Data Science Solutions for OCBC Bank: Overcoming Challenges

VerifiedAdded on 2023/04/21

|18

|4069

|360

Report

AI Summary

This report evaluates the challenges faced by OCBC Limited, a Singapore-based bank, focusing on profitability and customer satisfaction. It explores the company's background, key challenges, and the impact of improvements in these areas. The report proposes solutions such as cloud computing to enhance efficiency and customer relationships. It also assesses financial feasibility, including startup capital, potential profits, and sources of funding. Furthermore, it identifies potential risks and mitigation plans, along with an implementation roadmap. The analysis includes financial data, such as the #OCBCCares Fund, and concludes with recommendations for OCBC Bank to leverage data science for sustainable growth and improved customer experience. Desklib provides this student-contributed assignment and other study resources for students.

Data Science

Student’s Name:

Student’s ID:

Table of Contents

Student’s Name:

Student’s ID:

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Introduction.................................................................................................................................................2

Background of the Company.......................................................................................................................2

Key Challenges in the Company and Impact of Improvement.....................................................................2

Solution to the Challenges...........................................................................................................................5

Financial Feasibility......................................................................................................................................7

Risks and Challenges and Mitigation Plans..................................................................................................8

Implementation of Roadmap....................................................................................................................11

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

Introduction.................................................................................................................................................2

Background of the Company.......................................................................................................................2

Key Challenges in the Company and Impact of Improvement.....................................................................2

Solution to the Challenges...........................................................................................................................5

Financial Feasibility......................................................................................................................................7

Risks and Challenges and Mitigation Plans..................................................................................................8

Implementation of Roadmap....................................................................................................................11

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

2

Introduction

The report will help in evaluating the details about a Singapore based bank, OCBC Limited.

Brief information on the background of OCBC will help in understanding the aspects regarding

the execution of the business process of the firm. Moreover, the report will highlight the key

challenges faced by the OCBC bank throughout the nation. It will also provide solutions for

reducing the challenges. Two of the vital areas that can boost the overall growth of the firm are

profitability as well as the satisfaction of the customers. The enhancement in the quality of the

products will help in increasing the profitability of the firma and will bring more customers.

Moreover, the report will help in reflecting the details on sources of capital, return on investment

and amount of startup capital that are required by the OCBC Bank. It will analyze the challenges

and risks, and proper mitigation plans will be required. Finally, the implementation roadmap will

help in reducing these challenges and will facilitate the overall growth of the firm.

Background of the Company

Oversea-Chinese Banking Corporation (OCBC), Limited is financial services and multinational

banking corporation having its headquarter in OCBC Centre in Singapore. In 1932, because of

the Great Depression and consolidation of the three banks such as the Overseas Chinese Limited,

the bank of Ho Hong and the Chinese Commercial Bank Ltd, OCBC bank was born (Adzis,

Sheng and Bakar, 2018). The OCBC Bank is the second largest bank in South Asia having assets

over $454.9 billion. Moody gave a rating of Aa1 which makes it one of the world's most high-

rated banks. In the world, OCBC holds rank among the top 5 safest banks. It has over 570

branches in 18 countries.

Introduction

The report will help in evaluating the details about a Singapore based bank, OCBC Limited.

Brief information on the background of OCBC will help in understanding the aspects regarding

the execution of the business process of the firm. Moreover, the report will highlight the key

challenges faced by the OCBC bank throughout the nation. It will also provide solutions for

reducing the challenges. Two of the vital areas that can boost the overall growth of the firm are

profitability as well as the satisfaction of the customers. The enhancement in the quality of the

products will help in increasing the profitability of the firma and will bring more customers.

Moreover, the report will help in reflecting the details on sources of capital, return on investment

and amount of startup capital that are required by the OCBC Bank. It will analyze the challenges

and risks, and proper mitigation plans will be required. Finally, the implementation roadmap will

help in reducing these challenges and will facilitate the overall growth of the firm.

