Report: Customer Buying Behavior Analysis, Regression, and Results

VerifiedAdded on 2022/11/19

|12

|2411

|1

Report

AI Summary

This report presents an analysis of customer buying behavior, focusing on the factors that influence mall visit frequency. Using a dataset of 856 customers, the study employs descriptive statistics and multiple regression analysis to identify significant predictors. The descriptive analysis summarizes demographic data, income levels, credit card debt, and mall visit frequency. Regression modeling reveals that age, income type (salaried vs. hourly), credit card debt, and neighborhood (specifically, the western region) are statistically significant predictors of mall visit frequency. The report also includes managerial interpretations and implications, such as the importance of targeting younger customers, focusing marketing efforts in the western region, and leveraging credit card usage through reward programs. The conclusion emphasizes the need for a comprehensive buyer profile and suggests further research directions, including comparative studies and the inclusion of data from diverse market places.

Buying behavior of customers

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Abstract......................................................................................................................................3

Introduction................................................................................................................................4

Data Analysis.............................................................................................................................4

Descriptive analysis................................................................................................................4

Regression analytics...............................................................................................................7

Managerial interpretations and Implications..............................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

2

Abstract......................................................................................................................................3

Introduction................................................................................................................................4

Data Analysis.............................................................................................................................4

Descriptive analysis................................................................................................................4

Regression analytics...............................................................................................................7

Managerial interpretations and Implications..............................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

2

Abstract

Using the Pearson correlation and multiple-regression modeling buying behavior in terms of

mall visit frequency was estimated from age, credit card debt, neighborhood, and earning

pattern of consumers. The sample included demographic information and income, shopping

center visit regularity, neighborhood, and credit card liability for 856 customers. In the

sample, 53.5% were male buyers. Average of buyers was 38.78 years (SD =$ 9.61) with

average income of $ 45266.94 (SD = $ 28631.29), and average cc debt of $ 1431.20 (SD = $

1278.04). Age of buyers, earning type, CC debt and buyers from the western region were

statistically significant estimates of purchase frequency.

3

Using the Pearson correlation and multiple-regression modeling buying behavior in terms of

mall visit frequency was estimated from age, credit card debt, neighborhood, and earning

pattern of consumers. The sample included demographic information and income, shopping

center visit regularity, neighborhood, and credit card liability for 856 customers. In the

sample, 53.5% were male buyers. Average of buyers was 38.78 years (SD =$ 9.61) with

average income of $ 45266.94 (SD = $ 28631.29), and average cc debt of $ 1431.20 (SD = $

1278.04). Age of buyers, earning type, CC debt and buyers from the western region were

statistically significant estimates of purchase frequency.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Marketing in shopping malls is an emerging trend for purchasing varieties of commodities

under a single roof. It has great potential because of high penetration and great popularity in

urban areas. This study is about the relationships between mall shopping frequency and

background variables, both demographic and those related to shopping motivations, which

characterize the shopping tendency of a customer. It is well known that buying behavior

depends on the gender and age of customers. Also, affinity towards credit card usage inflicts

positive buying tendency (Arabzadeh, and Aghaeian, 2015, pp.245-256).

Specific reasons underlying mall visits are scrutinized with the help of the multiple regression

model. Using Pearson’s correlation the scholar obtained correlations between customer

variables and shopping frequency. The scholar was able to summarize age, income,

frequency of mall trips, and credit card debt through the descriptive summary. Causal relation

and corresponding hypothesis about the relationship between mall shopping frequency and

characteristics of shoppers such as age, salary type, and credit card debt were tested. A causal

relationship between buying or mall trip frequency and customer variables was established.

Data Analysis

Descriptive analysis

The sample consisted of demographic details along with income, frequency of shopping in

malls, credit card liability of 856 customers. The sample comprised 53.5% male with an

average age of 38.62 years, and 46.5% of females with an average age of 38.97 years. Sample

was primarily from west neighborhood (P = 43.46%), followed by east (P = 32.36%), and

south (P = 24.18%) neighborhoods. Salary payment options were also scrutinized, where

56.19% of participants were identified who earned their income through monthly salary and

4

Marketing in shopping malls is an emerging trend for purchasing varieties of commodities

under a single roof. It has great potential because of high penetration and great popularity in

urban areas. This study is about the relationships between mall shopping frequency and

background variables, both demographic and those related to shopping motivations, which

characterize the shopping tendency of a customer. It is well known that buying behavior

depends on the gender and age of customers. Also, affinity towards credit card usage inflicts

positive buying tendency (Arabzadeh, and Aghaeian, 2015, pp.245-256).

