Review of Current Accounting Issues: Financial Reporting and Ethics

VerifiedAdded on 2021/06/16

|13

|3508

|58

Report

AI Summary

This report provides a detailed review of current accounting issues, primarily focusing on ethical breaches within the accounting profession and the implications for financial reporting. The analysis begins with a discussion of the KPMG scandal, highlighting the detrimental effects of unethical practices and the importance of maintaining integrity in financial reporting. The report then explores the responsibilities of organizations and accountants to stakeholders, emphasizing the need for accurate and transparent financial information. It also delves into the importance of ethical accounting practices, the role of Generally Accepted Accounting Principles (GAAP), and the fundamental principles of professional conduct. Furthermore, the report examines the International Accounting Standards Board's (IASB) proposals for amending accounting standards related to errors, estimates, and policies, including the application of IAS 8 and the implications of voluntary changes. The report concludes by emphasizing the importance of ethical behavior and adherence to accounting standards to maintain trust and ensure the reliability of financial information.

Running head: REVIEW OF CURRENT ACCOUNTING ISSUES

REVIEW OF CURRENT ACCOUNTING ISSUES

Name of the Student:

Name of the University:

Authors Note:

REVIEW OF CURRENT ACCOUNTING ISSUES

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REVIEW OF CURRENT ACCOUNTING ISSUES

Answer to Question 1:

The major challenge that is faced by most of the organization in the recent times is to

convey the information to its non-financial stakeholders. The company’s financial performance

is to be transferred to non-financial employees in a very meaningful and interesting ways.

Recently, a group of former partner of the accounting leading organization KPMG obtained

relevant information and misinterpreted the information (Goldstein, 2018). According to the

reports, the vital data related to the upcoming audit inspections was obtained beforehand. The

information was manipulated to pass the inspection. The misconduct came as highly shocking

and egregious to their people. The upper level management actually steals the audit examination

information so that together audit deficiencies cannot be disclosed.

Since the implosion of WorldCom and Enron, such accounting practices at KPMG

created a negative impact on the mind of the people. The accountants at Public Company

Accounting Oversight Board and KPMG that regulates the activities of auditors in US has

allegedly received or passed information. They helped the firm to prepare their audit inspections

that included at least seven banks. The informationwas allegedly passed to one member to

another in such hope that they could easily get a job in the company. The accountants engaged in

such misconduct to get such passing grade by all the audit inspectors. The employees working at

PCAOB took the information when they were hired at the KPMG as per the charges filed against

them (Shubber, 2018).

It is important to get the clear idea of the problem that was the major cause for such

problem in the upper level of management. KPMG also took various remedial actions to assure

so that such kind of cannot happen again in the future. The companies are accountable to various

stakeholders including partners, customers and investors. It is important for the shareholders and

investors to know the true position of the company as such kind of financial information is

highly important for the achievement if sound investment decisions. The customers are entitled

to know the true financial position of the company so that they can enter into such transactions

that are related to the longevity of the company (Amidon, 2018). It is important for the customers

to know the solvency and stability condition of the organization.

Answer to Question 1:

The major challenge that is faced by most of the organization in the recent times is to

convey the information to its non-financial stakeholders. The company’s financial performance

is to be transferred to non-financial employees in a very meaningful and interesting ways.

Recently, a group of former partner of the accounting leading organization KPMG obtained

relevant information and misinterpreted the information (Goldstein, 2018). According to the

reports, the vital data related to the upcoming audit inspections was obtained beforehand. The

information was manipulated to pass the inspection. The misconduct came as highly shocking

and egregious to their people. The upper level management actually steals the audit examination

information so that together audit deficiencies cannot be disclosed.

Since the implosion of WorldCom and Enron, such accounting practices at KPMG

created a negative impact on the mind of the people. The accountants at Public Company

Accounting Oversight Board and KPMG that regulates the activities of auditors in US has

allegedly received or passed information. They helped the firm to prepare their audit inspections

that included at least seven banks. The informationwas allegedly passed to one member to

another in such hope that they could easily get a job in the company. The accountants engaged in

such misconduct to get such passing grade by all the audit inspectors. The employees working at

PCAOB took the information when they were hired at the KPMG as per the charges filed against

them (Shubber, 2018).

It is important to get the clear idea of the problem that was the major cause for such

problem in the upper level of management. KPMG also took various remedial actions to assure

so that such kind of cannot happen again in the future. The companies are accountable to various

stakeholders including partners, customers and investors. It is important for the shareholders and

investors to know the true position of the company as such kind of financial information is

highly important for the achievement if sound investment decisions. The customers are entitled

to know the true financial position of the company so that they can enter into such transactions

that are related to the longevity of the company (Amidon, 2018). It is important for the customers

to know the solvency and stability condition of the organization.

