Managerial Accounting: CVP, Working Capital, Stock Value, & Budgeting

VerifiedAdded on 2023/04/07

|34

|7808

|254

Report

AI Summary

This report provides a detailed analysis of several key concepts in managerial accounting. It begins with a discussion of the usefulness of cost-volume-profit (CVP) analysis, highlighting its benefits in evaluating the impact of changes in cost and volume on a company's operating income. The report then explores various policy options for working capital management, differentiating between short-term and long-term strategies, including hedging policies and their implications. Furthermore, it addresses the statement that managers should not overemphasize current stock value at the expense of long-term profits, examining the potential pitfalls of such a focus. The purpose of internal controls for budgeting is also discussed, emphasizing their role in ensuring financial accuracy and accountability. Finally, the report illustrates the break-even point and analyzes its usefulness, while also acknowledging the limitations of break-even charts. The document uses examples, charts, and calculations to explain these concepts.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 2

Table of Contents

Discuss the usefulness of cost-profit-volume analysis from the company’s point of view..........................3

References...............................................................................................................................................8

Discuss the various policy options available for working capital management in the short versus long

term.............................................................................................................................................................9

References.................................................................................................................................................14

Discuss the statement “Managers should not focus on the current stock value because doing so will lead

to an overemphasis on short-term profits at the expense of long term profits. 232....................................15

References.............................................................................................................................................19

Discuss the purpose of having internal controls for budgeting purposes...................................................21

References.............................................................................................................................................27

Illustrate how the break-even looks like and describe the usefulness of Break-even analysis...................28

References.............................................................................................................................................31

Discuss some of the limitations of break-even charts................................................................................32

References.............................................................................................................................................34

Table of Contents

Discuss the usefulness of cost-profit-volume analysis from the company’s point of view..........................3

References...............................................................................................................................................8

Discuss the various policy options available for working capital management in the short versus long

term.............................................................................................................................................................9

References.................................................................................................................................................14

Discuss the statement “Managers should not focus on the current stock value because doing so will lead

to an overemphasis on short-term profits at the expense of long term profits. 232....................................15

References.............................................................................................................................................19

Discuss the purpose of having internal controls for budgeting purposes...................................................21

References.............................................................................................................................................27

Illustrate how the break-even looks like and describe the usefulness of Break-even analysis...................28

References.............................................................................................................................................31

Discuss some of the limitations of break-even charts................................................................................32

References.............................................................................................................................................34

