|17

|4663

|31

Report

AI Summary

This report examines the importance of Corporate Social Responsibility (CSR) in the modern business era, focusing on its impact on financial objectives and stakeholder relations. It begins with a literature review on CSR, comparing sustainability reporting to other reporting concepts and explaining relevant theories like stakeholder and resource-based theories. The report then analyzes CYBG Plc's sustainability reporting practices, assessing its governance, financial performance, and use of Global Reporting Initiative (GRI) guidelines. The analysis includes a scoring index based on GRI standards to evaluate the extent and quality of CYBG Plc's sustainability disclosures. The report concludes by summarizing the key findings and implications of CSR and sustainability reporting for businesses in the financial sector. The report also highlights the importance of CSR activities for the company's long-term growth and development.

1

ACCT20074 Contemporary Accounting Theory

ACCT20074 Contemporary Accounting Theory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Section 1: Executive Summary

The main aim of this report is to review the literature review on importance of corporate

social responsibility within the modern business era in order to fulfill the requirements of all the

stakeholders. On the basis of overall review of literature present in selected journal that CSR

disclosures are highly important for the reporting entities as they deliver their products and

service to society through using their own resources. Sustainability reporting requirements as

prescribed by GRI guidelines aims to provide performance of company towards various

indicators of sustainability and also discloses information on material aspects that impacts the

performance of the company. In this report CYBG Plc has been selected to review its disclosure

made on behalf of its sustainability performance.

Section 1: Executive Summary

The main aim of this report is to review the literature review on importance of corporate

social responsibility within the modern business era in order to fulfill the requirements of all the

stakeholders. On the basis of overall review of literature present in selected journal that CSR

disclosures are highly important for the reporting entities as they deliver their products and

service to society through using their own resources. Sustainability reporting requirements as

prescribed by GRI guidelines aims to provide performance of company towards various

indicators of sustainability and also discloses information on material aspects that impacts the

performance of the company. In this report CYBG Plc has been selected to review its disclosure

made on behalf of its sustainability performance.

3

Table of Contents

Section 1: Executive Summary........................................................................................................2

Section 2: Introduction....................................................................................................................4

Section 3: Part A: Theoretical Knowledge......................................................................................4

(i) Literature Review for explaining the importance of Corporate Social Responsibility (CSR)

in firms to improve the financial objectives.................................................................................4

(ii): Comparison of Sustainability reporting to other Reporting Concepts Providing Complete

View of CSR activities of businesses..........................................................................................5

(iii): Explanation of the theories relevant for explaining the significance of sustainability

reporting.......................................................................................................................................6

Section 4: Part B: Application of Theoretical Knowledge for Explaining Reporting Practices of

CYBG Plc Cdi 1:1 Foreign Exempt LSE........................................................................................7

(iv): Company Brief about its ownership, governance and financial performance.....................7

(v): Use of Global Reporting Guidelines to prepare the sustainability reporting scoring index. 8

(vi): Extent and quality of disclosure of sustainability reporting of the selected company

according to the GRI scoring index...........................................................................................13

Section 5: Conclusion....................................................................................................................14

Section 6: References....................................................................................................................15

Table of Contents

Section 1: Executive Summary........................................................................................................2

Section 2: Introduction....................................................................................................................4

Section 3: Part A: Theoretical Knowledge......................................................................................4

(i) Literature Review for explaining the importance of Corporate Social Responsibility (CSR)

in firms to improve the financial objectives.................................................................................4

(ii): Comparison of Sustainability reporting to other Reporting Concepts Providing Complete

View of CSR activities of businesses..........................................................................................5

(iii): Explanation of the theories relevant for explaining the significance of sustainability

reporting.......................................................................................................................................6

Section 4: Part B: Application of Theoretical Knowledge for Explaining Reporting Practices of

CYBG Plc Cdi 1:1 Foreign Exempt LSE........................................................................................7

(iv): Company Brief about its ownership, governance and financial performance.....................7

(v): Use of Global Reporting Guidelines to prepare the sustainability reporting scoring index. 8

(vi): Extent and quality of disclosure of sustainability reporting of the selected company

according to the GRI scoring index...........................................................................................13

Section 5: Conclusion....................................................................................................................14

Section 6: References....................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Section 2: Introduction

The report is developed to analyze and examine the importance of corporate social

responsibility measures that a business organization should adopt for maximizing the faith and

interest of its stakeholder members. The significance of sustainable reporting for providing a

complete view of CSR activities of a firm has also been discussed within the report. The

significance of sustainability reporting is discussed in the context of stakeholder and resource

based theories. In addition to this, the report ahs also examined the annual report of a selected

ASX listed entity, that is, CYBG PLC (CYB) for determining its governance outlook and the

nature of sustainability reporting as per the GRI (Global Reporting Initiative) guidelines.

