ITC516: Data Mining and Visualization Business Case Analysis I

VerifiedAdded on 2020/03/23

|12

|1608

|142

Homework Assignment

AI Summary

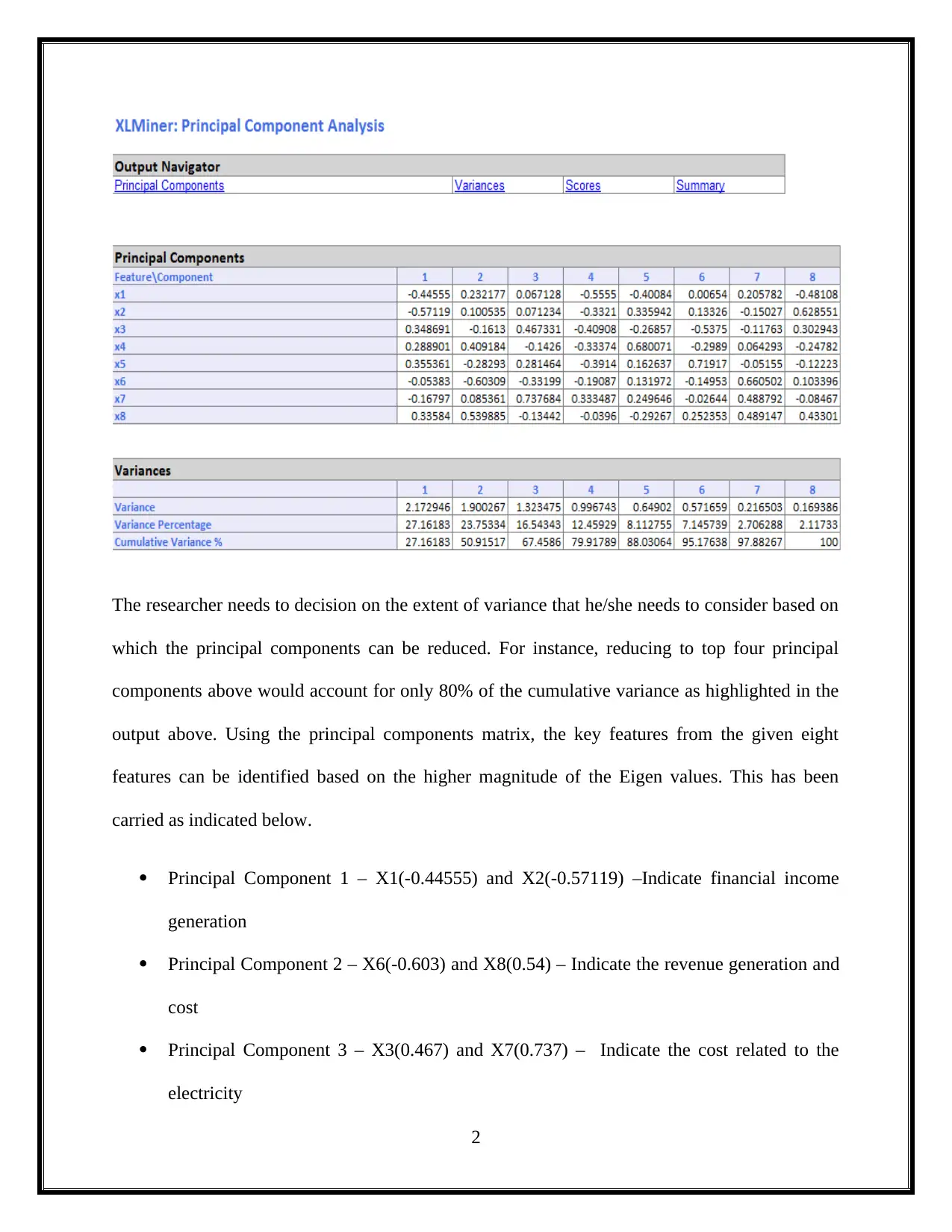

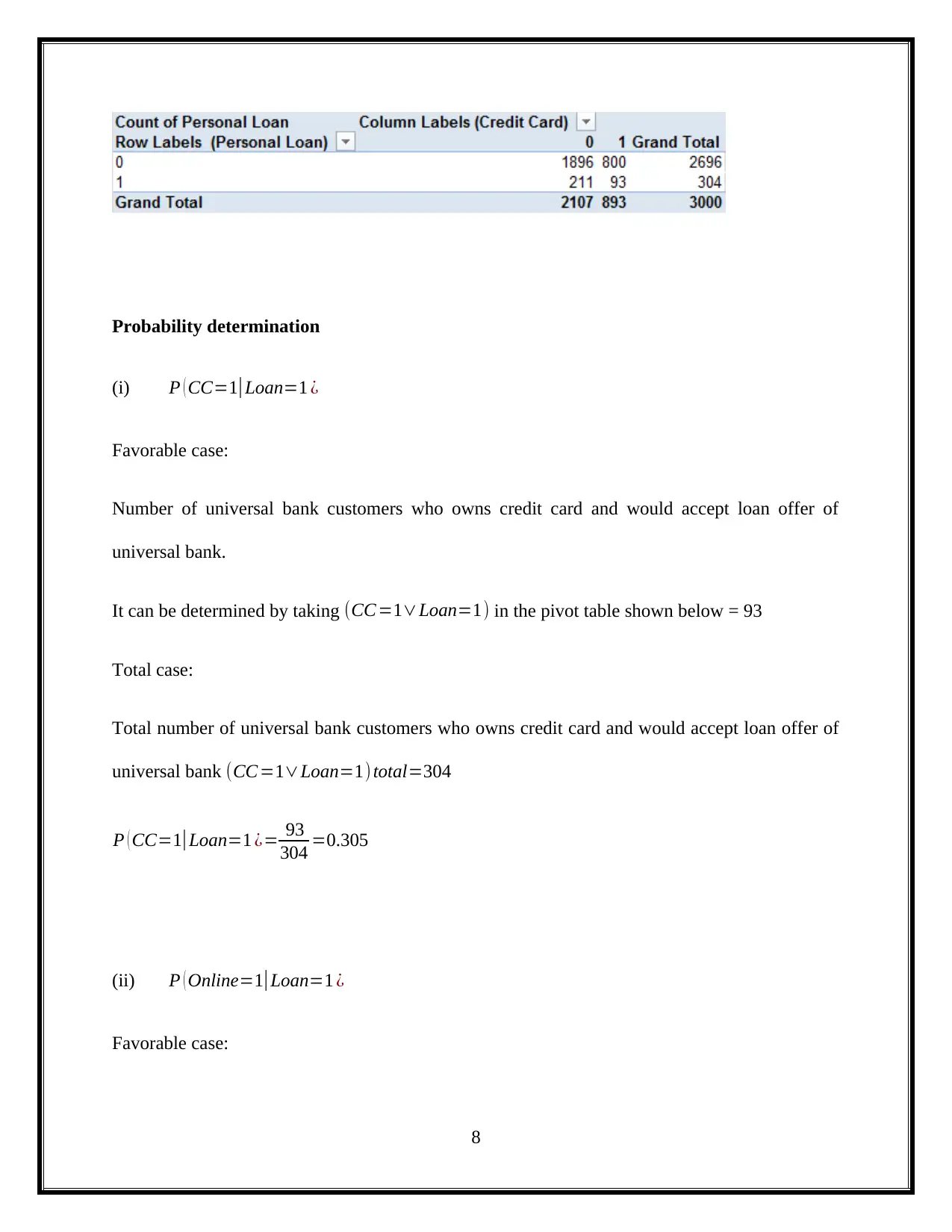

