Accounting Theory and Contemporary Issues: Dali Food Group Analysis

VerifiedAdded on 2021/06/17

|13

|3069

|33

Report

AI Summary

This report delves into the accounting issues presented in the Dali Food Group's annual report, specifically highlighting problems related to disclosure, misrepresentation, and tax inconsistencies. The analysis focuses on the company's non-compliance with IFRS standards, particularly IAS 1, and the implications for its financial reporting. The report identifies the disclosure theory as a key framework, emphasizing the importance of transparent and accurate financial information. It examines specific issues such as discrepancies in revenue and cost of sales, changes in asset and liability values, and inconsistencies in finance costs and tax payments. The report suggests incorporating IFRS standards like IAS 16, 38, 9, 19, 21, and 39 to improve the accuracy and transparency of the annual report. The study underscores the significance of ethical financial reporting and the impact of non-disclosure on stakeholders, advocating for enhanced disclosure practices to build investor trust and ensure accurate financial representation.

Running head: ACCOUNTING THEORY & CONTEMPORARY ISSUES

Accounting Theory & Contemporary Issues

Name of the Student:

Name of the University:

Authors Note:

Accounting Theory & Contemporary Issues

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY & CONTEMPORARY ISSUES

1

Table of Contents

Assignment 1:.............................................................................................................................2

Hong Kong Exchange (Dali Food Group):................................................................................2

Introduction:...............................................................................................................................2

Analysis:.....................................................................................................................................3

Detailing the accounting problems:...........................................................................................3

Discussing the accounting requirements:...................................................................................4

Discussing the theory and the identified accounting problems:.................................................5

Discussing the main theme of the theory:..................................................................................8

Changes and suggestions that can be incorporated in the annual report:...................................8

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................11

1

Table of Contents

Assignment 1:.............................................................................................................................2

Hong Kong Exchange (Dali Food Group):................................................................................2

Introduction:...............................................................................................................................2

Analysis:.....................................................................................................................................3

Detailing the accounting problems:...........................................................................................3

Discussing the accounting requirements:...................................................................................4

Discussing the theory and the identified accounting problems:.................................................5

Discussing the main theme of the theory:..................................................................................8

Changes and suggestions that can be incorporated in the annual report:...................................8

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................11

ACCOUNTING THEORY & CONTEMPORARY ISSUES

2

Assignment 1:

Hong Kong Exchange (Dali Food Group):

Introduction:

The discussion is mainly based on the accounting issue, which is faced by Dali Food

Group and is depicted in their annual report. The article published in Reuters about Dali Food

Group portrayed the misdoing or misrepresentation of data, which has been conducted by the

organisation. The news directly indicated the problems regarding its books, as the company

has implausible low expenses and salary cost, while the tax filings also display inconsistency,

which escalates the chance of a fraud conducted by the organisation.

The company has been operating within the circular premises of China, while it deals

with snack food and beverage products. The company has been strengthening its position in

retail sector, as it deals with snacks and beverages. The company acquired a total revenue of

23 Billion HKD in 2017, while its net profit stood at 4 Billion HKD, which indicated an

inclination on the growth prospects of the organisation.

However, there are certain accounting issues, which has been detected in Dali Food

Group, such as non-disclosure, mis-representation, and Tax issues. The above identified

accounting issues directly affect the financial reporting structure of the organisation, which

will have a negative impact on its shareholders. The organisation has violated the disclosure

clause that has been set up by IFRS for preventing any kind of mishap or unethical activities

that has been conducted within an organisation. On the whole, the organisation prepares the

annual report in accordance with the Hong Kong Financial Reporting Standards. This directly

2

Assignment 1:

Hong Kong Exchange (Dali Food Group):

Introduction:

The discussion is mainly based on the accounting issue, which is faced by Dali Food

Group and is depicted in their annual report. The article published in Reuters about Dali Food

Group portrayed the misdoing or misrepresentation of data, which has been conducted by the

organisation. The news directly indicated the problems regarding its books, as the company

has implausible low expenses and salary cost, while the tax filings also display inconsistency,

which escalates the chance of a fraud conducted by the organisation.

