Data Handling and Decision Making Report: Robert Bosch GmbH Analysis

VerifiedAdded on 2023/01/13

|30

|6004

|43

Report

AI Summary

This report provides a comprehensive data analysis of Robert Bosch GmbH, focusing on data handling and its impact on decision-making. The analysis begins with an introduction to data handling and its importance, followed by an examination of Bosch's financial statements, including the balance sheet, income statement, and cash flow statement. The report explores data protection requirements, ethical considerations, and the role of stakeholders in data analysis. It also delves into the application of big data, strategic decision-making, and the impact of financial and non-financial data on business performance. The report includes data cleaning and preparation, along with an assessment of sample effectiveness and multicollinearity. Descriptive data analysis, including PBT and financial income/expenses, is presented, along with a forecast report and justification of the model. The interpretation of results, recommendations, and the application of a big data framework conclude the analysis, providing a thorough overview of data-driven decision-making at Bosch.

Data Handling and Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

Task 4...............................................................................................................................................6

Business related information dataset presents.............................................................................6

Data cleaning and preparation.....................................................................................................6

Sample effectiveness...................................................................................................................7

Task 5...............................................................................................................................................7

Multicollinearity and descriptive data analysis...........................................................................7

PBT and financial income and expenses...........................................................................7

Forecast report...............................................................................................................................13

Table (1) Sales revenue COGS.................................................................................................13

Table (2) Sales revenue and Administrative expenses.............................................................14

Table (3) Sales revenue and R&D............................................................................................15

Table (4) Sales revenue and operating expenses.......................................................................16

Table (5) PBT and financial income.........................................................................................17

Table (6) PBT and financial expenses......................................................................................18

Justification of model................................................................................................................19

TASK 6..........................................................................................................................................19

Interpretation of results.............................................................................................................19

TASK 7..........................................................................................................................................27

Recommendation .....................................................................................................................27

Big data framework...................................................................................................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

Task 4...............................................................................................................................................6

Business related information dataset presents.............................................................................6

Data cleaning and preparation.....................................................................................................6

Sample effectiveness...................................................................................................................7

Task 5...............................................................................................................................................7

Multicollinearity and descriptive data analysis...........................................................................7

PBT and financial income and expenses...........................................................................7

Forecast report...............................................................................................................................13

Table (1) Sales revenue COGS.................................................................................................13

Table (2) Sales revenue and Administrative expenses.............................................................14

Table (3) Sales revenue and R&D............................................................................................15

Table (4) Sales revenue and operating expenses.......................................................................16

Table (5) PBT and financial income.........................................................................................17

Table (6) PBT and financial expenses......................................................................................18

Justification of model................................................................................................................19

TASK 6..........................................................................................................................................19

Interpretation of results.............................................................................................................19

TASK 7..........................................................................................................................................27

Recommendation .....................................................................................................................27

Big data framework...................................................................................................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

INTRODUCTION

Data handling is referred to as an effective procedure which helps in ensuring that the

data researched is appropriately stored and disposed in the most secured manner (Luh, 2018).

Data is referred to as the numerical facts and figures who in turn tends to focus on protecting the

set information in an electronic and non- electronic mean. This study will highlight on the key

sources of the data collected, data protection requirements, major strategic decision making,

business related information, data mining and interpretations of the results and lastly effective

recommendation for the decision-making procedure.

Robert Bosch GmbH is one of the leading private company which was founded in the

year 1886 by Robert Bosh. This company is headquartered in the Gerlingen, Germany. This

company mainly deals in various range of products and services such as power tool, engineering,

home appliances, cloud computing, electronics, internet of things, automotive parts, security

system, etc.

TASK 1

The financial statements used by the Bosh company to make an appropriate decision

making mainly comprise balance sheet, statement of cash flow, statement of shareholder's equity

and income statement. Balance sheet in turn helps n providing a snapshot of the entity for the

specific period. On the other hand, income statement of the company in turn focuses on

effectively determining the capability of the company to generate high degree of profits. Cash

flow statement is crucial in the decision making procedure because it helps in effectively

determining the inflow ad outflow of the cash for the specific organization. As per the income

statement, the sales revenue of the company has been increasing from the year 2014 at 48951 to

78465 in the year 2018. But on the other hand the financial expenses of the company is also

increasing from 1769 in 2014 to 2391 ion 2018. This in turn leads to slower growth rate for the

Bosh company. Non – financial data associated with the environmental impacts, social

responsibility, relationship with vendors, etc. in turn is considered to be an effective measure for

appropriate decision making.

Data integrity is referred to as the completeness, accuracy and consistency of the data for

the specific time duration. The data presented in the financial and non financial statements tends

to have data integrity (Lavreniuk and et.al., 2016). Identification of the gap within the data

analysis in turn helps in recognition of the current state by electively measuring the money,

Data handling is referred to as an effective procedure which helps in ensuring that the

data researched is appropriately stored and disposed in the most secured manner (Luh, 2018).

Data is referred to as the numerical facts and figures who in turn tends to focus on protecting the

set information in an electronic and non- electronic mean. This study will highlight on the key

sources of the data collected, data protection requirements, major strategic decision making,

business related information, data mining and interpretations of the results and lastly effective

recommendation for the decision-making procedure.

Robert Bosch GmbH is one of the leading private company which was founded in the

year 1886 by Robert Bosh. This company is headquartered in the Gerlingen, Germany. This

company mainly deals in various range of products and services such as power tool, engineering,

home appliances, cloud computing, electronics, internet of things, automotive parts, security

system, etc.