Specific reasons underlying mall visits are scrutinized with the help of the multiple regression

model. Using Pearson’s correlation the scholar obtained correlations between customer

variables and shopping frequency. The scholar was able to summarize age, income,

frequency of mall trips, and credit card debt through the descriptive summary. Causal relation

and corresponding hypothesis about the relationship between mall shopping frequency and

characteristics of shoppers such as age, salary type, and credit card debt were tested. A causal

relationship between buying or mall trip frequency and customer variables was established.

Data Analysis

Descriptive analysis

The sample consisted of demographic details along with income, frequency of shopping in

malls, credit card liability of 856 customers. The sample comprised 53.5% male with an

average age of 38.62 years, and 46.5% of females with an average age of 38.97 years. Sample

was primarily from west neighborhood (P = 43.46%), followed by east (P = 32.36%), and

south (P = 24.18%) neighborhoods. Salary payment options were also scrutinized, where

56.19% of participants were identified who earned their income through monthly salary and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

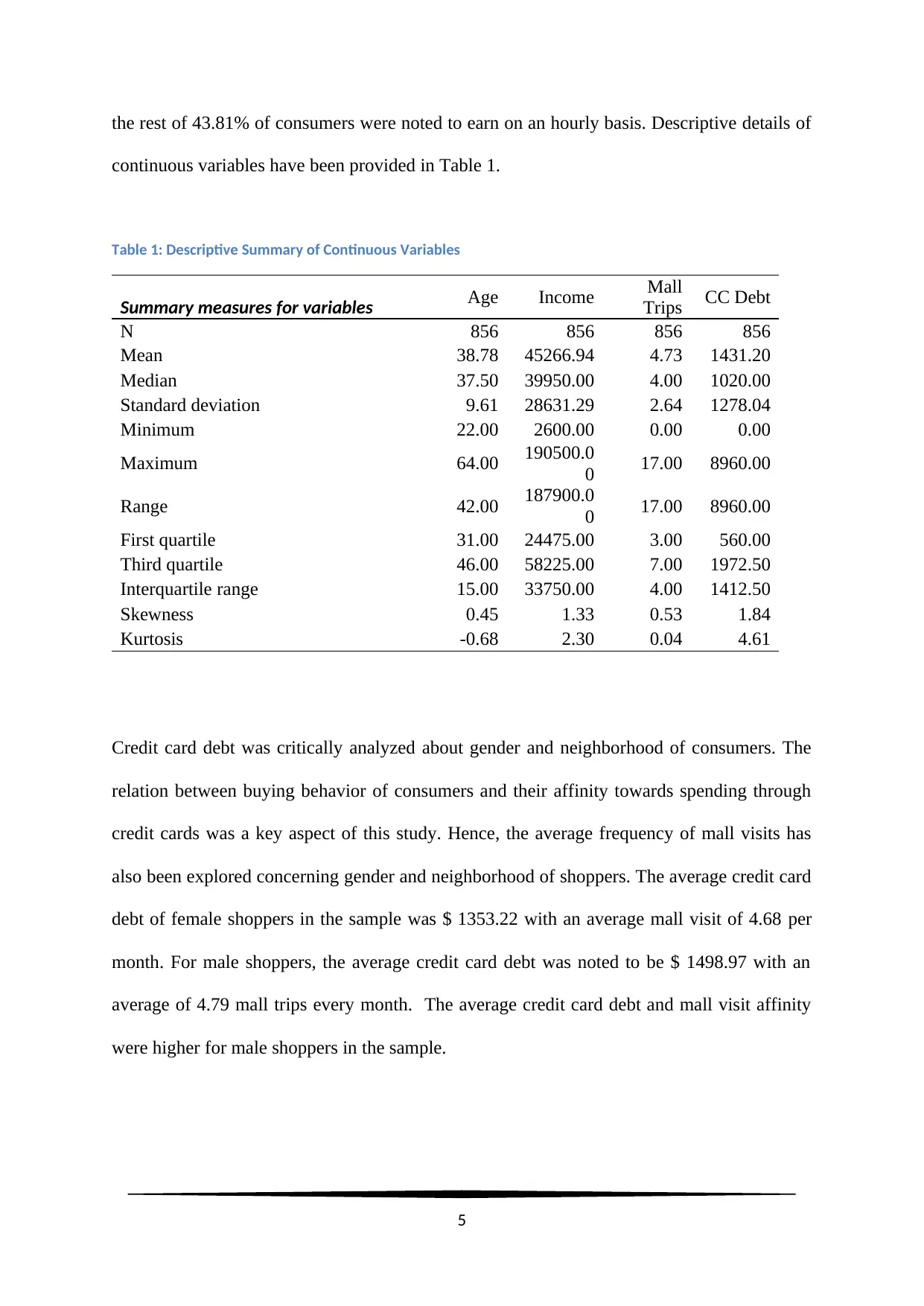

the rest of 43.81% of consumers were noted to earn on an hourly basis. Descriptive details of

continuous variables have been provided in Table 1.

