BUS0002: Report on Data Analysis and British Airways Financials

VerifiedAdded on 2023/01/18

|14

|3670

|54

Report

AI Summary

This report delves into the application of information and data analysis in organizational decision-making. It begins by comparing qualitative and quantitative data, horizontal and vertical analysis, and statistical versus big data. The report emphasizes the importance of data quality in financial statements, highlighting its impact on decision-making, compliance, and productivity. The second part of the report presents a case study of British Airways, analyzing its fleet composition, evaluating its financial performance using ratios like ROCE, ROE, and the current ratio, and discussing associated risk factors. The analysis reveals insights into British Airways' financial health and operational efficiency, providing a comprehensive overview of its performance and the factors influencing it.

BUS0002 Using

Information

Information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Assessment Part 1............................................................................................................................1

Comparison..................................................................................................................................1

Explaining ‘data quality’ and its importance in financial statements..........................................2

Assessment Part 2............................................................................................................................3

Analysis the fleet table.................................................................................................................3

Evaluating performance of British Airways Group using ratios.................................................5

Discussing risk factors.................................................................................................................7

Commenting on British Airways’ revenue..................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Assessment Part 1............................................................................................................................1

Comparison..................................................................................................................................1

Explaining ‘data quality’ and its importance in financial statements..........................................2

Assessment Part 2............................................................................................................................3

Analysis the fleet table.................................................................................................................3

Evaluating performance of British Airways Group using ratios.................................................5

Discussing risk factors.................................................................................................................7

Commenting on British Airways’ revenue..................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Using information is a process of using the data whether raw or processed to analyse its

elements in order to get desired results (Bloom and et.al., 2017). It is a concept in which assessor

or investigator uses the data available to develop conclusions (Bzdok, Altman and Krzywinski,

2018). Main aim of this report is to investigate various types of data and their applications in

making various organisational decisions. The present report is classified into two sections. The

first section will compare various statistical theories which are quantitative and qualitative,

horizontal and vertical analysis and statistical and big data. Besides which concept of data

quality is also assessed along with its importance. In the second section of the report, a case

study of British airways is assessed in order to evaluate its financial performance.

Assessment Part 1

Comparison

a) Qualitative and Quantitative data

Qualitative data is the information about features and qualities which cannot be measured

and is collected with the aim of understanding human behaviour (Chevalier and Kashyap, 2019).

This type of data is collected by an investigator through observations and interviews which is

further analysed using thematic analysis. This data follows a subjective approach by which

unstructured data is collected to get the outcome of high level of understanding. The only

drawback in this data is that it is collected against a small sample of representatives.

On the other hand, quantitative is the information about the quantities which can be both

measured and presented numerically (Koutras, Koutras and Yalcin, 2016). In case of quantitative

data, accuracy level is comparatively high as it is structurally collected from a large number of

representatives. An investigator uses objective approach (surveys) to collect this type of data

which is further analysed using statistical methods of descriptive and inferential statistics. This

data is limited due to its complexity of methods which requires statistical skills.

b) Horizontal and Vertical Analysis (under the subject of trend analysis)

Horizontal analysis is a technique to analyse the trend in financial statements of organisation

by comparing current year statements from historical statements. These financial statements

usually include income statement, balance sheet and cash flow statement (Nisar, Prabhakar and

Strakova, 2019). Under this technique, a financial statement is analysed in which one year is

1

Using information is a process of using the data whether raw or processed to analyse its

elements in order to get desired results (Bloom and et.al., 2017). It is a concept in which assessor

or investigator uses the data available to develop conclusions (Bzdok, Altman and Krzywinski,

2018). Main aim of this report is to investigate various types of data and their applications in

making various organisational decisions. The present report is classified into two sections. The

first section will compare various statistical theories which are quantitative and qualitative,

horizontal and vertical analysis and statistical and big data. Besides which concept of data

quality is also assessed along with its importance. In the second section of the report, a case

study of British airways is assessed in order to evaluate its financial performance.

Assessment Part 1

Comparison

a) Qualitative and Quantitative data

Qualitative data is the information about features and qualities which cannot be measured

and is collected with the aim of understanding human behaviour (Chevalier and Kashyap, 2019).

This type of data is collected by an investigator through observations and interviews which is

further analysed using thematic analysis. This data follows a subjective approach by which

unstructured data is collected to get the outcome of high level of understanding. The only

drawback in this data is that it is collected against a small sample of representatives.

On the other hand, quantitative is the information about the quantities which can be both

measured and presented numerically (Koutras, Koutras and Yalcin, 2016). In case of quantitative

data, accuracy level is comparatively high as it is structurally collected from a large number of

representatives. An investigator uses objective approach (surveys) to collect this type of data

which is further analysed using statistical methods of descriptive and inferential statistics. This

data is limited due to its complexity of methods which requires statistical skills.

b) Horizontal and Vertical Analysis (under the subject of trend analysis)

Horizontal analysis is a technique to analyse the trend in financial statements of organisation

by comparing current year statements from historical statements. These financial statements

usually include income statement, balance sheet and cash flow statement (Nisar, Prabhakar and

Strakova, 2019). Under this technique, a financial statement is analysed in which one year is

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered as a base and then all other years are compared to that base year in order to analyse

the trend of increase and decrease. By using this technique, factors such as seasonality and

others can be determined due to which trends of financial statement are changing. This technique

is often used to manipulate the results in order to make the current year revenue better due to

which this technique is not suitable for analysing the growth but sure is useful for analysing

trend.