TASK 1

The financial statements used by the Bosh company to make an appropriate decision

making mainly comprise balance sheet, statement of cash flow, statement of shareholder's equity

and income statement. Balance sheet in turn helps n providing a snapshot of the entity for the

specific period. On the other hand, income statement of the company in turn focuses on

effectively determining the capability of the company to generate high degree of profits. Cash

flow statement is crucial in the decision making procedure because it helps in effectively

determining the inflow ad outflow of the cash for the specific organization. As per the income

statement, the sales revenue of the company has been increasing from the year 2014 at 48951 to

78465 in the year 2018. But on the other hand the financial expenses of the company is also

increasing from 1769 in 2014 to 2391 ion 2018. This in turn leads to slower growth rate for the

Bosh company. Non – financial data associated with the environmental impacts, social

responsibility, relationship with vendors, etc. in turn is considered to be an effective measure for

appropriate decision making.

Data integrity is referred to as the completeness, accuracy and consistency of the data for

the specific time duration. The data presented in the financial and non financial statements tends

to have data integrity (Lavreniuk and et.al., 2016). Identification of the gap within the data

analysis in turn helps in recognition of the current state by electively measuring the money,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

labour and time in order to compare with the current market states of the Bosh company. The

financial data presented in the reports tends to assess that, the profit and growth of the company

has been increasing but in turn there seems to be a decreasing trend of growth in the Bosh

company.

Data source in turn is considered to be a digitalized information which in turn is useful in

streamlining the various set of data services across the internet. The key sources of the data for

the financial sources in turn mainly keeps all the important information with database

management system. This in turn helps in protecting the right information within prescribed time

frame. File data sources, machine data sources, etc. in turn is considered to be one of the most

appropriate tool in order to protect the data which in turn eventually leads to better decision

making (Konstantopoulos and Pantziou, 2018). Modern analytic, Internet of things and big data

are considered to be one of the key sources which in turn is considered to be very useful in

collection of data for better decision making. This in turn eventually leads to higher operational

growth and efficiency of the business.

TASK 2

Data protection in turn is referred to as the ethical issue because it tends to focus on

respecting the individual rights associated with the use of information and privacy (Prince, Vonn

and Gill, 2018). Stakeholders of the company tends to require financial position in order to gain

idea associated with the tactical and strategical plans of management. The board of directors of

the company tends to review the various ratios and financial and non- financial statements of the

company. Shareholders of the company are interested in income statement, balance sheet and

profitability ratios of the company in order to assess the return on the investment made within the

company (Financial Statements and Stakeholders, 2017). Operating profit margin is necessary for

effectively measuring the performance of the business. The trade creditors and suppliers of the

company tends to evaluate the cash flow, balance sheet and liquidity ratios of the company.

Other non- financial reports such as competitive reports, budgetary reports, etc. in turn are

considered to be an effective reports and statements which in turn is useful in improving the risk

management. Governance report, notes of the financial statements, etc., are considered to be an

effective report in order to improve the decision making capability within the organisation.

In order to ensure data integrity within the organization, Bosch must in turn focus on

cleaning and effectively maintaining the various range of data sets within the organization.

financial data presented in the reports tends to assess that, the profit and growth of the company

has been increasing but in turn there seems to be a decreasing trend of growth in the Bosh

company.

Data source in turn is considered to be a digitalized information which in turn is useful in

streamlining the various set of data services across the internet. The key sources of the data for

the financial sources in turn mainly keeps all the important information with database

management system. This in turn helps in protecting the right information within prescribed time

frame. File data sources, machine data sources, etc. in turn is considered to be one of the most

appropriate tool in order to protect the data which in turn eventually leads to better decision

making (Konstantopoulos and Pantziou, 2018). Modern analytic, Internet of things and big data

are considered to be one of the key sources which in turn is considered to be very useful in

collection of data for better decision making. This in turn eventually leads to higher operational

growth and efficiency of the business.

TASK 2

Data protection in turn is referred to as the ethical issue because it tends to focus on

respecting the individual rights associated with the use of information and privacy (Prince, Vonn

and Gill, 2018). Stakeholders of the company tends to require financial position in order to gain

idea associated with the tactical and strategical plans of management. The board of directors of

the company tends to review the various ratios and financial and non- financial statements of the

company. Shareholders of the company are interested in income statement, balance sheet and

profitability ratios of the company in order to assess the return on the investment made within the

company (Financial Statements and Stakeholders, 2017). Operating profit margin is necessary for

effectively measuring the performance of the business. The trade creditors and suppliers of the

company tends to evaluate the cash flow, balance sheet and liquidity ratios of the company.

Other non- financial reports such as competitive reports, budgetary reports, etc. in turn are

considered to be an effective reports and statements which in turn is useful in improving the risk

management. Governance report, notes of the financial statements, etc., are considered to be an

effective report in order to improve the decision making capability within the organisation.

In order to ensure data integrity within the organization, Bosch must in turn focus on

cleaning and effectively maintaining the various range of data sets within the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Automation, validation of the data, updating the data on the continuous basis in turn helps in

assessing the various sets of data within the specific organization. Giving proper training to the

employees and giving them liability in turn helps the Bosch company in improving the data

integrity of the business. Updating data on the continuous and regular basis in turn helps in the

Bosch company in improving the data integrity of the business. Automation of the task and

automating the data entry helps in saving more time. This helps management to focus on more

complex task.

The General data protection regulation in turn tends to focus on effectively analysing the

various support services in order to embrace compliance and effectively overhauls the way an

organization protects its personal data. Protection of financial and personal data in turn is

considered to be one of the ethical requirement to ethically carry out several business activities.

