Danone Operations: Costing Systems, CSR, and Sustainability

VerifiedAdded on 2023/06/11

|18

|3514

|487

Report

AI Summary

This report provides a comprehensive analysis of Danone's operations, focusing on product costing systems, corporate social responsibility (CSR), and sustainability reporting. It begins by examining Danone's business processes, including upstream, manufacturing, and downstream activities, highlighting the company's commitment to health and well-being through its food products. The report then delves into the design of an activity-based costing (ABC) system, comparing it with traditional costing methods and illustrating its advantages for accurate service costing and decision-making. Finally, it addresses Danone's social and environmental concerns, evaluating its performance based on social indicators like employee satisfaction and industrial accident frequency, and discussing initiatives for waste reduction, resource management, and pollution prevention. The analysis incorporates cost management principles and decision models to support tactical decision-making and foster environmentally sustainable operations, offering valuable insights into Danone's strategic approach to cost management and corporate responsibility.

Running head: OPERATIONS MANAGEMENT

Operations Management

Name of Student:

Name of University:

Author’s Note:

Operations Management

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1OPERATIONS MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Component 1 – Business processes.................................................................................................2

Part A...........................................................................................................................................2

Part B...........................................................................................................................................3

Part C...........................................................................................................................................3

Component 2 – Activity based overhead costing system................................................................0

Part A...........................................................................................................................................0

Part B...........................................................................................................................................0

Part C...........................................................................................................................................1

v)..................................................................................................................................................2

Part D...........................................................................................................................................3

Component 3 – Corporate social responsibility and sustainability reporting..................................4

Part A...........................................................................................................................................4

Part B...........................................................................................................................................4

Part C...........................................................................................................................................9

Part D...........................................................................................................................................9

Part E.........................................................................................................................................10

Part F..........................................................................................................................................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Component 1 – Business processes.................................................................................................2

Part A...........................................................................................................................................2

Part B...........................................................................................................................................3

Part C...........................................................................................................................................3

Component 2 – Activity based overhead costing system................................................................0

Part A...........................................................................................................................................0

Part B...........................................................................................................................................0

Part C...........................................................................................................................................1

v)..................................................................................................................................................2

Part D...........................................................................................................................................3

Component 3 – Corporate social responsibility and sustainability reporting..................................4

Part A...........................................................................................................................................4

Part B...........................................................................................................................................4

Part C...........................................................................................................................................9

Part D...........................................................................................................................................9

Part E.........................................................................................................................................10

Part F..........................................................................................................................................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

2OPERATIONS MANAGEMENT

Introduction

The report aims to address the issues concerning various aspects of product costing

systems, social responsibility and sustainability of Danone. The first segment of the report has

discussed about the business process, the second segment have shown the design of activity-

based costing and the third portion of the report has stated about the corporate social

responsibility and sustainability aspects of the business. Some of the main concepts have been

demonstrated with an understanding of cost management principles, decision models cost

products and services and integrating cost management principles for supporting tactical

decision-making. The report has also included and is a discussion on determining different

perspectives of the stakeholder on management accounting systems.

Component 1 – Business processes

Part A

Danone is dedicated wholly in achieving health through food and the main mission of the

company is seen with delivering the best food product for a group of all people and ensure social

and cultural welfare. The main conviction at Danone that will be crucial for building sustaining

health and well-being from birth to old age. The global operations of the company are seen with

the presence in countries such as “United States, France, China, Russia, Indonesia, United

Kingdom, Spain, Mexico, Argentina and Germany”. The company’s portfolio consists of both

local brands and international brands. The main brands of the company include “Activia,

Actimel, Danimals, Yocrunch, waters including Evian, Aqua, Volvic and Aptamil” (Danone

North America 2018). Some of the main revenue streams of the company includes

Retail food products

Dairy products

Packaged drinking water

Fast Moving Consumer Goods

Introduction

The report aims to address the issues concerning various aspects of product costing

systems, social responsibility and sustainability of Danone. The first segment of the report has

discussed about the business process, the second segment have shown the design of activity-

based costing and the third portion of the report has stated about the corporate social

responsibility and sustainability aspects of the business. Some of the main concepts have been

demonstrated with an understanding of cost management principles, decision models cost

products and services and integrating cost management principles for supporting tactical

decision-making. The report has also included and is a discussion on determining different

perspectives of the stakeholder on management accounting systems.

Component 1 – Business processes

Part A

Danone is dedicated wholly in achieving health through food and the main mission of the

company is seen with delivering the best food product for a group of all people and ensure social

and cultural welfare. The main conviction at Danone that will be crucial for building sustaining

health and well-being from birth to old age. The global operations of the company are seen with

the presence in countries such as “United States, France, China, Russia, Indonesia, United

Kingdom, Spain, Mexico, Argentina and Germany”. The company’s portfolio consists of both

local brands and international brands. The main brands of the company include “Activia,

Actimel, Danimals, Yocrunch, waters including Evian, Aqua, Volvic and Aptamil” (Danone

North America 2018). Some of the main revenue streams of the company includes

Retail food products

Dairy products

Packaged drinking water

Fast Moving Consumer Goods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3OPERATIONS MANAGEMENT

Part B

The product category is a new concept which focuses on health and well-being of

consumer by delivering natural and healthy food products. Changing market scenario with more

number of health-conscious people around the world, the need for a customised sustainable and

healthy food is fundamental. Therefore, the main category of the company’s depicted with

manufacturing industry. Several companies which are included in this type of product category

includes “General Mills, Nestle, The Kraft Heinz Company, The Coca-Cola Company and

PepsiCo who are responsible for manufacturing their own products which can be easily suited to

the health-conscious needs of the consumers. Therefore, some of the major products included in

this category includes all the different types of health drinks, dairy products, packaged drinking

water, nutritional food products for kids and children and various types of organic plant-based

food products. Therefore, the company digs deep into the anatomy of the present health needs of

people of the world and making the most of natural products with reduced amount of

preservatives (Danone.com 2018).

