CYBG PLC Audit Issues Report: ACCT20075, Term 1, CQUniversity

VerifiedAdded on 2023/03/17

|19

|3694

|82

Report

AI Summary

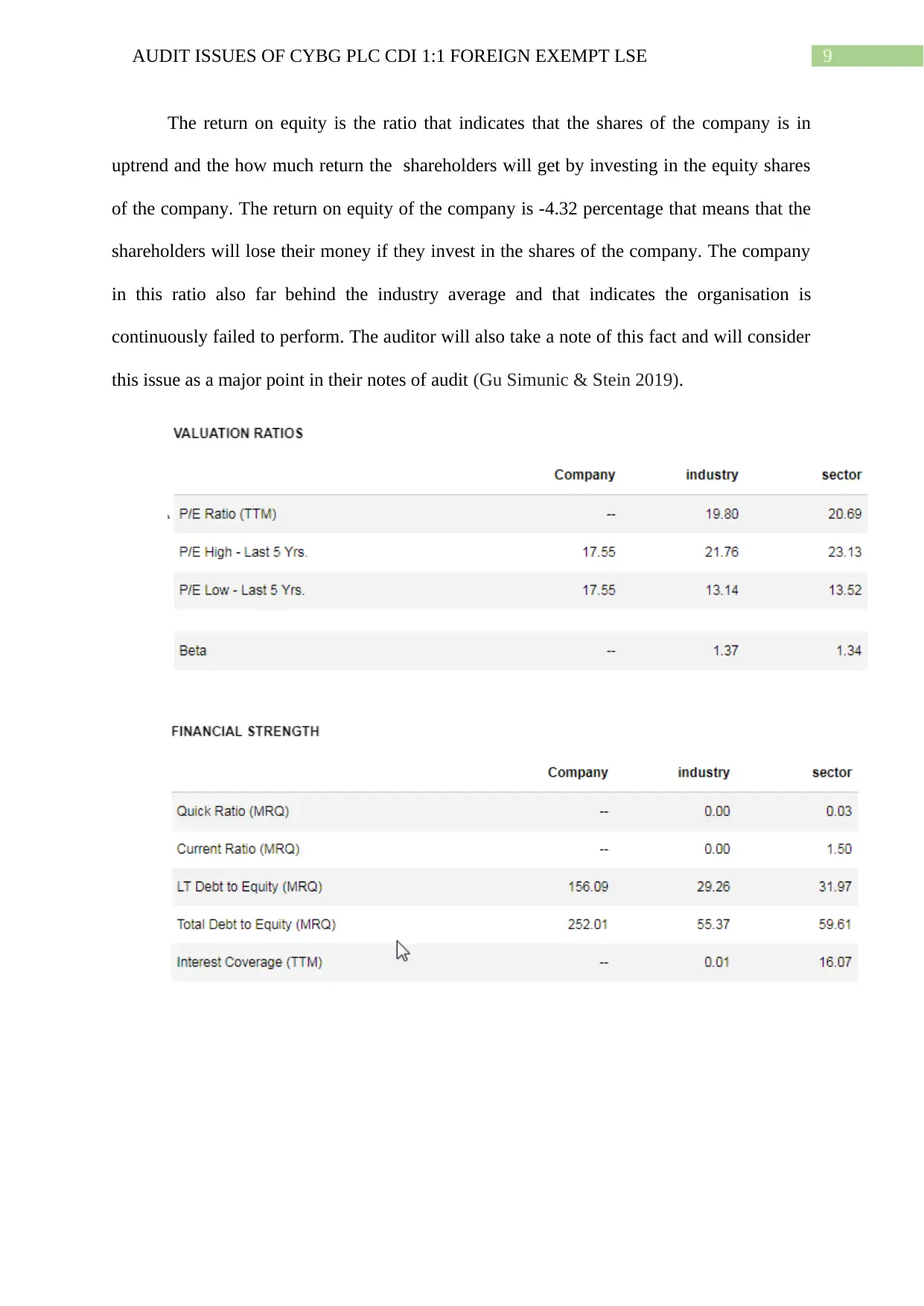

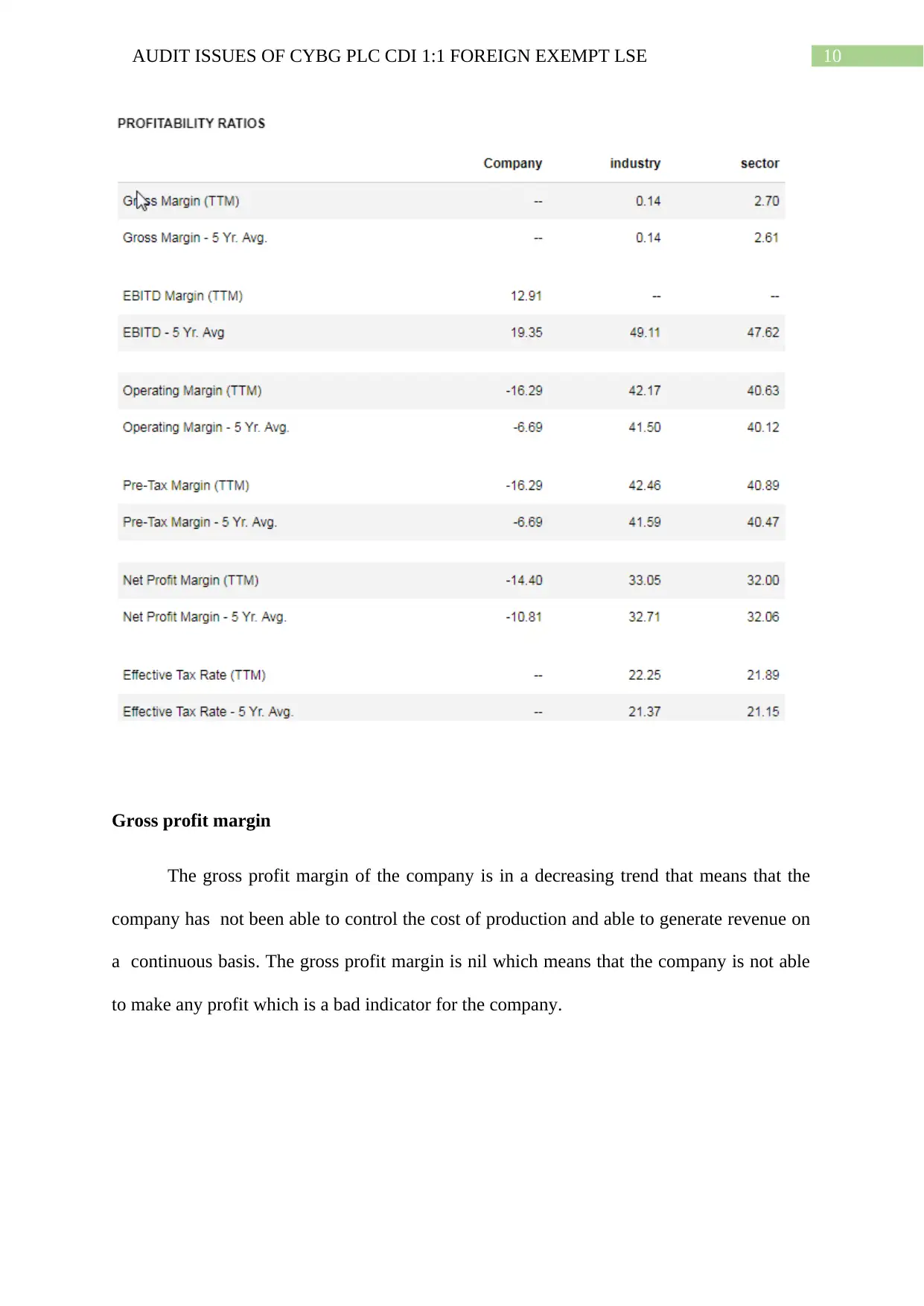

This report provides a comprehensive analysis of the audit issues pertaining to CYBG PLC CDI 1:1 Foreign Exempt LSE. The report begins by examining the concept of materiality in financial reporting, discussing its significance from the auditor's perspective, and outlining the steps involved in determining materiality levels, including setting benchmarks, determining the level of the benchmark, and justifying the choice. The report then delves into the application of materiality in identifying misstatements and differentiating between group and component materiality. The second section of the report assesses CYBG PLC's financial performance through various ratios, including receivable turnover, asset turnover, return on assets, return on investment, return on equity, gross profit margin, EBITD margin, operating margin, and net profit margin. The analysis reveals concerning trends, such as decreasing profitability and poor performance compared to industry standards. The final section of the report concludes the analysis by highlighting key risk areas for the audit, particularly the company's failure to meet industry standards across multiple financial ratios, and the potential implications of poor management. The report is based on the assignment brief to provide an academic report which addresses the tasks in the context of the allocated ASX listed company.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.