Section 3: Part A: Theoretical Knowledge

(i) Literature Review for explaining the importance of Corporate Social Responsibility

(CSR) in firms to improve the financial objectives

The corporate social responsibility (CSR) can be regarded as an internal business strategy

used by businesses for incorporating the social and environmental concerns in its different

activities and behave in a responsible manner towards all its stakeholders. There is high pressure

on the business companies nowadays to develop their goods and services in a socially

responsible manner from all of its stakeholders. This is because the rising concerns about the

damage caused to our ecosystem due to negative influences of business operations is causing the

need for them to conduct their different activities in a responsible manner. The CSR activities

that are measures undertaken by businesses to increase their social, economic and environmental

performance is leading to improving the integrity in the business operations in the mind of its

different stakeholders ((Porter & Kramer, 2010). This increased satisfaction of the stakeholders

helps in improving the firm performance by enhancing its goodwill and brand image leading to

higher sales and profits. Also, the businesses are able to enhance their competitive position

which in turn promotes their long-term growth and development (Deegan, 2014).

The businesses have placed less importance on incorporation of CSR activities within

their strategic objectives initially as they believed that it would lead them to incur additional

costs and can have a negative impact on their profitability. However, with the growing concerns

regarding the social and environmental impact of businesses and the increasing pressure from

stakeholders has caused the need for them to integrate CSR strategies as an integral part of their

corporate strategies (Nikolova & Arsic, 2017). The business companies around the world has

identified the importance of integration of CSR activities for improving their competitive

position by achieving increased customer satisfaction that in turns helps in improving the

financial performance. The customers around the world are becoming largely aware of the social

and environmental issues that are resulting due to negative impact of the business operations. As

such, there is increasing trend among them to consume the products or services that have been

Section 2: Introduction

The report is developed to analyze and examine the importance of corporate social

responsibility measures that a business organization should adopt for maximizing the faith and

interest of its stakeholder members. The significance of sustainable reporting for providing a

complete view of CSR activities of a firm has also been discussed within the report. The

significance of sustainability reporting is discussed in the context of stakeholder and resource

based theories. In addition to this, the report ahs also examined the annual report of a selected

ASX listed entity, that is, CYBG PLC (CYB) for determining its governance outlook and the

nature of sustainability reporting as per the GRI (Global Reporting Initiative) guidelines.

Section 3: Part A: Theoretical Knowledge

(i) Literature Review for explaining the importance of Corporate Social Responsibility

(CSR) in firms to improve the financial objectives

The corporate social responsibility (CSR) can be regarded as an internal business strategy

used by businesses for incorporating the social and environmental concerns in its different

activities and behave in a responsible manner towards all its stakeholders. There is high pressure

on the business companies nowadays to develop their goods and services in a socially

responsible manner from all of its stakeholders. This is because the rising concerns about the

damage caused to our ecosystem due to negative influences of business operations is causing the

need for them to conduct their different activities in a responsible manner. The CSR activities

that are measures undertaken by businesses to increase their social, economic and environmental

performance is leading to improving the integrity in the business operations in the mind of its

different stakeholders ((Porter & Kramer, 2010). This increased satisfaction of the stakeholders

helps in improving the firm performance by enhancing its goodwill and brand image leading to

higher sales and profits. Also, the businesses are able to enhance their competitive position

which in turn promotes their long-term growth and development (Deegan, 2014).

The businesses have placed less importance on incorporation of CSR activities within

their strategic objectives initially as they believed that it would lead them to incur additional

costs and can have a negative impact on their profitability. However, with the growing concerns

regarding the social and environmental impact of businesses and the increasing pressure from

stakeholders has caused the need for them to integrate CSR strategies as an integral part of their

corporate strategies (Nikolova & Arsic, 2017). The business companies around the world has

identified the importance of integration of CSR activities for improving their competitive

position by achieving increased customer satisfaction that in turns helps in improving the

financial performance. The customers around the world are becoming largely aware of the social

and environmental issues that are resulting due to negative impact of the business operations. As

such, there is increasing trend among them to consume the products or services that have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

provided to them in an ethical and responsible manner. Therefore, the businesses that have

presence of an adequate CSR strategy are able to achieve a higher financial growth as their

products are largely consumed by customers in comparison to the companies that do not

integrate the use of an adequate CSR strategy (Buchholtz, 2011).

It has been depicted by various researches that CSR influences the financial performance

of businesses through creating higher value for all its stakeholders. As such, it can be described

as a value-enhancing activity as it leads to improving the product market competition. The

business firms with strong governance structures as a sort of their CSR strategies have higher

equity returns due to improved operating performance and higher market value. The relation

between the CR and the financial performance of a firm can also be adequately explained with

the use of agency theory (Deegan, 2014). The agency theory has stated that the alignment of goal

and objectives of the business managers and shareholders is largely essential for maximizing a

firm value. The conflict of interest between the managers and owners can be regarded as a major

problem that can result in negatively influencing the business performance. However, the use of

CSR strategies by the business managers helps in improving transparency within business

operations from the perspective of its owners, that are, shareholders and thus leading to

alignment of their goals with the shareholder goals. This helps in reducing the agency costs and

thus maximizing a firm performance.

The CSR activities are helping the business firms to drive innovation, resolve their

material issues, strengthening the community engagement and overcoming the business risks in

an effective manner. Also, it helps them to ensure that they are complying with all the legislative

and regulatory requirements and thus seeking continuous support from the government. The

global investors around the world also intend to invest more in business corporations that have

an improved goodwill among the society. This in turns helps the businesses using CSR strategies

to drive their business growth and expansion in an adequate manner (Michelon, Boesso &

Kumar, 2013).

