Hampshire Company Case Study: A Detailed CVP Analysis - ACC 550

VerifiedAdded on 2023/04/19

|10

|1760

|416

Case Study

AI Summary

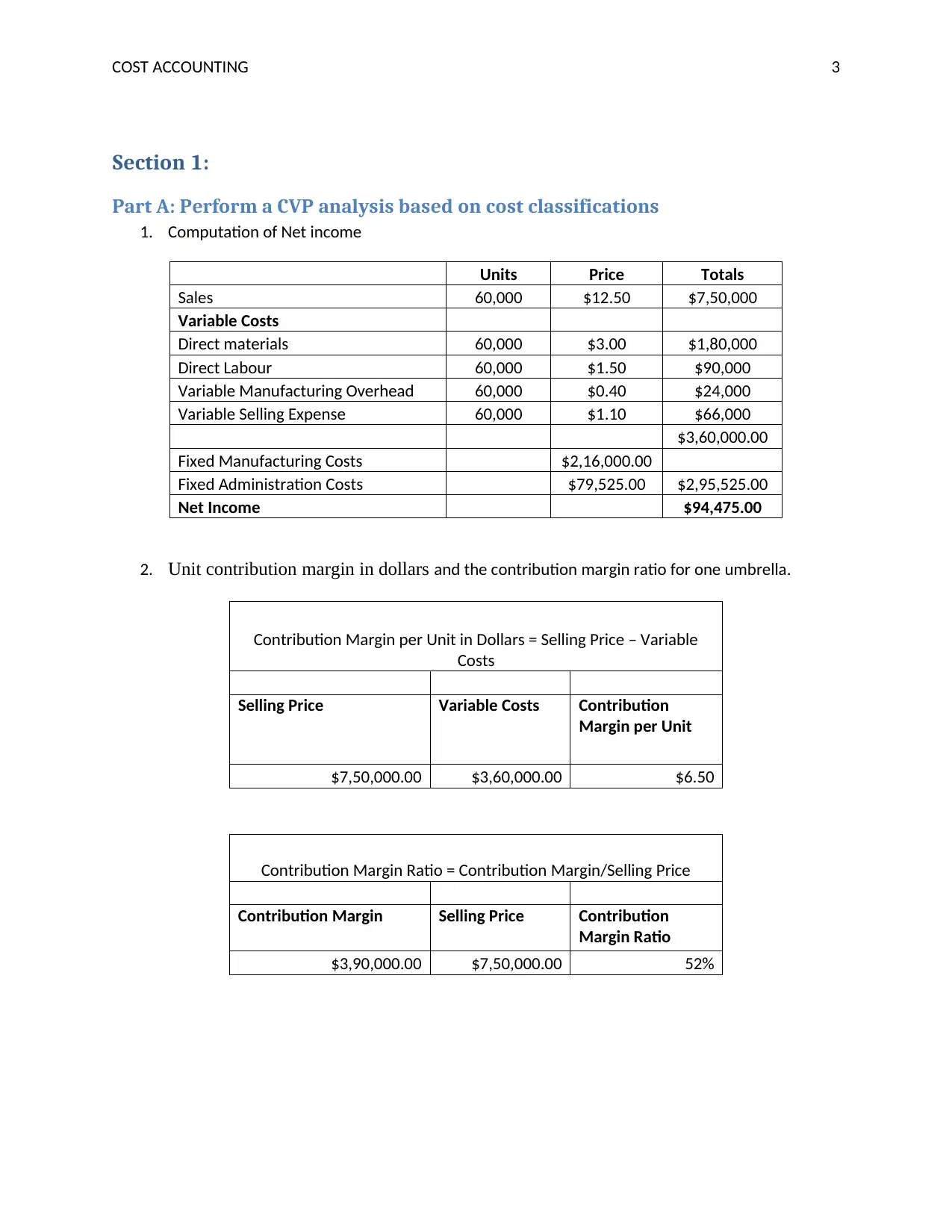

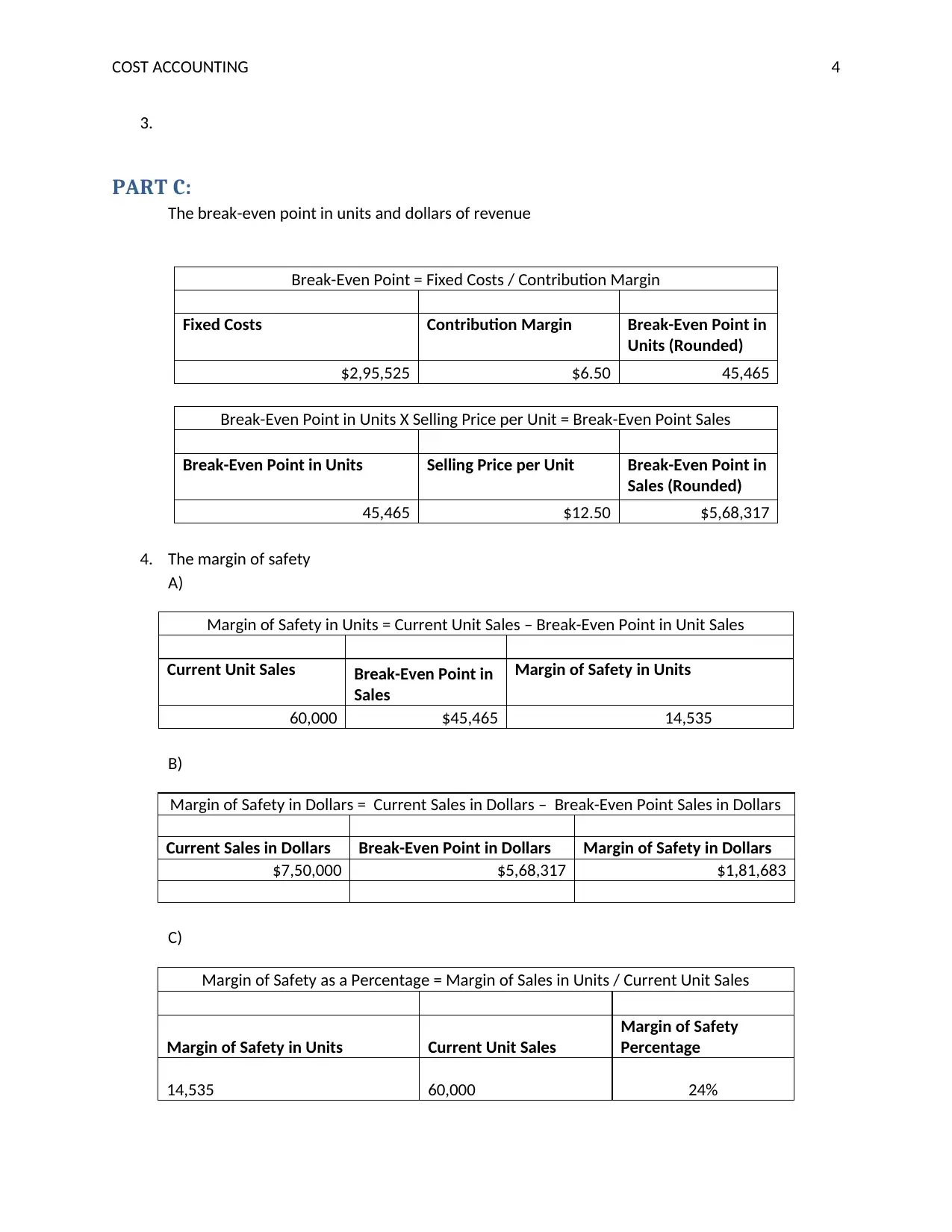

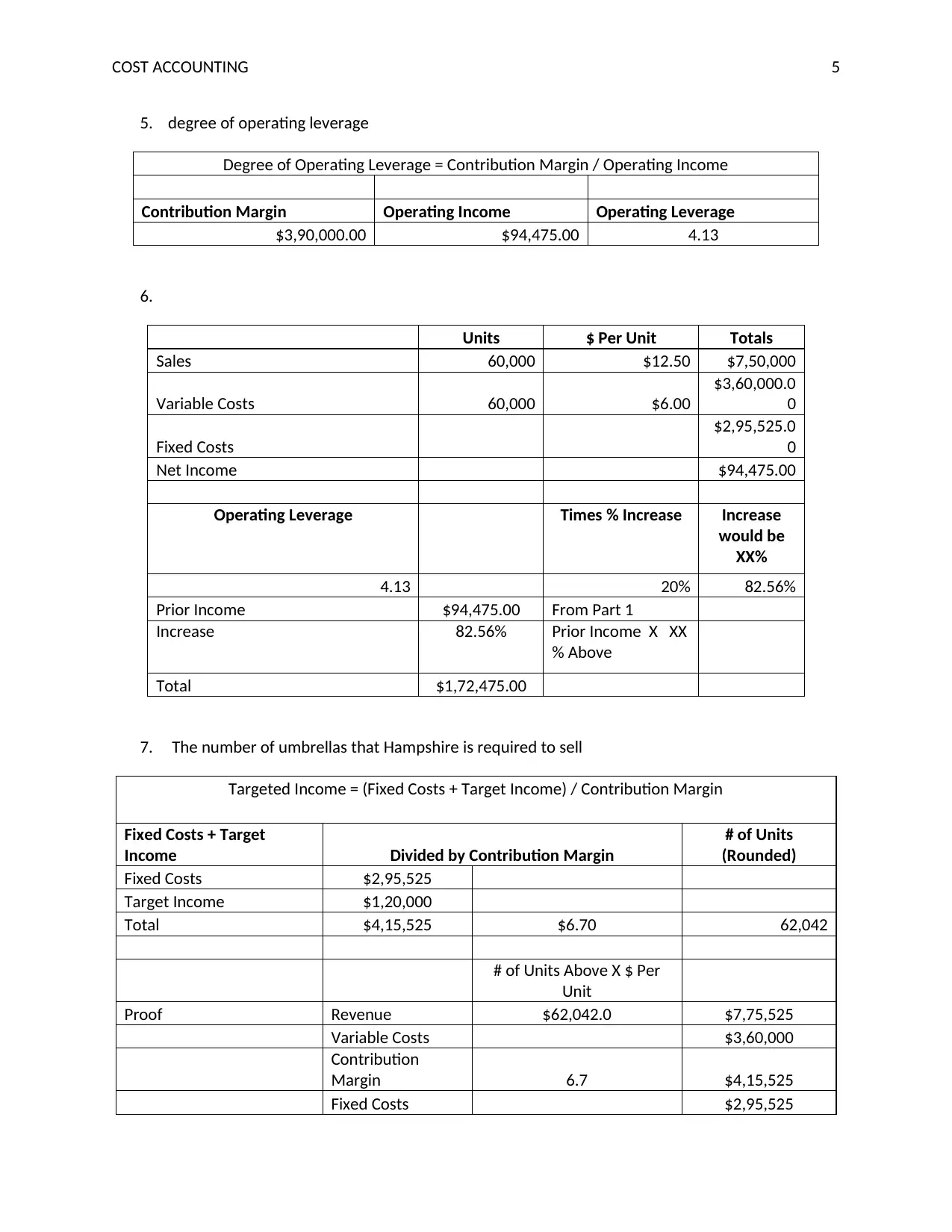

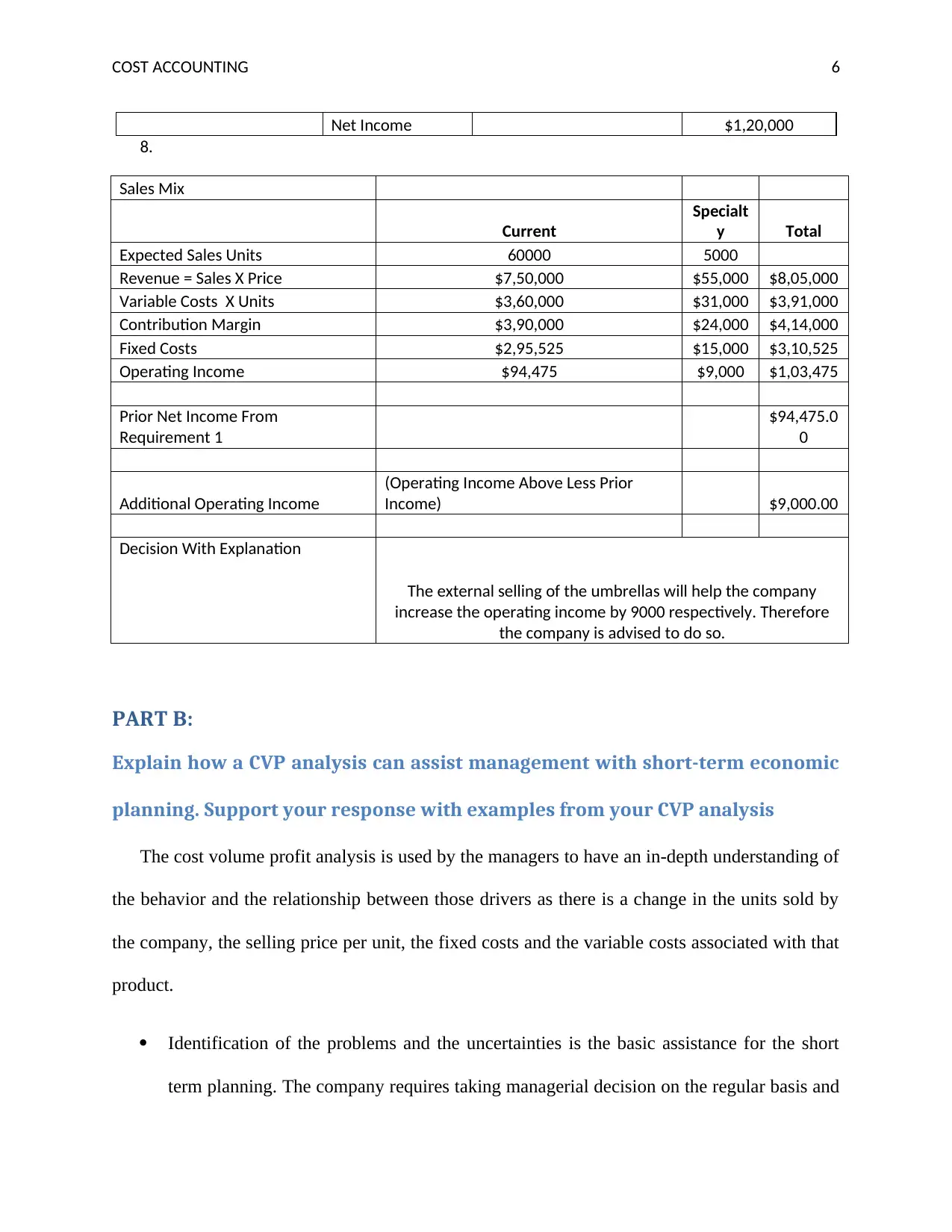

This assignment presents a comprehensive cost-volume-profit (CVP) analysis of the Hampshire Company, focusing on key financial metrics and decision-making implications. The analysis includes the computation of net income, unit contribution margin, contribution margin ratio, break-even points (in units and dollars), margin of safety (in units, dollars, and percentage), and the degree of operating leverage. It also explores the impact of a 20% increase in sales on before-tax income and evaluates the profitability of selling additional units to a touring company. The report further discusses how CVP analysis assists management with short-term economic planning by identifying problems, providing relevant information, and facilitating profit planning. Finally, it determines the company's break-even status and discusses CVP analysis implications on planning, emphasizing its role in cost control and sensitivity analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.