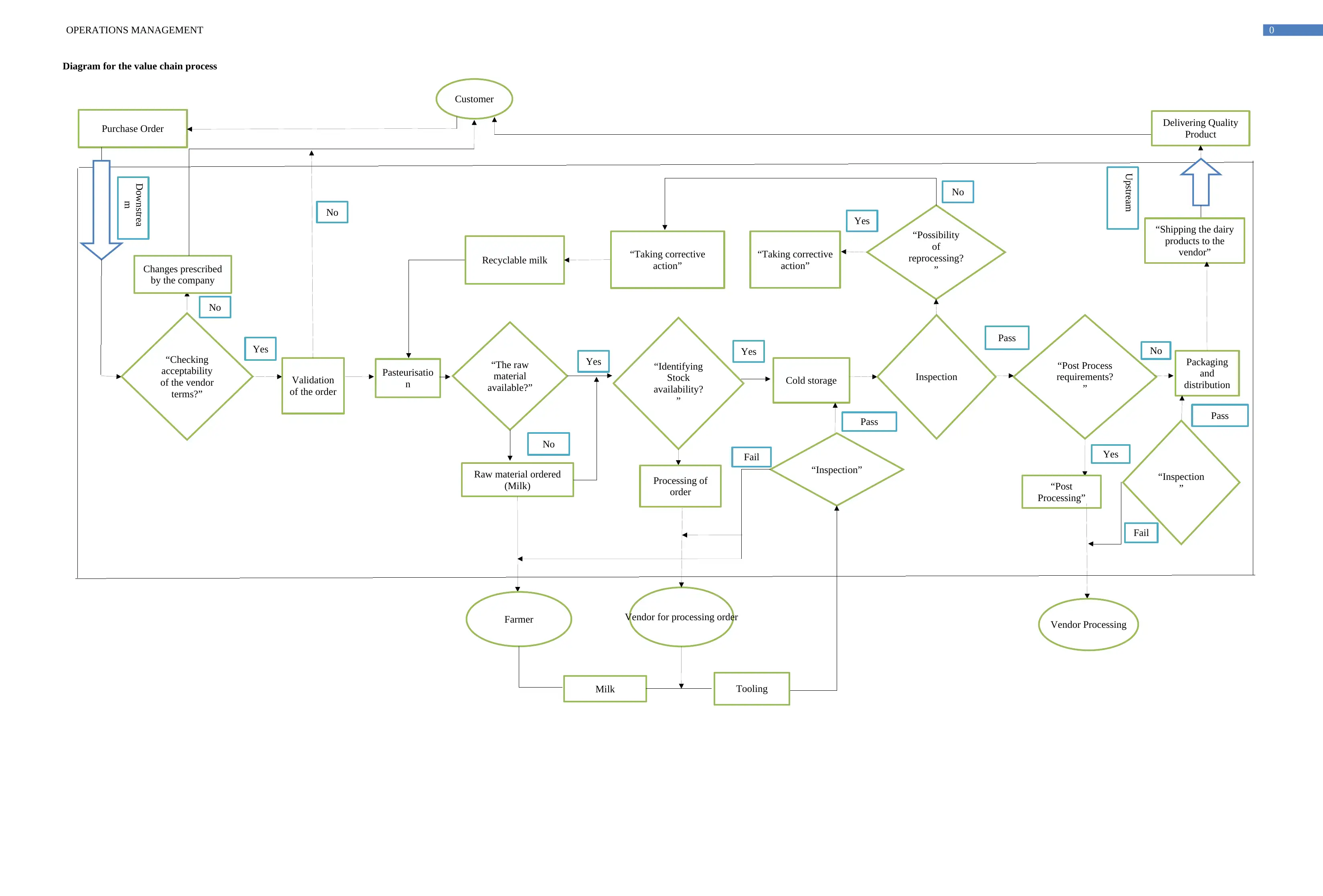

Part C

The process diagram depicts the equivalence of order which is carried out in the overall

manufacturing process of dairy products by the company. The value chain map has included both

upstream activities and downstream activities.

i. Upstream activities- The upstream activities can be clearly depicted with verification

and inspection of the dairy products at each stage of batch which have been customised

as per company specification. The final stage of the upstream operations include shipping

the final product to the vendor’s (Sizemore 2015).

ii. Manufacturing activities- Some of the main raw materials purchased by the company

includes Nutraceutical, Flavours, Butter, Cream, Powdered dairy ingredients and Milk.