(ii): Comparison of Sustainability reporting to other Reporting Concepts Providing

Complete View of CSR activities of businesses

The increasing importance of CSR realized by the companies has resulted in undertaking

the various voluntary disclosure initiatives by them to report on their social or environmental

performances. This type of information is provided within the annual reports of companies that

help the stakeholders to gain an insight about the measures that the company is undertaking to

overcome the negative impact of its different operations on the society or on the environment.

The changes in Australian Corporations Law in the year 1998 have also mandated certain

companies to report on their environmental performance (Figar, 2011). This is essential to

analyze the CSR strategies of a firm and ensuring that all its activities does not have any negative

impact on the society and the environment. The development of sustainability standards provided

by the Global Reporting Initiative (GRI) and other frameworks such as Integrated Reporting

framework is now causing the need for businesses to report on their CSR performances. This

provided to them in an ethical and responsible manner. Therefore, the businesses that have

presence of an adequate CSR strategy are able to achieve a higher financial growth as their

products are largely consumed by customers in comparison to the companies that do not

integrate the use of an adequate CSR strategy (Buchholtz, 2011).

It has been depicted by various researches that CSR influences the financial performance

of businesses through creating higher value for all its stakeholders. As such, it can be described

as a value-enhancing activity as it leads to improving the product market competition. The

business firms with strong governance structures as a sort of their CSR strategies have higher

equity returns due to improved operating performance and higher market value. The relation

between the CR and the financial performance of a firm can also be adequately explained with

the use of agency theory (Deegan, 2014). The agency theory has stated that the alignment of goal

and objectives of the business managers and shareholders is largely essential for maximizing a

firm value. The conflict of interest between the managers and owners can be regarded as a major

problem that can result in negatively influencing the business performance. However, the use of

CSR strategies by the business managers helps in improving transparency within business

operations from the perspective of its owners, that are, shareholders and thus leading to

alignment of their goals with the shareholder goals. This helps in reducing the agency costs and

thus maximizing a firm performance.

The CSR activities are helping the business firms to drive innovation, resolve their

material issues, strengthening the community engagement and overcoming the business risks in

an effective manner. Also, it helps them to ensure that they are complying with all the legislative

and regulatory requirements and thus seeking continuous support from the government. The

global investors around the world also intend to invest more in business corporations that have

an improved goodwill among the society. This in turns helps the businesses using CSR strategies

to drive their business growth and expansion in an adequate manner (Michelon, Boesso &

Kumar, 2013).

(ii): Comparison of Sustainability reporting to other Reporting Concepts Providing

Complete View of CSR activities of businesses

The increasing importance of CSR realized by the companies has resulted in undertaking

the various voluntary disclosure initiatives by them to report on their social or environmental

performances. This type of information is provided within the annual reports of companies that

help the stakeholders to gain an insight about the measures that the company is undertaking to

overcome the negative impact of its different operations on the society or on the environment.

The changes in Australian Corporations Law in the year 1998 have also mandated certain

companies to report on their environmental performance (Figar, 2011). This is essential to

analyze the CSR strategies of a firm and ensuring that all its activities does not have any negative

impact on the society and the environment. The development of sustainability standards provided

by the Global Reporting Initiative (GRI) and other frameworks such as Integrated Reporting

framework is now causing the need for businesses to report on their CSR performances. This

6

type of mandatory reporting by firms related to their non-financial information is largely being

adopted by them to provide disclosure about their information elated to society and

environmental aspects (Homayoun, Rezaee & Ahmadi, 2015).

The development of GRI standards and other relevant framework has provided well-

defined guidelines for businesses to provide information about their CSR initiatives in the form

of developing a sustainable report. It is an approach used by business firms to a large extent for

disclosing the materialistic non-financial information and communicates with its key

stakeholders about its social and environmental issues ((Mousa & Hassan, 2015). The disclosures

provided by the firms helps in improving the reliability of business operations in the mind of

stakeholders by gaining an insight about the ways in which they are managing their social and

environmental issues (Deegan, 2014). The major difference that can be stated between

sustainability reporting and other relevant reporting types adopted by business to report on their

CSR performance is that sustainable reports are developed on the basis of defined set of

standards and guidelines such as GRI. They integrate information related to all the CSR aspects

of a business corporation such as social, economic and environmental whereas other reporting

framework are not largely helpful in providing disclosures about all the CSR aspects of a

business. There is no defined set of pattern or standards on the basis of which the information is

disclosed. Thus, sustainability reporting is regarded as the most effective way adopted by

businesses to interact with its stakeholders as compared with other relevant reporting frameworks

(Kolk, 2016).