Table 1: Descriptive Summary of Continuous Variables

Summary measures for variables Age Income Mall

Trips CC Debt

N 856 856 856 856

Mean 38.78 45266.94 4.73 1431.20

Median 37.50 39950.00 4.00 1020.00

Standard deviation 9.61 28631.29 2.64 1278.04

Minimum 22.00 2600.00 0.00 0.00

Maximum 64.00 190500.0

0 17.00 8960.00

Range 42.00 187900.0

0 17.00 8960.00

First quartile 31.00 24475.00 3.00 560.00

Third quartile 46.00 58225.00 7.00 1972.50

Interquartile range 15.00 33750.00 4.00 1412.50

Skewness 0.45 1.33 0.53 1.84

Kurtosis -0.68 2.30 0.04 4.61

Credit card debt was critically analyzed about gender and neighborhood of consumers. The

relation between buying behavior of consumers and their affinity towards spending through

credit cards was a key aspect of this study. Hence, the average frequency of mall visits has

also been explored concerning gender and neighborhood of shoppers. The average credit card

debt of female shoppers in the sample was $ 1353.22 with an average mall visit of 4.68 per

month. For male shoppers, the average credit card debt was noted to be $ 1498.97 with an

average of 4.79 mall trips every month. The average credit card debt and mall visit affinity

were higher for male shoppers in the sample.

5

continuous variables have been provided in Table 1.

Table 1: Descriptive Summary of Continuous Variables

Summary measures for variables Age Income Mall

Trips CC Debt

N 856 856 856 856

Mean 38.78 45266.94 4.73 1431.20

Median 37.50 39950.00 4.00 1020.00

Standard deviation 9.61 28631.29 2.64 1278.04

Minimum 22.00 2600.00 0.00 0.00

Maximum 64.00 190500.0

0 17.00 8960.00

Range 42.00 187900.0

0 17.00 8960.00

First quartile 31.00 24475.00 3.00 560.00

Third quartile 46.00 58225.00 7.00 1972.50

Interquartile range 15.00 33750.00 4.00 1412.50

Skewness 0.45 1.33 0.53 1.84

Kurtosis -0.68 2.30 0.04 4.61

Credit card debt was critically analyzed about gender and neighborhood of consumers. The

relation between buying behavior of consumers and their affinity towards spending through

credit cards was a key aspect of this study. Hence, the average frequency of mall visits has

also been explored concerning gender and neighborhood of shoppers. The average credit card

debt of female shoppers in the sample was $ 1353.22 with an average mall visit of 4.68 per

month. For male shoppers, the average credit card debt was noted to be $ 1498.97 with an

average of 4.79 mall trips every month. The average credit card debt and mall visit affinity

were higher for male shoppers in the sample.