MANAGERIAL ACCOUNTING 3

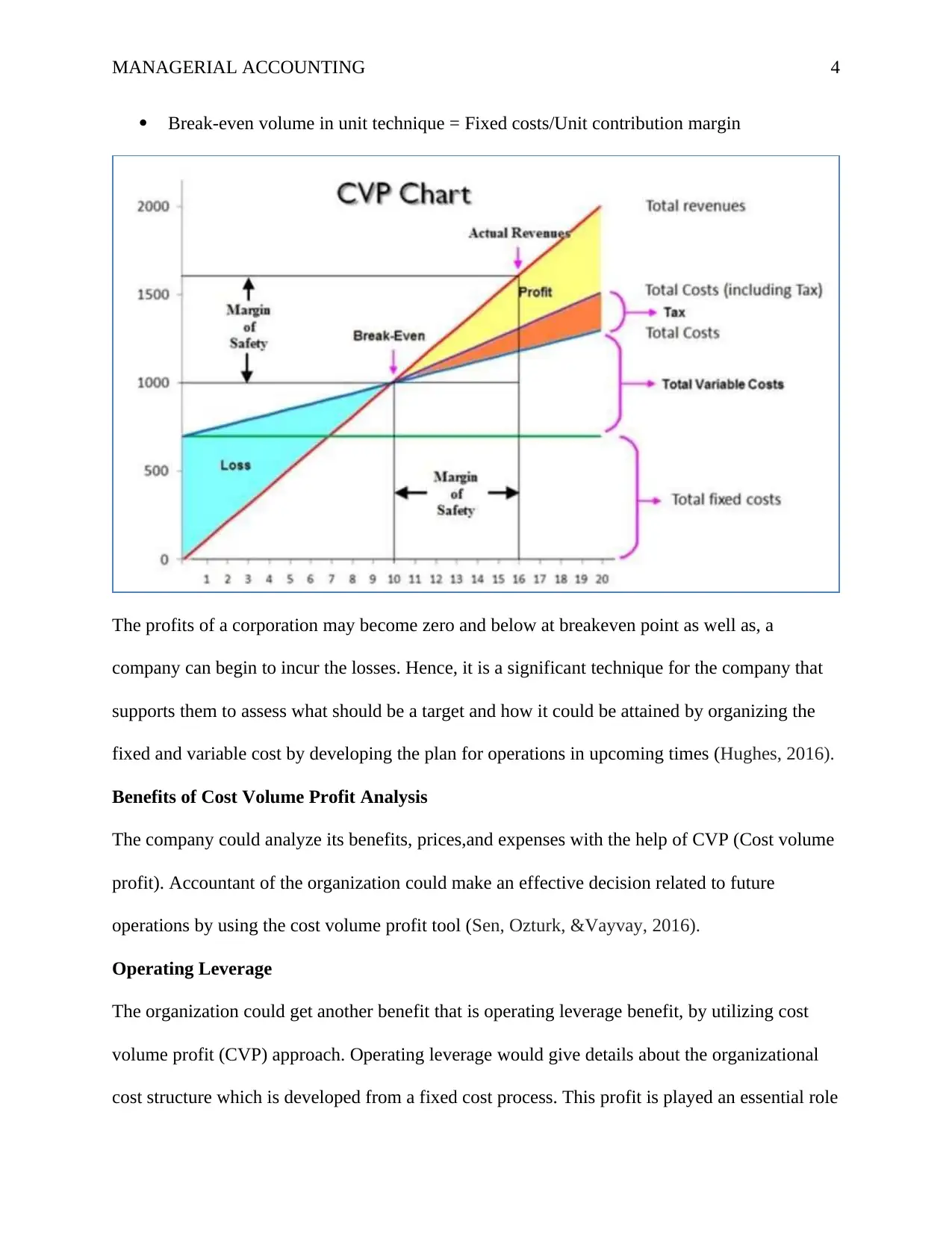

Discuss the usefulness of cost-profit-volume analysis from the company’s point of view.

Cost-volume-profit assessment is useful for evaluating how changes in cost and volume may

influence the operating income of the corporation and net income (Mohammaditabar,

Ghodsypour, &Hafezalkotob, 2016). In order to perform this assessment, several assumptions

were developed by a corporation:

SP(per unit) is stable

VC(per unit) are stable

There isaconstant total fixed cost (TFC)

Costs could be influenced because of activity transformation

When a corporation sells over one product then itcould be traded in the same mix (Peter,

2016).

CVP analysis is essential that all cost of a corporation like manufacturing, selling as well as the

administrative cost can be identified as fixed as well as variable. Cost volume profit assessment

can help the corporation for addressing the breakeven point and it is a point in which profit may

become equal to zero. It can be accomplished by assessing the break-even volume and then

exercising it to develop graphical illustration (Zaharia, &Bordeianu, 2018).

The volume of break-even can either be illustrated in dollars and in a unit. It relies on nature and

type of corporation. For illustration, while a corporation produces a larger volume of the product

then it can prefer for evaluating the breakeven volume in terms of sales dollar whereas, in

context of one Product Company, the unit tool could be a moresignificant calculation in context

of sales volume (Palacio, Adenso‐Díaz, & Lozano,2018). The calculation tool, as well as the

graphical illustration in both terms, would be as follow:

Break-even volume in sales dollar technique = Fixed costs/Contribution margin ratio

Discuss the usefulness of cost-profit-volume analysis from the company’s point of view.

Cost-volume-profit assessment is useful for evaluating how changes in cost and volume may

influence the operating income of the corporation and net income (Mohammaditabar,

Ghodsypour, &Hafezalkotob, 2016). In order to perform this assessment, several assumptions

were developed by a corporation:

SP(per unit) is stable

VC(per unit) are stable

There isaconstant total fixed cost (TFC)

Costs could be influenced because of activity transformation

When a corporation sells over one product then itcould be traded in the same mix (Peter,

2016).

CVP analysis is essential that all cost of a corporation like manufacturing, selling as well as the

administrative cost can be identified as fixed as well as variable. Cost volume profit assessment

can help the corporation for addressing the breakeven point and it is a point in which profit may

become equal to zero. It can be accomplished by assessing the break-even volume and then

exercising it to develop graphical illustration (Zaharia, &Bordeianu, 2018).

The volume of break-even can either be illustrated in dollars and in a unit. It relies on nature and

type of corporation. For illustration, while a corporation produces a larger volume of the product

then it can prefer for evaluating the breakeven volume in terms of sales dollar whereas, in

context of one Product Company, the unit tool could be a moresignificant calculation in context

of sales volume (Palacio, Adenso‐Díaz, & Lozano,2018). The calculation tool, as well as the

graphical illustration in both terms, would be as follow:

Break-even volume in sales dollar technique = Fixed costs/Contribution margin ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 4

Break-even volume in unit technique = Fixed costs/Unit contribution margin

The profits of a corporation may become zero and below at breakeven point as well as, a

company can begin to incur the losses. Hence, it is a significant technique for the company that

supports them to assess what should be a target and how it could be attained by organizing the

fixed and variable cost by developing the plan for operations in upcoming times (Hughes, 2016).

Benefits of Cost Volume Profit Analysis

The company could analyze its benefits, prices,and expenses with the help of CVP (Cost volume

profit). Accountant of the organization could make an effective decision related to future

operations by using the cost volume profit tool (Sen, Ozturk, &Vayvay, 2016).

Operating Leverage

The organization could get another benefit that is operating leverage benefit, by utilizing cost

volume profit (CVP) approach. Operating leverage would give details about the organizational

cost structure which is developed from a fixed cost process. This profit is played an essential role

Break-even volume in unit technique = Fixed costs/Unit contribution margin

The profits of a corporation may become zero and below at breakeven point as well as, a

company can begin to incur the losses. Hence, it is a significant technique for the company that

supports them to assess what should be a target and how it could be attained by organizing the

fixed and variable cost by developing the plan for operations in upcoming times (Hughes, 2016).

Benefits of Cost Volume Profit Analysis

The company could analyze its benefits, prices,and expenses with the help of CVP (Cost volume

profit). Accountant of the organization could make an effective decision related to future

operations by using the cost volume profit tool (Sen, Ozturk, &Vayvay, 2016).

Operating Leverage

The organization could get another benefit that is operating leverage benefit, by utilizing cost

volume profit (CVP) approach. Operating leverage would give details about the organizational

cost structure which is developed from a fixed cost process. This profit is played an essential role

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 5

for the company because the cost structure is related to the company’s benefit and development

phase of the firm (Klochko, Rybyantseva, &Oksanich,2016).