On the contrary, vertical analysis is the technique of trend analysis in which evaluation is

done of a single year (time period) only. Under this technique, an element of the financial

statement is considered as a base and then all other elements of the statement are compared to

that base. For example, revenue of the income statement is considered as base (100%) and then

other elements such as cost of goods sold and expenses are compared to that base in order to

analyse the trend of increase and decrease.

c) Statistical and Big data

Statistical data is a structured data which is first collected and then presented using statistics

techniques of descriptive and inferential statistics. This type of data is easy to understand and

conclude. This data helps in easy analysing the results (Puri and Sengupta, 2018) (Venkatesan,

2019).

Big data refers to the immense volume of data which is unstructured and hard to analyse to

conclude any results. This data is collected over a large period of time and it is important to

analyse this kind of data before getting any insights.

Explaining ‘data quality’ and its importance in financial statements

Data quality is the concept of controlling the planning and implementation of quality

management techniques on the data in order to ensure suitability of the data. A data is considered

of high quality, if it fits for the intended purpose of use (Walker, Michailov and Trukhanov,

2019).

To develop financial statements, it is important to have a quality data so that effective and

accurate financial statements can be developed. There are various arguments which can reflect

the importance of data quality in financial statements. These arguments are:

If the data in financial statements of high quality, then organisation can make effective

decisions. The better the data quality in financial statements is, the more confidence can users of

2

the trend of increase and decrease. By using this technique, factors such as seasonality and

others can be determined due to which trends of financial statement are changing. This technique

is often used to manipulate the results in order to make the current year revenue better due to

which this technique is not suitable for analysing the growth but sure is useful for analysing

trend.

On the contrary, vertical analysis is the technique of trend analysis in which evaluation is

done of a single year (time period) only. Under this technique, an element of the financial

statement is considered as a base and then all other elements of the statement are compared to

that base. For example, revenue of the income statement is considered as base (100%) and then

other elements such as cost of goods sold and expenses are compared to that base in order to

analyse the trend of increase and decrease.

c) Statistical and Big data

Statistical data is a structured data which is first collected and then presented using statistics

techniques of descriptive and inferential statistics. This type of data is easy to understand and

conclude. This data helps in easy analysing the results (Puri and Sengupta, 2018) (Venkatesan,

2019).

Big data refers to the immense volume of data which is unstructured and hard to analyse to

conclude any results. This data is collected over a large period of time and it is important to

analyse this kind of data before getting any insights.

Explaining ‘data quality’ and its importance in financial statements

Data quality is the concept of controlling the planning and implementation of quality

management techniques on the data in order to ensure suitability of the data. A data is considered

of high quality, if it fits for the intended purpose of use (Walker, Michailov and Trukhanov,

2019).

To develop financial statements, it is important to have a quality data so that effective and

accurate financial statements can be developed. There are various arguments which can reflect

the importance of data quality in financial statements. These arguments are:

If the data in financial statements of high quality, then organisation can make effective

decisions. The better the data quality in financial statements is, the more confidence can users of

2

financial statements can have which will mitigate the risk of unreliable outcome; and decisions

can be made without any guess work.

Another importance of data quality in financial statement is compliance. Every

organisation has to fulfil some compliance of international and national regulations against the

development of financial statements so that users of that statements can be fully aware of

position of the organisation. If the information in financial statement has bad quality due to

which its users has to suffer, then the company may need to pay penalties. In order to ignore

these penalties, it is important to have quality data in financial statements of the organisation.

Productivity of an organisation also enhances due to quality data of an organisation. If the

data in financial statements has bad quality, then staff of the organisation has to spend their time

in resolving the issues in financial statements from which productivity will be reduced. If the

financial statements have quality data, then this time of rectifying the errors can be minimised

and productivity of employees will be automatically enhanced (Yan and et.al., 2017).

Another importance of quality data in financial statements is avoiding the situation of

missed opportunity. It is evident that better analysing of financial reports can result in various

opportunities by analysing the future trends and threats. But if the competitors of an organisation

are abler to analyse their financial statements effectively then the organisation will miss various

opportunities. But if the organisation treats its data as an asset and ensure high quality in it then

the situation of missed opportunity can easily be evaded.

All the above arguments make it clear and evident that quality data plays an important role

in developing effective and accurate financial statements which can be used by an organisation in

making decisions and enhancing productivity of their employees.

Assessment Part 2

Analysis the fleet table

a)

“Airbus A320” aircraft type had the largest fleet as at December 2017 with total of 67

number of aircrafts. Among these 67 aircrafts, 40 were recorded as fixed assets on balance sheet

and 27 were still recorded as operating leases off the balance sheet.

b)

3

can be made without any guess work.

Another importance of data quality in financial statement is compliance. Every

organisation has to fulfil some compliance of international and national regulations against the

development of financial statements so that users of that statements can be fully aware of

position of the organisation. If the information in financial statement has bad quality due to

which its users has to suffer, then the company may need to pay penalties. In order to ignore

these penalties, it is important to have quality data in financial statements of the organisation.

Productivity of an organisation also enhances due to quality data of an organisation. If the

data in financial statements has bad quality, then staff of the organisation has to spend their time

in resolving the issues in financial statements from which productivity will be reduced. If the

financial statements have quality data, then this time of rectifying the errors can be minimised

and productivity of employees will be automatically enhanced (Yan and et.al., 2017).