2REVIEW OF CURRENT ACCOUNTING ISSUES

Ethical and honest accounting practices helps to create a positive environment for the

business. When an organization or its employee’s practices unethical accounting practices, they

lose their trust for their existing and potential customers. It is highly important with all such

industries that completely depend on effectiveand strong professional relationships with their

customers. The KPMG scandal led the employees to surrender their license for practicing

unethical approach to increase profit. The credibility and reputation of the organization is

completely compromised.

It is the legal obligation of the company to report on the financial information in a fair

and accurate manner. The inaccurate information that is provided to the tax agencies can

sometimes lower the organization tax burden but ultimately leads to high fines and charges

against the firm. Therefore ethical accounting practices enable the organization to get their tax

forms properly assessed (Brown, Preiato & Tarca, 2014). This helps the organization to have a

clear conscience and further keeps the matter out of trouble. It is the duty of the upper level

management and the accountants that the sound planning is made with accurate information. The

obligation also includes in facilitating adequate information and furthermore it should be

provided in a particular timeframe. The broad staffer has to further take confidential information

from PCAOB shared with their partners at KPMG. This had led them to struggle for improving

their inspection results.

Integrity is an important fundamental element of the accounting

profession. Integrity requires accountants to be honest, candid and forthright

with a client's financial information. Accountants should restrict themselves

from personal gain or advantage using confidential information (Dillard &

Vinnari, 2017). While errors or differences in opinion regarding the applicability

of accounting laws do exist, professional accountants should avoid the

intentional opportunity to deceive and manipulate financial information.

Integrity is one of the most crucialpart of the accounting profession.

The accountant should be candid, honest and forthright regarding the

client’s financial data. Accountants need to restrict itself from advantages or

personal gain by using confidential information. The differences in opinion or

errors regarding their application for accountability does not actually exists

Ethical and honest accounting practices helps to create a positive environment for the

business. When an organization or its employee’s practices unethical accounting practices, they

lose their trust for their existing and potential customers. It is highly important with all such

industries that completely depend on effectiveand strong professional relationships with their

customers. The KPMG scandal led the employees to surrender their license for practicing

unethical approach to increase profit. The credibility and reputation of the organization is

completely compromised.

It is the legal obligation of the company to report on the financial information in a fair

and accurate manner. The inaccurate information that is provided to the tax agencies can

sometimes lower the organization tax burden but ultimately leads to high fines and charges

against the firm. Therefore ethical accounting practices enable the organization to get their tax

forms properly assessed (Brown, Preiato & Tarca, 2014). This helps the organization to have a

clear conscience and further keeps the matter out of trouble. It is the duty of the upper level

management and the accountants that the sound planning is made with accurate information. The

obligation also includes in facilitating adequate information and furthermore it should be

provided in a particular timeframe. The broad staffer has to further take confidential information

from PCAOB shared with their partners at KPMG. This had led them to struggle for improving

their inspection results.

Integrity is an important fundamental element of the accounting

profession. Integrity requires accountants to be honest, candid and forthright

with a client's financial information. Accountants should restrict themselves

from personal gain or advantage using confidential information (Dillard &

Vinnari, 2017). While errors or differences in opinion regarding the applicability

of accounting laws do exist, professional accountants should avoid the

intentional opportunity to deceive and manipulate financial information.

Integrity is one of the most crucialpart of the accounting profession.

The accountant should be candid, honest and forthright regarding the

client’s financial data. Accountants need to restrict itself from advantages or

personal gain by using confidential information. The differences in opinion or

errors regarding their application for accountability does not actually exists

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REVIEW OF CURRENT ACCOUNTING ISSUES

(Baboukardos & Rimmel, 2016). Therefore, it is important for all such professional

accountant should not avoid this opportunity to manipulate and deceive such

financial information. The private companies or the public accounting firm

should often develop ethical conducts and such codes for their accountants.

The conduct and ethical rules should ensure that the entire accountant

should act in a more consistent manner. When the specific standards or rules

are inadequate within the firm, the accountants should review their actions

and ensure that accepted principles are followed.

The accounting industry actually limits their services accounting firms

and certified public accountant (CPA) and offers their clients. The upper level

management needs to be perform more effectively should compromise their

independence and objectivity. The people performing accounting functions

and has to audit such information by reviewing their own performance. This

furthermore leads them, to hide all such negative financial information for

their company.

Generally Accepted Accounting Principles (GAAP) should be reviewed

by the accountant and such framework should be applied by the company.

Due care are all such ethical values that makes the accountant to review all

the ethical and technical accounting standards. Therefore, clear

understanding of all the financial information so that accountants exercise

competences.

