Stock Price Forecasting: An AI and Data Mining Approach Project

VerifiedAdded on 2020/03/16

|5

|1493

|94

Project

AI Summary

This project presents a prototype for predicting stock prices using data mining and artificial intelligence. The study focuses on neural networks and employs a decision tree categorizer to analyze historical stock data. The project utilizes the CRISP-DM model, examining stock data from a database and considering factors like company size and liquidity. The methodology involves data preparation, model construction with decision trees, and deployment for forecasting efficient trading decisions. The results highlight the limitations of the approach, particularly the impact of external factors like news and political events on stock price accuracy, and suggests future research directions that incorporate additional training methods and comprehensive aspects of the stock market.

Prediction of stock

prices using Data

Mining and Artificial

Intelligence

prices using Data

Mining and Artificial

Intelligence

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

In fiscal period progression, the forecast of stock prices is a demanding job. Currently, more number of

online software is used for purchasing and trading the market share but not for predicting the prices of

specific and meticulous shares. Hence, a prototype is proposed for learning the shares database to provide

the prophecies. This study is established on the basis of neural networks. A data mining method namely

decision tree categorizer is employed for making decisions associated with shares.

Keywords: AI, Data Mining, Decision Tree Categorizer, Forecast Stock arrival, Data Mining Techniques

1. Introduction

The sensible precision cannot be achieved easily in share market which is of non-statics nature. The

shareholders are searching for a technique to forecast the prices of stocks, precise stock, and correct

period for purchasing and trading the stocks. According to a research on the stock price prediction

techniques, the former methods of elemental and technological examination are used (Wu & Lin, 2006).

The data related to international and financial viable organization, drafts the trading procedures in this

elemental examination technique. Moreover, this technique can be appropriate for efficiently predicting

the prices of long-term shares alone.

The prime goal of this paper is to evaluate the chronological stock data by employing determination tree

method as one of the data mining technique for assisting the traders to be aware of the time to purchase

and trade the shares. The chronological stock data will be selected from millions of records of many

companies in the database and not on thousands of evidences.

2. Literature Review

According to the research by Wu and Lin (2006), in order to predict the stock prices, a filter condition is

applied and the method for grouping the exchange position possess only the previous data and not aims

on the future data.

In the model proposed by Wang and Chan (2006), a new determination prototype called the dual layer

partial determination tree is constructed by means of sequential topology for the purpose of forecasting

the stock prices. Based on the experimental outcomes of this research, the stock buying precision by using

this dual decision tree is efficient than the unsystematic buying.

In fiscal period progression, the forecast of stock prices is a demanding job. Currently, more number of

online software is used for purchasing and trading the market share but not for predicting the prices of

specific and meticulous shares. Hence, a prototype is proposed for learning the shares database to provide

the prophecies. This study is established on the basis of neural networks. A data mining method namely

decision tree categorizer is employed for making decisions associated with shares.

Keywords: AI, Data Mining, Decision Tree Categorizer, Forecast Stock arrival, Data Mining Techniques

1. Introduction

The sensible precision cannot be achieved easily in share market which is of non-statics nature. The

shareholders are searching for a technique to forecast the prices of stocks, precise stock, and correct

period for purchasing and trading the stocks. According to a research on the stock price prediction

techniques, the former methods of elemental and technological examination are used (Wu & Lin, 2006).

The data related to international and financial viable organization, drafts the trading procedures in this

elemental examination technique. Moreover, this technique can be appropriate for efficiently predicting

the prices of long-term shares alone.

The prime goal of this paper is to evaluate the chronological stock data by employing determination tree

method as one of the data mining technique for assisting the traders to be aware of the time to purchase

and trade the shares. The chronological stock data will be selected from millions of records of many

companies in the database and not on thousands of evidences.

2. Literature Review

According to the research by Wu and Lin (2006), in order to predict the stock prices, a filter condition is

applied and the method for grouping the exchange position possess only the previous data and not aims

on the future data.

In the model proposed by Wang and Chan (2006), a new determination prototype called the dual layer

partial determination tree is constructed by means of sequential topology for the purpose of forecasting

the stock prices. Based on the experimental outcomes of this research, the stock buying precision by using

this dual decision tree is efficient than the unsystematic buying.

Enke and Thawornwong (2005) proposed a method that incorporates data mining techniques and neural

system to forecast the stock prices. And the outcomes of this approach indicated that the neural system

prototypes used for prediction and categorization, proffers privileged turnovers beneath the similar

jeopardy revelation when contrasted with other prediction models.