Another importance of quality data in financial statements is avoiding the situation of

missed opportunity. It is evident that better analysing of financial reports can result in various

opportunities by analysing the future trends and threats. But if the competitors of an organisation

are abler to analyse their financial statements effectively then the organisation will miss various

opportunities. But if the organisation treats its data as an asset and ensure high quality in it then

the situation of missed opportunity can easily be evaded.

All the above arguments make it clear and evident that quality data plays an important role

in developing effective and accurate financial statements which can be used by an organisation in

making decisions and enhancing productivity of their employees.

Assessment Part 2

Analysis the fleet table

a)

“Airbus A320” aircraft type had the largest fleet as at December 2017 with total of 67

number of aircrafts. Among these 67 aircrafts, 40 were recorded as fixed assets on balance sheet

and 27 were still recorded as operating leases off the balance sheet.

b)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

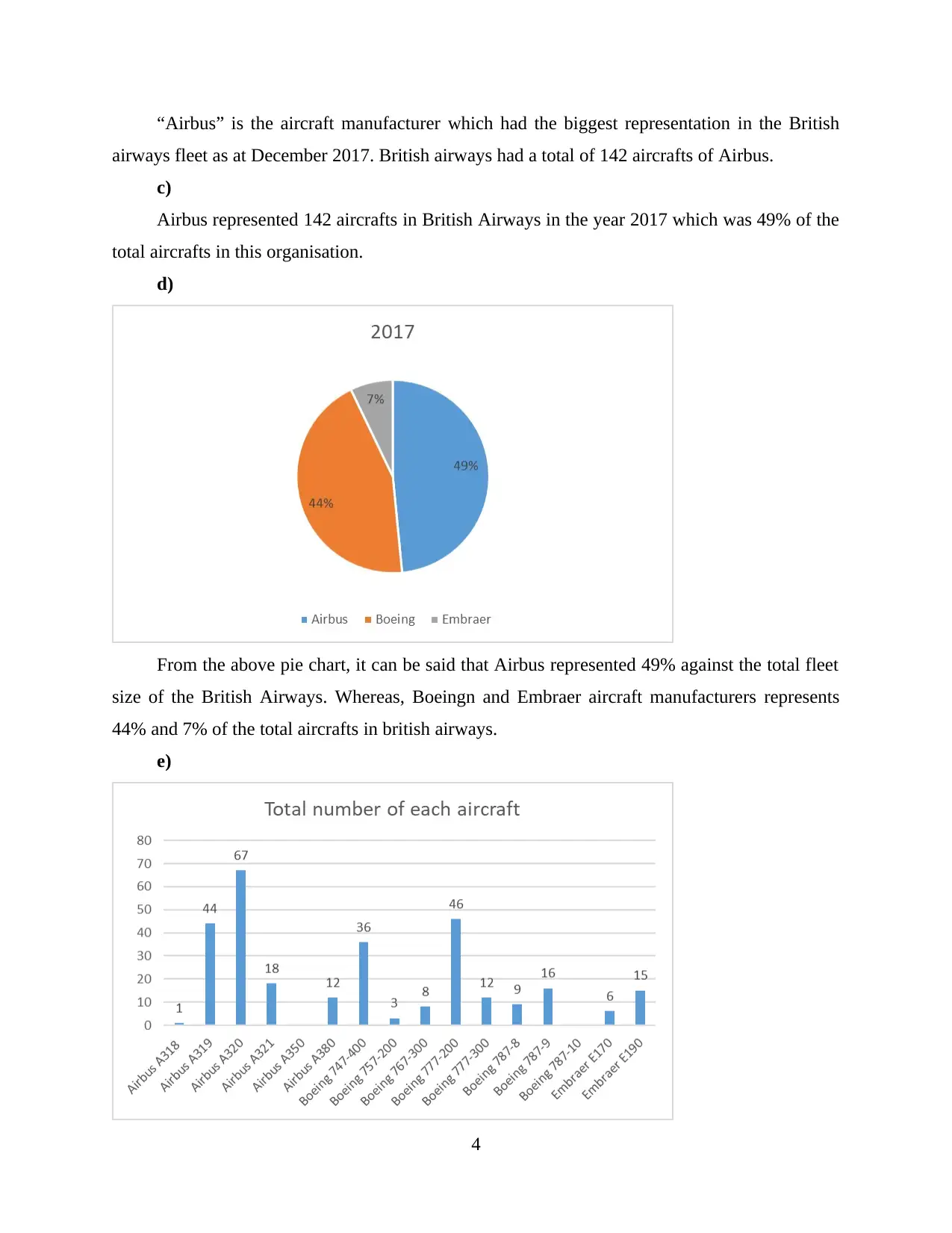

“Airbus” is the aircraft manufacturer which had the biggest representation in the British

airways fleet as at December 2017. British airways had a total of 142 aircrafts of Airbus.

c)

Airbus represented 142 aircrafts in British Airways in the year 2017 which was 49% of the

total aircrafts in this organisation.

d)

From the above pie chart, it can be said that Airbus represented 49% against the total fleet

size of the British Airways. Whereas, Boeingn and Embraer aircraft manufacturers represents

44% and 7% of the total aircrafts in british airways.

e)

4

airways fleet as at December 2017. British airways had a total of 142 aircrafts of Airbus.

c)