Each organization has its own operating leverage approach due to differentiatingits position from

the competitors in the market place. Operating leverage of the company would be good when

their fixed cost would be high from variable cost and it contributes to increasing the margins of

product. Besides this, a higher breakeven point of organization would support to increase the

fixed sale of the company. The financial success of an organization totally depends upon a higher

breakeven point as it would assist the company to get more profits (Potkány, &Krajčírová,

2017).

Future Forecasting

Through the above-mentioned approaches, models, and graphs, a manager can assess the way

where the company can move and this assessment would support to better comprehend the

different activities as well as an operation within the company. By getting earlier understanding

regarding profits and costs, companies can them in a more effective wayof gaining productivity

(Yao, &Xu, 2018).

Price Determination

It is another advantage of practicing this approach. For instance, when any market player within

the dental industry has developed the price at 50, 000 for single dental operation as well as

business cannot offer this operation at any expenses lower than 20000 then company can practice

cost profit volume assessment for comparing the price of competitor with variable and fixed

costs of its operations and therefore it can manage the price of company (Venegas, & Ventura,

2018).

Profit Planning

for the company because the cost structure is related to the company’s benefit and development

phase of the firm (Klochko, Rybyantseva, &Oksanich,2016).

Each organization has its own operating leverage approach due to differentiatingits position from

the competitors in the market place. Operating leverage of the company would be good when

their fixed cost would be high from variable cost and it contributes to increasing the margins of

product. Besides this, a higher breakeven point of organization would support to increase the

fixed sale of the company. The financial success of an organization totally depends upon a higher

breakeven point as it would assist the company to get more profits (Potkány, &Krajčírová,

2017).

Future Forecasting

Through the above-mentioned approaches, models, and graphs, a manager can assess the way

where the company can move and this assessment would support to better comprehend the

different activities as well as an operation within the company. By getting earlier understanding

regarding profits and costs, companies can them in a more effective wayof gaining productivity

(Yao, &Xu, 2018).

Price Determination

It is another advantage of practicing this approach. For instance, when any market player within

the dental industry has developed the price at 50, 000 for single dental operation as well as

business cannot offer this operation at any expenses lower than 20000 then company can practice

cost profit volume assessment for comparing the price of competitor with variable and fixed

costs of its operations and therefore it can manage the price of company (Venegas, & Ventura,

2018).

Profit Planning

MANAGERIAL ACCOUNTING 6

The objective of any business is to generate the value for consumers and to obtain the profits for

the corporation. But, managing all costs and operation is such a way that can increase profit is

not an easy task. Hence, an organization has to consider different things for engaging in adequate

profit planning tools. The CVP assessment can support the corporations for developing the best

and most profitable integration related to sales volume, cost,and price. Hence, it can support the

manager for estimated and calculated their profit at a different level as well as, for different

products range (Mohammaditabar, Ghodsypour, &Hafezalkotob, 2016).

Risk Assessment

The business world is transforming and because of several internal and external threats related to

any industry, businesses should face too many uncertainties. Although, the measurement of risk

and return through measuring the constant (beta) is a technique in finance however, managerial

accounting is also concerned about this. Managing uncertainty is too effective for business as it

may tend to define all the process as well as practices entailed within the company. Hence, CVP

is a technique that helps for measuring the risk specifically with respect to cost and volumes.

After assessing this uncertainty, companies can get a better solution for declining this risk (Peter,

2016).

Decision Making

All of the above-stated benefits regarding cost volume profit assessment are directly and

indirectly associated with the decision procedure for the company. Any business company

should develop the decision about price, products, their cost as well as fixed and variable unit

expenses. The CVP approach may simplify the process by offering the corporation with a

breakeven point as well as by helping them for engaging in effective decision-making as well as

planning for future (Zaharia, &Bordeianu, 2018).

The objective of any business is to generate the value for consumers and to obtain the profits for

the corporation. But, managing all costs and operation is such a way that can increase profit is

not an easy task. Hence, an organization has to consider different things for engaging in adequate

profit planning tools. The CVP assessment can support the corporations for developing the best

and most profitable integration related to sales volume, cost,and price. Hence, it can support the

manager for estimated and calculated their profit at a different level as well as, for different

products range (Mohammaditabar, Ghodsypour, &Hafezalkotob, 2016).

Risk Assessment

The business world is transforming and because of several internal and external threats related to

any industry, businesses should face too many uncertainties. Although, the measurement of risk

and return through measuring the constant (beta) is a technique in finance however, managerial

accounting is also concerned about this. Managing uncertainty is too effective for business as it

may tend to define all the process as well as practices entailed within the company. Hence, CVP

is a technique that helps for measuring the risk specifically with respect to cost and volumes.

After assessing this uncertainty, companies can get a better solution for declining this risk (Peter,

2016).

Decision Making

All of the above-stated benefits regarding cost volume profit assessment are directly and

indirectly associated with the decision procedure for the company. Any business company

should develop the decision about price, products, their cost as well as fixed and variable unit

expenses. The CVP approach may simplify the process by offering the corporation with a

breakeven point as well as by helping them for engaging in effective decision-making as well as

planning for future (Zaharia, &Bordeianu, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 7

Operating Leverage

Another advantageous that a company can gain by practicing the CVP approach is operating

leverage advantageous which describes how the structuring of cost within an organization is

made up related to fixed cost procedure. There is huge advantageous as cost structure may be

directly associated with the level of profit and growth related to the company (Palacio, Adenso‐

Díaz, & Lozano, 2018).