5

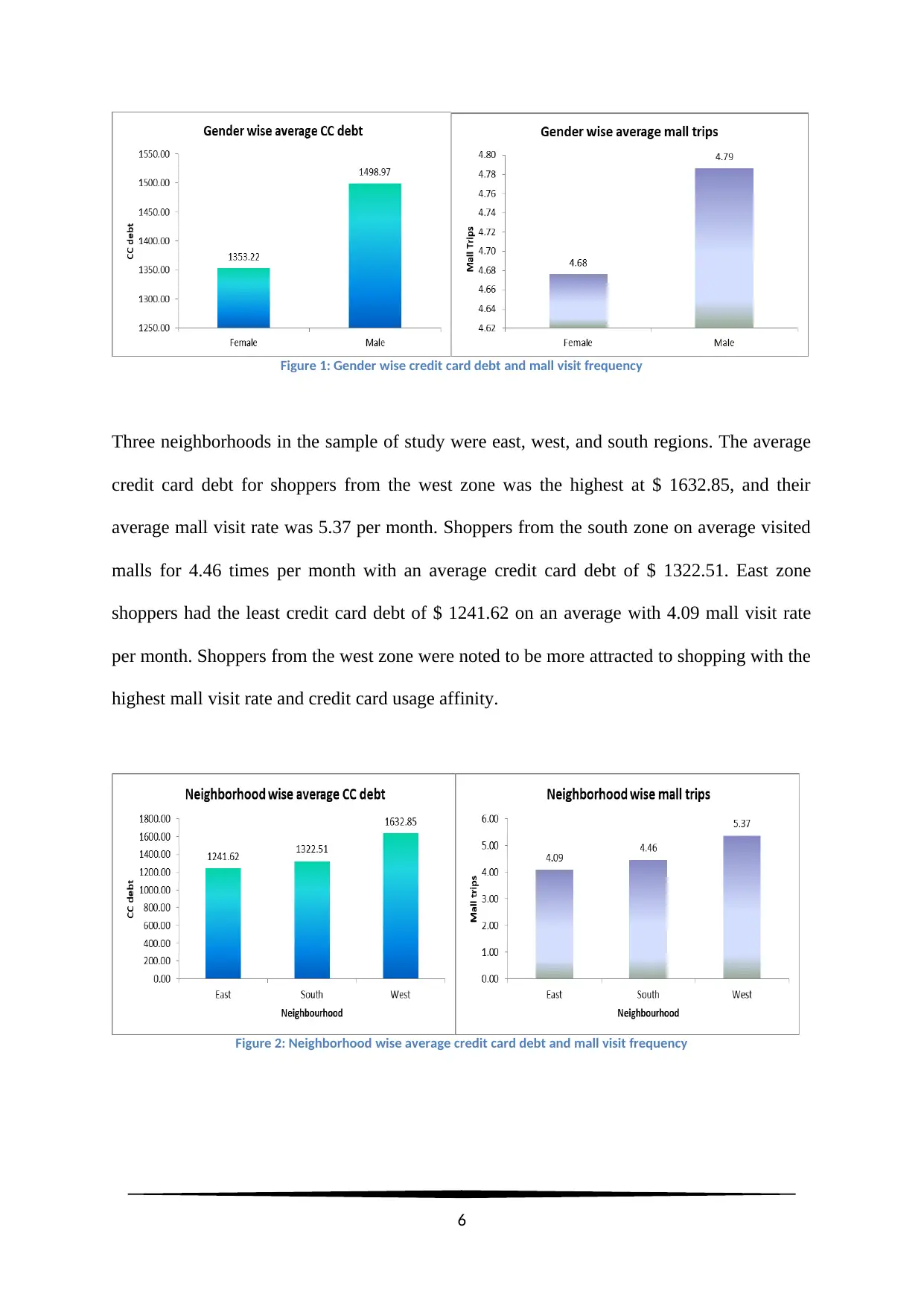

Figure 1: Gender wise credit card debt and mall visit frequency

Three neighborhoods in the sample of study were east, west, and south regions. The average

credit card debt for shoppers from the west zone was the highest at $ 1632.85, and their

average mall visit rate was 5.37 per month. Shoppers from the south zone on average visited

malls for 4.46 times per month with an average credit card debt of $ 1322.51. East zone

shoppers had the least credit card debt of $ 1241.62 on an average with 4.09 mall visit rate

per month. Shoppers from the west zone were noted to be more attracted to shopping with the

highest mall visit rate and credit card usage affinity.

Figure 2: Neighborhood wise average credit card debt and mall visit frequency

6

Three neighborhoods in the sample of study were east, west, and south regions. The average

credit card debt for shoppers from the west zone was the highest at $ 1632.85, and their

average mall visit rate was 5.37 per month. Shoppers from the south zone on average visited

malls for 4.46 times per month with an average credit card debt of $ 1322.51. East zone

shoppers had the least credit card debt of $ 1241.62 on an average with 4.09 mall visit rate

per month. Shoppers from the west zone were noted to be more attracted to shopping with the

highest mall visit rate and credit card usage affinity.

