Analyzing Daniel's Portfolio: Risk, Return, and Beta Calculations

VerifiedAdded on 2022/08/14

|4

|947

|12

Project

AI Summary

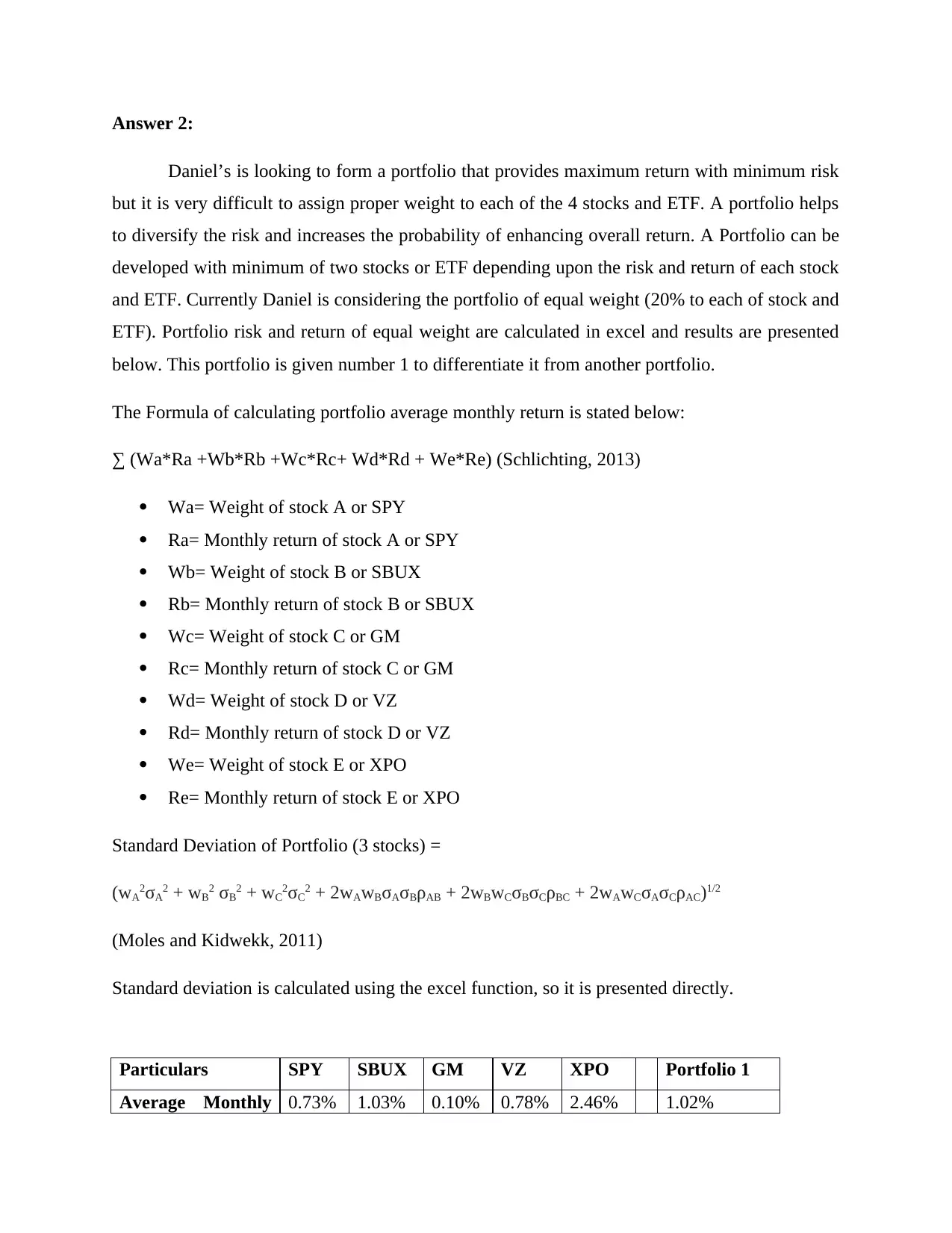

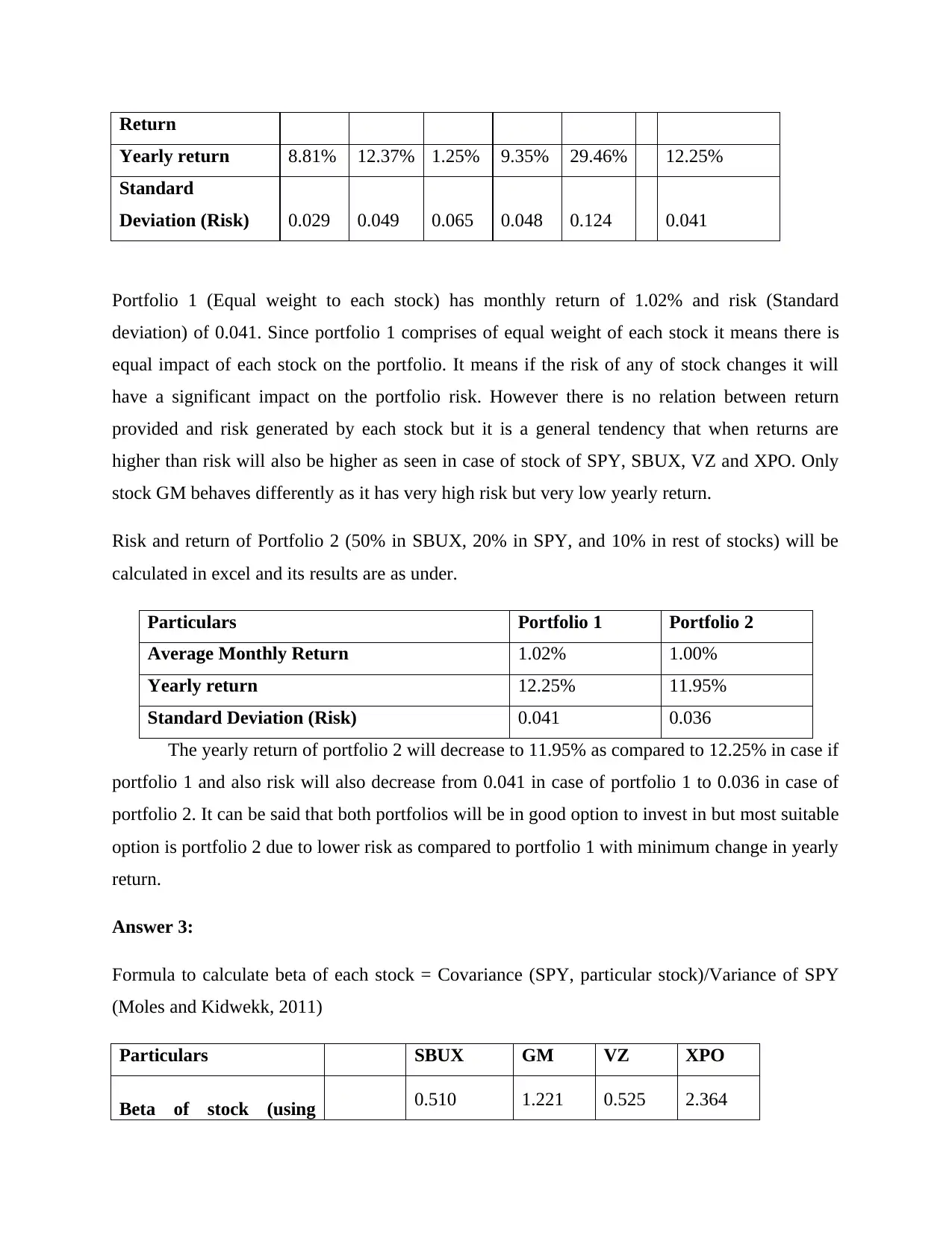

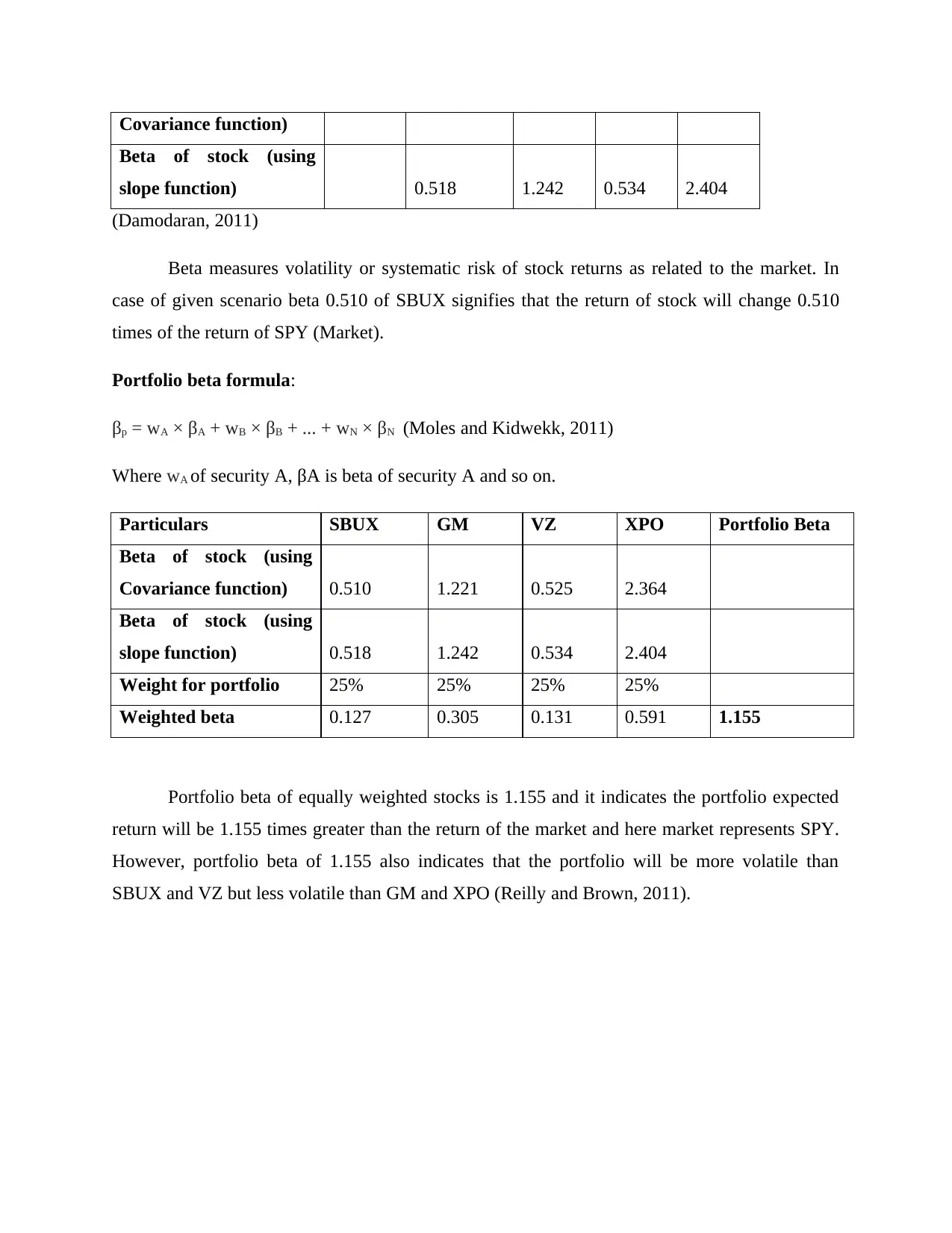

This project analyzes Daniel's portfolio, a case study involving a finance student's investments. The assignment calculates and compares the risk and return of two different portfolios, one with equal weight allocation and another with a modified allocation favoring Starbucks stock. It uses formulas to determine average monthly and yearly returns, as well as standard deviation (risk). The project further calculates the beta of individual stocks within the portfolio, using both covariance and slope functions, and determines the overall portfolio beta. The analysis aims to identify the portfolio with the optimal balance of risk and return, demonstrating key concepts in portfolio management, diversification, and the significance of beta in assessing stock volatility. The project also includes references to relevant financial literature.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.