Proper behavior and ethics is highly important for managing the

organization and it gives the accountant a great deal of power relating to

their clients (Shafer, 2015). It is vital for the firm to have certain business ethics

that can be considered as the codes related to values, morals and principles.

This governs their decisions and actions related to the organization. This

covers generally all the broad elements from corporate social responsibility

to corporate governance. The firm should have their own guidelines and

moral principles. This helps them to attract and retain all the employees,

investors and customers. For each and every organization one of the crucial

assets is reputation. It is important to build a positive reputation with an

ethical and consistent behavior. The shareholders and potential investors are

(Baboukardos & Rimmel, 2016). Therefore, it is important for all such professional

accountant should not avoid this opportunity to manipulate and deceive such

financial information. The private companies or the public accounting firm

should often develop ethical conducts and such codes for their accountants.

The conduct and ethical rules should ensure that the entire accountant

should act in a more consistent manner. When the specific standards or rules

are inadequate within the firm, the accountants should review their actions

and ensure that accepted principles are followed.

The accounting industry actually limits their services accounting firms

and certified public accountant (CPA) and offers their clients. The upper level

management needs to be perform more effectively should compromise their

independence and objectivity. The people performing accounting functions

and has to audit such information by reviewing their own performance. This

furthermore leads them, to hide all such negative financial information for

their company.

Generally Accepted Accounting Principles (GAAP) should be reviewed

by the accountant and such framework should be applied by the company.

Due care are all such ethical values that makes the accountant to review all

the ethical and technical accounting standards. Therefore, clear

understanding of all the financial information so that accountants exercise

competences.

Proper behavior and ethics is highly important for managing the

organization and it gives the accountant a great deal of power relating to

their clients (Shafer, 2015). It is vital for the firm to have certain business ethics

that can be considered as the codes related to values, morals and principles.

This governs their decisions and actions related to the organization. This

covers generally all the broad elements from corporate social responsibility

to corporate governance. The firm should have their own guidelines and

moral principles. This helps them to attract and retain all the employees,

investors and customers. For each and every organization one of the crucial

assets is reputation. It is important to build a positive reputation with an

ethical and consistent behavior. The shareholders and potential investors are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REVIEW OF CURRENT ACCOUNTING ISSUES

more likely to get attracted to the organization that adheres to the moral

guidelines of the company. This also makes the company share prices very

high (West, 2018).

Under Section 100, a professional accountant has to generally adopt

the following fundamental principles:

Integrity: the individuals dealing with the financial matters or issues

should be clear, honest and straight forward in providing information related

to all kinds of business and professional relationship.

Objectivity: the accountant should not let any kind of undue influence,

bias or conflict of interest to overstate the business or professional

judgments (Thomson, 2015).

Professional Competence as well as Due Care: the professional

accountant has continued all the duty so that professional knowledge should

be related to current developments in legislations, practices and techniques.

The employees should act diligently and as per the applicable professional

and technical standards while providing their professional services.

Confidentiality: it is the duty of the accountant to respect the

information confidentiality gained as the result of business and professional

relationships. The information obtained should not be disclosed to the third

parties. Unless there is a professional duty or right to disclose the

information, it should not be disclosed.

Professional behavior: the accountant should comply with all the

adequate regulations and laws. Actions should be avoided that discredits the

professions of the accountants (Ho et al., 2015).

Business must be committed to operate in an ethical foundation by

retaining a positive environment. This is possible with effective treatment of

employees as well as good marketing practices that relates to the treatment

of customers and also its prices. Employees always want to work for such

business firms that have a strong business ethics and a long-term goal (De

Colle, Henrique’s & Sarasvathy, 2014). This helps in increasing the productivity of

more likely to get attracted to the organization that adheres to the moral

guidelines of the company. This also makes the company share prices very

high (West, 2018).

Under Section 100, a professional accountant has to generally adopt

the following fundamental principles:

Integrity: the individuals dealing with the financial matters or issues

should be clear, honest and straight forward in providing information related

to all kinds of business and professional relationship.

Objectivity: the accountant should not let any kind of undue influence,

bias or conflict of interest to overstate the business or professional

judgments (Thomson, 2015).

Professional Competence as well as Due Care: the professional

accountant has continued all the duty so that professional knowledge should

be related to current developments in legislations, practices and techniques.

The employees should act diligently and as per the applicable professional

and technical standards while providing their professional services.

Confidentiality: it is the duty of the accountant to respect the

information confidentiality gained as the result of business and professional

relationships. The information obtained should not be disclosed to the third

parties. Unless there is a professional duty or right to disclose the

information, it should not be disclosed.