The company has been operating within the circular premises of China, while it deals

with snack food and beverage products. The company has been strengthening its position in

retail sector, as it deals with snacks and beverages. The company acquired a total revenue of

23 Billion HKD in 2017, while its net profit stood at 4 Billion HKD, which indicated an

inclination on the growth prospects of the organisation.

However, there are certain accounting issues, which has been detected in Dali Food

Group, such as non-disclosure, mis-representation, and Tax issues. The above identified

accounting issues directly affect the financial reporting structure of the organisation, which

will have a negative impact on its shareholders. The organisation has violated the disclosure

clause that has been set up by IFRS for preventing any kind of mishap or unethical activities

that has been conducted within an organisation. On the whole, the organisation prepares the

annual report in accordance with the Hong Kong Financial Reporting Standards. This directly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY & CONTEMPORARY ISSUES

3

violates the measures that needs to be taken by the organisation while preparing the annual

report as per the financial conceptual framework.

The adequate disclosure theory is relatively identified for the organisation, as it does

not put all the relevant information in their annual report as per the IFRS.

Analysis:

Detailing the accounting problems:

The adoption of IFRS by the Chinese regulatory authorities has a relatively allowed

organisations to prepare an annual report as per the accounting standard. however, some of

the organisation still does not embed their annual report as per the complex nature of IFRS,

which increases the uncertainty in their operations. The major accounting problem that could

be identified from the annual report of Dali Food Group is the ignorance of IFRS rules in

preparing the financial statement. The organisation does not follow the first standard rule of

IAS 1, which depicts about the presentation of the financial statements. The organisation does

not follow the ruling depicted by IFRS in preparing their annual report, which directly affects

their disclosure measure and indicates the miss representation of their financial statement.

On the other hand, the organisation directly follows the Hong Kong financial

reporting statement for preparing the annual report. However, Schaltegger and Burritt (2017)

indicated that organisations use the IFRS measure for reducing the level of uncertainty in

their annual report and gain trust of their International investors. On the contrary, Hoque

(2018) mentioned that companies that are not using IFRS financial statement does not attract

International investors, as they are not aware of the regional accounting standards and their

exceptions.

3

violates the measures that needs to be taken by the organisation while preparing the annual

report as per the financial conceptual framework.

The adequate disclosure theory is relatively identified for the organisation, as it does

not put all the relevant information in their annual report as per the IFRS.

Analysis:

Detailing the accounting problems:

The adoption of IFRS by the Chinese regulatory authorities has a relatively allowed

organisations to prepare an annual report as per the accounting standard. however, some of

the organisation still does not embed their annual report as per the complex nature of IFRS,

which increases the uncertainty in their operations. The major accounting problem that could

be identified from the annual report of Dali Food Group is the ignorance of IFRS rules in

preparing the financial statement. The organisation does not follow the first standard rule of

IAS 1, which depicts about the presentation of the financial statements. The organisation does

not follow the ruling depicted by IFRS in preparing their annual report, which directly affects

their disclosure measure and indicates the miss representation of their financial statement.

On the other hand, the organisation directly follows the Hong Kong financial

reporting statement for preparing the annual report. However, Schaltegger and Burritt (2017)

indicated that organisations use the IFRS measure for reducing the level of uncertainty in

their annual report and gain trust of their International investors. On the contrary, Hoque

(2018) mentioned that companies that are not using IFRS financial statement does not attract

International investors, as they are not aware of the regional accounting standards and their

exceptions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY & CONTEMPORARY ISSUES

4

Discussing the accounting requirements:

Dali Food Group mainly need to follow the IFRS Standards for preparing the annual

report, which was previously not followed by the management. The basic requirements of the

financial report preparation are the maintenance of IAS 1 ruling, which requires that the

organisation represents the financial statement as per the standard. This preparation relatively

helps in depicting the financial transactions of the organisation in more organized and ethical

manner. The use of valuation standard such as IFRS 9 also needs to be maintained by the

organisation while preparing the annual report (Iasplus.com 2018). This would eventually

help in depicting the actual valuation of the Assets and liabilities in accordance with the

market value. This ethical presentation would eventually help in identifying the level of

actual financial performance of the organisation.