Figure 2: Neighborhood wise average credit card debt and mall visit frequency

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

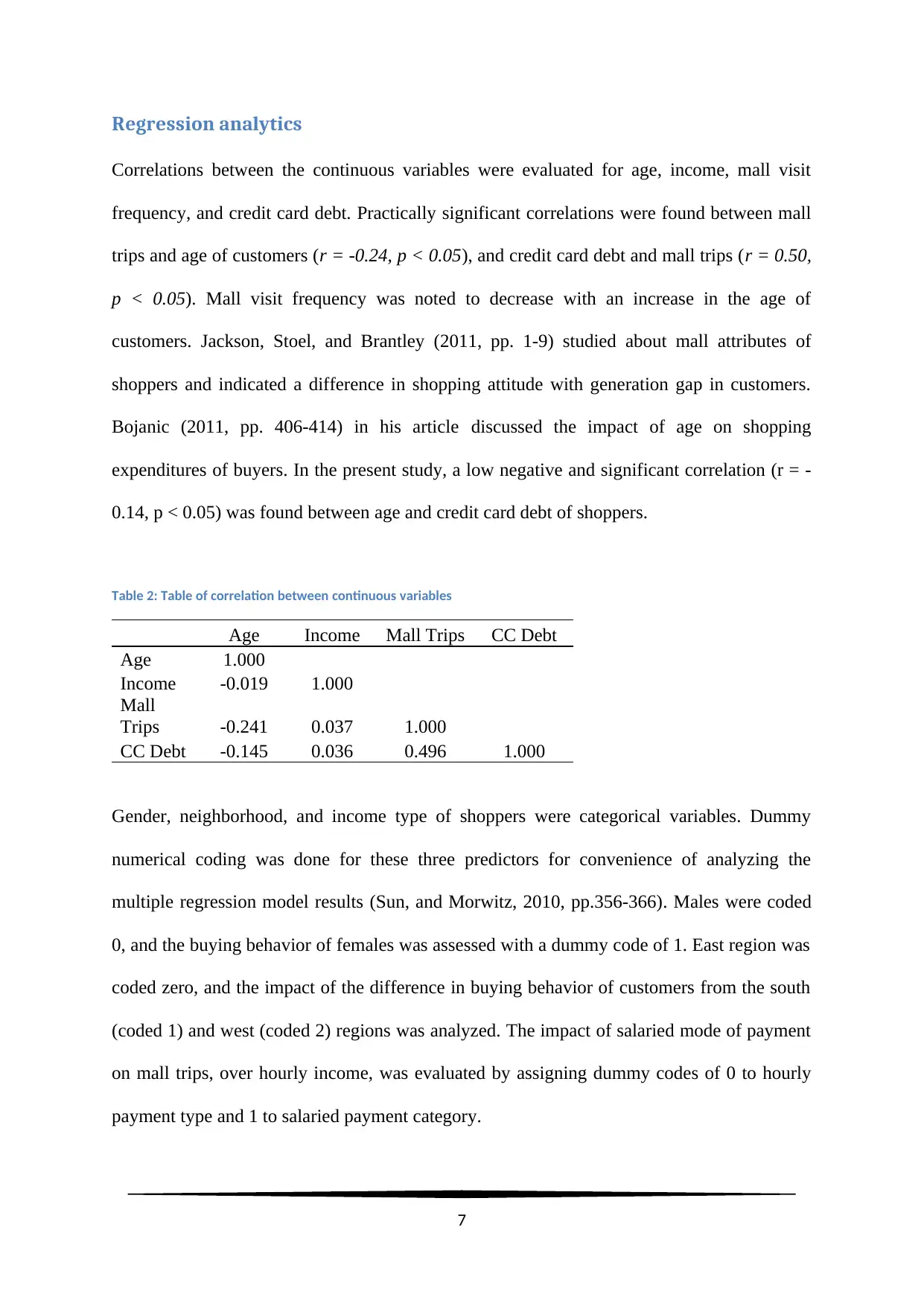

Regression analytics

Correlations between the continuous variables were evaluated for age, income, mall visit

frequency, and credit card debt. Practically significant correlations were found between mall

trips and age of customers (r = -0.24, p < 0.05), and credit card debt and mall trips (r = 0.50,

p < 0.05). Mall visit frequency was noted to decrease with an increase in the age of

customers. Jackson, Stoel, and Brantley (2011, pp. 1-9) studied about mall attributes of

shoppers and indicated a difference in shopping attitude with generation gap in customers.

Bojanic (2011, pp. 406-414) in his article discussed the impact of age on shopping

expenditures of buyers. In the present study, a low negative and significant correlation (r = -

0.14, p < 0.05) was found between age and credit card debt of shoppers.