Professional behavior: the accountant should comply with all the

adequate regulations and laws. Actions should be avoided that discredits the

professions of the accountants (Ho et al., 2015).

Business must be committed to operate in an ethical foundation by

retaining a positive environment. This is possible with effective treatment of

employees as well as good marketing practices that relates to the treatment

of customers and also its prices. Employees always want to work for such

business firms that have a strong business ethics and a long-term goal (De

Colle, Henrique’s & Sarasvathy, 2014). This helps in increasing the productivity of

5REVIEW OF CURRENT ACCOUNTING ISSUES

the employees besides reducing the turnover rates of the labor. When an

individual follows the company moral policies and guidelines, with honesty

and integrity it actually helps the organization to prosper.

It is the responsibility of the Human resource department to make sure

that all of its employees are highly equipped with effective tools. This would

enable them to perform and implement their actions in amore ethical

manner. Organizations that recognize the need of business ethics required to

protect itself from all kind of external and internal risks (Benson et al., 2015).

This approach helps in both the risk and cost reduction of the company.

Appendix:

the employees besides reducing the turnover rates of the labor. When an

individual follows the company moral policies and guidelines, with honesty

and integrity it actually helps the organization to prosper.

It is the responsibility of the Human resource department to make sure

that all of its employees are highly equipped with effective tools. This would

enable them to perform and implement their actions in amore ethical

manner. Organizations that recognize the need of business ethics required to

protect itself from all kind of external and internal risks (Benson et al., 2015).

This approach helps in both the risk and cost reduction of the company.

Appendix:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REVIEW OF CURRENT ACCOUNTING ISSUES