The other standards such as IAS 16 and IAS 38 are mainly used for the valuation

process of their plant, machinery and intangible assets. This valuation directly helps in

detecting the overall total Assets of the organisation, as of the current fiscal year. The

measures taken by IFRS directly helps in detecting the actual financial performance of the

organisation during the fiscal year by identifying the growth in its assets and revenues.

Different standards such as IAS 19, IAS 21 and IAS 39 are also essential while preparing the

annual report of an organisation (Iasplus.com 2018). Therefore, Dali food group needs to

follow all the above accounting standards while preparing the annual report, which will

increase their authenticity in the eyes of the international investors. The above accounting

requirements needs to be met by the organisation for preparing the annual report as per the

International Financial Regulation Standard.

4

Discussing the accounting requirements:

Dali Food Group mainly need to follow the IFRS Standards for preparing the annual

report, which was previously not followed by the management. The basic requirements of the

financial report preparation are the maintenance of IAS 1 ruling, which requires that the

organisation represents the financial statement as per the standard. This preparation relatively

helps in depicting the financial transactions of the organisation in more organized and ethical

manner. The use of valuation standard such as IFRS 9 also needs to be maintained by the

organisation while preparing the annual report (Iasplus.com 2018). This would eventually

help in depicting the actual valuation of the Assets and liabilities in accordance with the

market value. This ethical presentation would eventually help in identifying the level of

actual financial performance of the organisation.

The other standards such as IAS 16 and IAS 38 are mainly used for the valuation

process of their plant, machinery and intangible assets. This valuation directly helps in

detecting the overall total Assets of the organisation, as of the current fiscal year. The

measures taken by IFRS directly helps in detecting the actual financial performance of the

organisation during the fiscal year by identifying the growth in its assets and revenues.

Different standards such as IAS 19, IAS 21 and IAS 39 are also essential while preparing the

annual report of an organisation (Iasplus.com 2018). Therefore, Dali food group needs to

follow all the above accounting standards while preparing the annual report, which will

increase their authenticity in the eyes of the international investors. The above accounting

requirements needs to be met by the organisation for preparing the annual report as per the

International Financial Regulation Standard.