Table 2: Table of correlation between continuous variables

Age Income Mall Trips CC Debt

Age 1.000

Income -0.019 1.000

Mall

Trips -0.241 0.037 1.000

CC Debt -0.145 0.036 0.496 1.000

Gender, neighborhood, and income type of shoppers were categorical variables. Dummy

numerical coding was done for these three predictors for convenience of analyzing the

multiple regression model results (Sun, and Morwitz, 2010, pp.356-366). Males were coded

0, and the buying behavior of females was assessed with a dummy code of 1. East region was

coded zero, and the impact of the difference in buying behavior of customers from the south

(coded 1) and west (coded 2) regions was analyzed. The impact of salaried mode of payment

on mall trips, over hourly income, was evaluated by assigning dummy codes of 0 to hourly

payment type and 1 to salaried payment category.

7

Correlations between the continuous variables were evaluated for age, income, mall visit

frequency, and credit card debt. Practically significant correlations were found between mall

trips and age of customers (r = -0.24, p < 0.05), and credit card debt and mall trips (r = 0.50,

p < 0.05). Mall visit frequency was noted to decrease with an increase in the age of

customers. Jackson, Stoel, and Brantley (2011, pp. 1-9) studied about mall attributes of

shoppers and indicated a difference in shopping attitude with generation gap in customers.

Bojanic (2011, pp. 406-414) in his article discussed the impact of age on shopping

expenditures of buyers. In the present study, a low negative and significant correlation (r = -

0.14, p < 0.05) was found between age and credit card debt of shoppers.

Table 2: Table of correlation between continuous variables

Age Income Mall Trips CC Debt

Age 1.000

Income -0.019 1.000

Mall

Trips -0.241 0.037 1.000

CC Debt -0.145 0.036 0.496 1.000

Gender, neighborhood, and income type of shoppers were categorical variables. Dummy

numerical coding was done for these three predictors for convenience of analyzing the

multiple regression model results (Sun, and Morwitz, 2010, pp.356-366). Males were coded

0, and the buying behavior of females was assessed with a dummy code of 1. East region was

coded zero, and the impact of the difference in buying behavior of customers from the south

(coded 1) and west (coded 2) regions was analyzed. The impact of salaried mode of payment

on mall trips, over hourly income, was evaluated by assigning dummy codes of 0 to hourly

payment type and 1 to salaried payment category.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A linear multiple regression model has been used to predict frequency of mall visits based on

age, credit card debt, income, gender, neighborhood, and income type of shoppers (west and

south) (Bellman, Lohse, and Johnson, 2009, pp.32-48). In the first model, no statistical

evidence was found to establish any significant difference in the impact of buying behavior of

female shoppers on the frequency of mall visit (t = 0.41, p = 0.68), compared to that of the

males. Income (t = -1.10, p = 0.27), and south region (t = 1.22, p = 0.22) were also noted to

be two statistically insignificant predictors. The second regression model was constructed

without the independent categorical variable, gender. The income of individuals was noted to

be an insignificant predictor (t = -1.09, p = 0.27), and no mediating impact of gender was

noted on income (as income was still not significant predictor, instead of removal of gender

in the second model). After stepwise exclusion of income and south zone from a list of

predictors, the final estimation model was constructed. Age (t = -4.92, p < 0.05), pay type (t

= 4.33, p < 0.05), cc debt (t = 15.47, p < 0.05), and west region (t = 4.03, p < 0.05)

compared to east zone were identified as the four statistically significant estimators of mall

visit frequency of shoppers. The equation of the final regression model was found as Mall

Trips = 4.29 – 0.04 * Age + 0.62 * West + 0.66 * Pay Type (Salaried) + 0.001 * CC Debt.

The residuals of the final model were found to be slightly right-skewed with the presence of

few outlier observations for mall trips. Residual versus fitted plot indicated a well-spread plot

and indicated the presence of no heteroscedasticity. From Table 1, mall trips can be noted as

a slightly positively skewed variable. Therefore, no gross violation of assumptions for

regression modeling was noted (Osborne, and Waters, 2002, pp.1-9).

8

age, credit card debt, income, gender, neighborhood, and income type of shoppers (west and

south) (Bellman, Lohse, and Johnson, 2009, pp.32-48). In the first model, no statistical

evidence was found to establish any significant difference in the impact of buying behavior of

female shoppers on the frequency of mall visit (t = 0.41, p = 0.68), compared to that of the

males. Income (t = -1.10, p = 0.27), and south region (t = 1.22, p = 0.22) were also noted to

be two statistically insignificant predictors. The second regression model was constructed

without the independent categorical variable, gender. The income of individuals was noted to

be an insignificant predictor (t = -1.09, p = 0.27), and no mediating impact of gender was

noted on income (as income was still not significant predictor, instead of removal of gender

in the second model). After stepwise exclusion of income and south zone from a list of

predictors, the final estimation model was constructed. Age (t = -4.92, p < 0.05), pay type (t

= 4.33, p < 0.05), cc debt (t = 15.47, p < 0.05), and west region (t = 4.03, p < 0.05)

compared to east zone were identified as the four statistically significant estimators of mall

visit frequency of shoppers. The equation of the final regression model was found as Mall

Trips = 4.29 – 0.04 * Age + 0.62 * West + 0.66 * Pay Type (Salaried) + 0.001 * CC Debt.