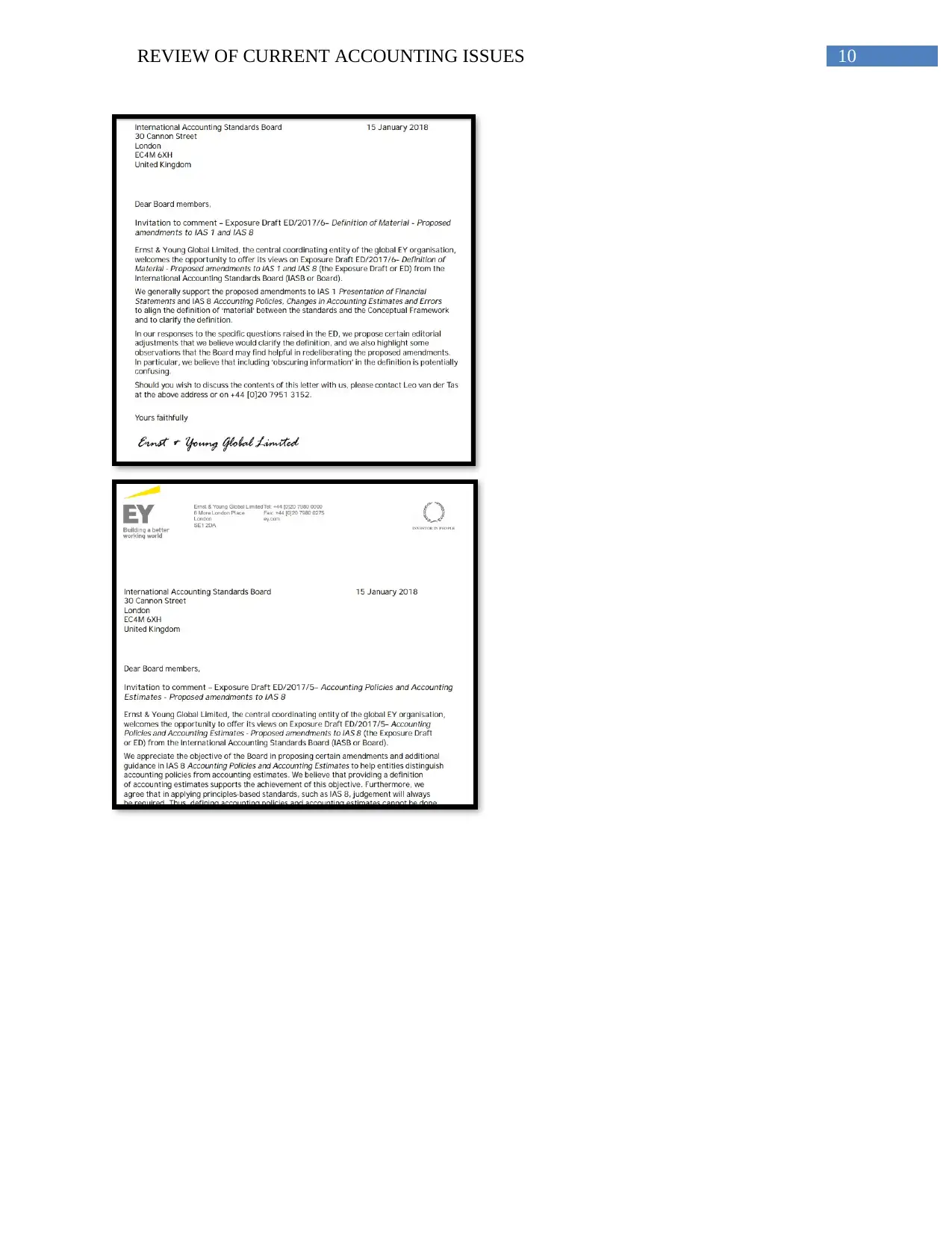

Answer to Question 2:

The international Accounting Standards Board in their exposure draft proposes to amend

the changes related to Accounting Error and Estimates and Accounting policies. The board

expects that such amendments facilitate voluntary changes related to the accounting policy. The

changes will facilities in improving the quality of the financial reporting.

Applying the IAS 8, the organizations accounting policy would be changed if the IFRS

standards allow such kind of changes within the organization. This changes results in the

improving the usefulness of all such information that is provide to the users about the financial

statements. The objectives of the explanatory material that is included in the agenda facilitates

higher amount of consistency due to the application of IFRS standards.

Applying voluntary changes related to the accounting policies can makes the agenda

decisions quite challenging in certain situations. This is due to the fact that IAS 8 requires an

organization to apply such voluntary changes in their accounting policy to such an extent that it

is impracticable.

The IASB board wants to amend IAS 8 by introducing new kind of voluntary changes

within the accounting policy. This results from the decisions of the agenda, which is published

Answer to Question 2:

The international Accounting Standards Board in their exposure draft proposes to amend

the changes related to Accounting Error and Estimates and Accounting policies. The board

expects that such amendments facilitate voluntary changes related to the accounting policy. The

changes will facilities in improving the quality of the financial reporting.

Applying the IAS 8, the organizations accounting policy would be changed if the IFRS

standards allow such kind of changes within the organization. This changes results in the

improving the usefulness of all such information that is provide to the users about the financial

statements. The objectives of the explanatory material that is included in the agenda facilitates

higher amount of consistency due to the application of IFRS standards.

Applying voluntary changes related to the accounting policies can makes the agenda

decisions quite challenging in certain situations. This is due to the fact that IAS 8 requires an

organization to apply such voluntary changes in their accounting policy to such an extent that it

is impracticable.

The IASB board wants to amend IAS 8 by introducing new kind of voluntary changes

within the accounting policy. This results from the decisions of the agenda, which is published

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REVIEW OF CURRENT ACCOUNTING ISSUES

by the IFRS Committee. The proposed threshold initiated by the organization would therefore

include all such considerations that are required for the expected benefits for the financial

statement users. Through the application of latest accounting policy, the cost of entity for deter

mining the effects related to retrospective applications can be easily determined. The draft is

issued in lieu of the public interest and posted on the organizational websites.

Applying changes in the accounting policies:

This includes that an organization is liable for changes in their accounting policy that

results from the application of an IFRS as per the specific transitional provisions.

Whenever an entity would make changes in their accounting policy as per the initial

application of an IFRS. This should not include any particular transitional provisions that

are to be applied voluntarily but all the changes should be applied in a retrospective

manner.

Retrospective application in the accounting policy is possible as per Para 19(a) or (b),

which makes the entity to adjust their opening balance of equity at the earliest most period and

furthermore the other comparative amounts discloses each prior period that is presented as the

new accounting policies has been applied. Though there are various limitations that are related to

these practices. Whenever an organization applies this new policy in a retrospective manner, it

becomes difficult to cumulative or period specific changes.

The other respondent is the Institute of Singapore Chartered Accountants. They

responded to the exposure draft that applies to IFRS 9 financial statements in relation with the

IFRS 4 insurance contracts. ISCA had made a clear cut views from their members on the

exposure via public consultation. The ISCA committee related to Insurance that consists

experienced technical and accounting professionals from the accounting firms. The initiative

taken by IASB to acknowledge the consequences related to different effective dates for IFRS 9

and IFRS 4 phase II involves all such possibilities so that IFRS 9 will be deferred until IFRS

Phase II becomes highly effective (Gimbar, Hansen & Ozlanski, 2016). Although there is a

disadvantage of decreasing comparability related in the intervening period.

