Cost Volume Profit Analysis: Garnet Hotels Budget Hotel Proposal

VerifiedAdded on 2022/09/10

|6

|1407

|20

Report

AI Summary

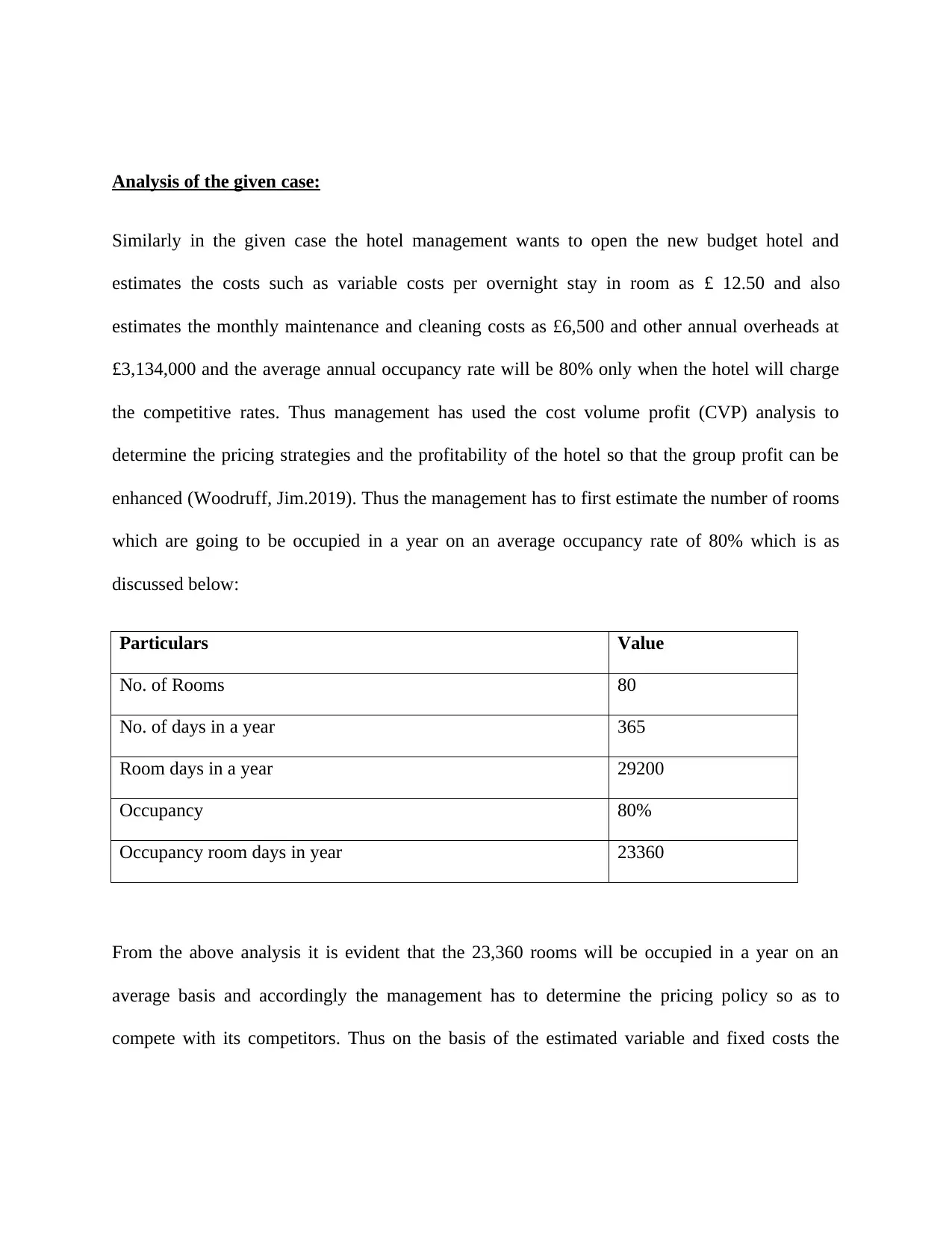

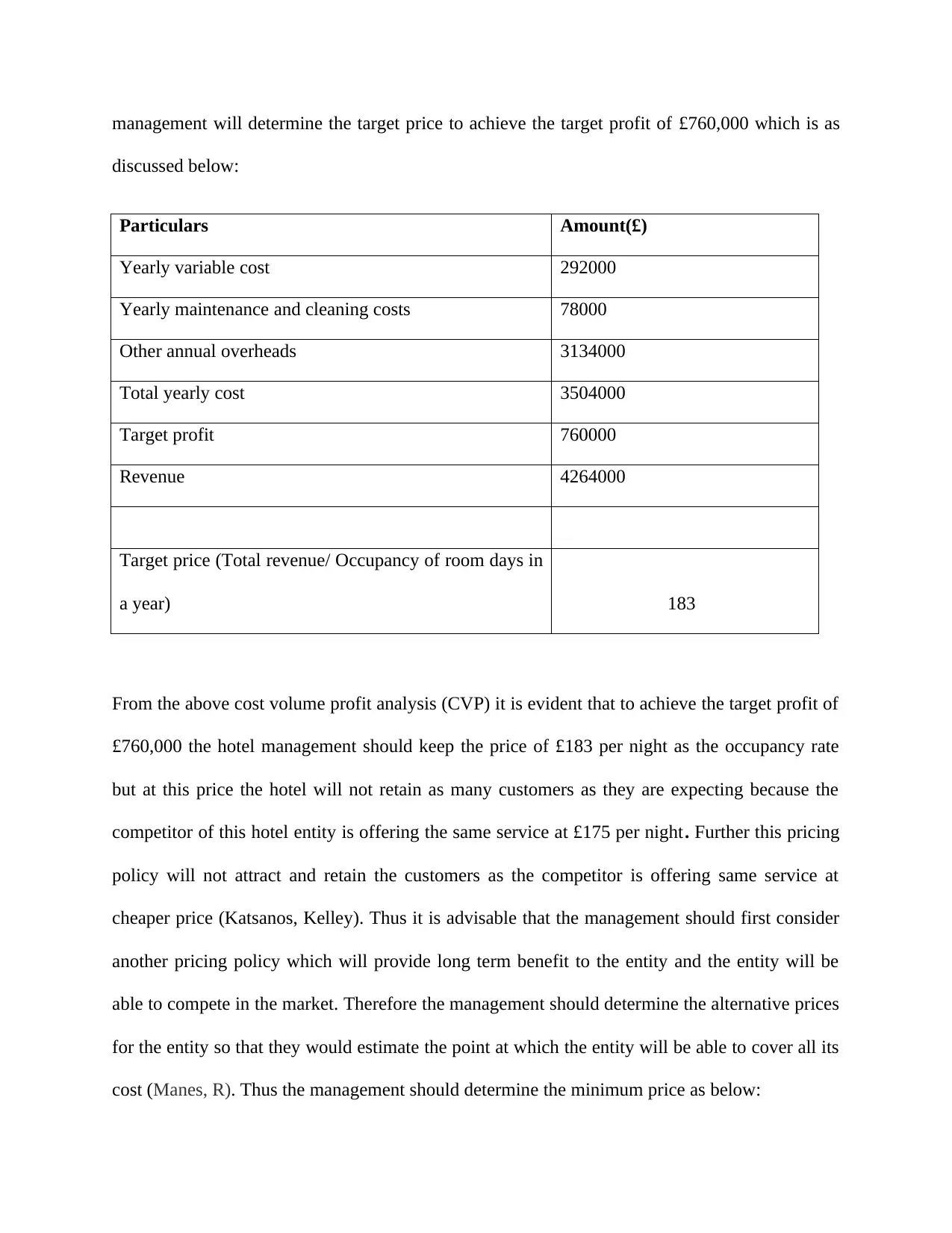

The assignment presents a Cost Volume Profit (CVP) analysis for Garnet Hotels, focusing on the potential expansion with a new budget hotel in London. The analysis considers various costs, including variable costs per room, maintenance, and overheads, to determine the optimal pricing strategy and break-even point. The report calculates the number of occupied rooms, estimates total yearly costs, and evaluates different pricing scenarios to achieve the target profit. It highlights the importance of competitive pricing and occupancy rates, comparing the proposed pricing with competitor offerings. The analysis suggests a price range to maintain competitiveness and profitability, along with the limitations of the CVP analysis, such as dependence on occupancy rates and competitor strategies. The report recommends setting prices between £150 and £175 per night and providing discounts to increase occupancy and profit. The report concludes by emphasizing the need for careful consideration of pricing and market dynamics to ensure the success of the new hotel venture.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.