ACCOUNTING THEORY & CONTEMPORARY ISSUES

5

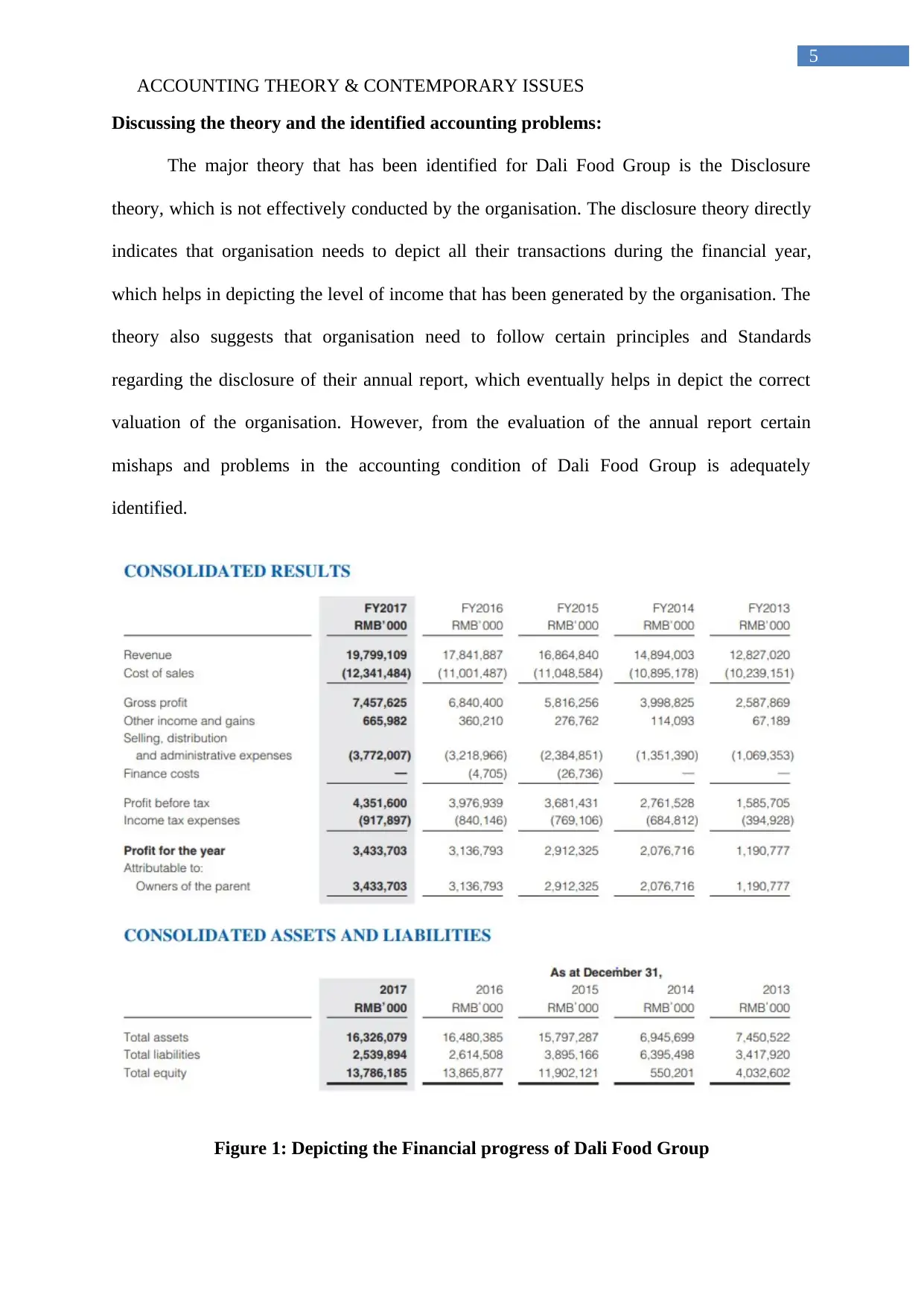

Discussing the theory and the identified accounting problems:

The major theory that has been identified for Dali Food Group is the Disclosure

theory, which is not effectively conducted by the organisation. The disclosure theory directly

indicates that organisation needs to depict all their transactions during the financial year,

which helps in depicting the level of income that has been generated by the organisation. The

theory also suggests that organisation need to follow certain principles and Standards

regarding the disclosure of their annual report, which eventually helps in depict the correct

valuation of the organisation. However, from the evaluation of the annual report certain

mishaps and problems in the accounting condition of Dali Food Group is adequately

identified.

Figure 1: Depicting the Financial progress of Dali Food Group

5

Discussing the theory and the identified accounting problems:

The major theory that has been identified for Dali Food Group is the Disclosure

theory, which is not effectively conducted by the organisation. The disclosure theory directly

indicates that organisation needs to depict all their transactions during the financial year,

which helps in depicting the level of income that has been generated by the organisation. The

theory also suggests that organisation need to follow certain principles and Standards

regarding the disclosure of their annual report, which eventually helps in depict the correct

valuation of the organisation. However, from the evaluation of the annual report certain

mishaps and problems in the accounting condition of Dali Food Group is adequately

identified.