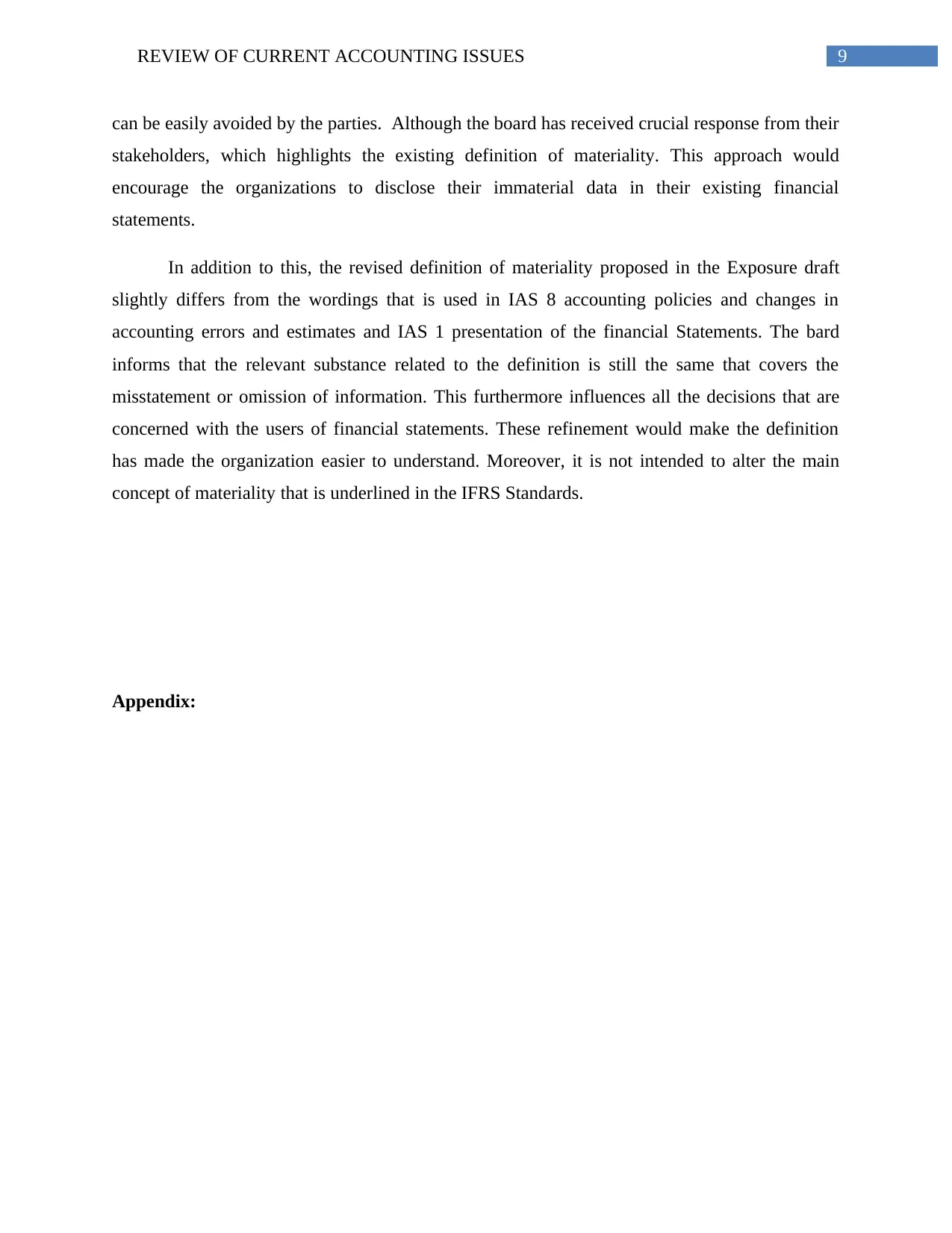

In the exposure draft, the clarification of material is defined while making minor

amendments related to the IAS 1, presentation of financial statements and IAS 8 that is

by the IFRS Committee. The proposed threshold initiated by the organization would therefore

include all such considerations that are required for the expected benefits for the financial

statement users. Through the application of latest accounting policy, the cost of entity for deter

mining the effects related to retrospective applications can be easily determined. The draft is

issued in lieu of the public interest and posted on the organizational websites.

Applying changes in the accounting policies:

This includes that an organization is liable for changes in their accounting policy that

results from the application of an IFRS as per the specific transitional provisions.

Whenever an entity would make changes in their accounting policy as per the initial

application of an IFRS. This should not include any particular transitional provisions that

are to be applied voluntarily but all the changes should be applied in a retrospective

manner.