Airbus represented 142 aircrafts in British Airways in the year 2017 which was 49% of the

total aircrafts in this organisation.

d)

From the above pie chart, it can be said that Airbus represented 49% against the total fleet

size of the British Airways. Whereas, Boeingn and Embraer aircraft manufacturers represents

44% and 7% of the total aircrafts in british airways.

e)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

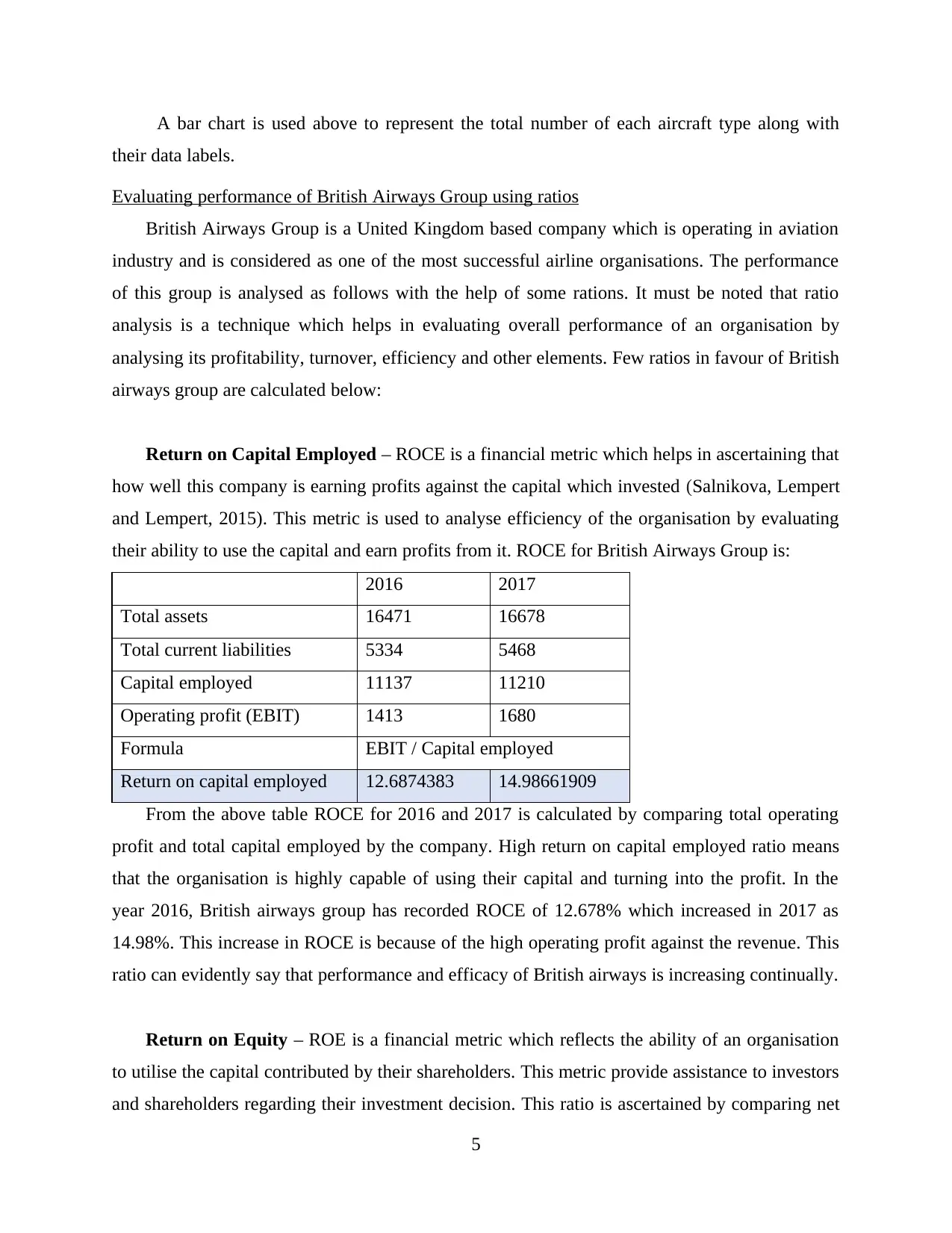

A bar chart is used above to represent the total number of each aircraft type along with

their data labels.

Evaluating performance of British Airways Group using ratios

British Airways Group is a United Kingdom based company which is operating in aviation

industry and is considered as one of the most successful airline organisations. The performance

of this group is analysed as follows with the help of some rations. It must be noted that ratio

analysis is a technique which helps in evaluating overall performance of an organisation by

analysing its profitability, turnover, efficiency and other elements. Few ratios in favour of British

airways group are calculated below:

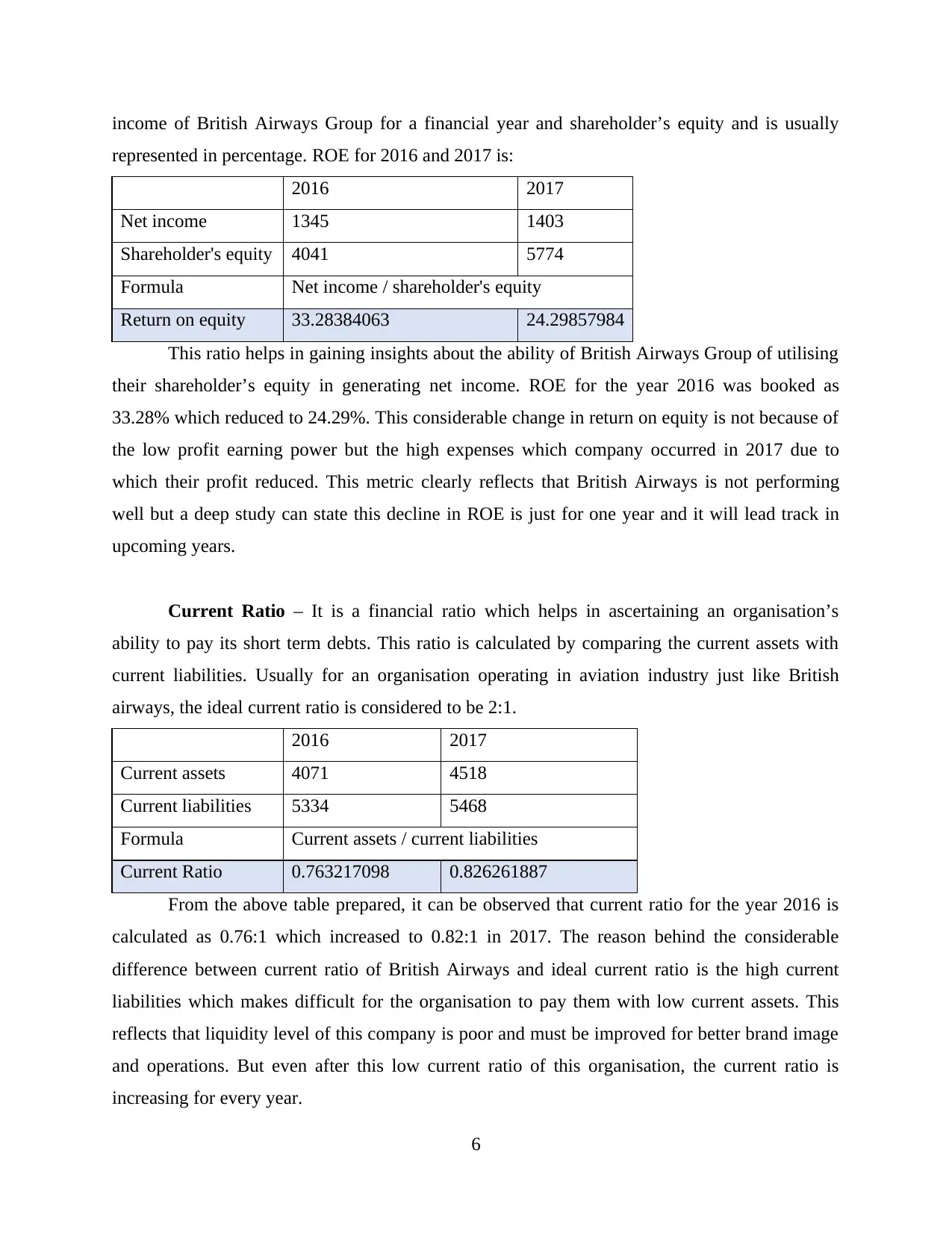

Return on Capital Employed – ROCE is a financial metric which helps in ascertaining that

how well this company is earning profits against the capital which invested (Salnikova, Lempert

and Lempert, 2015). This metric is used to analyse efficiency of the organisation by evaluating

their ability to use the capital and earn profits from it. ROCE for British Airways Group is:

2016 2017

Total assets 16471 16678

Total current liabilities 5334 5468

Capital employed 11137 11210

Operating profit (EBIT) 1413 1680

Formula EBIT / Capital employed

Return on capital employed 12.6874383 14.98661909

From the above table ROCE for 2016 and 2017 is calculated by comparing total operating

profit and total capital employed by the company. High return on capital employed ratio means

that the organisation is highly capable of using their capital and turning into the profit. In the

year 2016, British airways group has recorded ROCE of 12.678% which increased in 2017 as

14.98%. This increase in ROCE is because of the high operating profit against the revenue. This

ratio can evidently say that performance and efficacy of British airways is increasing continually.

Return on Equity – ROE is a financial metric which reflects the ability of an organisation

to utilise the capital contributed by their shareholders. This metric provide assistance to investors

and shareholders regarding their investment decision. This ratio is ascertained by comparing net

5

their data labels.

Evaluating performance of British Airways Group using ratios

British Airways Group is a United Kingdom based company which is operating in aviation

industry and is considered as one of the most successful airline organisations. The performance

of this group is analysed as follows with the help of some rations. It must be noted that ratio

analysis is a technique which helps in evaluating overall performance of an organisation by

analysing its profitability, turnover, efficiency and other elements. Few ratios in favour of British

airways group are calculated below:

Return on Capital Employed – ROCE is a financial metric which helps in ascertaining that

how well this company is earning profits against the capital which invested (Salnikova, Lempert

and Lempert, 2015). This metric is used to analyse efficiency of the organisation by evaluating

their ability to use the capital and earn profits from it. ROCE for British Airways Group is:

2016 2017

Total assets 16471 16678

Total current liabilities 5334 5468

Capital employed 11137 11210

Operating profit (EBIT) 1413 1680

Formula EBIT / Capital employed

Return on capital employed 12.6874383 14.98661909

From the above table ROCE for 2016 and 2017 is calculated by comparing total operating

profit and total capital employed by the company. High return on capital employed ratio means

that the organisation is highly capable of using their capital and turning into the profit. In the

year 2016, British airways group has recorded ROCE of 12.678% which increased in 2017 as

14.98%. This increase in ROCE is because of the high operating profit against the revenue. This

ratio can evidently say that performance and efficacy of British airways is increasing continually.