Among the raw materials milk is considered as the most important ingredient. The

conversion of the raw material leads to various types of dairy products such as yoghurt,

packaged milk, cheese, flavoured milk product and health drink based on milk.

iii. Downstream activities- Some of the downstream activities of the company can be

clearly depicted with beginning of placing the order by the vendors for products such as

yoghurt, packaged milk, cheese, flavoured milk product and health drink based on milk.

Part B

The product category is a new concept which focuses on health and well-being of

consumer by delivering natural and healthy food products. Changing market scenario with more

number of health-conscious people around the world, the need for a customised sustainable and

healthy food is fundamental. Therefore, the main category of the company’s depicted with

manufacturing industry. Several companies which are included in this type of product category

includes “General Mills, Nestle, The Kraft Heinz Company, The Coca-Cola Company and

PepsiCo who are responsible for manufacturing their own products which can be easily suited to

the health-conscious needs of the consumers. Therefore, some of the major products included in

this category includes all the different types of health drinks, dairy products, packaged drinking

water, nutritional food products for kids and children and various types of organic plant-based

food products. Therefore, the company digs deep into the anatomy of the present health needs of

people of the world and making the most of natural products with reduced amount of

preservatives (Danone.com 2018).

Part C

The process diagram depicts the equivalence of order which is carried out in the overall

manufacturing process of dairy products by the company. The value chain map has included both

upstream activities and downstream activities.

i. Upstream activities- The upstream activities can be clearly depicted with verification

and inspection of the dairy products at each stage of batch which have been customised

as per company specification. The final stage of the upstream operations include shipping

the final product to the vendor’s (Sizemore 2015).

ii. Manufacturing activities- Some of the main raw materials purchased by the company

includes Nutraceutical, Flavours, Butter, Cream, Powdered dairy ingredients and Milk.

Among the raw materials milk is considered as the most important ingredient. The

conversion of the raw material leads to various types of dairy products such as yoghurt,

packaged milk, cheese, flavoured milk product and health drink based on milk.

iii. Downstream activities- Some of the downstream activities of the company can be

clearly depicted with beginning of placing the order by the vendors for products such as

yoghurt, packaged milk, cheese, flavoured milk product and health drink based on milk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4OPERATIONS MANAGEMENT

This is followed with checking of satisfactoriness of the vendor by providing them a

sample. The next process is followed by confirmation of the prescribed changes in the

order. After this stage, the company includes terms for carriers and seeking the validity of

the overall process. The next downstream activity is concerned with making the best use

of by-products of dairy products and using them in other retail food items manufactured

by the company (Teh et al. 2015).

iv. Administration activities- The main form of administrative activities involve

monitoring the overall activities in the value chain process. Some of the most evident

corporate overhead costs include machine -related costs, setup costs, delivery costs,

quality related costs, total overhead costs, total units, production overhead per unit, prime

cost and production cost per unit (Margolies and Hoddinott 2015).

This is followed with checking of satisfactoriness of the vendor by providing them a

sample. The next process is followed by confirmation of the prescribed changes in the

order. After this stage, the company includes terms for carriers and seeking the validity of

the overall process. The next downstream activity is concerned with making the best use

of by-products of dairy products and using them in other retail food items manufactured

by the company (Teh et al. 2015).

iv. Administration activities- The main form of administrative activities involve

monitoring the overall activities in the value chain process. Some of the most evident

corporate overhead costs include machine -related costs, setup costs, delivery costs,

quality related costs, total overhead costs, total units, production overhead per unit, prime

cost and production cost per unit (Margolies and Hoddinott 2015).

Customer

Purchase Order Delivering Quality

Product

“Checking

acceptability

of the vendor

terms?”

Changes prescribed

by the company

Validation

of the order

Pasteurisatio

n

“The raw

material

available?”

“Identifying

Stock

availability?

”

Cold storage Inspection

“Post Process

requirements?

”

Packaging

and

distribution

“Shipping the dairy

products to the

vendor”

“Inspection

”“Post

Processing”

Vendor Processing

Raw material ordered

(Milk)

Farmer

Processing of

order

“Inspection”

Milk Tooling

Vendor for processing order

Recyclable milk “Taking corrective

action”

“Taking corrective

action”

“Possibility

of

reprocessing?

”

No

Yes

Yes Yes

Yes

No

Pass

Pass

Fail

Fail

No

Pass

Yes

No

Downstrea

m

UpstreamNo

0OPERATIONS MANAGEMENT

Diagram for the value chain process

Purchase Order Delivering Quality

Product

“Checking

acceptability

of the vendor

terms?”

Changes prescribed

by the company

Validation

of the order

Pasteurisatio

n

“The raw

material

available?”

“Identifying

Stock

availability?

”

Cold storage Inspection

“Post Process

requirements?

”

Packaging

and

distribution

“Shipping the dairy

products to the

vendor”

“Inspection

”“Post

Processing”

Vendor Processing

Raw material ordered

(Milk)

Farmer

Processing of

order

“Inspection”

Milk Tooling

Vendor for processing order

Recyclable milk “Taking corrective

action”

“Taking corrective

action”

“Possibility

of

reprocessing?