Meeting all the ethical standards and assurance engagement in turn is considered to be one of the

major requirement while protecting the data within the organization.

TASK 3

The Bosch company can use big data to enhance the quality of carrying organization

activities. Big data in turn is considered to be one of the effective field which in turn is useful in

analysing and systematically extracting information from large complex data. Big data in turn is

considered to be very useful in systematically extracting large set of complex information which

in turn tends to inundate business on the day top day basis. Big data in turn is referred to as the

wide set of the information that in turn tends to grow at a very increasing rate (Higgins and et.al.,

2019). Current financial and and non- financial information are effectively used by

systematically analysing the set data with the help of various financial models.

The key strategic decision of the Bosh is to lower their financial expenses in order to gain

higher growth in the current financial year. The company also tends to focus on delivering

innovation and also improve the quality of life across the globe. This in turn eventually leads to

long term growth and sustainability for the Bosch company. The diversification strategy of the

Bosh in turn is considered to be as one of the most effective strategy in order to sustain in the

competitive market. Bosch company must in turn also focus on reducing its financial expenses

and cost reduction. This in turn helps in attaining economies of scale and growth of the company

over the years. Another effective strategy associated with the Bosch is to focus on the research

and development (Yuniarti and et.al., 2017, October). These strategies in turn is considered to be

assessing the various sets of data within the specific organization. Giving proper training to the

employees and giving them liability in turn helps the Bosch company in improving the data

integrity of the business. Updating data on the continuous and regular basis in turn helps in the

Bosch company in improving the data integrity of the business. Automation of the task and

automating the data entry helps in saving more time. This helps management to focus on more

complex task.

The General data protection regulation in turn tends to focus on effectively analysing the

various support services in order to embrace compliance and effectively overhauls the way an

organization protects its personal data. Protection of financial and personal data in turn is

considered to be one of the ethical requirement to ethically carry out several business activities.

Meeting all the ethical standards and assurance engagement in turn is considered to be one of the

major requirement while protecting the data within the organization.

TASK 3

The Bosch company can use big data to enhance the quality of carrying organization

activities. Big data in turn is considered to be one of the effective field which in turn is useful in

analysing and systematically extracting information from large complex data. Big data in turn is

considered to be very useful in systematically extracting large set of complex information which

in turn tends to inundate business on the day top day basis. Big data in turn is referred to as the

wide set of the information that in turn tends to grow at a very increasing rate (Higgins and et.al.,

2019). Current financial and and non- financial information are effectively used by

systematically analysing the set data with the help of various financial models.

The key strategic decision of the Bosh is to lower their financial expenses in order to gain

higher growth in the current financial year. The company also tends to focus on delivering

innovation and also improve the quality of life across the globe. This in turn eventually leads to

long term growth and sustainability for the Bosch company. The diversification strategy of the

Bosh in turn is considered to be as one of the most effective strategy in order to sustain in the

competitive market. Bosch company must in turn also focus on reducing its financial expenses

and cost reduction. This in turn helps in attaining economies of scale and growth of the company

over the years. Another effective strategy associated with the Bosch is to focus on the research

and development (Yuniarti and et.al., 2017, October). These strategies in turn is considered to be

one of the most appropriate which in turn helps in gaining competitive advantage and is also

useful in the improvement of the performance.

The Bosch company must focus on increasing the research and development expenditure of the

company in order to perform effective functions within the organization. Increase in the cost of

the creaser and expenditure will in turn results in effectively carrying several business

operations. The research and development expenditure of Bosch has been increasing over the

years from 3889 in 2008 to 7264 in 2017. On the other hand, the research and development

expenditure has in turn fallen down to 5963 million euros in the year 2018. The lower research

and development expenditure in turn tends to result in lower growth for the company (__-).

High degree of R&D expenditure in turn leads higher sustainable growth within the business

operations.

Task 4

Business related information dataset presents

Dataset presents business revenue, PBT and expenditures it made in its business. By

analysing dataset areas where firm need to work will be clearly identified and pin points will be

identified. In category of expenditure varied items are included like COGS, Distribution and

administrative cost, R&D Cost, Other operating expenses and Financial expenses.

Data cleaning and preparation

As can be seen that data is related to company financial performance and due to this

reason, no efforts are made for its preparation as it is already available in the Bosch annual report

in the final format. Data cleaning is done and no outliers are identified because every year

performance get changed slightly and due to this reason, no changes are made to the raw data. It

is very important to do data cleaning because in the data there are number of fluctuations that are

observed. These fluctuations are occasional in nature and observed only few times. In other

words, it can be said that these fluctuations do not represent actual behaviour of the variable.

Hence, it is very important to remove these data points from the variable so that more actual

picture of the variable can be seen about the variable by the analyst. Hence, in the analytics

analyst before using data for regression purpose clean it. Under this, spikes that are observed in

the data set are completely removed. In this regard varied approaches can be used and use of box

plot chart is one of them. In this chart quartiles are plotted and outliers can be easily seen in the

useful in the improvement of the performance.

The Bosch company must focus on increasing the research and development expenditure of the

company in order to perform effective functions within the organization. Increase in the cost of

the creaser and expenditure will in turn results in effectively carrying several business

operations. The research and development expenditure of Bosch has been increasing over the

years from 3889 in 2008 to 7264 in 2017. On the other hand, the research and development

expenditure has in turn fallen down to 5963 million euros in the year 2018. The lower research

and development expenditure in turn tends to result in lower growth for the company (__-).