Return on Equity – ROE is a financial metric which reflects the ability of an organisation

to utilise the capital contributed by their shareholders. This metric provide assistance to investors

and shareholders regarding their investment decision. This ratio is ascertained by comparing net

5

income of British Airways Group for a financial year and shareholder’s equity and is usually

represented in percentage. ROE for 2016 and 2017 is:

2016 2017

Net income 1345 1403

Shareholder's equity 4041 5774

Formula Net income / shareholder's equity

Return on equity 33.28384063 24.29857984

This ratio helps in gaining insights about the ability of British Airways Group of utilising

their shareholder’s equity in generating net income. ROE for the year 2016 was booked as

33.28% which reduced to 24.29%. This considerable change in return on equity is not because of

the low profit earning power but the high expenses which company occurred in 2017 due to

which their profit reduced. This metric clearly reflects that British Airways is not performing

well but a deep study can state this decline in ROE is just for one year and it will lead track in

upcoming years.

Current Ratio – It is a financial ratio which helps in ascertaining an organisation’s

ability to pay its short term debts. This ratio is calculated by comparing the current assets with

current liabilities. Usually for an organisation operating in aviation industry just like British

airways, the ideal current ratio is considered to be 2:1.

2016 2017

Current assets 4071 4518

Current liabilities 5334 5468

Formula Current assets / current liabilities

Current Ratio 0.763217098 0.826261887

From the above table prepared, it can be observed that current ratio for the year 2016 is

calculated as 0.76:1 which increased to 0.82:1 in 2017. The reason behind the considerable

difference between current ratio of British Airways and ideal current ratio is the high current

liabilities which makes difficult for the organisation to pay them with low current assets. This

reflects that liquidity level of this company is poor and must be improved for better brand image

and operations. But even after this low current ratio of this organisation, the current ratio is

increasing for every year.

6

represented in percentage. ROE for 2016 and 2017 is:

2016 2017

Net income 1345 1403

Shareholder's equity 4041 5774

Formula Net income / shareholder's equity

Return on equity 33.28384063 24.29857984

This ratio helps in gaining insights about the ability of British Airways Group of utilising

their shareholder’s equity in generating net income. ROE for the year 2016 was booked as

33.28% which reduced to 24.29%. This considerable change in return on equity is not because of

the low profit earning power but the high expenses which company occurred in 2017 due to

which their profit reduced. This metric clearly reflects that British Airways is not performing

well but a deep study can state this decline in ROE is just for one year and it will lead track in

upcoming years.

Current Ratio – It is a financial ratio which helps in ascertaining an organisation’s

ability to pay its short term debts. This ratio is calculated by comparing the current assets with

current liabilities. Usually for an organisation operating in aviation industry just like British

airways, the ideal current ratio is considered to be 2:1.

2016 2017

Current assets 4071 4518

Current liabilities 5334 5468

Formula Current assets / current liabilities

Current Ratio 0.763217098 0.826261887

From the above table prepared, it can be observed that current ratio for the year 2016 is

calculated as 0.76:1 which increased to 0.82:1 in 2017. The reason behind the considerable

difference between current ratio of British Airways and ideal current ratio is the high current

liabilities which makes difficult for the organisation to pay them with low current assets. This

reflects that liquidity level of this company is poor and must be improved for better brand image

and operations. But even after this low current ratio of this organisation, the current ratio is

increasing for every year.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above ratio analysis of British Airways, it can be said that this company is rapidly

growing company and performing well. Even after its low liquidity position, the company is able

to generate high profits against the capital employed and amount invested by shareholders.

Discussing risk factors

Risk factors are elements associated with internal or external environment of the

organisation which can cause the chances of damaging the market position and revenue

(Wiersema and León, 2016). In context of British Airways group, there are various risk in their

business environment which levies high risk on their revenue and positioning. Some of these risk

factors which are acquired from annual report of the company are mentioned as follows:

Brand reputation is the most influential factor which can affect the future revenues.

Brand reputation is the image of a brand in the eyes of its consumers and people of the society.

People tend to pay for a service when they feel, the brand name has enough worth. In any future

contingent case, where reputation of British Airways reduces then the it will directly impact the

revenue of the company.

Another risk factor is competition. Competition in aviation industry is low and there is a

low threat of new entrants. But in the case, if the aviation industry becomes more attractive and

ample firms start working against the British Airways then both revenue and market positioning

of the company will start to decline. British Airways is currently considered as the market leader,

but in the situation when competition in this industry becomes high then the market share will be

distributed.

Mergers and acquisitions among the competitor firms of British Airways will provide

adversely impact the market position and revenue of the company. In such case, two or more

companies will amalgamate to become one by which their market share and assets will hike

rapidly. This high market share will ultimately result in low future revenue of British Airways.

British Airways is a technologically updated company and the management of the

company believes in high spending against upgrading their technological ability. In the current

scenario of where technology is advancing every day, it becomes high influential risk factor

which can result in obsolesce of the process of this company.

Government regulations and compliances is also a risk factor which can result in

damaging revenue and market position of the company. In the case where government restricts

7

growing company and performing well. Even after its low liquidity position, the company is able

to generate high profits against the capital employed and amount invested by shareholders.