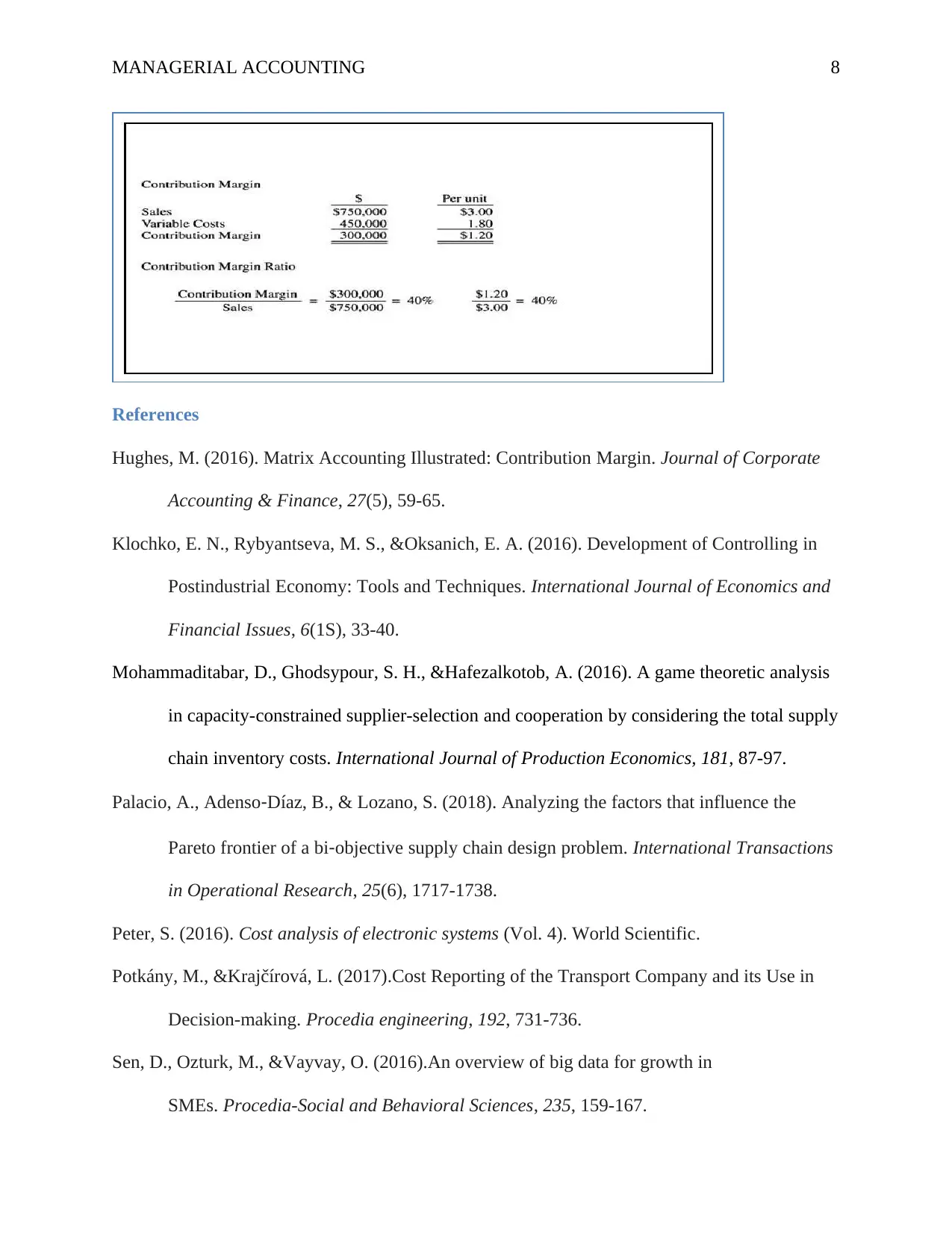

Contribution margin and contribution margin ratio

Major calculation while considering CVP assessment is contribution as well as contribution

margin ration. The contribution margin demonstrates amount of income and profits of company

before withholding its FC. In another way, it is sales dollars amount that are presentedto cover

the fixed expenses. While measured as the ratio, companies can demonstrate the percent of sales

dollars that areavailable for covering the fixed expenses. After covering the fixed expenses, the

next dollar of sales outcomes will create income (Hughes, 2016).

It is also related to revenues deducting from variable expenses. Contribution margin could be

measured through per unit as well as dollar basis. When a company has revenue of $750,000 as

well as TVC is $450,000 then, contribution margin for this company would be $300,000. It is

assumed that a company can sell 250,000 units at the time of year; per unit sales price is $3, as

well as $1.80 will obtain as a TVC per unit. Furthermore, $1.20 will be obtained as contribution

margin per unit and, 40% will be contribution margin ratio. CVP is calculated through

contribution margin in dollars and per unit. For assessing ratio related to margin ofcontribution,

it is divided by revenue and sales volume (Sen, Ozturk, &Vayvay, 2016).

Operating Leverage

Another advantageous that a company can gain by practicing the CVP approach is operating

leverage advantageous which describes how the structuring of cost within an organization is

made up related to fixed cost procedure. There is huge advantageous as cost structure may be

directly associated with the level of profit and growth related to the company (Palacio, Adenso‐

Díaz, & Lozano, 2018).