High degree of R&D expenditure in turn leads higher sustainable growth within the business

operations.

Task 4

Business related information dataset presents

Dataset presents business revenue, PBT and expenditures it made in its business. By

analysing dataset areas where firm need to work will be clearly identified and pin points will be

identified. In category of expenditure varied items are included like COGS, Distribution and

administrative cost, R&D Cost, Other operating expenses and Financial expenses.

Data cleaning and preparation

As can be seen that data is related to company financial performance and due to this

reason, no efforts are made for its preparation as it is already available in the Bosch annual report

in the final format. Data cleaning is done and no outliers are identified because every year

performance get changed slightly and due to this reason, no changes are made to the raw data. It

is very important to do data cleaning because in the data there are number of fluctuations that are

observed. These fluctuations are occasional in nature and observed only few times. In other

words, it can be said that these fluctuations do not represent actual behaviour of the variable.

Hence, it is very important to remove these data points from the variable so that more actual

picture of the variable can be seen about the variable by the analyst. Hence, in the analytics

analyst before using data for regression purpose clean it. Under this, spikes that are observed in

the data set are completely removed. In this regard varied approaches can be used and use of box

plot chart is one of them. In this chart quartiles are plotted and outliers can be easily seen in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

chart if there are spikes in the data set. Effort are made by the analyst to remove these outliers to

maximum possible extent so that flat data can be obtained. If data with outliers will be used in

the regression then accurate results cannot be obtained. Hence, due to this reason data that is

cleaned by removing outliers is finally taken into account to run regression and to obtain relevant

results. It can be observed that there are certain assumptions for running

Sample effectiveness

Data set is accurately representing population as is clearly indicating current business

performance of the firm. Data of only 5 years is taken into account which is the one of the major

limitation of the research study.

Task 5

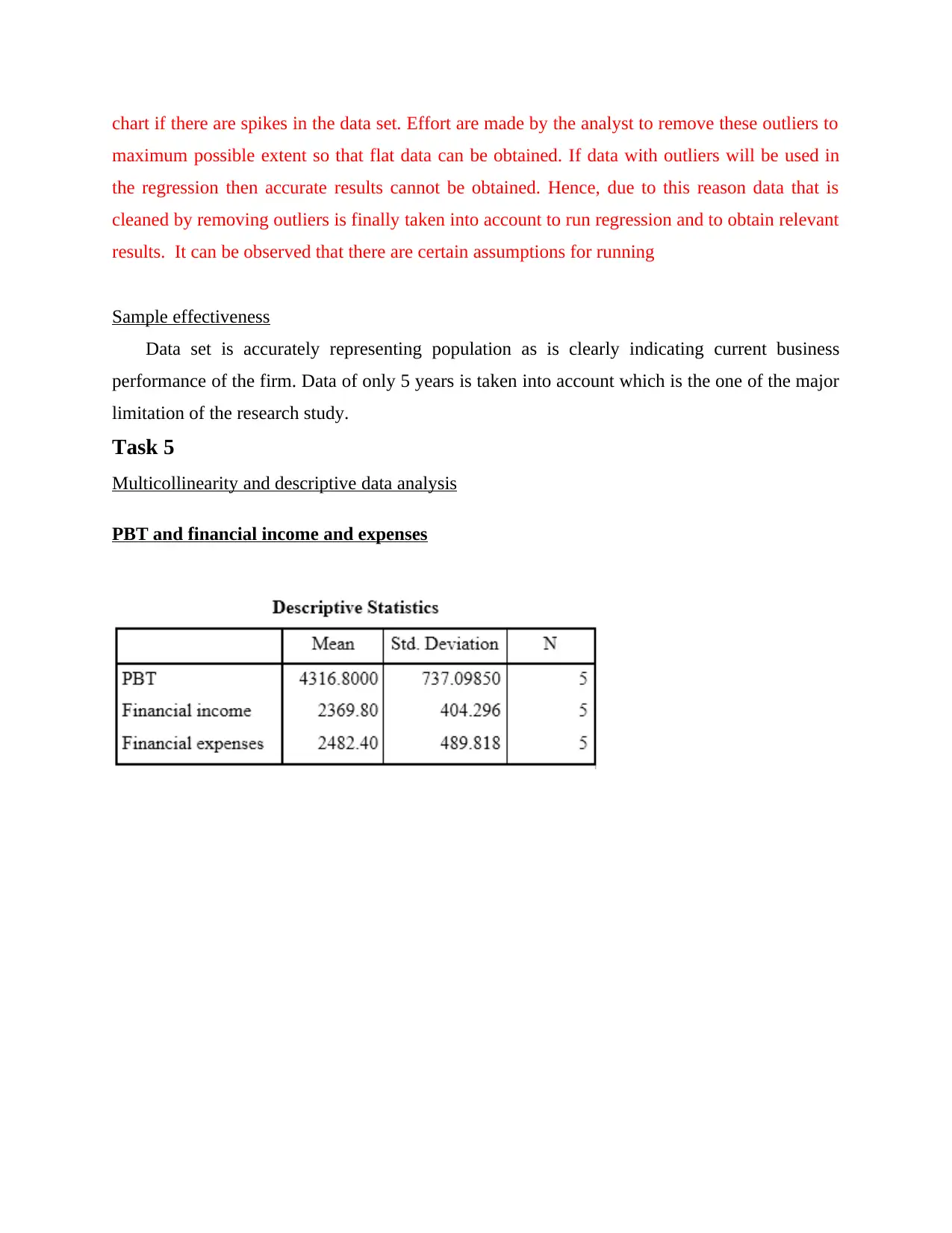

Multicollinearity and descriptive data analysis

PBT and financial income and expenses

maximum possible extent so that flat data can be obtained. If data with outliers will be used in

the regression then accurate results cannot be obtained. Hence, due to this reason data that is

cleaned by removing outliers is finally taken into account to run regression and to obtain relevant

results. It can be observed that there are certain assumptions for running

Sample effectiveness

Data set is accurately representing population as is clearly indicating current business

performance of the firm. Data of only 5 years is taken into account which is the one of the major

limitation of the research study.