Retrospective application in the accounting policy is possible as per Para 19(a) or (b),

which makes the entity to adjust their opening balance of equity at the earliest most period and

furthermore the other comparative amounts discloses each prior period that is presented as the

new accounting policies has been applied. Though there are various limitations that are related to

these practices. Whenever an organization applies this new policy in a retrospective manner, it

becomes difficult to cumulative or period specific changes.

The other respondent is the Institute of Singapore Chartered Accountants. They

responded to the exposure draft that applies to IFRS 9 financial statements in relation with the

IFRS 4 insurance contracts. ISCA had made a clear cut views from their members on the

exposure via public consultation. The ISCA committee related to Insurance that consists

experienced technical and accounting professionals from the accounting firms. The initiative

taken by IASB to acknowledge the consequences related to different effective dates for IFRS 9

and IFRS 4 phase II involves all such possibilities so that IFRS 9 will be deferred until IFRS

Phase II becomes highly effective (Gimbar, Hansen & Ozlanski, 2016). Although there is a

disadvantage of decreasing comparability related in the intervening period.

In the exposure draft, the clarification of material is defined while making minor

amendments related to the IAS 1, presentation of financial statements and IAS 8 that is

8REVIEW OF CURRENT ACCOUNTING ISSUES

concerned with the accounting policies and all changes in the accounting errors and estimates.

The proposed draft redefines the nature of material and clears it application to:

Improve the idea related to the explanations that defines material.

Incorporate existing supporting requirements within IAS 1 to all the definitions that allow

them additional prominences.

Align the materiality concept related to IFRS standards. Moreover improvements are to

be made (Watson, 2015).

The Board proposes all such amendment related to IAS 8 and IAS 1 to align the

materiality concept. The respondents are IFRS foundations and the major highlighted issued in

the draft to IAS 8 are as follows:

Materiality of the data obtained is actually depended on the magnitude or the nature of

the information or both. The organization should assess whether all such information’s are preset

individually or in relation with the other information. The material information may be obscured

in nature if it is not communicated clearly to the other parties.

Basis for conclusion:

The basis for conclusion actually summarizes all the considerations related to the

International Accounting Standard Boards while proposing the amendments. The Board of the

company was informed about the financial reporting disclosure through its feedback provided in

the Exposure Draft Initiative (Apostolou et al., 2015). The entities also experience various

difficulties to make materiality judgments while preparing for the financial statements. The

feedback obtained from the respondents will help in making all such materiality judgments that

are related to the generally behavior instead of relating to definitions of material.

The feedback that also indicates few auditors, entities and regulators considers the

financial statements primarily as an important document. Few of the entities have made it quite

easier to use this checklist approach by applying judgment due to the management resources

constraints. Moreover, practicing a mechanical approach would make the judgment to be

challenged by their regulators, auditors and users of the financial statements (Crawford et al.,

2105). Moreover, entities prefer to be cautious while omitting crucial disclosures so that risks

concerned with the accounting policies and all changes in the accounting errors and estimates.

The proposed draft redefines the nature of material and clears it application to:

Improve the idea related to the explanations that defines material.

Incorporate existing supporting requirements within IAS 1 to all the definitions that allow

them additional prominences.

Align the materiality concept related to IFRS standards. Moreover improvements are to

be made (Watson, 2015).

The Board proposes all such amendment related to IAS 8 and IAS 1 to align the

materiality concept. The respondents are IFRS foundations and the major highlighted issued in

the draft to IAS 8 are as follows:

Materiality of the data obtained is actually depended on the magnitude or the nature of

the information or both. The organization should assess whether all such information’s are preset

individually or in relation with the other information. The material information may be obscured

in nature if it is not communicated clearly to the other parties.

Basis for conclusion:

The basis for conclusion actually summarizes all the considerations related to the

International Accounting Standard Boards while proposing the amendments. The Board of the

company was informed about the financial reporting disclosure through its feedback provided in

the Exposure Draft Initiative (Apostolou et al., 2015). The entities also experience various

difficulties to make materiality judgments while preparing for the financial statements. The

feedback obtained from the respondents will help in making all such materiality judgments that

are related to the generally behavior instead of relating to definitions of material.

The feedback that also indicates few auditors, entities and regulators considers the

financial statements primarily as an important document. Few of the entities have made it quite

easier to use this checklist approach by applying judgment due to the management resources

constraints. Moreover, practicing a mechanical approach would make the judgment to be

challenged by their regulators, auditors and users of the financial statements (Crawford et al.,

2105). Moreover, entities prefer to be cautious while omitting crucial disclosures so that risks

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REVIEW OF CURRENT ACCOUNTING ISSUES

can be easily avoided by the parties. Although the board has received crucial response from their

stakeholders, which highlights the existing definition of materiality. This approach would

encourage the organizations to disclose their immaterial data in their existing financial

statements.