Figure 1: Depicting the Financial progress of Dali Food Group

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY & CONTEMPORARY ISSUES

6

(Source: Dali-group.com 2018)

The above figure directly depicts the configuration results, Assets and liabilities of

Dali Food Group from 2013 to 2017. The depiction of the current financial performance of

the organisation is actually in question, as it could be seen that revenues of the organisation

has improved drastically over the period of 5 years, but the cost of sales stagnated during the

time. This relatively indicates that the overall expenses that was being conducted by the

organisation to support their field has drastically declined. This kind of decline in retail sector

is a relatively low, as organisation needs to maintain high level of expenses to support their

rising demand. Therefore, it could be identified, that a relevant misrepresentation of the

current cost of sales of the organisation is being conducted by the management (Dali-

group.com 2018).

The other alternative behaviour of Dali Food Group annual report is the Change in the

Asset, liabilities and equity section of the organisation. From the fiscal year of 2015 the

drastic change in assets, liabilities and equity of Dali Food Group Can we see in the above

figure. This drastic change in the overall financial condition of the organisation resulted in

the increment in Assets and equity by declining the total liabilities of the company. The main

problem that could be identified from the annual report is the inclusion of Finance cost,

which depicted the use of debt supporting its operations. However, the changes in the value

of Finance cost drastically declined in fiscal 2016 and was nil during the fiscal year of 2017.

Moreover, changes in the values of total Assets and total liabilities of the organisation has

been drastic, which raises the alarm of the accounting issues that might be followed by the

organisation during the past couple years. Furthermore, the changes in cash payment and the

actual finance cost of the organisation for the fiscal year of 2016 is different. The

organization during the fiscal year of 2016 has paid RMB 4,705,000 as finance costs, which

is depicted in the income statement (Dali-group.com 2018). On the other hand, the cash

6

(Source: Dali-group.com 2018)

The above figure directly depicts the configuration results, Assets and liabilities of

Dali Food Group from 2013 to 2017. The depiction of the current financial performance of

the organisation is actually in question, as it could be seen that revenues of the organisation

has improved drastically over the period of 5 years, but the cost of sales stagnated during the

time. This relatively indicates that the overall expenses that was being conducted by the

organisation to support their field has drastically declined. This kind of decline in retail sector

is a relatively low, as organisation needs to maintain high level of expenses to support their

rising demand. Therefore, it could be identified, that a relevant misrepresentation of the

current cost of sales of the organisation is being conducted by the management (Dali-

group.com 2018).

The other alternative behaviour of Dali Food Group annual report is the Change in the

Asset, liabilities and equity section of the organisation. From the fiscal year of 2015 the

drastic change in assets, liabilities and equity of Dali Food Group Can we see in the above

figure. This drastic change in the overall financial condition of the organisation resulted in

the increment in Assets and equity by declining the total liabilities of the company. The main

problem that could be identified from the annual report is the inclusion of Finance cost,

which depicted the use of debt supporting its operations. However, the changes in the value

of Finance cost drastically declined in fiscal 2016 and was nil during the fiscal year of 2017.

Moreover, changes in the values of total Assets and total liabilities of the organisation has

been drastic, which raises the alarm of the accounting issues that might be followed by the

organisation during the past couple years. Furthermore, the changes in cash payment and the

actual finance cost of the organisation for the fiscal year of 2016 is different. The

organization during the fiscal year of 2016 has paid RMB 4,705,000 as finance costs, which

is depicted in the income statement (Dali-group.com 2018). On the other hand, the cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY & CONTEMPORARY ISSUES

7

statement indicates that the overall interest paid by the organisation amounts to RMB

6,706,000. The changes in the values of interest payments is directly indicating and

accounting issue, which is being conducted by the organisation while preparing the annual

report. The use of IFRS standard would eventually help in reducing the occurrence of Shady

transactions and improve authenticity of the annual report.