Task 5

Multicollinearity and descriptive data analysis

PBT and financial income and expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation

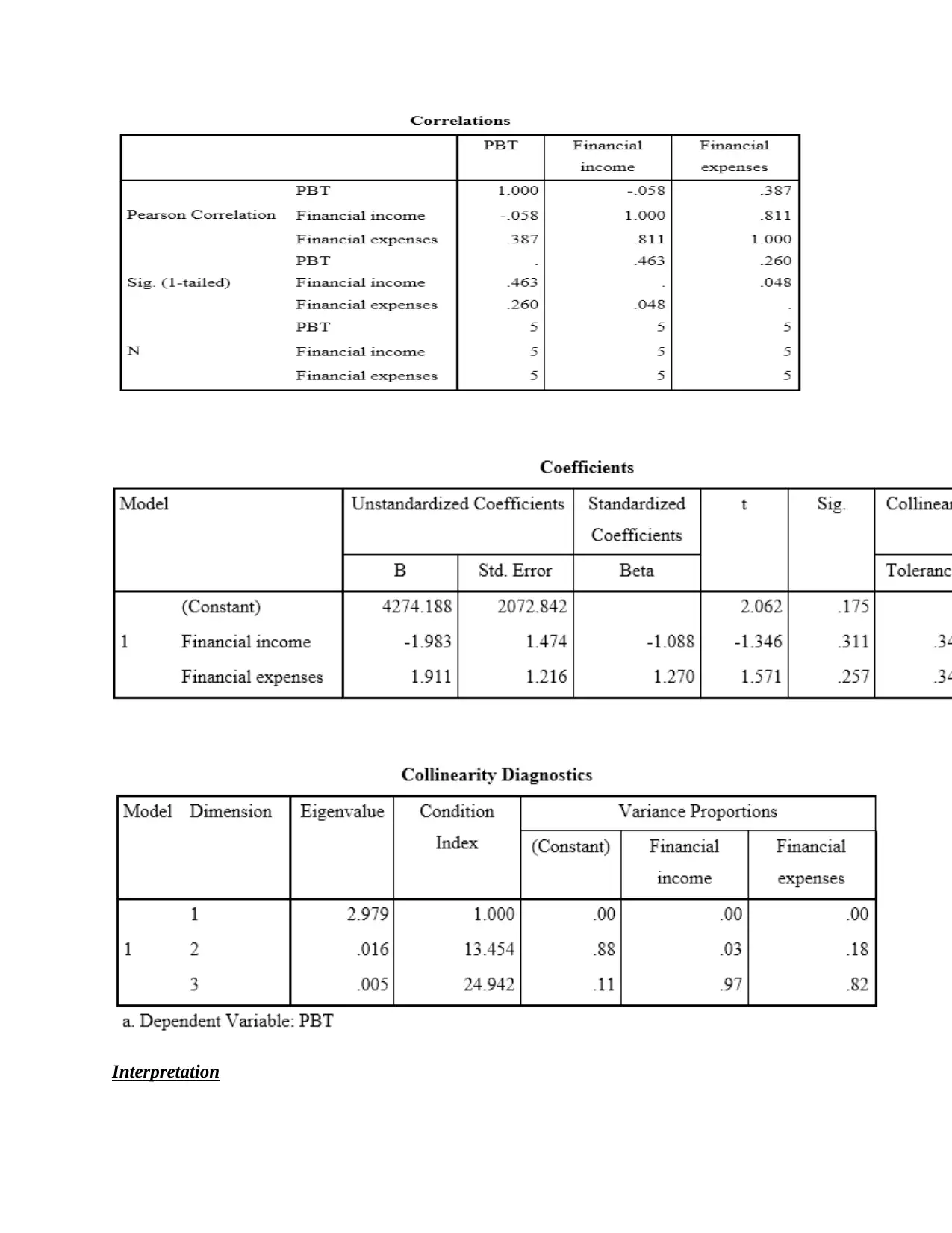

Problem of multicollinearity is find out in the solution that is given above. It can be

observed that value of VIF is below 10 as it can be seen that in case of financial income value of

VIF is 2.928 and in case of financial expenses value of VIF is 2.928 which is lower then 10.

Further, condition index value is 0.016 for financial income and 0.005 for financial expenses.

Value above 15 indicate multicollinearity problem and value above 30 reflect strong problem of

multicollinearity. In present case in the above tables it can be seen that value of condition index

for financial income is 13.45 and for financial expense is 24.94. Hence, in case of financial

income value is nearby to 15 and in case of financial expenses value is more then 15 which

reflect that there is problem of multicollinearity. Hence, it can be said that there is problem of

multicollinearity. Problem of multicollinearity comes in existence when multiple independent

variables are interrelated to each other and performance of one is affected by another one

(Regorz., 2020). Estimates made from the regression model in which multiple independent

variables are correlated accurate estimations can not be obtained. There may be multiple reasons

due to which multicollinearity is observed. Collinearity may occur between variables due to

inclusion of variable which is computed from other variables in the dataset. In order to remove

collinearity one of the corelated variable is removed from the model.