In addition to this, the revised definition of materiality proposed in the Exposure draft

slightly differs from the wordings that is used in IAS 8 accounting policies and changes in

accounting errors and estimates and IAS 1 presentation of the financial Statements. The bard

informs that the relevant substance related to the definition is still the same that covers the

misstatement or omission of information. This furthermore influences all the decisions that are

concerned with the users of financial statements. These refinement would make the definition

has made the organization easier to understand. Moreover, it is not intended to alter the main

concept of materiality that is underlined in the IFRS Standards.

Appendix:

can be easily avoided by the parties. Although the board has received crucial response from their

stakeholders, which highlights the existing definition of materiality. This approach would

encourage the organizations to disclose their immaterial data in their existing financial

statements.

In addition to this, the revised definition of materiality proposed in the Exposure draft

slightly differs from the wordings that is used in IAS 8 accounting policies and changes in

accounting errors and estimates and IAS 1 presentation of the financial Statements. The bard

informs that the relevant substance related to the definition is still the same that covers the

misstatement or omission of information. This furthermore influences all the decisions that are

concerned with the users of financial statements. These refinement would make the definition

has made the organization easier to understand. Moreover, it is not intended to alter the main

concept of materiality that is underlined in the IFRS Standards.

Appendix:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REVIEW OF CURRENT ACCOUNTING ISSUES

11REVIEW OF CURRENT ACCOUNTING ISSUES

References:

Amidon, B. (2018). Giving employees skin in the game. [online] Journal of Accountancy.

Available at: https://www.journalofaccountancy.com/issues/2018/may/educating-

employees-on-profitability.html [Accessed 14 May 2018].

Apostolou, B., Dorminey, J. W., Hassell, J. M., & Rebele, J. E. (2015). Accounting education

literature review (2013–2014). Journal of Accounting Education, 33(2), 69-127.

Baboukardos, D., & Rimmel, G. (2016). Value relevance of accounting information under an

integrated reporting approach: A research note. Journal of Accounting and Public

Policy, 35(4), 437-452.

Benson, K., Clarkson, P. M., Smith, T., & Tutticci, I. (2015). A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), 36-88.

Brown, P., Preiato, J., & Tarca, A. (2014). Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), 1-52.

Crawford, L., Ferguson, J., Helliar, C. V., & Power, D. M. (2014). Control over accounting

standards within the European Union: the political controversy surrounding the adoption

of IFRS 8. Critical Perspectives on Accounting, 25(4-5), 304-318.

De Colle, S., Henriques, A., & Sarasvathy, S. (2014). The paradox of corporate social

responsibility standards. Journal of Business Ethics, 125(2), 177-191.

Dillard, J., & Vinnari, E. (2017). A case study of critique: Critical perspectives on critical

accounting. Critical Perspectives on Accounting, 43, 88-109.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6),

1629-1646.

Goldstein, M. (2018). U.S. Accuses Accountants of Trying to Game Reviews of KPMG Audits.

Retrieved from https://www.nytimes.com/2018/01/22/business/kpmg-accountants-

References:

Amidon, B. (2018). Giving employees skin in the game. [online] Journal of Accountancy.

Available at: https://www.journalofaccountancy.com/issues/2018/may/educating-

employees-on-profitability.html [Accessed 14 May 2018].

Apostolou, B., Dorminey, J. W., Hassell, J. M., & Rebele, J. E. (2015). Accounting education

literature review (2013–2014). Journal of Accounting Education, 33(2), 69-127.

Baboukardos, D., & Rimmel, G. (2016). Value relevance of accounting information under an

integrated reporting approach: A research note. Journal of Accounting and Public

Policy, 35(4), 437-452.

Benson, K., Clarkson, P. M., Smith, T., & Tutticci, I. (2015). A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), 36-88.

Brown, P., Preiato, J., & Tarca, A. (2014). Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), 1-52.

Crawford, L., Ferguson, J., Helliar, C. V., & Power, D. M. (2014). Control over accounting

standards within the European Union: the political controversy surrounding the adoption

of IFRS 8. Critical Perspectives on Accounting, 25(4-5), 304-318.

De Colle, S., Henriques, A., & Sarasvathy, S. (2014). The paradox of corporate social

responsibility standards. Journal of Business Ethics, 125(2), 177-191.

Dillard, J., & Vinnari, E. (2017). A case study of critique: Critical perspectives on critical

accounting. Critical Perspectives on Accounting, 43, 88-109.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6),

1629-1646.

Goldstein, M. (2018). U.S. Accuses Accountants of Trying to Game Reviews of KPMG Audits.

Retrieved from https://www.nytimes.com/2018/01/22/business/kpmg-accountants-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.