Further elaboration can also be conducted on the income tax payment that the

organisation conducts during its fiscal year. from the evaluation off the annual report

difference in the income tax expense and Income Tax paid amount can be seen, which is

depicted in the income statement and cash flow statement. The difference in the values is a

relatively depicting the problems or issues that is currently present in their accounting system.

The article also indicated that the tax expense of the organisation is not adding up, which is

directly indicating the problems that is currently present within Dali Food Group (Dali-

group.com 2018).

The annual report of the organisation directly indicated the representation of different

accounts, which directly depicted the issues in their current accounting system. The drastic

changes in the Asset and liability value output depicted the current problems that might be

faced by the organisation. the exuberant increment in revenues, while the cost of good

remained same, which directly indicates the problems that is currently present within the

operations of Dali Food Group. The company directly belongs to Retail Industry, which

adequately increases the cost of sales due to the incremental revenue, while this type of

transaction is not seen in the operations of Dali Food Group. This mainly increases the

concern for foreign investors and raises the alarm for the current operation that has being

conducted by the organisation. The identification of the interest payment is also

Questionable, as the overall finance course declined immensely, while there is alteration

between actual finance cost depicted in the income statement and the interest paid depicted in

7

statement indicates that the overall interest paid by the organisation amounts to RMB

6,706,000. The changes in the values of interest payments is directly indicating and

accounting issue, which is being conducted by the organisation while preparing the annual

report. The use of IFRS standard would eventually help in reducing the occurrence of Shady

transactions and improve authenticity of the annual report.

Further elaboration can also be conducted on the income tax payment that the

organisation conducts during its fiscal year. from the evaluation off the annual report

difference in the income tax expense and Income Tax paid amount can be seen, which is

depicted in the income statement and cash flow statement. The difference in the values is a

relatively depicting the problems or issues that is currently present in their accounting system.

The article also indicated that the tax expense of the organisation is not adding up, which is

directly indicating the problems that is currently present within Dali Food Group (Dali-

group.com 2018).

The annual report of the organisation directly indicated the representation of different

accounts, which directly depicted the issues in their current accounting system. The drastic

changes in the Asset and liability value output depicted the current problems that might be

faced by the organisation. the exuberant increment in revenues, while the cost of good

remained same, which directly indicates the problems that is currently present within the

operations of Dali Food Group. The company directly belongs to Retail Industry, which

adequately increases the cost of sales due to the incremental revenue, while this type of

transaction is not seen in the operations of Dali Food Group. This mainly increases the

concern for foreign investors and raises the alarm for the current operation that has being

conducted by the organisation. The identification of the interest payment is also

Questionable, as the overall finance course declined immensely, while there is alteration

between actual finance cost depicted in the income statement and the interest paid depicted in

ACCOUNTING THEORY & CONTEMPORARY ISSUES

8

the annual report. The contrast between both the amount directly indicates the problem which

is currently present in the financial department of the organisation. Hence, changes in the

current accounting standard would eventually help the organization to depict the actual

transaction and financial position to the investor (Dali-group.com 2018).

Discussing the main theme of the theory:

The main theme of the theory is about disclosure, which needs to be conducted by the

organisations in their annual report. Disclosures are relatively depicted as the notes to the

financial transaction that has been conducted by the organisation during the fiscal year. The

disclosure would eventually help in identifying different level of transaction and that value,

which has been conducted by the company. Moreover, disclosures regarding all the relevant

transactions that is conducted by the company needs to be depicted in the annual report. The

disclosure transformation theory directly proposes that companies need to explain the process

of change in the mandatory and voluntary corporate disclosure practice. Hence, disclosure

theory relatively defines the activities in different sections such as mandatory and voluntary

disclosure which needs to be conducted by the organisation. Therefore, with adequate

disclosures organisations are able to depict their actual financial transactions and condition

during the fiscal year to their investors with the help of the financial report. In this context,

Beattie (2014) stated that with the incorporation of disclosure theories in the financial

conceptual framework, organisations are bound to provide all the relevant information in the

annual report, which reduces the possibility of unethical practices.