Contribution margin and contribution margin ratio

Major calculation while considering CVP assessment is contribution as well as contribution

margin ration. The contribution margin demonstrates amount of income and profits of company

before withholding its FC. In another way, it is sales dollars amount that are presentedto cover

the fixed expenses. While measured as the ratio, companies can demonstrate the percent of sales

dollars that areavailable for covering the fixed expenses. After covering the fixed expenses, the

next dollar of sales outcomes will create income (Hughes, 2016).

It is also related to revenues deducting from variable expenses. Contribution margin could be

measured through per unit as well as dollar basis. When a company has revenue of $750,000 as

well as TVC is $450,000 then, contribution margin for this company would be $300,000. It is

assumed that a company can sell 250,000 units at the time of year; per unit sales price is $3, as

well as $1.80 will obtain as a TVC per unit. Furthermore, $1.20 will be obtained as contribution

margin per unit and, 40% will be contribution margin ratio. CVP is calculated through

contribution margin in dollars and per unit. For assessing ratio related to margin ofcontribution,

it is divided by revenue and sales volume (Sen, Ozturk, &Vayvay, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 8

References

Hughes, M. (2016). Matrix Accounting Illustrated: Contribution Margin. Journal of Corporate

Accounting & Finance, 27(5), 59-65.

Klochko, E. N., Rybyantseva, M. S., &Oksanich, E. A. (2016). Development of Controlling in

Postindustrial Economy: Tools and Techniques. International Journal of Economics and

Financial Issues, 6(1S), 33-40.

Mohammaditabar, D., Ghodsypour, S. H., &Hafezalkotob, A. (2016). A game theoretic analysis

in capacity-constrained supplier-selection and cooperation by considering the total supply

chain inventory costs. International Journal of Production Economics, 181, 87-97.

Palacio, A., Adenso‐Díaz, B., & Lozano, S. (2018). Analyzing the factors that influence the

Pareto frontier of a bi‐objective supply chain design problem. International Transactions

in Operational Research, 25(6), 1717-1738.

Peter, S. (2016). Cost analysis of electronic systems (Vol. 4). World Scientific.

Potkány, M., &Krajčírová, L. (2017).Cost Reporting of the Transport Company and its Use in

Decision-making. Procedia engineering, 192, 731-736.

Sen, D., Ozturk, M., &Vayvay, O. (2016).An overview of big data for growth in

SMEs. Procedia-Social and Behavioral Sciences, 235, 159-167.

References

Hughes, M. (2016). Matrix Accounting Illustrated: Contribution Margin. Journal of Corporate

Accounting & Finance, 27(5), 59-65.

Klochko, E. N., Rybyantseva, M. S., &Oksanich, E. A. (2016). Development of Controlling in

Postindustrial Economy: Tools and Techniques. International Journal of Economics and

Financial Issues, 6(1S), 33-40.

Mohammaditabar, D., Ghodsypour, S. H., &Hafezalkotob, A. (2016). A game theoretic analysis

in capacity-constrained supplier-selection and cooperation by considering the total supply

chain inventory costs. International Journal of Production Economics, 181, 87-97.

Palacio, A., Adenso‐Díaz, B., & Lozano, S. (2018). Analyzing the factors that influence the

Pareto frontier of a bi‐objective supply chain design problem. International Transactions

in Operational Research, 25(6), 1717-1738.

Peter, S. (2016). Cost analysis of electronic systems (Vol. 4). World Scientific.

Potkány, M., &Krajčírová, L. (2017).Cost Reporting of the Transport Company and its Use in

Decision-making. Procedia engineering, 192, 731-736.

Sen, D., Ozturk, M., &Vayvay, O. (2016).An overview of big data for growth in

SMEs. Procedia-Social and Behavioral Sciences, 235, 159-167.

MANAGERIAL ACCOUNTING 9

Venegas, B. B., & Ventura, J. A. (2018). A two-stage supply chain coordination mechanism

considering price-sensitive demand and quantity discounts. European Journal of

Operational Research, 264(2), 524-533.

Yao, Y., &Xu, Y. (2018).Dynamic decision making in mass customization. Computers &

Industrial Engineering, 120, 129-136.

Zaharia, V., &Bordeianu, D. (2018). COST STRATEGIES IN MANUFACTURING

COMPANIES. Proceedings in Manufacturing Systems, 13(4), 157.

Discuss the various policy options available for working capital management in the short

versus long term.

Working capital policy deals to sources as well as the working capital amount that a corporation

can maintain. A company cannot only face issues regarding the number of existing assetsbut also

regarding the proportion related to long-term sources in order to finances the existing assets.

There are different policies related to working capital that a company can adopt after focusing on

variability regarding the cash inflows and outflows as well as a level of risk (Wu, & Dunn,

1995).

Hedging Policy:

Under this policy, a company can finance its working capital requirement. It is also known as a

matching policy. This policy is effective to match the current assets with current liabilities of a

business. According to this policy, long-terms sources is applied for financing the current as well

as fixed assets. And, short term sources can be used for financing the changeable assets. It could

be associated to volume and proposition of goods. For illustration, bank loan would be

compensated after 6 month then it would ensure that adequate cash will be obtained for repaying

mortgage related to maturity period (Bernanke, & Reinhart, 2004). It does not matter company

Venegas, B. B., & Ventura, J. A. (2018). A two-stage supply chain coordination mechanism

considering price-sensitive demand and quantity discounts. European Journal of

Operational Research, 264(2), 524-533.