The research conducted by Cao, Leggio, & Schniederjans (2003), is the distinction between the models

proposed by Fama & French (1993). This approach embeds the simulated neural system for the stock

price forecasting in Chinese share market.

3. Proposed Methodology

For constructing the prototype in order to determine the share prices by using the determination tree

method, the CRISP-DM (Cross-industry Standard Process for Data Mining) is employed. This model is

considered as a non-owner data mining prototype (Hajizadeh, Ardakani & Shahrabi, 2010). The CRISP-

DM model comprises the following steps:

The purpose and aim for mining the share value should be analyzed.

The structure of the gathered stock information must be examined.

The information utilized in the categorization prototype can be generated.

The methodology for constructing the data mining technique is selected.

By using the familiar estimation techniques, the prototype must be validated.

The constructed model is finally implemented in the share market in order to forecast the better

choice, i.e. either purchasing or trading the shares.

The purpose and aim of the constructed data mining model should be analyzed further.

The decision for evaluating the time for purchasing and trading the shares is provided by the

determination tree categorizer, which achieves the prime goal of building this model.

3.1. Comprehending the gathered information

Any stock exchange for example, X Stock Exchange (XSE) oracle database is considered. This database

comprises the historical stock prices of many companies for several consequent years. The final

resolution is to pick up any three companies in the stock exchange, since there are larger amount of

records. The organization selection depends on the factors that correspond to the size of the company and

liquidity inside the company. The selection factors include traded days, marketplace exploitation, yield

quotient, total number of traded stocks, and share values (Hazem, Bakry & Wael, 2010).

system to forecast the stock prices. And the outcomes of this approach indicated that the neural system

prototypes used for prediction and categorization, proffers privileged turnovers beneath the similar

jeopardy revelation when contrasted with other prediction models.

The research conducted by Cao, Leggio, & Schniederjans (2003), is the distinction between the models

proposed by Fama & French (1993). This approach embeds the simulated neural system for the stock

price forecasting in Chinese share market.

3. Proposed Methodology

For constructing the prototype in order to determine the share prices by using the determination tree

method, the CRISP-DM (Cross-industry Standard Process for Data Mining) is employed. This model is

considered as a non-owner data mining prototype (Hajizadeh, Ardakani & Shahrabi, 2010). The CRISP-

DM model comprises the following steps:

The purpose and aim for mining the share value should be analyzed.

The structure of the gathered stock information must be examined.

The information utilized in the categorization prototype can be generated.

The methodology for constructing the data mining technique is selected.

By using the familiar estimation techniques, the prototype must be validated.

The constructed model is finally implemented in the share market in order to forecast the better

choice, i.e. either purchasing or trading the shares.

The purpose and aim of the constructed data mining model should be analyzed further.

The decision for evaluating the time for purchasing and trading the shares is provided by the

determination tree categorizer, which achieves the prime goal of building this model.

3.1. Comprehending the gathered information

Any stock exchange for example, X Stock Exchange (XSE) oracle database is considered. This database

comprises the historical stock prices of many companies for several consequent years. The final

resolution is to pick up any three companies in the stock exchange, since there are larger amount of

records. The organization selection depends on the factors that correspond to the size of the company and

liquidity inside the company. The selection factors include traded days, marketplace exploitation, yield

quotient, total number of traded stocks, and share values (Hazem, Bakry & Wael, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