(iii): Explanation of the theories relevant for explaining the significance of sustainability

reporting

The most relevant theory in this context can be regarded as the stakeholder theory which

has stated that business companies should emphasize on developing long-term relations with all

its stakeholder members for maximizing its value creation. The stakeholders on the basis of this

theory have been identified as members who have either a direct or indirect impact form the

various activities of a business firm (Carroll & Shabana, 2010). The important stakeholders of a

firm can be regarded as customers, employees, creditors, investors, debtors, government and

other members who are impacted by its different operational activities. As such, it can be said on

the basis of this theory that a firm can achieve the satisfaction of all its stakeholder members

through reporting on their CSR activities in the form of a sustainable report (Deegan, 2014). The

sustainable report provides information to the various stakeholders of a business about their

social, economic and environmental aspects which in turn helps in achieving stakeholder faith

through ensuring that their different needs and requirements are met in an appropriate manner

(Asemah Okpanachi & Edegoh, 2013).

On the other hand, the resource based theory can also be regarded as an effective

theoretical formwork that can be used for demonstrating the significance of sustainable reporting

within businesses. The resource-based theory has stated that strategic resources of a firm should

be exploited in a sustainability manner for ensuring its long-term growth and success. The

type of mandatory reporting by firms related to their non-financial information is largely being

adopted by them to provide disclosure about their information elated to society and

environmental aspects (Homayoun, Rezaee & Ahmadi, 2015).

The development of GRI standards and other relevant framework has provided well-

defined guidelines for businesses to provide information about their CSR initiatives in the form

of developing a sustainable report. It is an approach used by business firms to a large extent for

disclosing the materialistic non-financial information and communicates with its key

stakeholders about its social and environmental issues ((Mousa & Hassan, 2015). The disclosures

provided by the firms helps in improving the reliability of business operations in the mind of

stakeholders by gaining an insight about the ways in which they are managing their social and

environmental issues (Deegan, 2014). The major difference that can be stated between

sustainability reporting and other relevant reporting types adopted by business to report on their

CSR performance is that sustainable reports are developed on the basis of defined set of

standards and guidelines such as GRI. They integrate information related to all the CSR aspects

of a business corporation such as social, economic and environmental whereas other reporting

framework are not largely helpful in providing disclosures about all the CSR aspects of a

business. There is no defined set of pattern or standards on the basis of which the information is

disclosed. Thus, sustainability reporting is regarded as the most effective way adopted by

businesses to interact with its stakeholders as compared with other relevant reporting frameworks

(Kolk, 2016).

(iii): Explanation of the theories relevant for explaining the significance of sustainability

reporting

The most relevant theory in this context can be regarded as the stakeholder theory which

has stated that business companies should emphasize on developing long-term relations with all

its stakeholder members for maximizing its value creation. The stakeholders on the basis of this

theory have been identified as members who have either a direct or indirect impact form the

various activities of a business firm (Carroll & Shabana, 2010). The important stakeholders of a

firm can be regarded as customers, employees, creditors, investors, debtors, government and

other members who are impacted by its different operational activities. As such, it can be said on

the basis of this theory that a firm can achieve the satisfaction of all its stakeholder members

through reporting on their CSR activities in the form of a sustainable report (Deegan, 2014). The

sustainable report provides information to the various stakeholders of a business about their

social, economic and environmental aspects which in turn helps in achieving stakeholder faith

through ensuring that their different needs and requirements are met in an appropriate manner

(Asemah Okpanachi & Edegoh, 2013).

On the other hand, the resource based theory can also be regarded as an effective

theoretical formwork that can be used for demonstrating the significance of sustainable reporting

within businesses. The resource-based theory has stated that strategic resources of a firm should

be exploited in a sustainability manner for ensuring its long-term growth and success. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

strategic resources play an essential role in developing the capabilities of a firm and thus

achieving superior performance over time (Matten & Moon, 2010). As such, the sustainable

reporting enables the firms to gain an analysis of the strategic use of its different resources and

identifying the issues of concerns that need to be addressed for prompting its sustainable growth.

The CSR strategies enable a firm to develop new internal resources such as adequate workplace

culture and also realizing large benefits by achieving higher corporate reputation (Nurn & Tan,

2010).

Section 4: Part B: Application of Theoretical Knowledge for Explaining Reporting

Practices of CYBG Plc Cdi 1:1 Foreign Exempt LSE

(iv): Company Brief about its ownership, governance and financial performance

CYBG PLC (CYB) is regarded as company operating within the financial sector and is

listed on the Australian Securities Exchange (ASX). It is regarded to be a holding company of

Clydesdate Bank that has been established by the National Australia Bank in the year 2016. The

bank has largely been involved in promoting growth and innovation within the financial sector of

Australia. The bank operates through retail and commercial bank channels of Clydesdale bank. It

adopts the use of a multichannel approach to reach to its customers and is highly focused on

providing them improved value services. It has maintained a strong and growing digital offering

in addition with its branch network and extensive broker channel that has enabled in achieving

higher business growth. The bank is also promoting its extensive investment in improving its

digital platform and accelerating the adoption of mobile and online tools to increase the

automation of the banks. The holding company is owned by Clydesdate Bank and thus conducts

its business operations on the part of the banking corporation (Annual Report, 2018, p. 256).

The Board is focused on achieving the highest standards of corporate governance and is

highly dedicated towards delivering long-term value to the shareholders through emphasizing on

creating sustainable value. The Board has developed strong governance and nomination

committee, audit and risk committee and remuneration committee to ensure that it is conducting

its diverse operations in an ethical and responsible manner. The Board has highly focused on

creating long-term sustainable value to the shareholders and has developed a strong leadership

team for attainment of its determined strategic objectives. It also places higher importance on

developing a team-based culture that is based on determined set of ethical values and behaviors.