Yao, Y., &Xu, Y. (2018).Dynamic decision making in mass customization. Computers &

Industrial Engineering, 120, 129-136.

Zaharia, V., &Bordeianu, D. (2018). COST STRATEGIES IN MANUFACTURING

COMPANIES. Proceedings in Manufacturing Systems, 13(4), 157.

Discuss the various policy options available for working capital management in the short

versus long term.

Working capital policy deals to sources as well as the working capital amount that a corporation

can maintain. A company cannot only face issues regarding the number of existing assetsbut also

regarding the proportion related to long-term sources in order to finances the existing assets.

There are different policies related to working capital that a company can adopt after focusing on

variability regarding the cash inflows and outflows as well as a level of risk (Wu, & Dunn,

1995).

Hedging Policy:

Under this policy, a company can finance its working capital requirement. It is also known as a

matching policy. This policy is effective to match the current assets with current liabilities of a

business. According to this policy, long-terms sources is applied for financing the current as well

as fixed assets. And, short term sources can be used for financing the changeable assets. It could

be associated to volume and proposition of goods. For illustration, bank loan would be

compensated after 6 month then it would ensure that adequate cash will be obtained for repaying

mortgage related to maturity period (Bernanke, & Reinhart, 2004). It does not matter company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 10

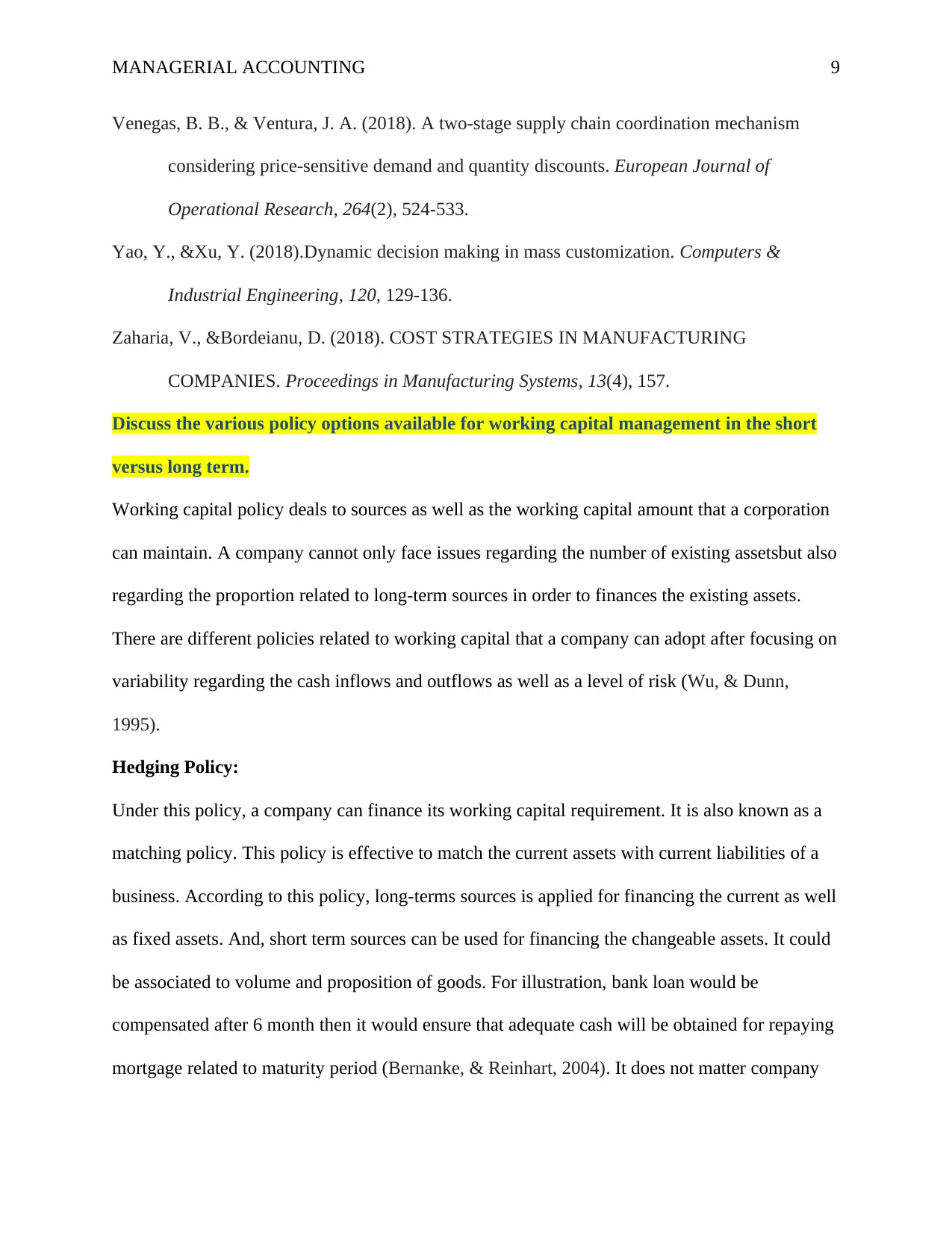

have adequate cash or not. In the case of company that has higher growth, TFC and FCA can

increase on time to time. However, the amount of varying existing assets may change with the

transformation in the construction level (Hallegatte, 2009).