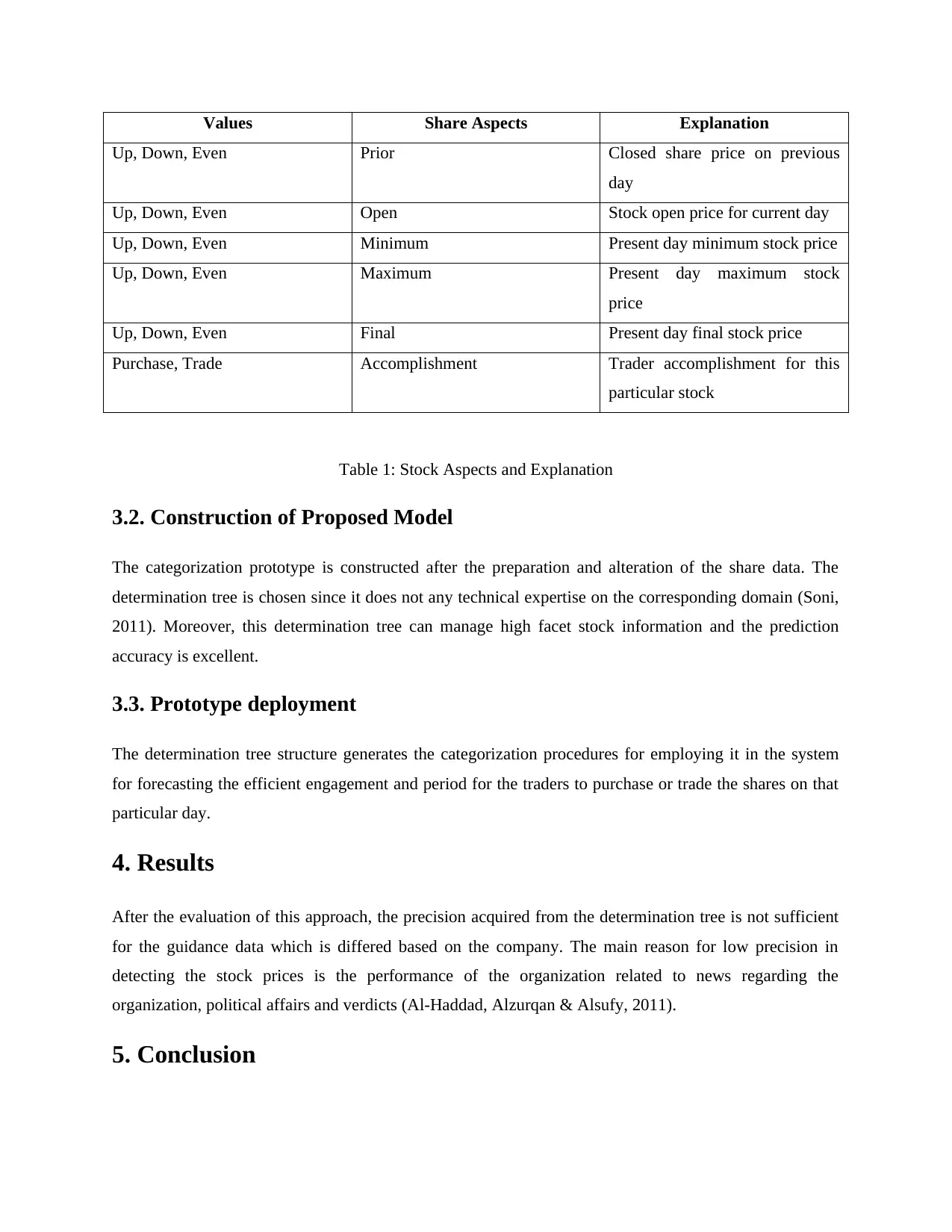

Values Share Aspects Explanation

Up, Down, Even Prior Closed share price on previous

day

Up, Down, Even Open Stock open price for current day

Up, Down, Even Minimum Present day minimum stock price

Up, Down, Even Maximum Present day maximum stock

price

Up, Down, Even Final Present day final stock price

Purchase, Trade Accomplishment Trader accomplishment for this

particular stock

Table 1: Stock Aspects and Explanation

3.2. Construction of Proposed Model

The categorization prototype is constructed after the preparation and alteration of the share data. The

determination tree is chosen since it does not any technical expertise on the corresponding domain (Soni,

2011). Moreover, this determination tree can manage high facet stock information and the prediction

accuracy is excellent.

3.3. Prototype deployment

The determination tree structure generates the categorization procedures for employing it in the system

for forecasting the efficient engagement and period for the traders to purchase or trade the shares on that

particular day.

4. Results

After the evaluation of this approach, the precision acquired from the determination tree is not sufficient

for the guidance data which is differed based on the company. The main reason for low precision in

detecting the stock prices is the performance of the organization related to news regarding the

organization, political affairs and verdicts (Al-Haddad, Alzurqan & Alsufy, 2011).

5. Conclusion

Up, Down, Even Prior Closed share price on previous

day

Up, Down, Even Open Stock open price for current day

Up, Down, Even Minimum Present day minimum stock price

Up, Down, Even Maximum Present day maximum stock

price

Up, Down, Even Final Present day final stock price

Purchase, Trade Accomplishment Trader accomplishment for this

particular stock

Table 1: Stock Aspects and Explanation

3.2. Construction of Proposed Model

The categorization prototype is constructed after the preparation and alteration of the share data. The

determination tree is chosen since it does not any technical expertise on the corresponding domain (Soni,

2011). Moreover, this determination tree can manage high facet stock information and the prediction

accuracy is excellent.