The Board largely emphasizes on developing a workplace culture that is determined by strong

governance and is committed to developing leaders that enable the business to continually evolve

and change in line with the market strategy. Also, there have strong principles developed in

relation to promotion of stakeholder engagement within the company that include its customers,

shareholders, colleagues and government bodies (Annual report, 2018, p. 50-68).

It has been analyzed from the annual report of the bank that the financial year of 2018 is

regarded as another strong year determining its financial progress in terms of its strategic pillars

strategic resources play an essential role in developing the capabilities of a firm and thus

achieving superior performance over time (Matten & Moon, 2010). As such, the sustainable

reporting enables the firms to gain an analysis of the strategic use of its different resources and

identifying the issues of concerns that need to be addressed for prompting its sustainable growth.

The CSR strategies enable a firm to develop new internal resources such as adequate workplace

culture and also realizing large benefits by achieving higher corporate reputation (Nurn & Tan,

2010).

Section 4: Part B: Application of Theoretical Knowledge for Explaining Reporting

Practices of CYBG Plc Cdi 1:1 Foreign Exempt LSE

(iv): Company Brief about its ownership, governance and financial performance

CYBG PLC (CYB) is regarded as company operating within the financial sector and is

listed on the Australian Securities Exchange (ASX). It is regarded to be a holding company of

Clydesdate Bank that has been established by the National Australia Bank in the year 2016. The

bank has largely been involved in promoting growth and innovation within the financial sector of

Australia. The bank operates through retail and commercial bank channels of Clydesdale bank. It

adopts the use of a multichannel approach to reach to its customers and is highly focused on

providing them improved value services. It has maintained a strong and growing digital offering

in addition with its branch network and extensive broker channel that has enabled in achieving

higher business growth. The bank is also promoting its extensive investment in improving its

digital platform and accelerating the adoption of mobile and online tools to increase the

automation of the banks. The holding company is owned by Clydesdate Bank and thus conducts

its business operations on the part of the banking corporation (Annual Report, 2018, p. 256).

The Board is focused on achieving the highest standards of corporate governance and is

highly dedicated towards delivering long-term value to the shareholders through emphasizing on

creating sustainable value. The Board has developed strong governance and nomination

committee, audit and risk committee and remuneration committee to ensure that it is conducting

its diverse operations in an ethical and responsible manner. The Board has highly focused on

creating long-term sustainable value to the shareholders and has developed a strong leadership

team for attainment of its determined strategic objectives. It also places higher importance on

developing a team-based culture that is based on determined set of ethical values and behaviors.

The Board largely emphasizes on developing a workplace culture that is determined by strong

governance and is committed to developing leaders that enable the business to continually evolve

and change in line with the market strategy. Also, there have strong principles developed in

relation to promotion of stakeholder engagement within the company that include its customers,

shareholders, colleagues and government bodies (Annual report, 2018, p. 50-68).

It has been analyzed from the annual report of the bank that the financial year of 2018 is

regarded as another strong year determining its financial progress in terms of its strategic pillars