The above chart shows that upward slopped represent the Line A and B.According to hedging

principle,company can obtain growth time to time.For this, long-term sources such as equity as

well as long-term debt could be used for financing. Along with this, varying the existing assets

are demonstrated by curved line C and it could be financed by short-term sources (Juan García-

Teruel, & Martinez-Solano, 2007).

In Hedging strategy, each assetof balance sheet in side of assetscan be compensated by financing

instrument related to same estimated maturity. It is beneficial for financing the working capital

needs of company.Along with this, just in time inventory management tool could be

implemented to decline the carrying cost by decline the time of inventory stock. In order to

shorten the receivable period without declining the credit period, sales discount can be provided

by company for quickcompensation (Michaelas, Chittenden, &Poutziouris, 1999).

It is detailed strategy related to financing the working capital related to moderate profitability as

well as risk. In such strategy, each of the resources can be financed through debt instruments

regarding almost the same maturity. It indicates when the asset is maturing after 30 days and the

payment of debt for this asset is financed, then due date of payment will be after almost 30 days.

Along with this, hedging strategy focuses on cardinal principle regarding financing such as

have adequate cash or not. In the case of company that has higher growth, TFC and FCA can

increase on time to time. However, the amount of varying existing assets may change with the

transformation in the construction level (Hallegatte, 2009).

The above chart shows that upward slopped represent the Line A and B.According to hedging

principle,company can obtain growth time to time.For this, long-term sources such as equity as

well as long-term debt could be used for financing. Along with this, varying the existing assets

are demonstrated by curved line C and it could be financed by short-term sources (Juan García-

Teruel, & Martinez-Solano, 2007).

In Hedging strategy, each assetof balance sheet in side of assetscan be compensated by financing

instrument related to same estimated maturity. It is beneficial for financing the working capital

needs of company.Along with this, just in time inventory management tool could be

implemented to decline the carrying cost by decline the time of inventory stock. In order to

shorten the receivable period without declining the credit period, sales discount can be provided

by company for quickcompensation (Michaelas, Chittenden, &Poutziouris, 1999).

It is detailed strategy related to financing the working capital related to moderate profitability as

well as risk. In such strategy, each of the resources can be financed through debt instruments

regarding almost the same maturity. It indicates when the asset is maturing after 30 days and the

payment of debt for this asset is financed, then due date of payment will be after almost 30 days.

Along with this, hedging strategy focuses on cardinal principle regarding financing such as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 11

practicing the long-term sources to finance the long-term assets, fixed assets and part of

permanent working capital as well as temporary working capital can be financed through short-

term sources for finance (Juan García-Teruel, & Martinez-Solano, 2007).

Financing Strategy:

Short-term funds = Total temporary current assets

Long-term funds = (Fixed assets) FA + Total permanent CA (current assets) (Abuzayed, 2012).

Conservative Policy:

This policy is used to eliminate risk entailed in the financing of CA (current assets). There is

associatively high proportion related to long-term sources that could be implemented for

financing the existing resources. The companyis not only matching the CA (current assets) but

also, some excess amount can create uncertainty (Shapiro, 2008).

This policy is related to minimize risk as but unable to make sure the effective use of funds.

Therefore, it can decline the potential returns related to shareholders.

