An Analysis of CVP and Standard Costing in Hospitality and Healthcare

VerifiedAdded on 2019/12/03

|10

|2176

|421

Report

AI Summary

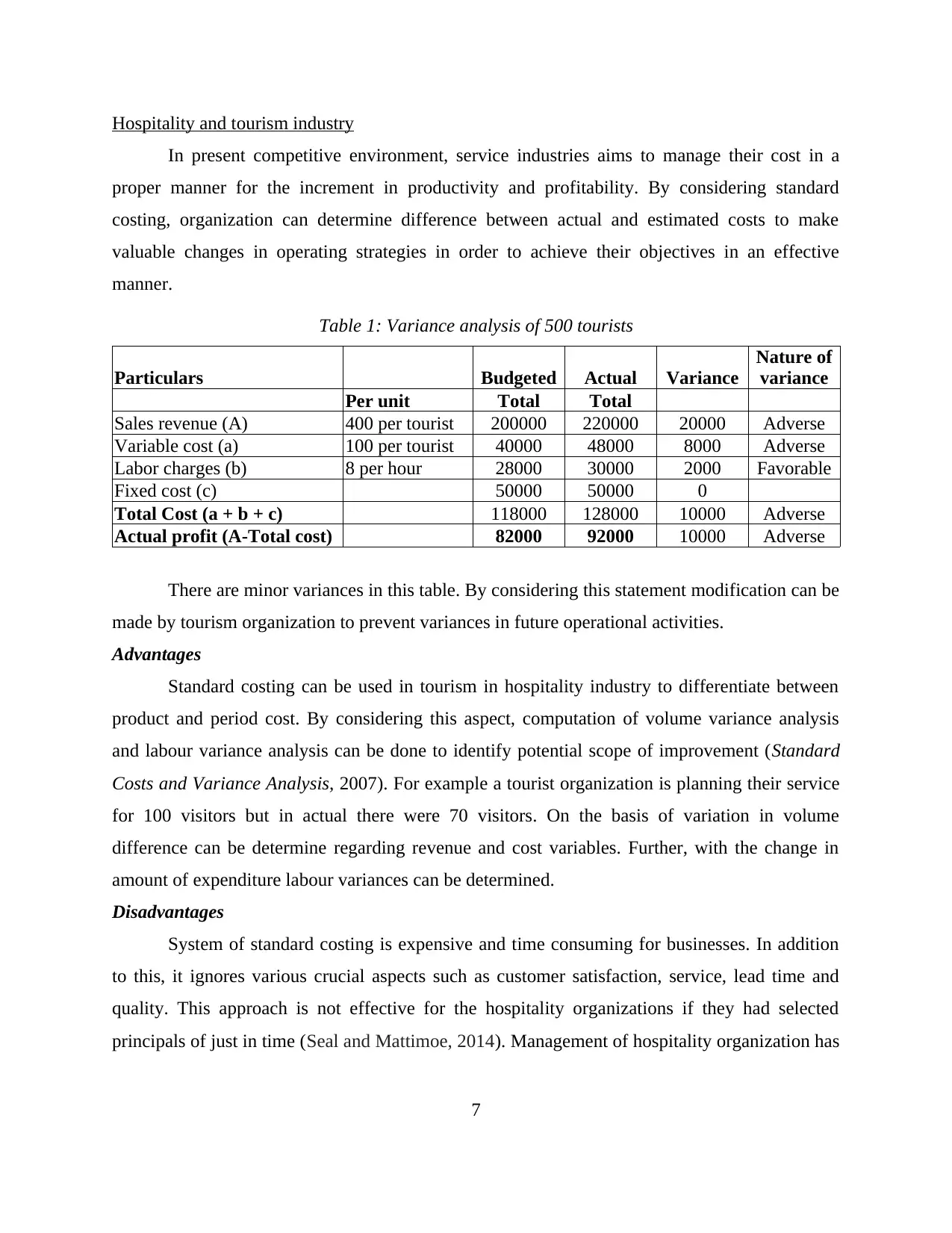

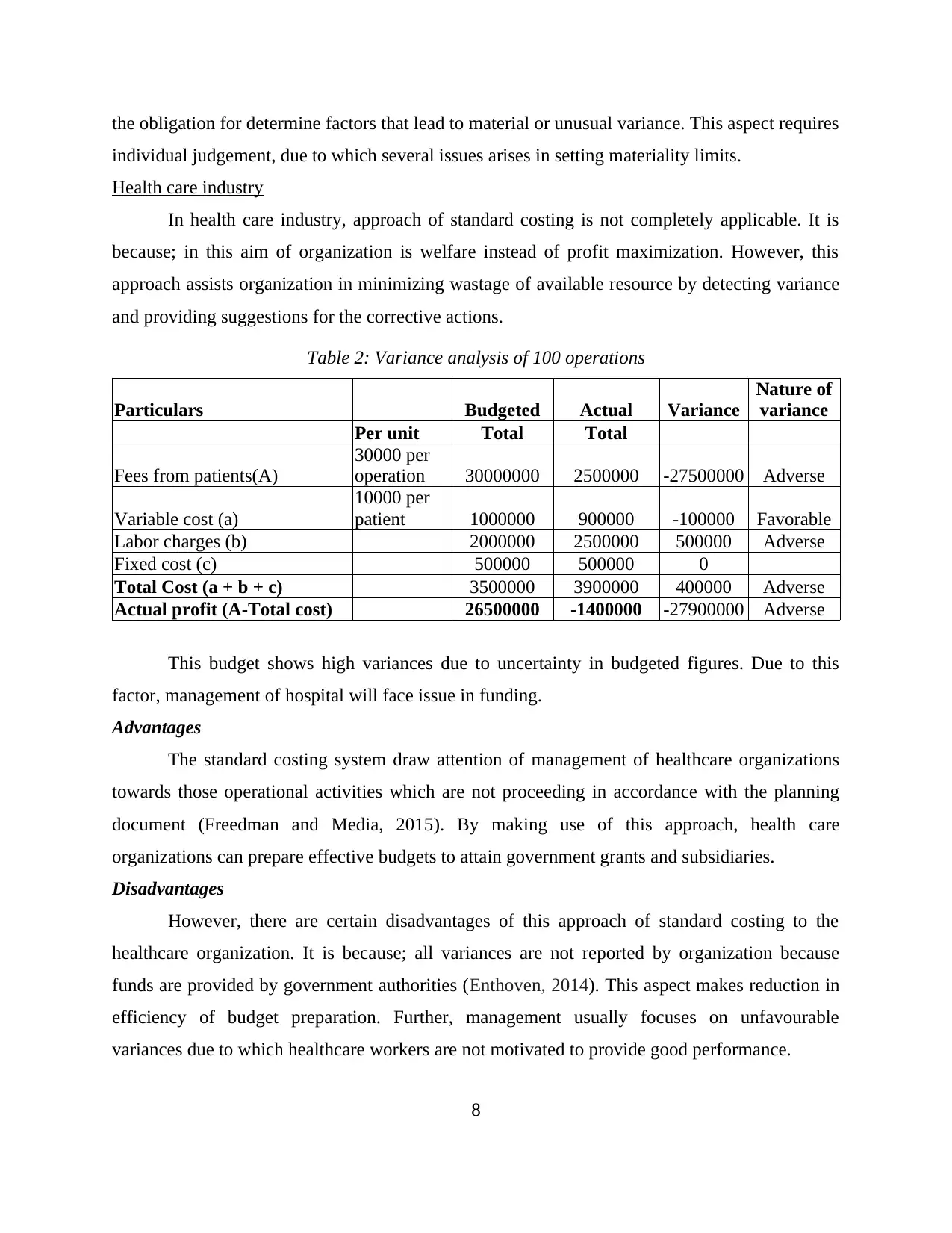

This report provides an in-depth analysis of Cost Volume Profit (CVP) analysis and standard costing, examining their application, advantages, and disadvantages within the hospitality and healthcare industries. The report begins with an introduction to both CVP analysis, which focuses on the impact of product costs and sales volume on profit, and standard costing, which substitutes expected expenditures with actual expenditures. The study then delves into the application of these techniques in the hospitality and tourism industry, illustrating how CVP analysis helps in determining break-even points and setting pricing strategies, while standard costing aids in variance analysis. The report also explores the application of these techniques in the healthcare industry, discussing how CVP analysis helps in determining fees and production capacity, and how standard costing assists in minimizing resource wastage through variance detection. The report includes examples, tables for variance analysis, and concludes by summarizing the suitability and limitations of these accounting techniques in the modern business era, highlighting their role in managerial decision-making and performance improvement.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.