Discussing risk factors

Risk factors are elements associated with internal or external environment of the

organisation which can cause the chances of damaging the market position and revenue

(Wiersema and León, 2016). In context of British Airways group, there are various risk in their

business environment which levies high risk on their revenue and positioning. Some of these risk

factors which are acquired from annual report of the company are mentioned as follows:

Brand reputation is the most influential factor which can affect the future revenues.

Brand reputation is the image of a brand in the eyes of its consumers and people of the society.

People tend to pay for a service when they feel, the brand name has enough worth. In any future

contingent case, where reputation of British Airways reduces then the it will directly impact the

revenue of the company.

Another risk factor is competition. Competition in aviation industry is low and there is a

low threat of new entrants. But in the case, if the aviation industry becomes more attractive and

ample firms start working against the British Airways then both revenue and market positioning

of the company will start to decline. British Airways is currently considered as the market leader,

but in the situation when competition in this industry becomes high then the market share will be

distributed.

Mergers and acquisitions among the competitor firms of British Airways will provide

adversely impact the market position and revenue of the company. In such case, two or more

companies will amalgamate to become one by which their market share and assets will hike

rapidly. This high market share will ultimately result in low future revenue of British Airways.

British Airways is a technologically updated company and the management of the

company believes in high spending against upgrading their technological ability. In the current

scenario of where technology is advancing every day, it becomes high influential risk factor

which can result in obsolesce of the process of this company.

Government regulations and compliances is also a risk factor which can result in

damaging revenue and market position of the company. In the case where government restricts

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operations of the companies operating in aviation industry in future, will directly impact the

market position and strategies of British Airways.

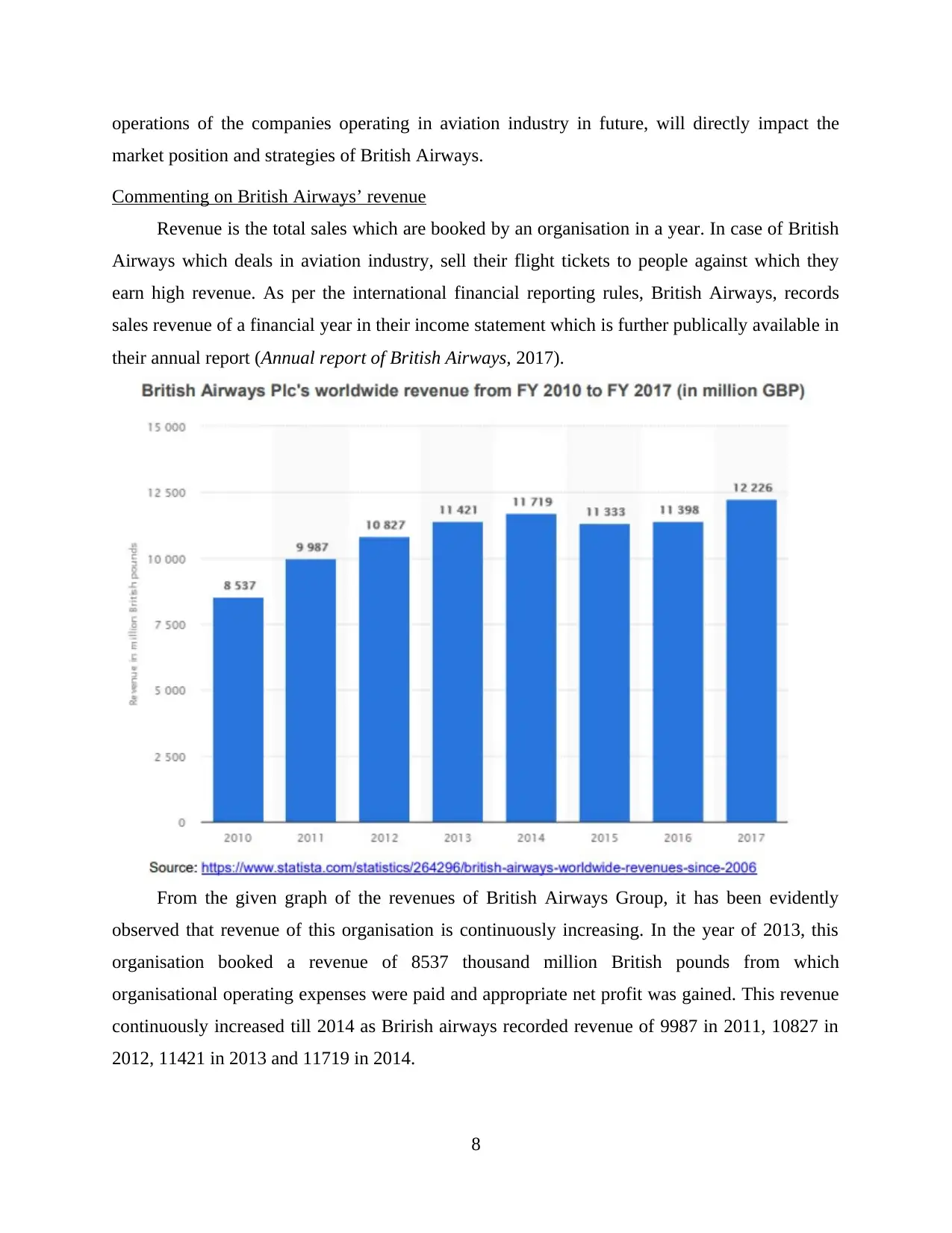

Commenting on British Airways’ revenue

Revenue is the total sales which are booked by an organisation in a year. In case of British

Airways which deals in aviation industry, sell their flight tickets to people against which they

earn high revenue. As per the international financial reporting rules, British Airways, records

sales revenue of a financial year in their income statement which is further publically available in

their annual report (Annual report of British Airways, 2017).