The residuals of the final model were found to be slightly right-skewed with the presence of

few outlier observations for mall trips. Residual versus fitted plot indicated a well-spread plot

and indicated the presence of no heteroscedasticity. From Table 1, mall trips can be noted as

a slightly positively skewed variable. Therefore, no gross violation of assumptions for

regression modeling was noted (Osborne, and Waters, 2002, pp.1-9).

8

Managerial interpretations and Implications

The study of buying behavior is considered a key factor in improving the commodity market

business system in shopping malls. This research tried to explain the problem by examining

demographic as well as other consumer behavioral factors. Understanding these relations can

help in identifying the factors behind the success of a business.

It was interesting that gender was a meaningless factor in describing buying behavior in terms

of purchasing frequency. The results of the present study confirm the outcomes of Paul, and

Rana, (2012, pp.412-422), which argue that gender was not able to predict purchasing

behavior. As age had a detrimental impact on buying tendencies, companies need to attract

more young customers with a variety of products with discounts and online offers. Gamboa

and Gonçalves (2014, pp.709-717) emphasized on attracting young customers through

Facebook promotions, and mall management could do the same. Buyers from the Western

zone were frequently purchasing products, which was evident from higher average credit debt

and mall visits. Following the guidelines provided by Bhattacharya, and Mitra, (2012, pp.1-

4), special offers with aggressive online and offline marketing should be conducted in the

Western region. The most influential factor was the willingness of people to spend through

credit cards. Special emphasis on reward points will be beneficial for attracting young and

credit card using buyers (Bellman, Lohse, and Johnson, 2009, pp.32-48). Salaried buyers

were noted to have considerable high purchasing inclination (mall trips) compared to that of

the hourly paid consumers. Therefore, a consumer profile could be collected utilizing a

product or offer a demonstration. Salaried customers can be provided with attractive EMI

offers (Latha, and Akila, 2016, pp.603-606).

9

The study of buying behavior is considered a key factor in improving the commodity market

business system in shopping malls. This research tried to explain the problem by examining

demographic as well as other consumer behavioral factors. Understanding these relations can

help in identifying the factors behind the success of a business.

It was interesting that gender was a meaningless factor in describing buying behavior in terms

of purchasing frequency. The results of the present study confirm the outcomes of Paul, and

Rana, (2012, pp.412-422), which argue that gender was not able to predict purchasing

behavior. As age had a detrimental impact on buying tendencies, companies need to attract

more young customers with a variety of products with discounts and online offers. Gamboa

and Gonçalves (2014, pp.709-717) emphasized on attracting young customers through

Facebook promotions, and mall management could do the same. Buyers from the Western

zone were frequently purchasing products, which was evident from higher average credit debt

and mall visits. Following the guidelines provided by Bhattacharya, and Mitra, (2012, pp.1-

4), special offers with aggressive online and offline marketing should be conducted in the

Western region. The most influential factor was the willingness of people to spend through

credit cards. Special emphasis on reward points will be beneficial for attracting young and

credit card using buyers (Bellman, Lohse, and Johnson, 2009, pp.32-48). Salaried buyers

were noted to have considerable high purchasing inclination (mall trips) compared to that of

the hourly paid consumers. Therefore, a consumer profile could be collected utilizing a

product or offer a demonstration. Salaried customers can be provided with attractive EMI

offers (Latha, and Akila, 2016, pp.603-606).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

The results in the current article of the correlation and regression analyses revealed the

impact of the significant predictors of the buying behavior of customers. Gender wise

difference in purchasing behavior was not present, but, income type and neighborhood of

buyers mattered a lot. Interestingly, the income of individuals was not a determinant factor in

describing the frequency of mall visits in this research. Age and credit card debt/ heavy usage

of the card were two significant predictors of mall trip frequency.

Any forthcoming research should focus on the complete profile assessment of buyers. A

comparative study with a separate hypothesis for each categorical variable also can reveal the

exact impact on the buying frequency of customers. For a generalization of results, sample

data from all types of market places (including malls) will be necessary.