Changes and suggestions that can be incorporated in the annual report:

Dali Food Group can implement Different segments of the IAS standards for

preparing the annual report. the use of IAS 16 and 38 would eventually help in depicting the

actual valuation for their assets such as plant machinery and intangible assets. the description

8

the annual report. The contrast between both the amount directly indicates the problem which

is currently present in the financial department of the organisation. Hence, changes in the

current accounting standard would eventually help the organization to depict the actual

transaction and financial position to the investor (Dali-group.com 2018).

Discussing the main theme of the theory:

The main theme of the theory is about disclosure, which needs to be conducted by the

organisations in their annual report. Disclosures are relatively depicted as the notes to the

financial transaction that has been conducted by the organisation during the fiscal year. The

disclosure would eventually help in identifying different level of transaction and that value,

which has been conducted by the company. Moreover, disclosures regarding all the relevant

transactions that is conducted by the company needs to be depicted in the annual report. The

disclosure transformation theory directly proposes that companies need to explain the process

of change in the mandatory and voluntary corporate disclosure practice. Hence, disclosure

theory relatively defines the activities in different sections such as mandatory and voluntary

disclosure which needs to be conducted by the organisation. Therefore, with adequate

disclosures organisations are able to depict their actual financial transactions and condition

during the fiscal year to their investors with the help of the financial report. In this context,

Beattie (2014) stated that with the incorporation of disclosure theories in the financial

conceptual framework, organisations are bound to provide all the relevant information in the

annual report, which reduces the possibility of unethical practices.

Changes and suggestions that can be incorporated in the annual report:

Dali Food Group can implement Different segments of the IAS standards for

preparing the annual report. the use of IAS 16 and 38 would eventually help in depicting the

actual valuation for their assets such as plant machinery and intangible assets. the description

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY & CONTEMPORARY ISSUES

9

of the actual valuation would eventually help the organisation to put their actual financial

position in the fiscal year. after incorporating the evaluation system, the use of IAS 19, 21

and 39 could also be effective for the organisation, as a directly helps in putting the current

financial position of a company. The above standards would eventually increase reliability of

the financial report, which would eventually increase the trust of international investors. The

regulation such as IFRS 9 should also be maintained by Dali Food Group, as it increases

authenticity of their current valuation. IFRS 9 many uses the market valuation system for

identifying the actual value for the assets held by the organisation. This valuation system

eventually improves the current financial report of an organisation and depict their actual

value to the investors. Hence, it is advisable that the organisation change the current Hong

King financial Reporting system of IFRS system.

Conclusion:

From the overall evaluation of the above statement it could be identified that Dali

Food Group does not use IFRS accounting standards for preparing their annual report. This is

the main reason where discrepancy in the accounting system adopted by the organisation is

identified. The company has drastically improved over the five fiscal years, where the

revenues have increased events. On the other hand, the overall expenses of the company have

deteriorated of contracted, which is not possible for retail organisation, as the continuous

demand and inventory stock it would eventually increase the cost with sales. The discrepancy

in the accounting system is directly affecting the organisations ability to provide adequate

financial statement for its foreign investors. Therefore, the use of different accounting

policies and standards of IAS could eventually help in depicting the annual report as per the

requirements of IFRS. Hence, the improvement on the financial report would eventually

allow Dali Food Group to depict their current and actual financial position to with investors.

