Current Issues in Financial Reporting: A Case Study of Dynamics Ltd.

VerifiedAdded on 2021/04/21

|8

|1211

|98

Report

AI Summary

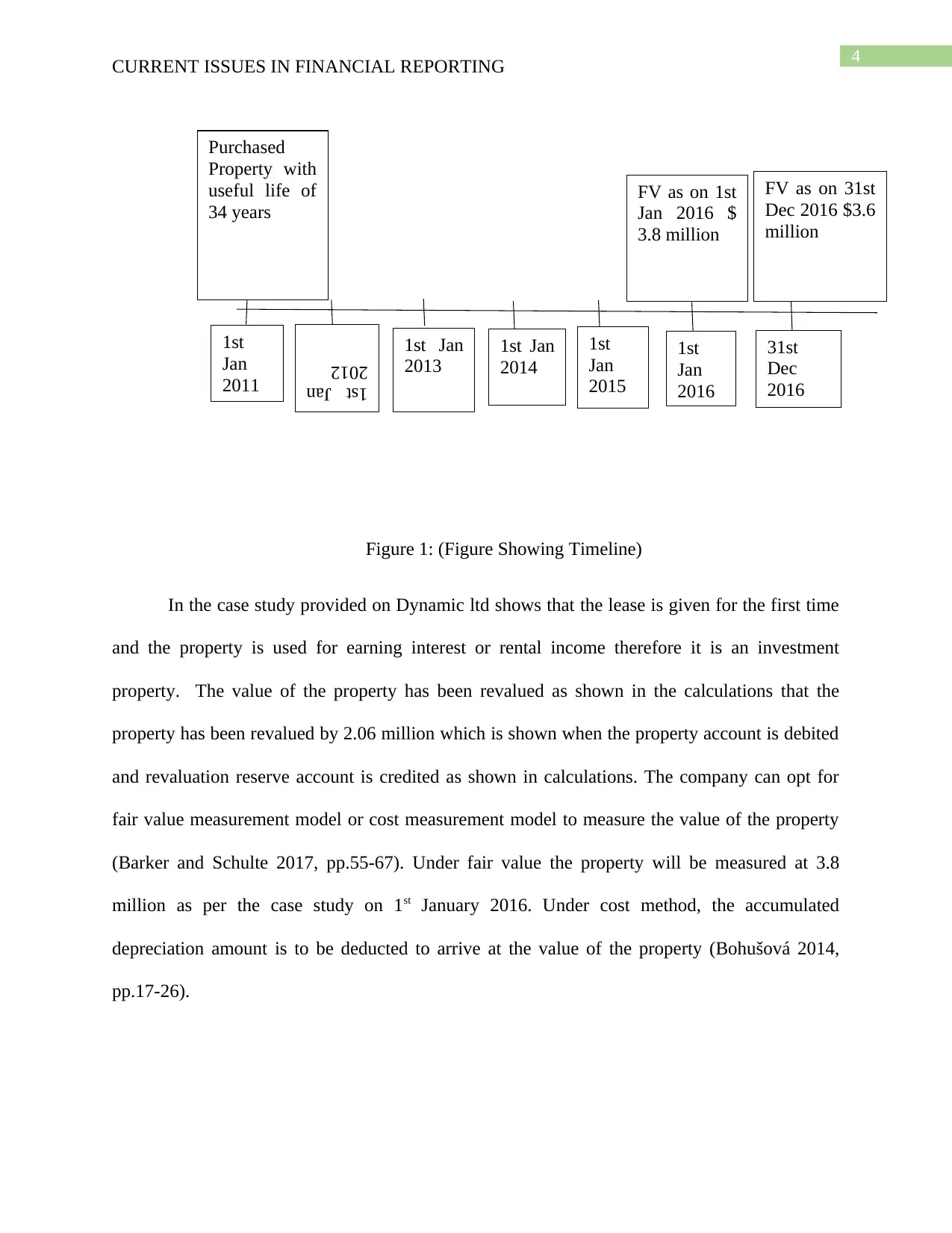

This report analyzes the financial data of Dynamics Ltd., specifically focusing on the accounting treatment of its leased property. The assignment examines the application of International Accounting Standards (IAS) 16, Property, Plant, and Equipment, and IAS 40, Investment Property. The report addresses the recognition of property, plant, and equipment, considering factors like future economic benefits and measurability of cost. It also delves into the measurement principles of investment properties, discussing both the fair value and cost models. The analysis includes a timeline of the property's acquisition, use, and lease, along with the calculation of depreciation and revaluation. The report concludes by highlighting the company's options for measurement and the required disclosures related to these standards. The report is designed to provide insights into financial reporting for students and professionals.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.