”

No

Yes

Yes Yes

Yes

No

Pass

Pass

Fail

Fail

No

Pass

Yes

No

Downstrea

m

UpstreamNo

0OPERATIONS MANAGEMENT

Diagram for the value chain process

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0OPERATIONS MANAGEMENT

Component 2 – Activity based overhead costing system

Part A

In the subject of accounting, activity based costing and traditional costing are considered

as two different methods for allocation of indirect overhead cost to a product. In the traditional

costing system, the indirect costs are based on a previously identified overhead rate. In addition

to this, the overhead costs are treated as a single pool of indirect costs. This system is optimal

when indirect costs are low compared to direct costs. On the other hand, “activity-based costing”

system is often identified to be more accurate than the traditional costing system. This involves

segregating the indirect costs into a more precise activity pool.

Part B

Some of the main advantage of activity-based costing for the present manufacturing

organisation for producing yogurt is getting a more accurate method of service costing, thereby

creating a more accurate decision for pricing. The activity-based costing will be conducive in

making the non-value adding activities more visible thereby providing the management a scope

to eliminate them. For instance, in the present process the for the excess milk is not visible in the

traditional system. However, the company can look forward to create a separate processing

design to reuse the unused milk instead of treating it as a waste.

Some of the major drawback of the ABC system company can be clearly depicted with

difficulties in understanding of the cost drivers for certain products which has high volatility of

fluctuations in the market. In addition to this, the company should confirm that the resources are

available to implement the ABC and the costs outweigh the benefits of the ABC system.

Component 2 – Activity based overhead costing system

Part A

In the subject of accounting, activity based costing and traditional costing are considered

as two different methods for allocation of indirect overhead cost to a product. In the traditional

costing system, the indirect costs are based on a previously identified overhead rate. In addition

to this, the overhead costs are treated as a single pool of indirect costs. This system is optimal

when indirect costs are low compared to direct costs. On the other hand, “activity-based costing”

system is often identified to be more accurate than the traditional costing system. This involves

segregating the indirect costs into a more precise activity pool.

Part B

Some of the main advantage of activity-based costing for the present manufacturing

organisation for producing yogurt is getting a more accurate method of service costing, thereby

creating a more accurate decision for pricing. The activity-based costing will be conducive in

making the non-value adding activities more visible thereby providing the management a scope

to eliminate them. For instance, in the present process the for the excess milk is not visible in the

traditional system. However, the company can look forward to create a separate processing

design to reuse the unused milk instead of treating it as a waste.

Some of the major drawback of the ABC system company can be clearly depicted with

difficulties in understanding of the cost drivers for certain products which has high volatility of

fluctuations in the market. In addition to this, the company should confirm that the resources are

available to implement the ABC and the costs outweigh the benefits of the ABC system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1OPERATIONS MANAGEMENT