9

of the actual valuation would eventually help the organisation to put their actual financial

position in the fiscal year. after incorporating the evaluation system, the use of IAS 19, 21

and 39 could also be effective for the organisation, as a directly helps in putting the current

financial position of a company. The above standards would eventually increase reliability of

the financial report, which would eventually increase the trust of international investors. The

regulation such as IFRS 9 should also be maintained by Dali Food Group, as it increases

authenticity of their current valuation. IFRS 9 many uses the market valuation system for

identifying the actual value for the assets held by the organisation. This valuation system

eventually improves the current financial report of an organisation and depict their actual

value to the investors. Hence, it is advisable that the organisation change the current Hong

King financial Reporting system of IFRS system.

Conclusion:

From the overall evaluation of the above statement it could be identified that Dali

Food Group does not use IFRS accounting standards for preparing their annual report. This is

the main reason where discrepancy in the accounting system adopted by the organisation is

identified. The company has drastically improved over the five fiscal years, where the

revenues have increased events. On the other hand, the overall expenses of the company have

deteriorated of contracted, which is not possible for retail organisation, as the continuous

demand and inventory stock it would eventually increase the cost with sales. The discrepancy

in the accounting system is directly affecting the organisations ability to provide adequate

financial statement for its foreign investors. Therefore, the use of different accounting

policies and standards of IAS could eventually help in depicting the annual report as per the

requirements of IFRS. Hence, the improvement on the financial report would eventually

allow Dali Food Group to depict their current and actual financial position to with investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY & CONTEMPORARY ISSUES

10

Adequate suggestions have been conducted for the organisation, where it needs to comply

with the disclosure theory, which depicts that organisation need to portray all the relevant

information in the financial report.

10

Adequate suggestions have been conducted for the organisation, where it needs to comply

with the disclosure theory, which depicts that organisation need to portray all the relevant

information in the financial report.

ACCOUNTING THEORY & CONTEMPORARY ISSUES

11

References and Bibliography:

Baskerville, R., Carrera, N., Gomes, D., Lai, A. and Parker, L., 2017. Accounting historians

engaging with scholars inside and outside accounting: Issues, opportunities and

obstacles. Accounting History, 22(4), pp.403-424.

Beattie, V., 2014. Accounting narratives and the narrative turn in accounting research: Issues,

theory, methodology, methods and a research framework. The British Accounting

Review, 46(2), pp.111-134.

Bloomberg.com. (2018). 3799:Hong Kong Stock Quote - Dali Foods Group Co Ltd. [online]

Available at: https://www.bloomberg.com/quote/3799:HK [Accessed 24 Aug. 2018].

Camilleri, E. and Camilleri, R., 2017. Accounting for Financial Instruments: A Guide to

Valuation and Risk Management. Routledge.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Dali-group.com. (2018). Investor relations-Financial Information. [online] Available at:

http://www.dali-group.com/en/relations.php?cid=122 [Accessed 24 Aug. 2018].

DesJardins, J.R. and McCall, J.J., 2014. Contemporary issues in business ethics. Cengage

Learning.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

11

References and Bibliography:

Baskerville, R., Carrera, N., Gomes, D., Lai, A. and Parker, L., 2017. Accounting historians

engaging with scholars inside and outside accounting: Issues, opportunities and

obstacles. Accounting History, 22(4), pp.403-424.

Beattie, V., 2014. Accounting narratives and the narrative turn in accounting research: Issues,

theory, methodology, methods and a research framework. The British Accounting

Review, 46(2), pp.111-134.

Bloomberg.com. (2018). 3799:Hong Kong Stock Quote - Dali Foods Group Co Ltd. [online]

Available at: https://www.bloomberg.com/quote/3799:HK [Accessed 24 Aug. 2018].

Camilleri, E. and Camilleri, R., 2017. Accounting for Financial Instruments: A Guide to

Valuation and Risk Management. Routledge.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, pp.1-13.

Dali-group.com. (2018). Investor relations-Financial Information. [online] Available at:

http://www.dali-group.com/en/relations.php?cid=122 [Accessed 24 Aug. 2018].

DesJardins, J.R. and McCall, J.J., 2014. Contemporary issues in business ethics. Cengage

Learning.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.