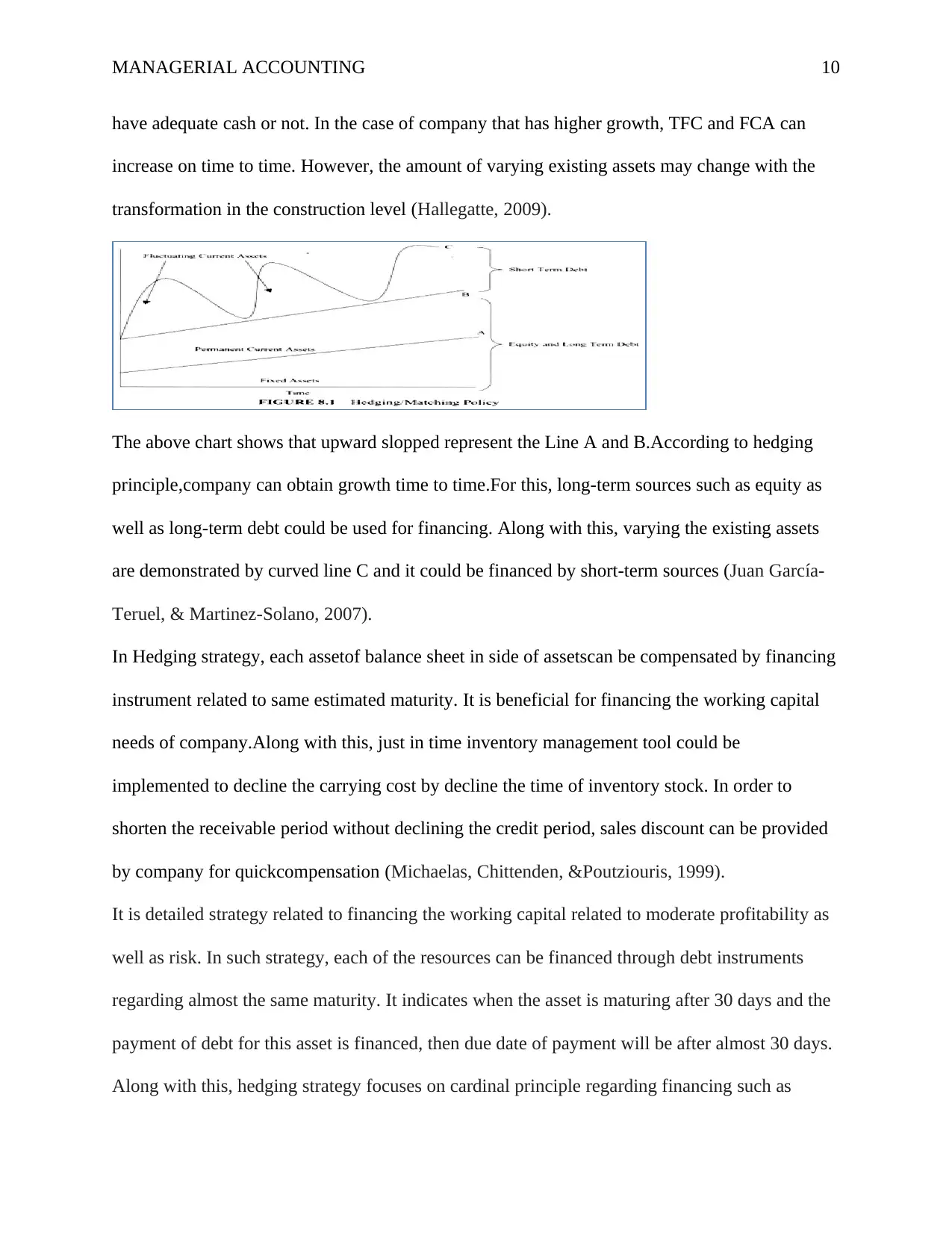

In the above chart, fixed assets are demonstrated by line A and fixed working capital is shown by

line B. For this, long-term sources could be used for financing. There isa different portion of

varying current assets that are demonstrated through Line C and it is financed by long-term

practicing the long-term sources to finance the long-term assets, fixed assets and part of

permanent working capital as well as temporary working capital can be financed through short-

term sources for finance (Juan García-Teruel, & Martinez-Solano, 2007).

Financing Strategy:

Short-term funds = Total temporary current assets

Long-term funds = (Fixed assets) FA + Total permanent CA (current assets) (Abuzayed, 2012).

Conservative Policy:

This policy is used to eliminate risk entailed in the financing of CA (current assets). There is

associatively high proportion related to long-term sources that could be implemented for

financing the existing resources. The companyis not only matching the CA (current assets) but

also, some excess amount can create uncertainty (Shapiro, 2008).

This policy is related to minimize risk as but unable to make sure the effective use of funds.

Therefore, it can decline the potential returns related to shareholders.

In the above chart, fixed assets are demonstrated by line A and fixed working capital is shown by

line B. For this, long-term sources could be used for financing. There isa different portion of

varying current assets that are demonstrated through Line C and it is financed by long-term

MANAGERIAL ACCOUNTING 12

sources. In such a policy, certain elements related to fluctuating existing assets are funded by

short-term sources (Healy, &Wahlen, 1999).

The conservative policy defines that company should not take risk associated with WCM as well

as, current assets as it may affect its sales. Excessive CA can make competent for corporation in

order to identify the sudden transformation in procurement time, sales and production plan

without considering the production plan. It is need for keeping the high extent regarding working

capital as well as long-terms sources could be used for finances like share capital with long-term

debts.

In addition to this, availability of adequate working capital will make competent to smooth

operational practices ofcompany as well as there would be no industrial action related to

production for want of raw materials as well as consumables goods. An adequate inventory of

finished goods could be kept in order to attain the fluctuations. Moreover, higher level of

liquidity may decline vagueness of liquidation (Tietenberg, & Lewis, 2016).

However, lower risk can translate into the lower return. In addition, larger investments in (CA)

current assets may lead to higher interest with carrying expenses as well as encouragement for

inefficiency. However, the conservation policy will make competent tothe company to absorb the

day to day business risk as well as assured continues operation flow (Wu, & Dunn, 1995).

Under this policy, working capital requirement can be met by using long term financing.

Marketable securities can be considered in the surplus liquidity and it could be traded in market

by considering the requirement for WC (Bernanke, & Reinhart, 2004).

Financing Strategy

Short-term funds = Part of temporary current assets

sources. In such a policy, certain elements related to fluctuating existing assets are funded by

short-term sources (Healy, &Wahlen, 1999).

The conservative policy defines that company should not take risk associated with WCM as well

as, current assets as it may affect its sales. Excessive CA can make competent for corporation in

order to identify the sudden transformation in procurement time, sales and production plan

without considering the production plan. It is need for keeping the high extent regarding working

capital as well as long-terms sources could be used for finances like share capital with long-term

debts.

In addition to this, availability of adequate working capital will make competent to smooth

operational practices ofcompany as well as there would be no industrial action related to

production for want of raw materials as well as consumables goods. An adequate inventory of

finished goods could be kept in order to attain the fluctuations. Moreover, higher level of

liquidity may decline vagueness of liquidation (Tietenberg, & Lewis, 2016).

However, lower risk can translate into the lower return. In addition, larger investments in (CA)

current assets may lead to higher interest with carrying expenses as well as encouragement for

inefficiency. However, the conservation policy will make competent tothe company to absorb the

day to day business risk as well as assured continues operation flow (Wu, & Dunn, 1995).

Under this policy, working capital requirement can be met by using long term financing.

Marketable securities can be considered in the surplus liquidity and it could be traded in market

by considering the requirement for WC (Bernanke, & Reinhart, 2004).

Financing Strategy

Short-term funds = Part of temporary current assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.