Data Mining Assignment: Universal Bank and Customer Analysis

VerifiedAdded on 2020/04/07

|10

|1148

|43

Homework Assignment

AI Summary

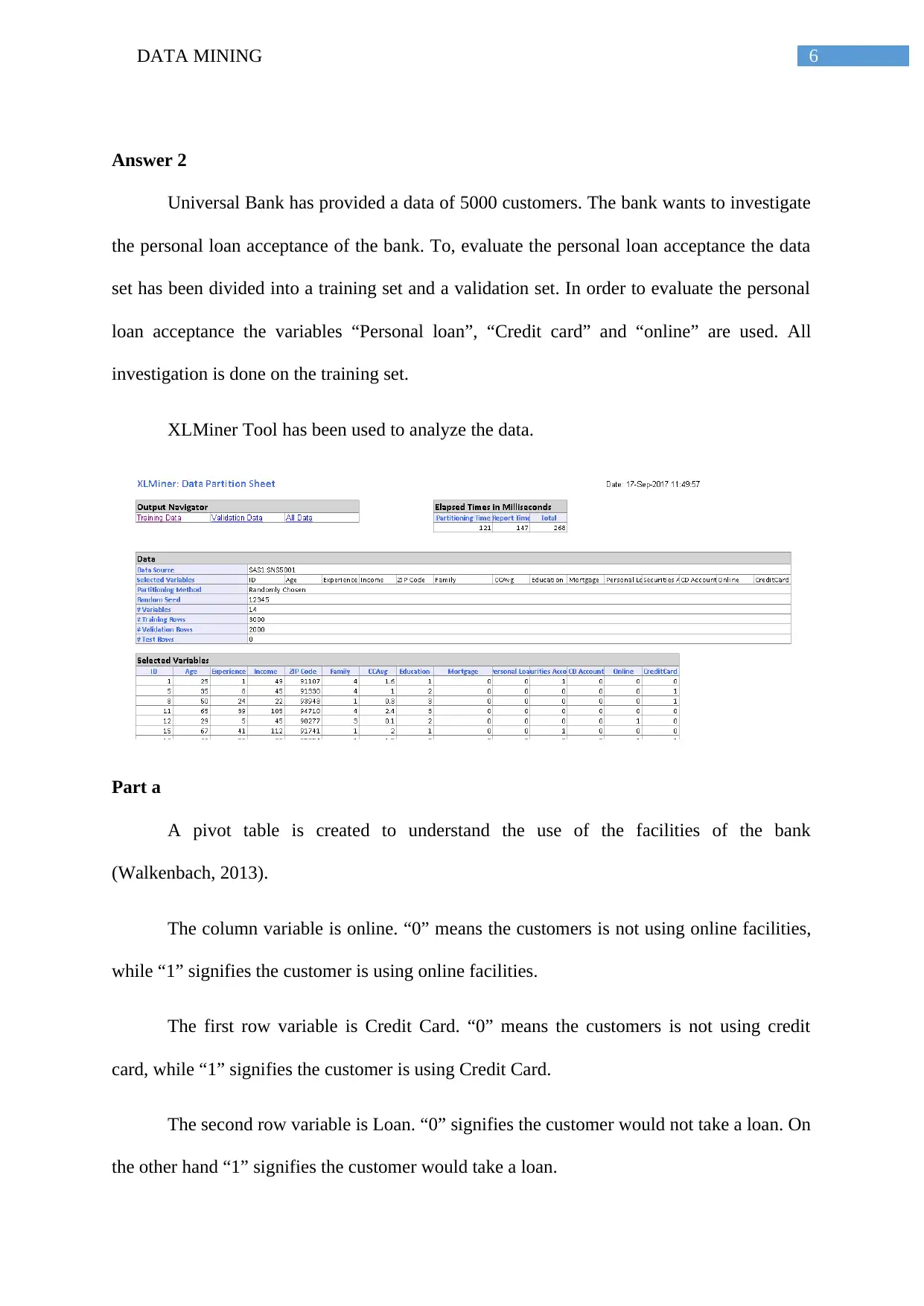

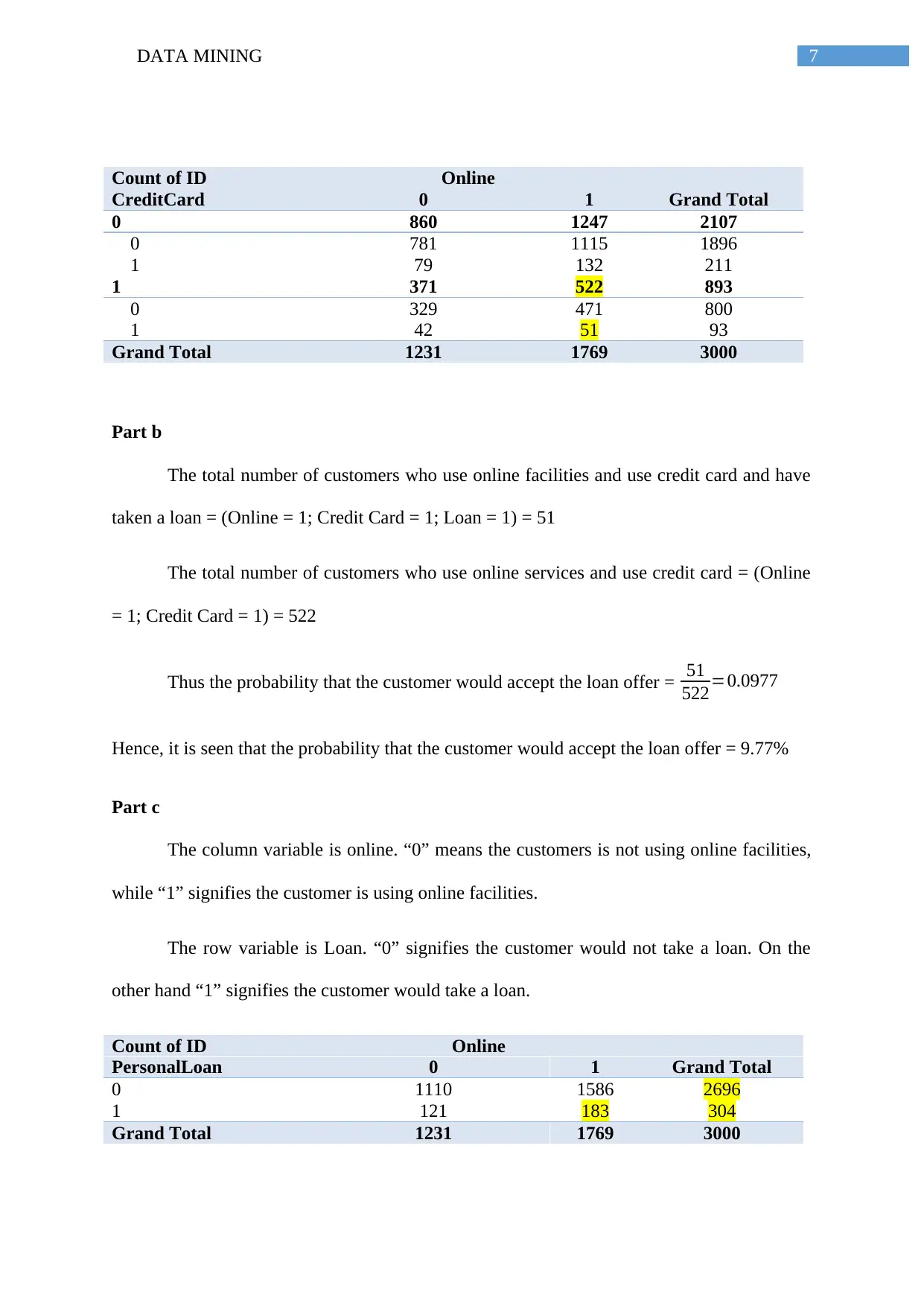

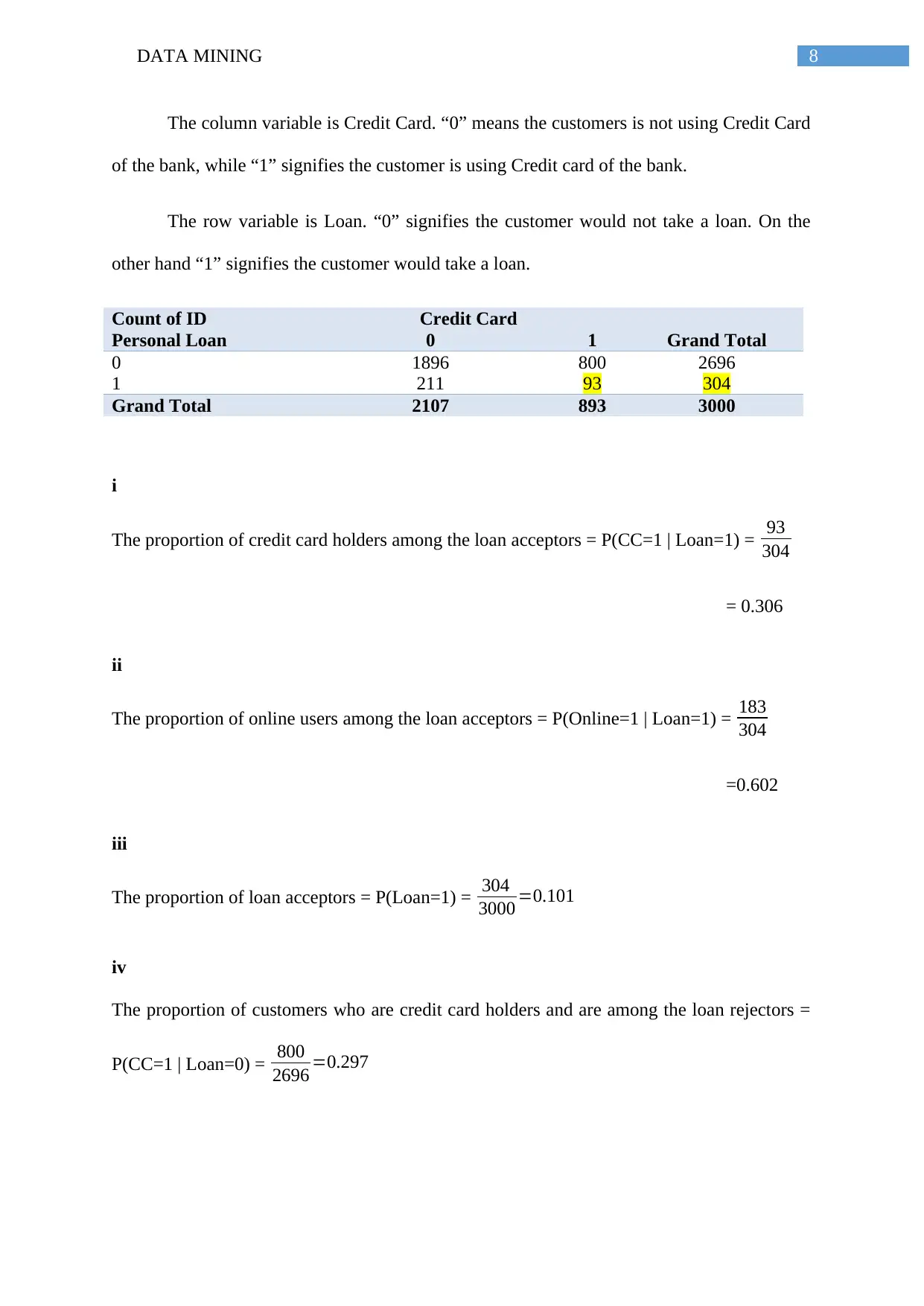

This data mining assignment analyzes data from Universal Bank using PCA (Principal Component Analysis) and pivot tables to assess customer behavior regarding loan acceptance. The first part of the assignment focuses on PCA, identifying key components like financial and operational performance of utilities, and discussing the need for data normalization. The second part involves analyzing customer data to evaluate personal loan acceptance, using variables like 'Personal loan', 'Credit card', and 'online' within XLMiner. The solution creates pivot tables to determine probabilities related to loan acceptance based on online facility usage and credit card ownership, calculating conditional probabilities and proportions for various customer segments. The analysis includes detailed calculations of probabilities, such as the likelihood of a customer accepting a loan given they use online services and have a credit card, and concludes with recommendations for loan eligibility based on customer behavior. The assignment references relevant sources to support its findings.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.