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

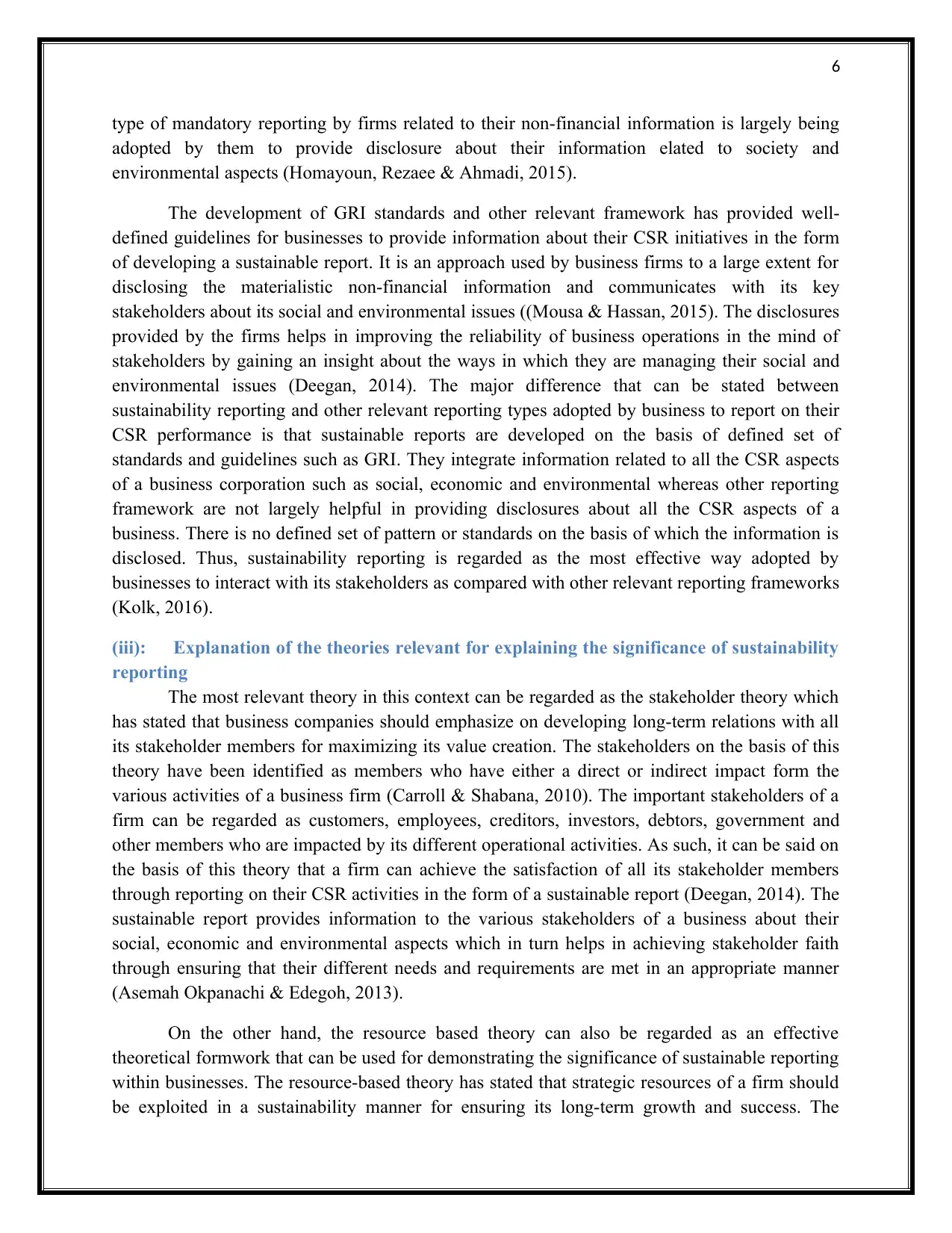

such as sustainable organic growth, efficiency and the optimization of capital. The financial

results of the company has depicted increase in its financial performance by depicting improved

underlying profits and returns, sustainable loan growth and paying an ordinary dividend of 3.1p

per share (Annual Report 2018, p 34-37). The extracts from the annual report of the bank

depicting its improved financial performance as follows:

(CYBG Plc Annual Report 2018, p. 3)

(v): Use of Global Reporting Guidelines to prepare the sustainability reporting scoring

index

The purpose of GRI sustainability reporting guidelines help companies with reporting

principles, standards of sustainability reporting and handy manual used to prepare the

sustainability reports, These guidelines does not differ the reporting initiative on the ground of

company size, sector and location (GRI, 2016, p. 5). GRI reporting guidelines have provided

various criteria that are used to score the sustainability reports prepared by the company. All

these criteria have been described below:

Two options to prepare sustainability reports: GRI Guidelines provides two different options

to prepare the sustainability reports “In accordance” with defined GRI guidelines. These two

core options are Core Option and Comprehensive Option. Any one option can be applied by

organization without considering their size, sector or location. The main focus of both the

options is to identify and make disclosure of all the material aspects. With respect to

sustainability disclosures, material aspects include the information on entities important

environmental, social, and economic impacts. In addition to this, it provides information on

matters that substantively influence the assessments and economic decisions of stakeholders

(GRI, 2016, p. 11).

such as sustainable organic growth, efficiency and the optimization of capital. The financial

results of the company has depicted increase in its financial performance by depicting improved

underlying profits and returns, sustainable loan growth and paying an ordinary dividend of 3.1p

per share (Annual Report 2018, p 34-37). The extracts from the annual report of the bank

depicting its improved financial performance as follows:

(CYBG Plc Annual Report 2018, p. 3)

(v): Use of Global Reporting Guidelines to prepare the sustainability reporting scoring

index

The purpose of GRI sustainability reporting guidelines help companies with reporting

principles, standards of sustainability reporting and handy manual used to prepare the

sustainability reports, These guidelines does not differ the reporting initiative on the ground of

company size, sector and location (GRI, 2016, p. 5). GRI reporting guidelines have provided

various criteria that are used to score the sustainability reports prepared by the company. All

these criteria have been described below:

Two options to prepare sustainability reports: GRI Guidelines provides two different options

to prepare the sustainability reports “In accordance” with defined GRI guidelines. These two

core options are Core Option and Comprehensive Option. Any one option can be applied by

organization without considering their size, sector or location. The main focus of both the

options is to identify and make disclosure of all the material aspects. With respect to

sustainability disclosures, material aspects include the information on entities important

environmental, social, and economic impacts. In addition to this, it provides information on

matters that substantively influence the assessments and economic decisions of stakeholders

(GRI, 2016, p. 11).

9

Core option contains all the essential elements that need to be disclosed in sustainability

report and provides all the material information organizational impacts due to social,

environmental, economical and governance performance of the company. On the other hand,

comprehensive option discloses information in addition to core option through adding the

requirement of additional standard disclosures on organizational strategy, ethics and integrity and

governance components. In comprehensive option organizations are required to communicate the

performance more extensively through reporting all the indicators mentioned and identified for

all the material aspects (GRI, 2016, p. 11).