There is close relationship between financial income and expenses as correlation value is

0.811. Hence, if financial income will increase then financial expenses will also elevate. With

slight increase in financial income slight decline is observed in case of PBT as correlation value

is -0.058. In case of financial expenses and PBT correlation value is 0.387 which reflect that

there is moderate relationship between both variables. In case of financial income value of

statistic is (M = 2369, SD =404). On other hand, in case of financial expense value of statistic is

(M = 2482.40, SD =498.18).

observed that value of VIF is below 10 as it can be seen that in case of financial income value of

VIF is 2.928 and in case of financial expenses value of VIF is 2.928 which is lower then 10.

Further, condition index value is 0.016 for financial income and 0.005 for financial expenses.

Value above 15 indicate multicollinearity problem and value above 30 reflect strong problem of

multicollinearity. In present case in the above tables it can be seen that value of condition index

for financial income is 13.45 and for financial expense is 24.94. Hence, in case of financial

income value is nearby to 15 and in case of financial expenses value is more then 15 which

reflect that there is problem of multicollinearity. Hence, it can be said that there is problem of

multicollinearity. Problem of multicollinearity comes in existence when multiple independent

variables are interrelated to each other and performance of one is affected by another one

(Regorz., 2020). Estimates made from the regression model in which multiple independent

variables are correlated accurate estimations can not be obtained. There may be multiple reasons

due to which multicollinearity is observed. Collinearity may occur between variables due to

inclusion of variable which is computed from other variables in the dataset. In order to remove

collinearity one of the corelated variable is removed from the model.

There is close relationship between financial income and expenses as correlation value is

0.811. Hence, if financial income will increase then financial expenses will also elevate. With

slight increase in financial income slight decline is observed in case of PBT as correlation value

is -0.058. In case of financial expenses and PBT correlation value is 0.387 which reflect that

there is moderate relationship between both variables. In case of financial income value of

statistic is (M = 2369, SD =404). On other hand, in case of financial expense value of statistic is

(M = 2482.40, SD =498.18).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales revenue and COGS, SGA expenses, R&D and other operating expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

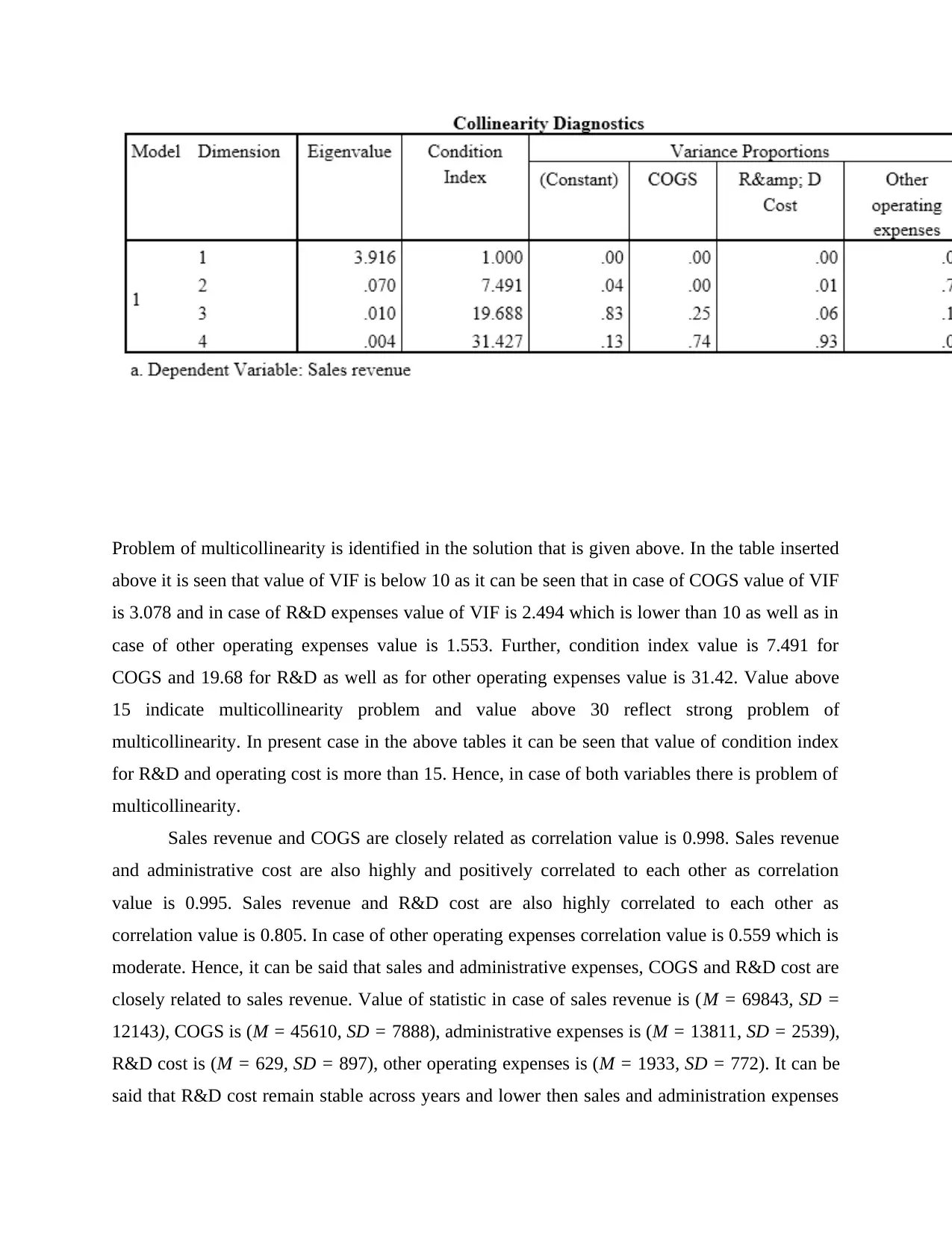

Problem of multicollinearity is identified in the solution that is given above. In the table inserted