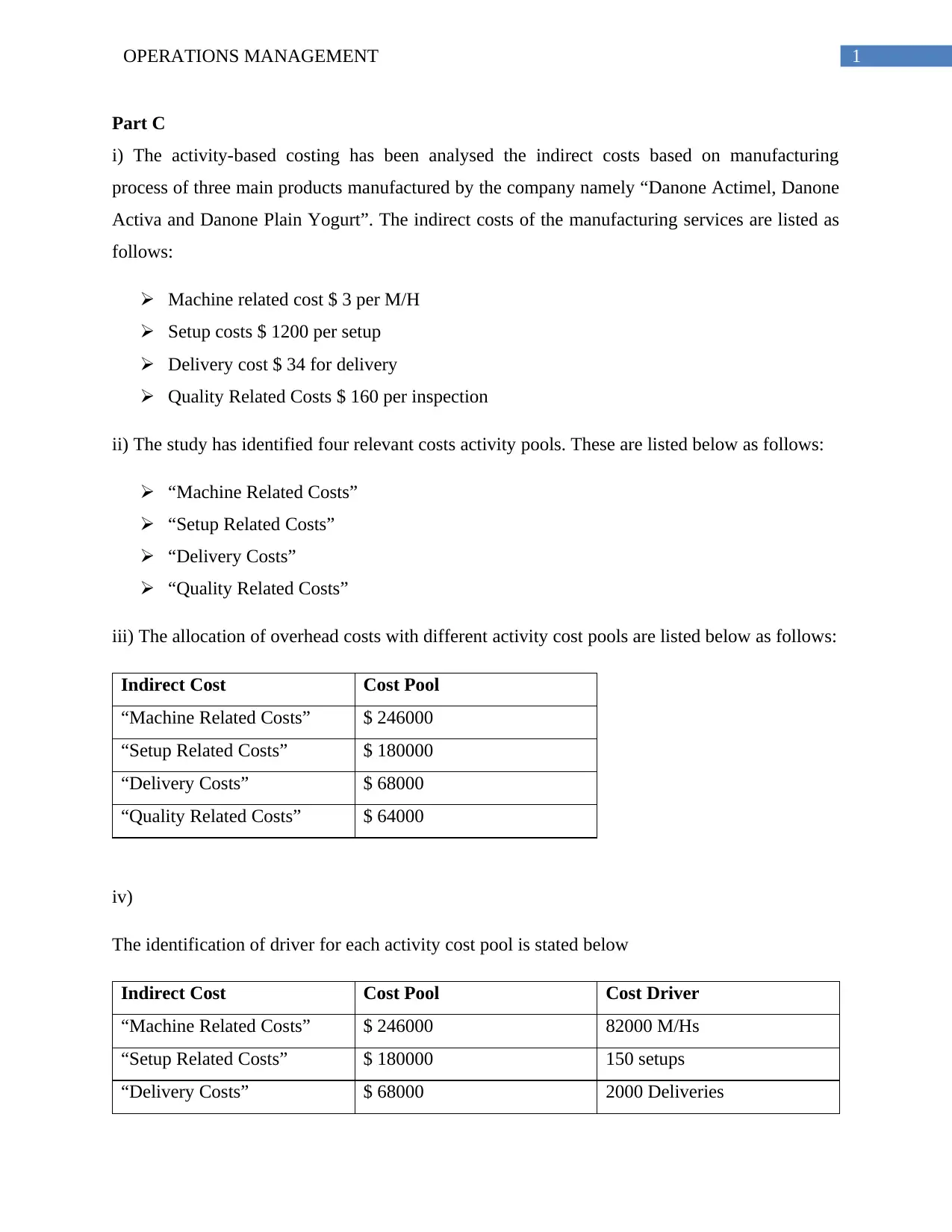

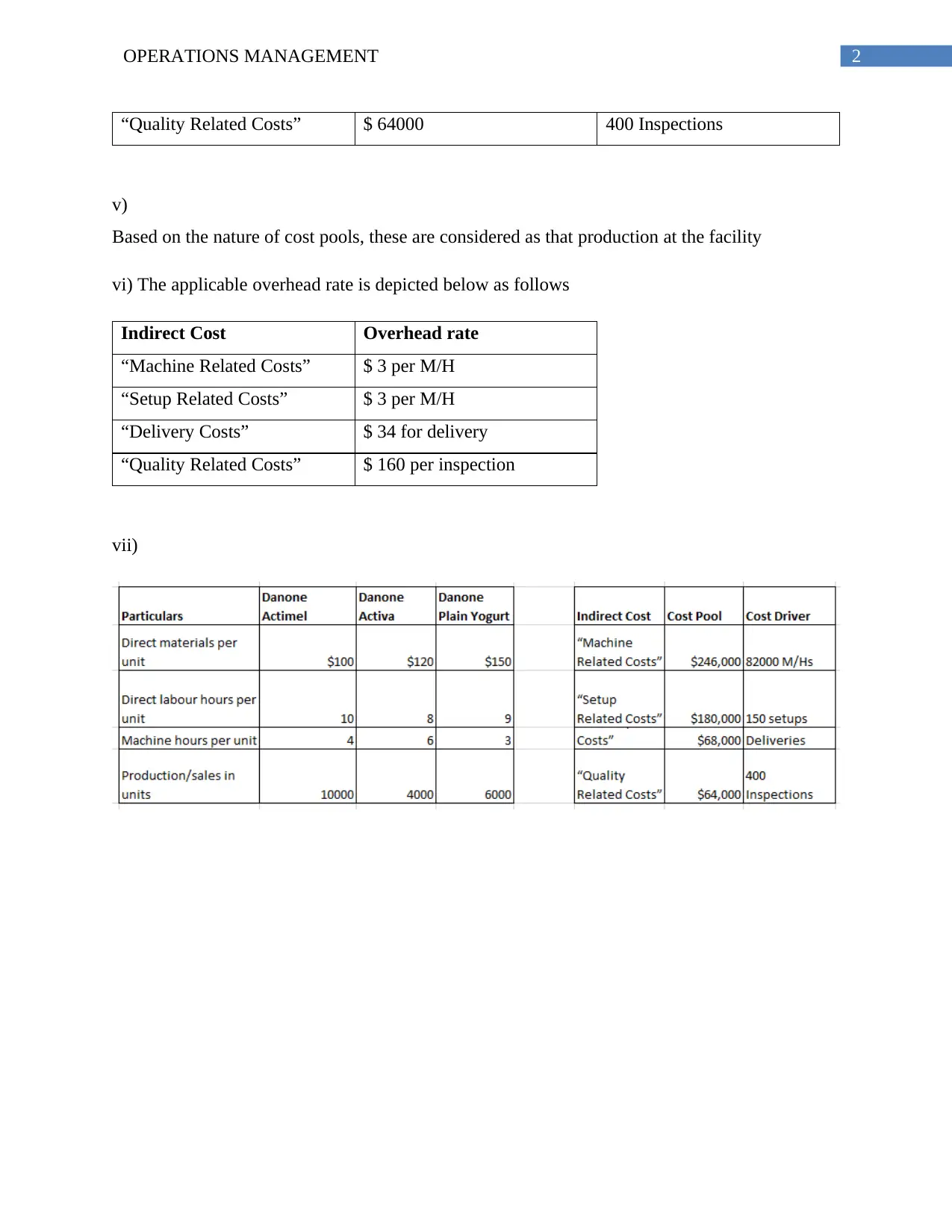

Part C

i) The activity-based costing has been analysed the indirect costs based on manufacturing

process of three main products manufactured by the company namely “Danone Actimel, Danone

Activa and Danone Plain Yogurt”. The indirect costs of the manufacturing services are listed as

follows:

Machine related cost $ 3 per M/H

Setup costs $ 1200 per setup

Delivery cost $ 34 for delivery

Quality Related Costs $ 160 per inspection

ii) The study has identified four relevant costs activity pools. These are listed below as follows:

“Machine Related Costs”

“Setup Related Costs”

“Delivery Costs”

“Quality Related Costs”

iii) The allocation of overhead costs with different activity cost pools are listed below as follows:

Indirect Cost Cost Pool

“Machine Related Costs” $ 246000

“Setup Related Costs” $ 180000

“Delivery Costs” $ 68000

“Quality Related Costs” $ 64000

iv)

The identification of driver for each activity cost pool is stated below

Indirect Cost Cost Pool Cost Driver

“Machine Related Costs” $ 246000 82000 M/Hs

“Setup Related Costs” $ 180000 150 setups

“Delivery Costs” $ 68000 2000 Deliveries

Part C

i) The activity-based costing has been analysed the indirect costs based on manufacturing

process of three main products manufactured by the company namely “Danone Actimel, Danone

Activa and Danone Plain Yogurt”. The indirect costs of the manufacturing services are listed as

follows:

Machine related cost $ 3 per M/H

Setup costs $ 1200 per setup

Delivery cost $ 34 for delivery

Quality Related Costs $ 160 per inspection

ii) The study has identified four relevant costs activity pools. These are listed below as follows:

“Machine Related Costs”

“Setup Related Costs”

“Delivery Costs”

“Quality Related Costs”

iii) The allocation of overhead costs with different activity cost pools are listed below as follows:

Indirect Cost Cost Pool

“Machine Related Costs” $ 246000

“Setup Related Costs” $ 180000

“Delivery Costs” $ 68000

“Quality Related Costs” $ 64000

iv)

The identification of driver for each activity cost pool is stated below

Indirect Cost Cost Pool Cost Driver

“Machine Related Costs” $ 246000 82000 M/Hs

“Setup Related Costs” $ 180000 150 setups

“Delivery Costs” $ 68000 2000 Deliveries

2OPERATIONS MANAGEMENT

“Quality Related Costs” $ 64000 400 Inspections

v)

Based on the nature of cost pools, these are considered as that production at the facility

vi) The applicable overhead rate is depicted below as follows

Indirect Cost Overhead rate

“Machine Related Costs” $ 3 per M/H

“Setup Related Costs” $ 3 per M/H

“Delivery Costs” $ 34 for delivery

“Quality Related Costs” $ 160 per inspection

vii)

“Quality Related Costs” $ 64000 400 Inspections

v)

Based on the nature of cost pools, these are considered as that production at the facility