Following are criteria provided under GRI guidelines for general standard disclosures and

subdivision according to above defined two CORE options:

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 12)

According to above table, companies are required to provide above mentioned general

disclosure standards for both core and comprehensive options. It has been seen that core option

limits the standard disclosures while in comprehensive option it is required to provide all

standards. It is certain that companies that make use of comprehensive option to disclose

sustainability information aims to score higher in comparison to reports that make of core option.

Core option contains all the essential elements that need to be disclosed in sustainability

report and provides all the material information organizational impacts due to social,

environmental, economical and governance performance of the company. On the other hand,

comprehensive option discloses information in addition to core option through adding the

requirement of additional standard disclosures on organizational strategy, ethics and integrity and

governance components. In comprehensive option organizations are required to communicate the

performance more extensively through reporting all the indicators mentioned and identified for

all the material aspects (GRI, 2016, p. 11).

Following are criteria provided under GRI guidelines for general standard disclosures and

subdivision according to above defined two CORE options:

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 12)

According to above table, companies are required to provide above mentioned general

disclosure standards for both core and comprehensive options. It has been seen that core option

limits the standard disclosures while in comprehensive option it is required to provide all

standards. It is certain that companies that make use of comprehensive option to disclose

sustainability information aims to score higher in comparison to reports that make of core option.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 21)

Following are the criteria for specific standard disclosures for both core and comprehensive

options:

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 21)

Following are the criteria for specific standard disclosures for both core and comprehensive

options:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 13)

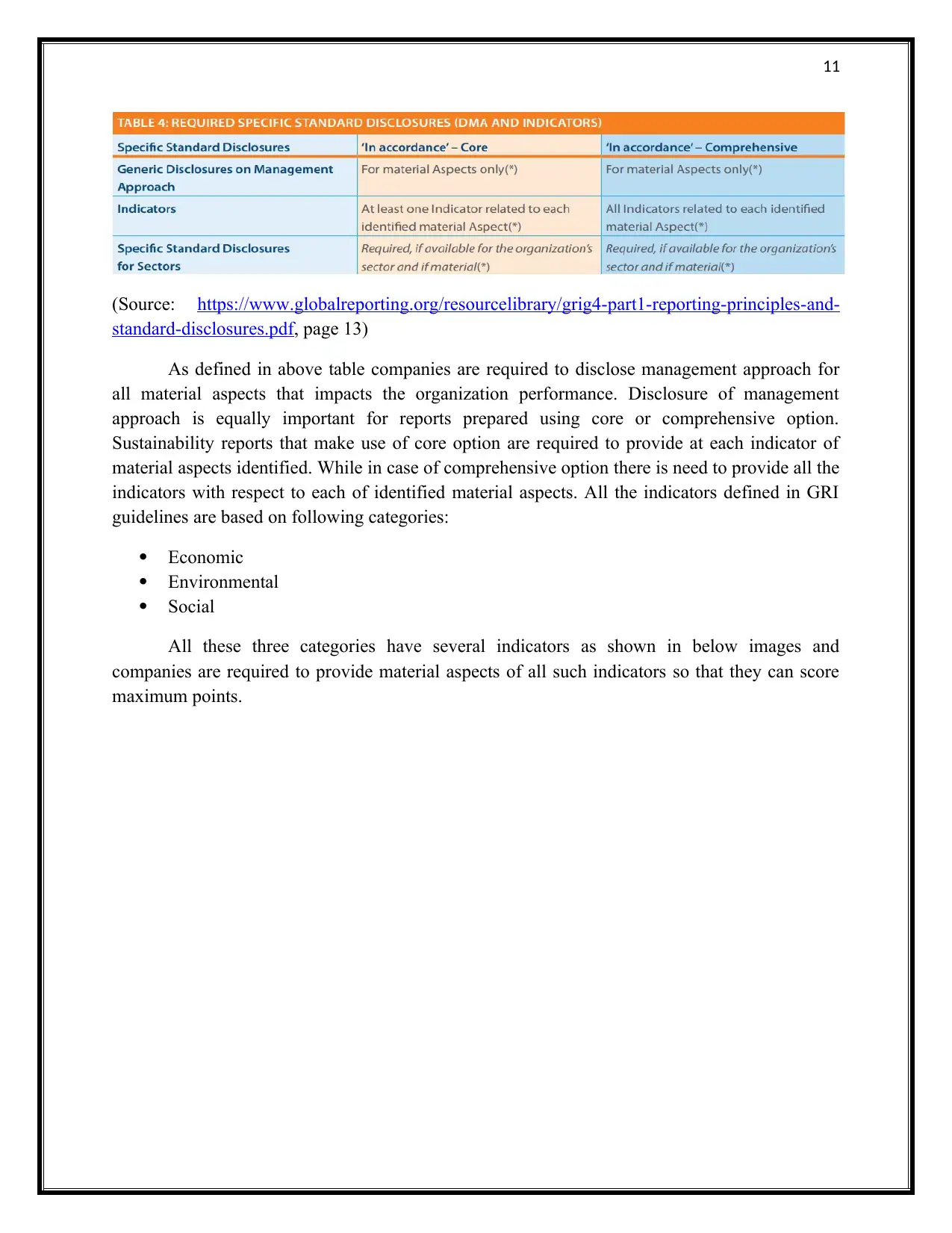

As defined in above table companies are required to disclose management approach for

all material aspects that impacts the organization performance. Disclosure of management

approach is equally important for reports prepared using core or comprehensive option.

