In-Depth Case Study: Customer Profitability and Transfer Pricing

VerifiedAdded on 2023/06/07

|9

|2263

|350

Case Study

AI Summary

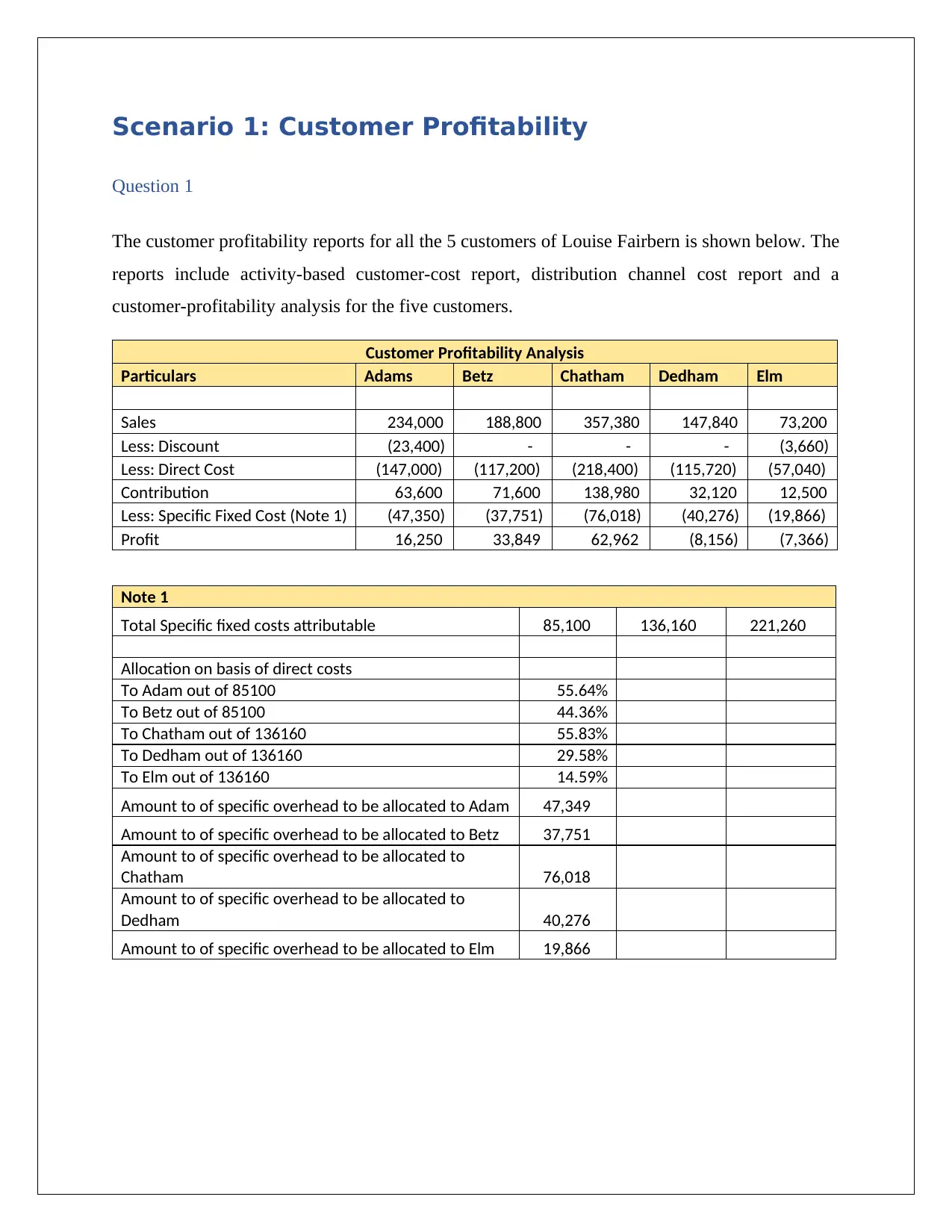

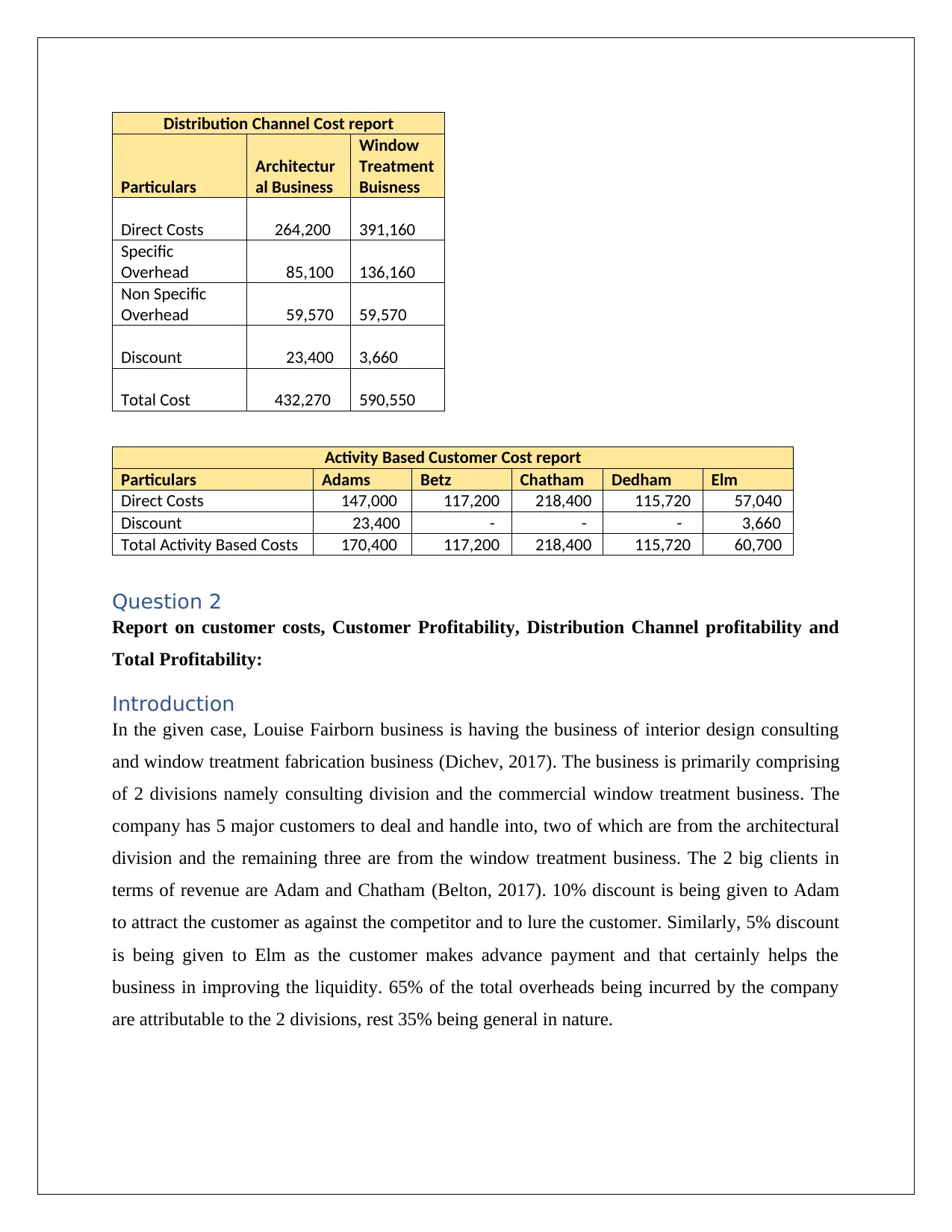

This case study provides a detailed analysis of customer profitability and transfer pricing within a business context. The first scenario focuses on evaluating the profitability of five different customers, considering factors like discounts, direct costs, and specific fixed costs. It highlights the importance of contribution margins and cost allocation in determining customer profitability, recommending cost optimization strategies to improve overall financial performance. The second scenario explores transfer pricing strategies between two divisions of a company, examining the impact of different transfer prices on divisional profitability and goal congruence. It includes calculations for minimum and maximum transfer prices, considering factors such as variable costs, external sales, and capacity constraints. Ultimately, the case study emphasizes the significance of effective cost management, strategic pricing decisions, and interdivisional coordination in achieving sustainable profitability and maximizing shareholder value. Desklib offers similar solved assignments and study tools for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.