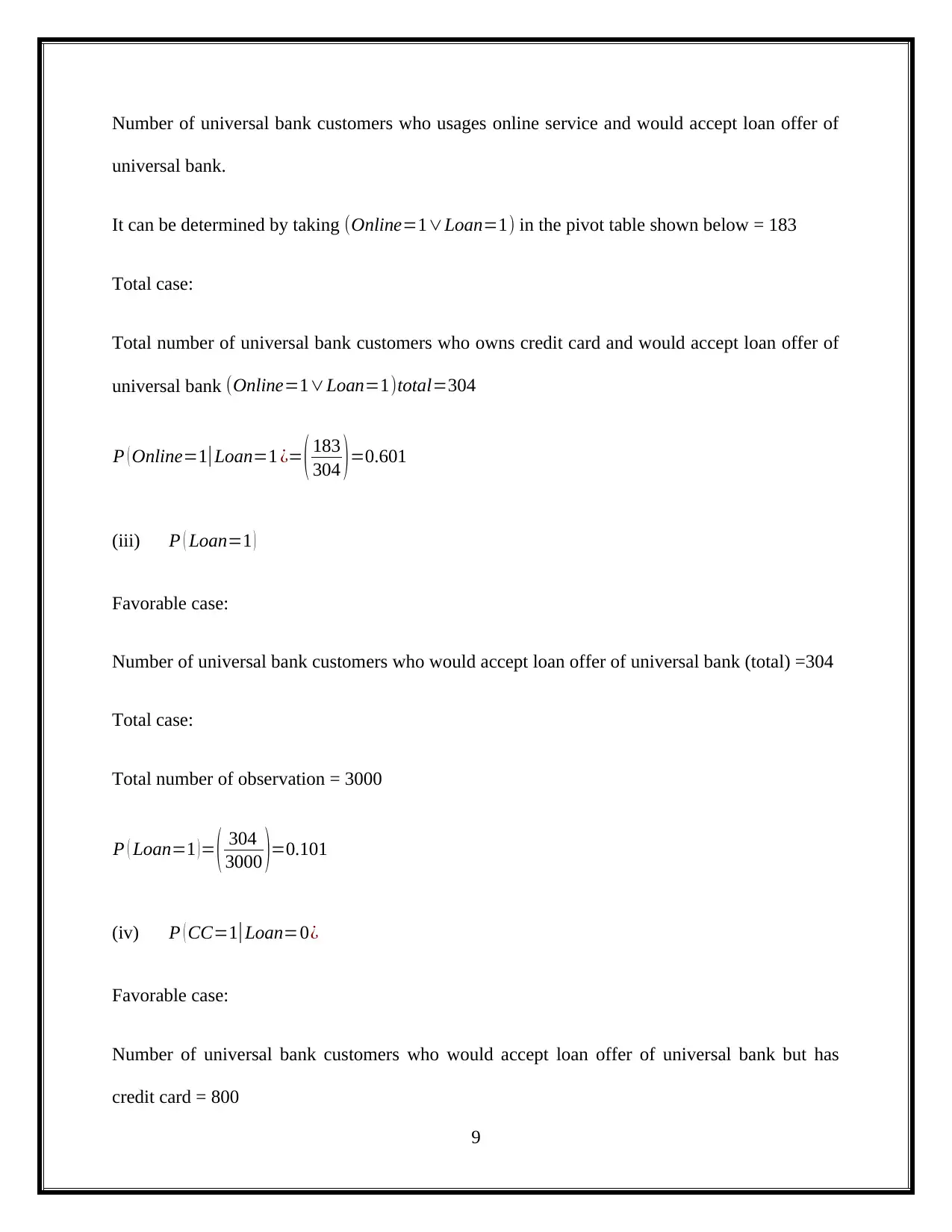

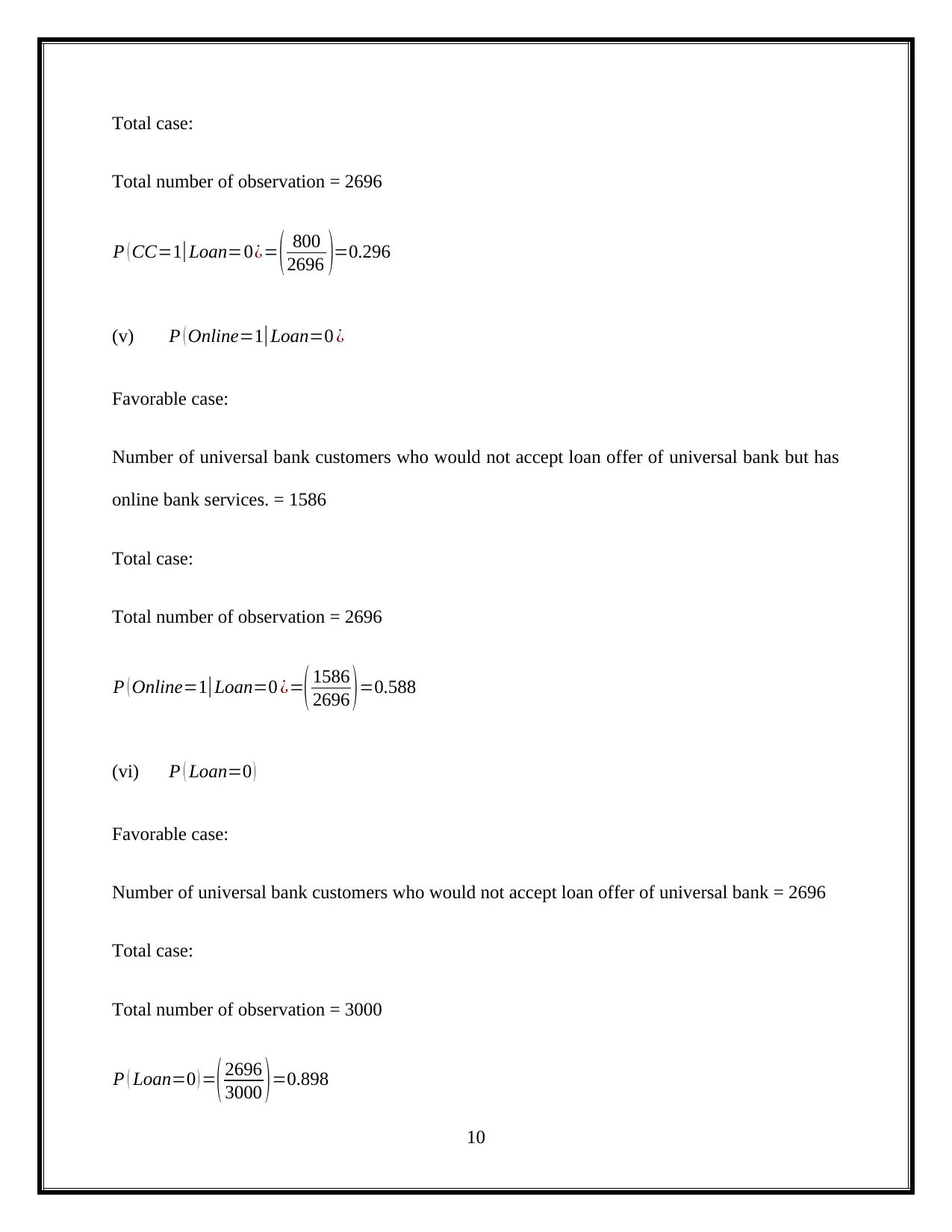

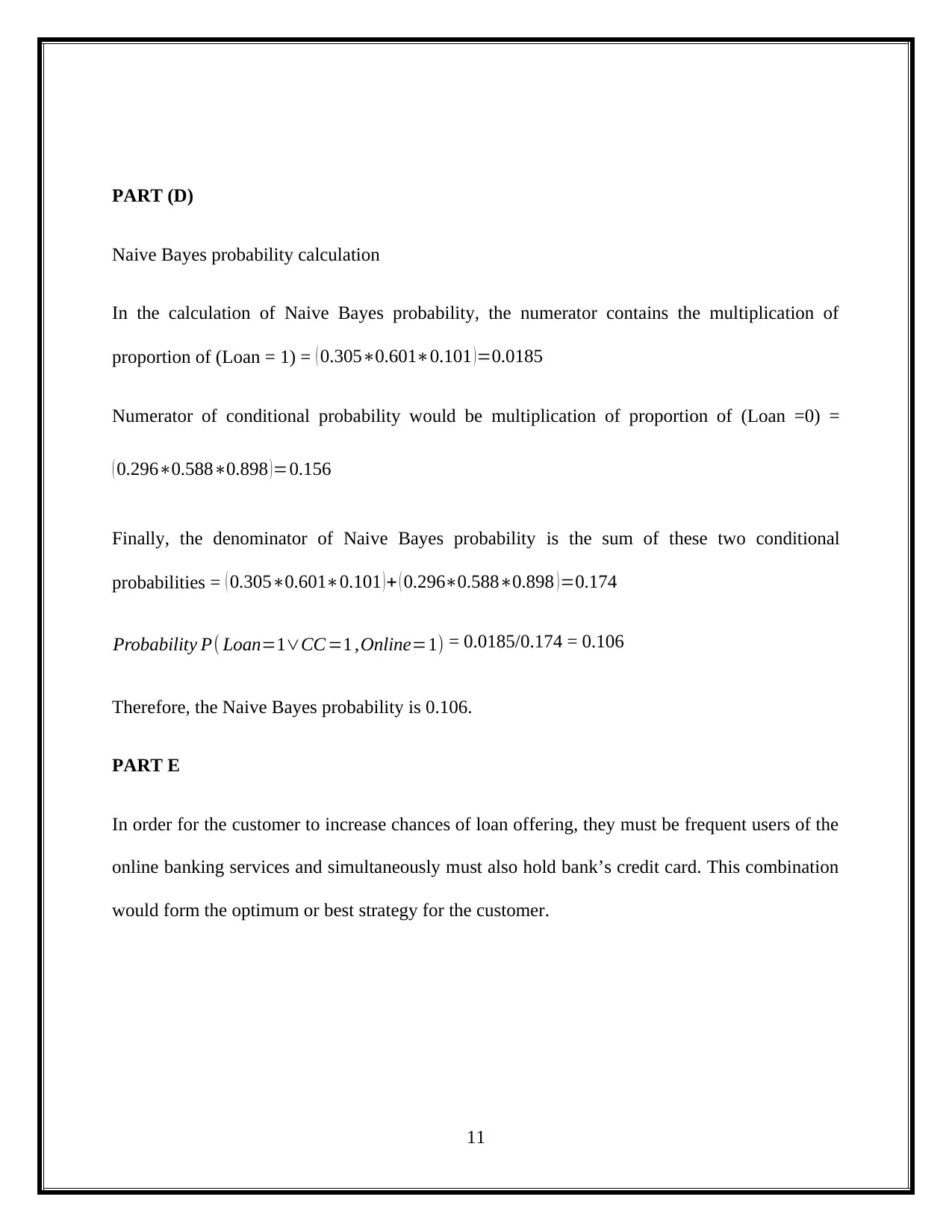

This document provides a comprehensive solution to a data mining assignment, addressing key concepts in business intelligence. It begins with an analysis of Principal Component Analysis (PCA), detailing the principal component matrix, variance, and feature selection for US utilities data. The solution explores the advantages and disadvantages of PCA. Subsequently, the assignment delves into a loan acceptance case study using a dataset of 5000 observations. It includes pivot table analysis to determine probabilities related to loan acceptance based on online banking usage and credit card ownership. The solution also calculates probabilities using Naive Bayes and concludes with a strategy for customers to increase their chances of loan approval.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.