3.3. Prototype deployment

The determination tree structure generates the categorization procedures for employing it in the system

for forecasting the efficient engagement and period for the traders to purchase or trade the shares on that

particular day.

4. Results

After the evaluation of this approach, the precision acquired from the determination tree is not sufficient

for the guidance data which is differed based on the company. The main reason for low precision in

detecting the stock prices is the performance of the organization related to news regarding the

organization, political affairs and verdicts (Al-Haddad, Alzurqan & Alsufy, 2011).

5. Conclusion

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For the destined endeavors, more number of training methods like neural system, inherited procedures,

and company policies should be focused. To end up with, the reconsideration of the aspects impacting the

stock market characteristics such as company gossips, trading quantity, and monetary records should be

made. Since these aspects are highly responsible for affecting the stock prices, the future research can be

presumed by considering these aspects.

6. Reference

Wu, M.C., Lin, S.Y., & Lin, C.H. (2006). An effective application of decision tree to stock trading.

Expert Systems with Applications, 31(2), 270-274.

Wang, J.L., & Chan, S.H. (2006). Stock market trading rule discovery using two-layer bias decision tree.

Expert Systems with Applications, 30(4), 605-611.

Enke, D., & Thawornwong, S. (2005). The use of data mining and neural networks for forecasting stock

market returns. Expert Systems with Applications, 29(2), 927- 940.

Cao, Q., Leggio, K.B., & Schniederjans, M.J. (2005). A comparison between Fama and French’s model

and artificial neural networks in predicting the Chinese stock market. Computers & Operations

Research, 32 (3), 2499-2512.

Hajizadeh, E., Ardakani, H., & Shahrabi, J. (2010). Application of data mining techniques in stock

markets: A survey. Journal of Economics and International Finance, 2(7), 109-118.

Soni, S. (2011). Applications of ANNs in Stock Market Prediction: A Survey. International Journal of

Computer Science & Engineering Technology (IJCSET), 2(3), 71-83.

Al-Haddad, W., Alzurqan, S., & Alsufy, S. (2011). The Effect of Corporate Governance on the

Performance of Jordanian Industrial Companies: An empirical study on Amman Stock Exchange.

International Journal of Humanities and Social Science, 1(4), 240-267.

Hazem, M., Bakry, E., & Wael, A. (2010). Fast Forecasting of Stock Market Prices by using New High

Speed Time Delay Neural Networks. International Journal of Computer and Information

Engineering, 4(2), 138-144.

and company policies should be focused. To end up with, the reconsideration of the aspects impacting the

stock market characteristics such as company gossips, trading quantity, and monetary records should be

made. Since these aspects are highly responsible for affecting the stock prices, the future research can be

presumed by considering these aspects.

6. Reference

Wu, M.C., Lin, S.Y., & Lin, C.H. (2006). An effective application of decision tree to stock trading.

Expert Systems with Applications, 31(2), 270-274.

Wang, J.L., & Chan, S.H. (2006). Stock market trading rule discovery using two-layer bias decision tree.

Expert Systems with Applications, 30(4), 605-611.

Enke, D., & Thawornwong, S. (2005). The use of data mining and neural networks for forecasting stock

market returns. Expert Systems with Applications, 29(2), 927- 940.

Cao, Q., Leggio, K.B., & Schniederjans, M.J. (2005). A comparison between Fama and French’s model

and artificial neural networks in predicting the Chinese stock market. Computers & Operations

Research, 32 (3), 2499-2512.

Hajizadeh, E., Ardakani, H., & Shahrabi, J. (2010). Application of data mining techniques in stock

markets: A survey. Journal of Economics and International Finance, 2(7), 109-118.

Soni, S. (2011). Applications of ANNs in Stock Market Prediction: A Survey. International Journal of

Computer Science & Engineering Technology (IJCSET), 2(3), 71-83.

Al-Haddad, W., Alzurqan, S., & Alsufy, S. (2011). The Effect of Corporate Governance on the

Performance of Jordanian Industrial Companies: An empirical study on Amman Stock Exchange.

International Journal of Humanities and Social Science, 1(4), 240-267.

Hazem, M., Bakry, E., & Wael, A. (2010). Fast Forecasting of Stock Market Prices by using New High

Speed Time Delay Neural Networks. International Journal of Computer and Information

Engineering, 4(2), 138-144.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.