From the given graph of the revenues of British Airways Group, it has been evidently

observed that revenue of this organisation is continuously increasing. In the year of 2013, this

organisation booked a revenue of 8537 thousand million British pounds from which

organisational operating expenses were paid and appropriate net profit was gained. This revenue

continuously increased till 2014 as Brirish airways recorded revenue of 9987 in 2011, 10827 in

2012, 11421 in 2013 and 11719 in 2014.

8

market position and strategies of British Airways.

Commenting on British Airways’ revenue

Revenue is the total sales which are booked by an organisation in a year. In case of British

Airways which deals in aviation industry, sell their flight tickets to people against which they

earn high revenue. As per the international financial reporting rules, British Airways, records

sales revenue of a financial year in their income statement which is further publically available in

their annual report (Annual report of British Airways, 2017).

From the given graph of the revenues of British Airways Group, it has been evidently

observed that revenue of this organisation is continuously increasing. In the year of 2013, this

organisation booked a revenue of 8537 thousand million British pounds from which

organisational operating expenses were paid and appropriate net profit was gained. This revenue

continuously increased till 2014 as Brirish airways recorded revenue of 9987 in 2011, 10827 in

2012, 11421 in 2013 and 11719 in 2014.

8

After 2014, the revenue of British Airways slightly lost the flow and resulted in decreased

revenue as 11333 in 2015. The reason behind this decreased revenue was the ample operating

expenses which were occurred in this year in order to effectively market the brand name. In next

year, revenue of this company was back at its track and then keep on increasing till date. The

revenue recorded in 2016 was 11398 million British pounds which increased in 2017 as 12226

million British pounds.

Years 2013 2014 2015 2016 2017

Revenue 11421 11719 11333 11398 12226

Mean 11619.4

Standard deviation 370.2327646

In order to effectively analyse the pattern and trend of revenue in British Airways, the mean

and standard deviation of revenue of 5 years is also analysed. The mean is the average value of

all the frequencies. The mean represents the average revenue which British Airways has booked

in the interval of five years. From 2013 to 2017, the mean value of revenue of this company is

11619.4. This means average revenue of this company 11619 thousand million British pounds.

Besides this, standard deviation of this company is recoded as 370 which means their error

margin of the booked revenue is 370 thousand million British pounds. In the context of statistics,

standard deviation is the measure of the amount which can variate from the set of values. This

measure is calculated using the number of observations and determined mean. From this it can be

said that standard deviation in regard to British Airways reflects that this company can earn an

addition of 370 thousand million pounds. But this standard error goes both ways which means,

this amount can be either included or reduced from the net revenue of this company.

CONCLUSION

From the above report, it has been concluded that using information from statements and

records is important to get desired results. From the above report, it has been found that data is

usually of two types which is qualitative and quantitative. Both this types of data are analysed

through its unique techniques by which data is statistically presented so that results of the

hypothesis can be determined. The above report is well structured by which it has been observed

that data of organisation can be used to analyse its financial performance and stability. From the

above report, financial stability of British Airways Group is analysed from which it is concluded

that despite of low liquidity ability of the company, the growth margin if this company is high

9

revenue as 11333 in 2015. The reason behind this decreased revenue was the ample operating

expenses which were occurred in this year in order to effectively market the brand name. In next

year, revenue of this company was back at its track and then keep on increasing till date. The

revenue recorded in 2016 was 11398 million British pounds which increased in 2017 as 12226

million British pounds.

Years 2013 2014 2015 2016 2017

Revenue 11421 11719 11333 11398 12226

Mean 11619.4

Standard deviation 370.2327646

In order to effectively analyse the pattern and trend of revenue in British Airways, the mean

and standard deviation of revenue of 5 years is also analysed. The mean is the average value of

all the frequencies. The mean represents the average revenue which British Airways has booked

in the interval of five years. From 2013 to 2017, the mean value of revenue of this company is

11619.4. This means average revenue of this company 11619 thousand million British pounds.

Besides this, standard deviation of this company is recoded as 370 which means their error

margin of the booked revenue is 370 thousand million British pounds. In the context of statistics,

standard deviation is the measure of the amount which can variate from the set of values. This

measure is calculated using the number of observations and determined mean. From this it can be

said that standard deviation in regard to British Airways reflects that this company can earn an

addition of 370 thousand million pounds. But this standard error goes both ways which means,

this amount can be either included or reduced from the net revenue of this company.

CONCLUSION

From the above report, it has been concluded that using information from statements and

records is important to get desired results. From the above report, it has been found that data is

usually of two types which is qualitative and quantitative. Both this types of data are analysed

through its unique techniques by which data is statistically presented so that results of the

hypothesis can be determined. The above report is well structured by which it has been observed

that data of organisation can be used to analyse its financial performance and stability. From the

above report, financial stability of British Airways Group is analysed from which it is concluded

that despite of low liquidity ability of the company, the growth margin if this company is high

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.