Sustainability reports that make use of core option are required to provide at each indicator of

material aspects identified. While in case of comprehensive option there is need to provide all the

indicators with respect to each of identified material aspects. All the indicators defined in GRI

guidelines are based on following categories:

Economic

Environmental

Social

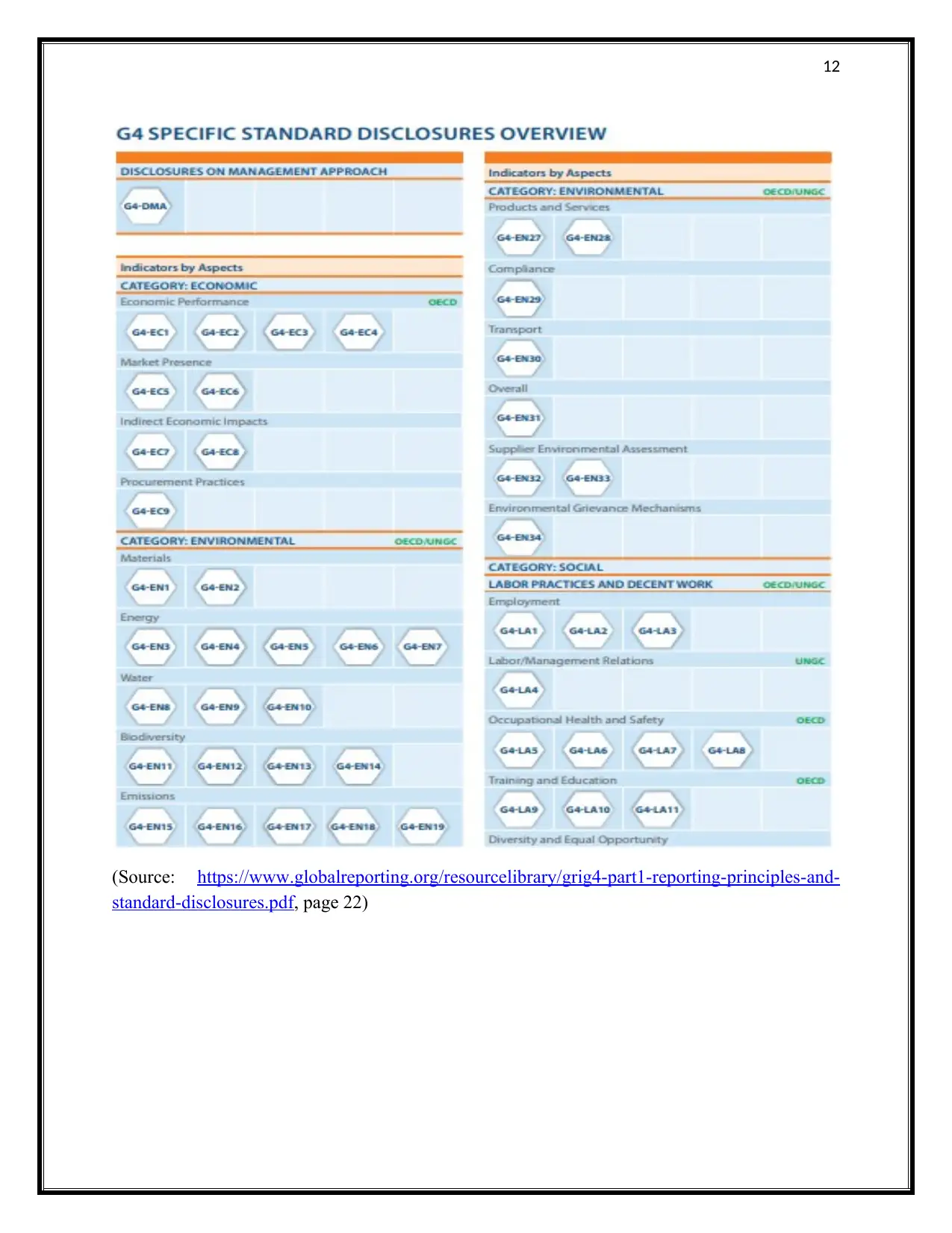

All these three categories have several indicators as shown in below images and

companies are required to provide material aspects of all such indicators so that they can score

maximum points.

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 13)

As defined in above table companies are required to disclose management approach for

all material aspects that impacts the organization performance. Disclosure of management

approach is equally important for reports prepared using core or comprehensive option.

Sustainability reports that make use of core option are required to provide at each indicator of

material aspects identified. While in case of comprehensive option there is need to provide all the

indicators with respect to each of identified material aspects. All the indicators defined in GRI

guidelines are based on following categories:

Economic

Environmental

Social

All these three categories have several indicators as shown in below images and

companies are required to provide material aspects of all such indicators so that they can score

maximum points.

12

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 22)

(Source: https://www.globalreporting.org/resourcelibrary/grig4-part1-reporting-principles-and-

standard-disclosures.pdf, page 22)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.