above it is seen that value of VIF is below 10 as it can be seen that in case of COGS value of VIF

is 3.078 and in case of R&D expenses value of VIF is 2.494 which is lower than 10 as well as in

case of other operating expenses value is 1.553. Further, condition index value is 7.491 for

COGS and 19.68 for R&D as well as for other operating expenses value is 31.42. Value above

15 indicate multicollinearity problem and value above 30 reflect strong problem of

multicollinearity. In present case in the above tables it can be seen that value of condition index

for R&D and operating cost is more than 15. Hence, in case of both variables there is problem of

multicollinearity.

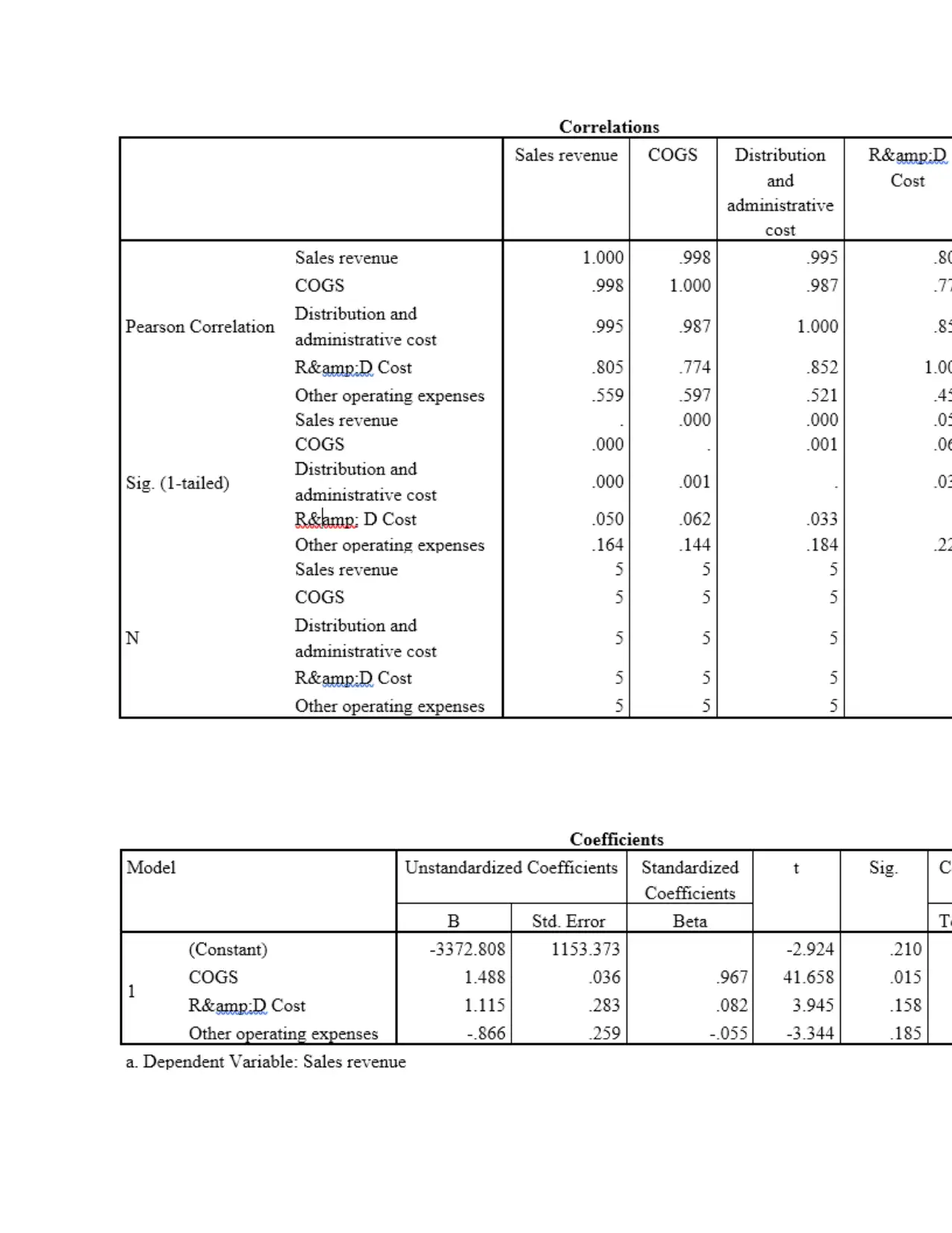

Sales revenue and COGS are closely related as correlation value is 0.998. Sales revenue

and administrative cost are also highly and positively correlated to each other as correlation

value is 0.995. Sales revenue and R&D cost are also highly correlated to each other as

correlation value is 0.805. In case of other operating expenses correlation value is 0.559 which is

moderate. Hence, it can be said that sales and administrative expenses, COGS and R&D cost are