10

The results in the current article of the correlation and regression analyses revealed the

impact of the significant predictors of the buying behavior of customers. Gender wise

difference in purchasing behavior was not present, but, income type and neighborhood of

buyers mattered a lot. Interestingly, the income of individuals was not a determinant factor in

describing the frequency of mall visits in this research. Age and credit card debt/ heavy usage

of the card were two significant predictors of mall trip frequency.

Any forthcoming research should focus on the complete profile assessment of buyers. A

comparative study with a separate hypothesis for each categorical variable also can reveal the

exact impact on the buying frequency of customers. For a generalization of results, sample

data from all types of market places (including malls) will be necessary.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Arabzadeh, E. and Aghaeian, S., 2015. The relationship between usages and Management of

credit cards on lifestyles and purchasing behaviors of Cardholders. International Journal of

Management Research and Business Strategy, 4(3), pp.245-256.

Bellman, S., Lohse, G. and Johnson, E.J., 2009. Predictors of online buying behavior.

Communications of the ACM, 42, pp.32-48.

Bellman, S., Lohse, G. and Johnson, E.J., 2009. Predictors of online buying behavior.

Communications of the ACM, 42, pp.32-48.

Bhattacharya, S. and Mitra, S., 2012. Consumer Behaviour And Impact Of Brand–A Study

On South Zone Of Kolkata City. Voice of Research, 1(2), pp.1-4.

Bojanic, D.C., 2011. The impact of age and family life experiences on Mexican visitor

shopping expenditures. Tourism Management, 32(2), pp.406-414.

Gamboa, A.M. and Gonçalves, H.M., 2014. Customer loyalty through social networks:

Lessons from Zara on Facebook. Business Horizons, 57(6), pp.709-717.

Jackson, V., Stoel, L., and Brantley, A., 2011. Mall attributes and shopping value:

Differences by gender and generational cohort. Journal of retailing and consumer services,

18(1), pp.1-9.

Latha, B. and Akila, M., 2016. Impact of brand loyalty on purchasing behaviour of selected

consumer durable goods. IJAR, 2(7), pp.603-606.

Osborne, J. and Waters, E., 2002. Four assumptions of multiple regression that researchers

should always test. Practical assessment, research & evaluation, 8(2), pp.1-9.

Paul, J. and Rana, J., 2012. Consumer behavior and purchase intention for organic food.

Journal of consumer Marketing, 29(6), pp.412-422.

Sun, B. and Morwitz, V.G., 2010. Stated intentions and purchase behavior: A unified model.

International Journal of Research in Marketing, 27(4), pp.356-366.

11

Arabzadeh, E. and Aghaeian, S., 2015. The relationship between usages and Management of

credit cards on lifestyles and purchasing behaviors of Cardholders. International Journal of

Management Research and Business Strategy, 4(3), pp.245-256.

Bellman, S., Lohse, G. and Johnson, E.J., 2009. Predictors of online buying behavior.

Communications of the ACM, 42, pp.32-48.

Bellman, S., Lohse, G. and Johnson, E.J., 2009. Predictors of online buying behavior.

Communications of the ACM, 42, pp.32-48.

Bhattacharya, S. and Mitra, S., 2012. Consumer Behaviour And Impact Of Brand–A Study

On South Zone Of Kolkata City. Voice of Research, 1(2), pp.1-4.

Bojanic, D.C., 2011. The impact of age and family life experiences on Mexican visitor

shopping expenditures. Tourism Management, 32(2), pp.406-414.

Gamboa, A.M. and Gonçalves, H.M., 2014. Customer loyalty through social networks:

Lessons from Zara on Facebook. Business Horizons, 57(6), pp.709-717.

Jackson, V., Stoel, L., and Brantley, A., 2011. Mall attributes and shopping value:

Differences by gender and generational cohort. Journal of retailing and consumer services,

18(1), pp.1-9.

Latha, B. and Akila, M., 2016. Impact of brand loyalty on purchasing behaviour of selected

consumer durable goods. IJAR, 2(7), pp.603-606.

Osborne, J. and Waters, E., 2002. Four assumptions of multiple regression that researchers

should always test. Practical assessment, research & evaluation, 8(2), pp.1-9.

Paul, J. and Rana, J., 2012. Consumer behavior and purchase intention for organic food.

Journal of consumer Marketing, 29(6), pp.412-422.

Sun, B. and Morwitz, V.G., 2010. Stated intentions and purchase behavior: A unified model.

International Journal of Research in Marketing, 27(4), pp.356-366.

11

Appendix

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.