vi) The applicable overhead rate is depicted below as follows

Indirect Cost Overhead rate

“Machine Related Costs” $ 3 per M/H

“Setup Related Costs” $ 3 per M/H

“Delivery Costs” $ 34 for delivery

“Quality Related Costs” $ 160 per inspection

vii)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3OPERATIONS MANAGEMENT

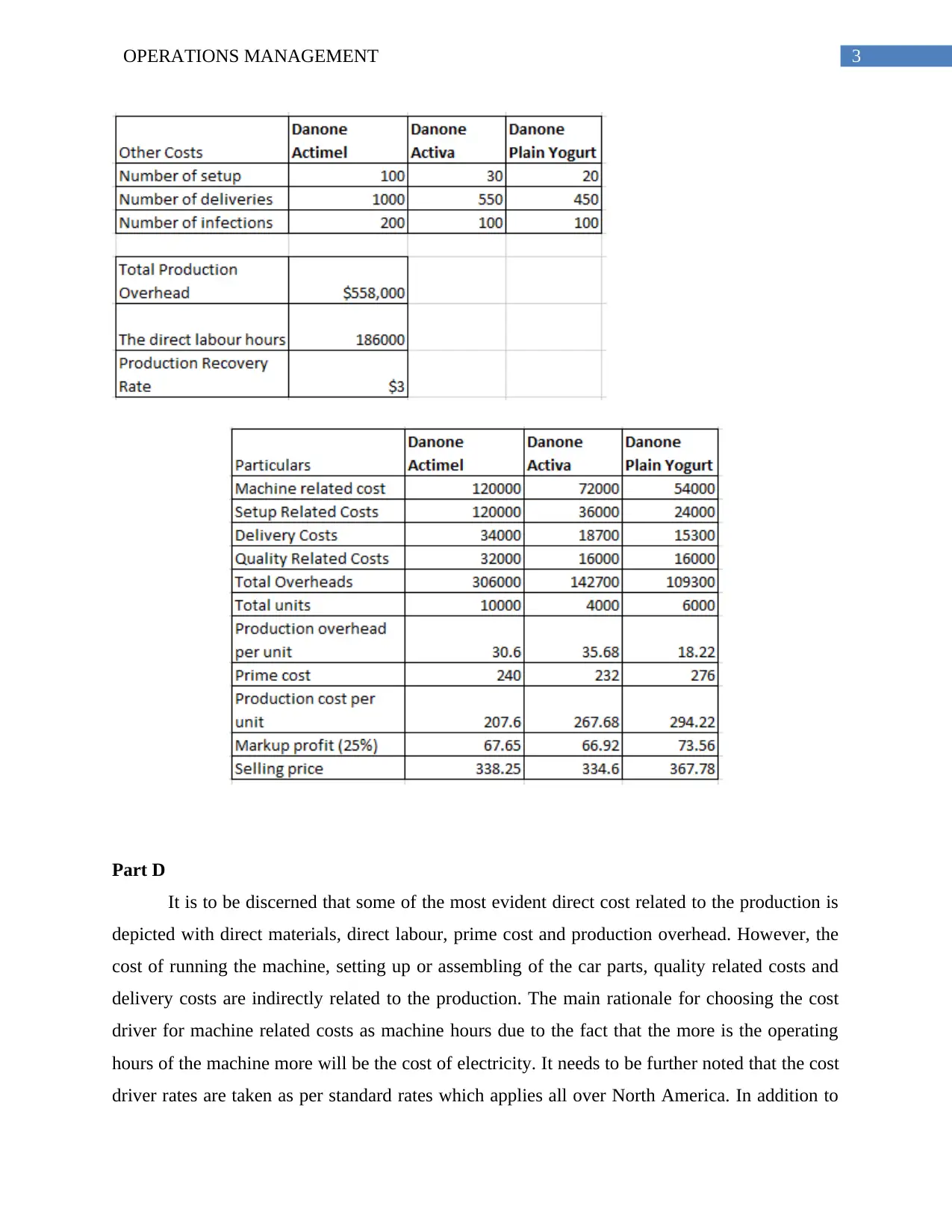

Part D

It is to be discerned that some of the most evident direct cost related to the production is

depicted with direct materials, direct labour, prime cost and production overhead. However, the

cost of running the machine, setting up or assembling of the car parts, quality related costs and

delivery costs are indirectly related to the production. The main rationale for choosing the cost

driver for machine related costs as machine hours due to the fact that the more is the operating

hours of the machine more will be the cost of electricity. It needs to be further noted that the cost

driver rates are taken as per standard rates which applies all over North America. In addition to

Part D

It is to be discerned that some of the most evident direct cost related to the production is

depicted with direct materials, direct labour, prime cost and production overhead. However, the

cost of running the machine, setting up or assembling of the car parts, quality related costs and

delivery costs are indirectly related to the production. The main rationale for choosing the cost

driver for machine related costs as machine hours due to the fact that the more is the operating

hours of the machine more will be the cost of electricity. It needs to be further noted that the cost

driver rates are taken as per standard rates which applies all over North America. In addition to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4OPERATIONS MANAGEMENT

this, the setup costs are driven by total number of setups. Similarly, the delivery costs are directly

controlled by the total number of deliveries in a day. Finally, the cost driver selected for quality

related costs is total number of inspections as more will be the number of inspections conducted

higher cost will be required to pay to the personnel (Kapić 2014).

It needs to be discerned that the company is operating in a highly competitive scenario of

retail food market. This shows that, there is a good level of understanding required for cost

structure of each product. The activity-based costing system is able to examine the overhead

each product consumes. Additionally, this costing system is conducive for the company in

establishment of selling prices. Since it is operating in a competitive market, the use of cost plus

for establishment of selling prices may not be particularly appropriate. Therefore, minimum

selling price strategy is ideal in the present scenario (Kapian and Anderson 2014).

Component 3 – Corporate social responsibility and sustainability reporting

Part A

As the selected industry is directly related to food manicuring industry, the most evident

social and environmental concerns are related to the waste and emissions, resource usage reuse,

recycle and disposal. Some of the non-product outputs in gaseous or liquid form during the

manufacturing process is identified as the main environmental concern. In addition to this, the

company is responsible for using a large amount of natural resources and any instance of misuse

of these resources can prove to be detrimental to the environment and sustainability. This is

responsible for causing a considerable amount of pollution in the environment. In addition to

this, these have also significant influence on the social issues (Snapshot 2015).

Part B

The three social indicators of the organisation are

Concern for the employees

Quality assurance to the customer

Initiatives for preventing industrial accidents

this, the setup costs are driven by total number of setups. Similarly, the delivery costs are directly

controlled by the total number of deliveries in a day. Finally, the cost driver selected for quality

related costs is total number of inspections as more will be the number of inspections conducted

higher cost will be required to pay to the personnel (Kapić 2014).

It needs to be discerned that the company is operating in a highly competitive scenario of

retail food market. This shows that, there is a good level of understanding required for cost

structure of each product. The activity-based costing system is able to examine the overhead

each product consumes. Additionally, this costing system is conducive for the company in

establishment of selling prices. Since it is operating in a competitive market, the use of cost plus

for establishment of selling prices may not be particularly appropriate. Therefore, minimum

selling price strategy is ideal in the present scenario (Kapian and Anderson 2014).

Component 3 – Corporate social responsibility and sustainability reporting

Part A

As the selected industry is directly related to food manicuring industry, the most evident

social and environmental concerns are related to the waste and emissions, resource usage reuse,

recycle and disposal. Some of the non-product outputs in gaseous or liquid form during the

manufacturing process is identified as the main environmental concern. In addition to this, the

company is responsible for using a large amount of natural resources and any instance of misuse

of these resources can prove to be detrimental to the environment and sustainability. This is

responsible for causing a considerable amount of pollution in the environment. In addition to

this, these have also significant influence on the social issues (Snapshot 2015).