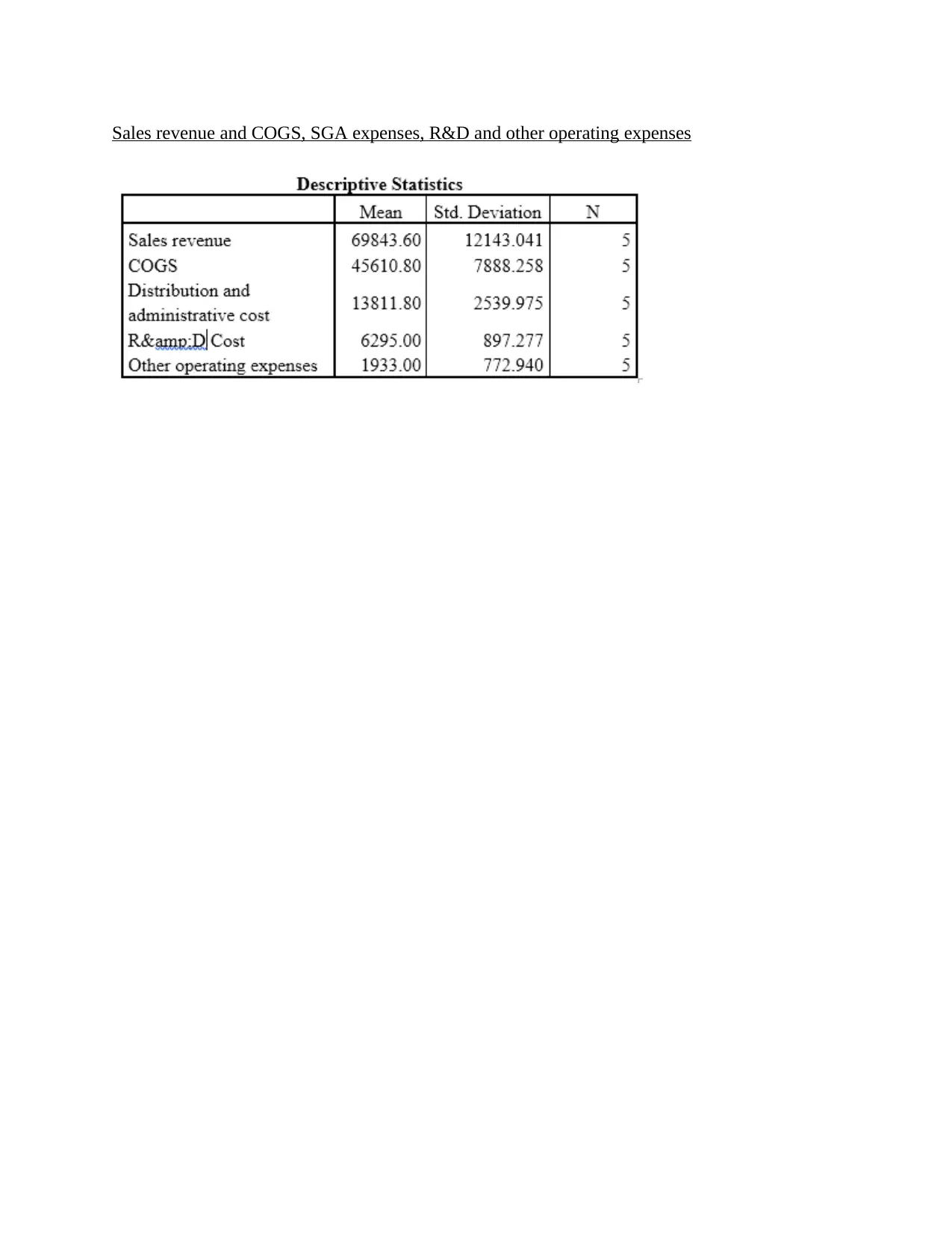

closely related to sales revenue. Value of statistic in case of sales revenue is (M = 69843, SD =

12143), COGS is (M = 45610, SD = 7888), administrative expenses is (M = 13811, SD = 2539),

R&D cost is (M = 629, SD = 897), other operating expenses is (M = 1933, SD = 772). It can be

said that R&D cost remain stable across years and lower then sales and administration expenses

above it is seen that value of VIF is below 10 as it can be seen that in case of COGS value of VIF

is 3.078 and in case of R&D expenses value of VIF is 2.494 which is lower than 10 as well as in

case of other operating expenses value is 1.553. Further, condition index value is 7.491 for

COGS and 19.68 for R&D as well as for other operating expenses value is 31.42. Value above

15 indicate multicollinearity problem and value above 30 reflect strong problem of

multicollinearity. In present case in the above tables it can be seen that value of condition index

for R&D and operating cost is more than 15. Hence, in case of both variables there is problem of

multicollinearity.

Sales revenue and COGS are closely related as correlation value is 0.998. Sales revenue

and administrative cost are also highly and positively correlated to each other as correlation

value is 0.995. Sales revenue and R&D cost are also highly correlated to each other as

correlation value is 0.805. In case of other operating expenses correlation value is 0.559 which is

moderate. Hence, it can be said that sales and administrative expenses, COGS and R&D cost are

closely related to sales revenue. Value of statistic in case of sales revenue is (M = 69843, SD =

12143), COGS is (M = 45610, SD = 7888), administrative expenses is (M = 13811, SD = 2539),

R&D cost is (M = 629, SD = 897), other operating expenses is (M = 1933, SD = 772). It can be

said that R&D cost remain stable across years and lower then sales and administration expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.