Part B

The three social indicators of the organisation are

Concern for the employees

Quality assurance to the customer

Initiatives for preventing industrial accidents

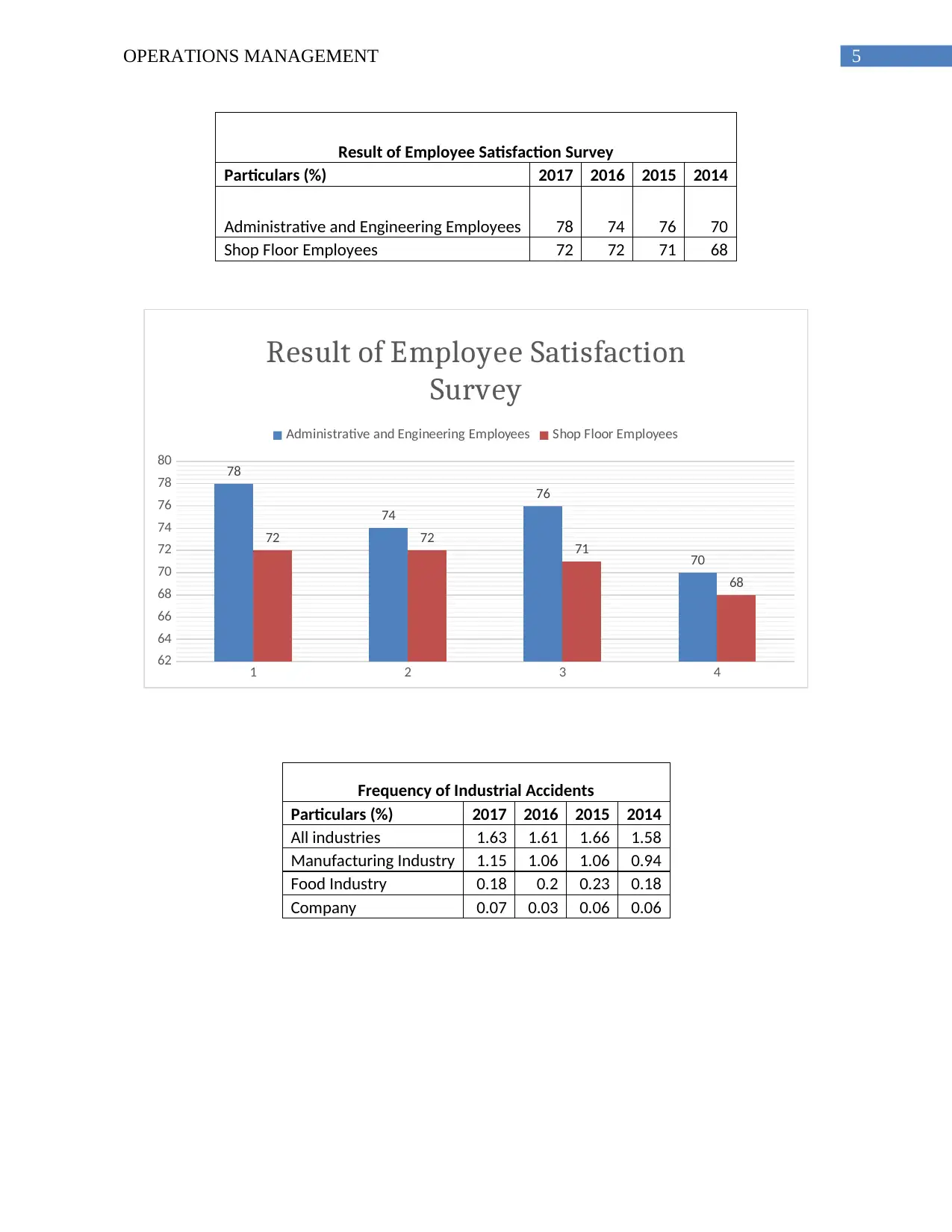

5OPERATIONS MANAGEMENT

Result of Employee Satisfaction Survey

Particulars (%) 2017 2016 2015 2014

Administrative and Engineering Employees 78 74 76 70

Shop Floor Employees 72 72 71 68

1 2 3 4

62

64

66

68

70

72

74

76

78

80 78

74

76

70

72 72 71

68

Result of Employee Satisfaction

Survey

Administrative and Engineering Employees Shop Floor Employees

Frequency of Industrial Accidents

Particulars (%) 2017 2016 2015 2014

All industries 1.63 1.61 1.66 1.58

Manufacturing Industry 1.15 1.06 1.06 0.94

Food Industry 0.18 0.2 0.23 0.18

Company 0.07 0.03 0.06 0.06

Result of Employee Satisfaction Survey

Particulars (%) 2017 2016 2015 2014

Administrative and Engineering Employees 78 74 76 70

Shop Floor Employees 72 72 71 68

1 2 3 4

62

64

66

68

70

72

74

76

78

80 78

74

76

70

72 72 71

68

Result of Employee Satisfaction

Survey

Administrative and Engineering Employees Shop Floor Employees

Frequency of Industrial Accidents

Particulars (%) 2017 2016 2015 2014

All industries 1.63 1.61 1.66 1.58

Manufacturing Industry 1.15 1.06 1.06 0.94

Food Industry 0.18 0.2 0.23 0.18

Company 0.07 0.03 0.06 0.06

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.