Background of the Company

Oversea-Chinese Banking Corporation (OCBC), Limited is financial services and multinational

banking corporation having its headquarter in OCBC Centre in Singapore. In 1932, because of

the Great Depression and consolidation of the three banks such as the Overseas Chinese Limited,

the bank of Ho Hong and the Chinese Commercial Bank Ltd, OCBC bank was born (Adzis,

Sheng and Bakar, 2018). The OCBC Bank is the second largest bank in South Asia having assets

over $454.9 billion. Moody gave a rating of Aa1 which makes it one of the world's most high-

rated banks. In the world, OCBC holds rank among the top 5 safest banks. It has over 570

branches in 18 countries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Key Challenges in the Company and Impact of Improvement

The key challenges faced by the OCBC Bank are as follows:

Profitability – The service investors of Moody had said that OCBC has been facing an

increasing problem in operating conditions both at regional markets and home which results in a

rise in pressure on profitability and the quality of the asset (Keffala, 2015). Because of these key

challenges, OCBC's rating dropped. OCBC bank Singapore is exposed to weak corporate

financial conditions, a momentum of growth, the higher delinquency rate of the loan, slow trade,

and economic growth. The dependency on the global economy is also posing challenges to the

profitability of the OCBC Bank. It can be defined as a situation when the revenues and costs rely

on the state of the global economy. As revenue has gone down, it has affected the OCBC bank

(Firth, Li and Shuye Wang, 2016).

An efficient and proper financial planning is not performed in OCBC bank. As a result of which

cash is not used efficiently (Quan and Khoe, 2016). Net contribution percent and the profitability

ratio is below average. As the unique position of selling and the position of OCBC Bank is not

well-defined, competitors can attack this segment. OCBC Bank is not well at forecasting demand

which results in keeping higher inventory both in the channel and in the home nation as

compared to its competitors (Koh, 2018).

Customer Satisfaction – The challenge of customer satisfaction is another issue in OCBC Bank.

A survey has shown that customers do not trust the bank and are dissatisfied due to longer

waiting time during mobile banking (Isa et al., 2016). The other reasons are waiting for the

number to be called at the counter, standing in the queue at the ATMs and additional banking

charges. OCBC was recently facing a technical glitch at its banking network in Singapore, which

created difficulties for the customers to use the internet banking facility and the ATMs (Keffala

Key Challenges in the Company and Impact of Improvement

The key challenges faced by the OCBC Bank are as follows:

Profitability – The service investors of Moody had said that OCBC has been facing an

increasing problem in operating conditions both at regional markets and home which results in a

rise in pressure on profitability and the quality of the asset (Keffala, 2015). Because of these key

challenges, OCBC's rating dropped. OCBC bank Singapore is exposed to weak corporate

financial conditions, a momentum of growth, the higher delinquency rate of the loan, slow trade,

and economic growth. The dependency on the global economy is also posing challenges to the

profitability of the OCBC Bank. It can be defined as a situation when the revenues and costs rely

on the state of the global economy. As revenue has gone down, it has affected the OCBC bank

(Firth, Li and Shuye Wang, 2016).

An efficient and proper financial planning is not performed in OCBC bank. As a result of which

cash is not used efficiently (Quan and Khoe, 2016). Net contribution percent and the profitability

ratio is below average. As the unique position of selling and the position of OCBC Bank is not

well-defined, competitors can attack this segment. OCBC Bank is not well at forecasting demand

which results in keeping higher inventory both in the channel and in the home nation as

compared to its competitors (Koh, 2018).

Customer Satisfaction – The challenge of customer satisfaction is another issue in OCBC Bank.

A survey has shown that customers do not trust the bank and are dissatisfied due to longer

waiting time during mobile banking (Isa et al., 2016). The other reasons are waiting for the

number to be called at the counter, standing in the queue at the ATMs and additional banking

charges. OCBC was recently facing a technical glitch at its banking network in Singapore, which

created difficulties for the customers to use the internet banking facility and the ATMs (Keffala

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

and De Peretti, 2016). The investment in technology of OCBC Bank is not at parity with the

vision of the firm.

40% of the customers of the bank are either cancelling or stopping their banking services due to

the poor customer experience. The repetition of the same information is the main reason for

cancelling the present relation with the OCBC Bank. Many customers have complained that the

banking staffs lack the ability to remember their previous interaction with the customer (Keffala,

2016). As a result, seamless handovers led to frustration among the consumers as they have to

repeat their queries several times. 45% of the customers have to contact the bank at least twice to

solve one problem whereas 40% have to utilize more than one channel to solve the same problem

(Shaban and James, 2018)

The impact of improvement in these areas are as follows:

Profitability – The financial strategies of the bank must be taken care and occasionally changed

so that it is capable of adapting the downturns and emergencies and it can take advantage of the

substantial changes in the global economy (Rasheed and Chauhan, 2016). New marketing

policies can be an excellent break for OCBC Bank to determine its advantage in new technology.

Moreover, the expansion of the market can lead to the weakening of the benefit of competitors,

and thus OCBC Bank can increase its profitability as compared to other competitors (Khaliq et

al., 2017).

Implementation of an efficient financial system by the OCBC Bank can improve its profitability,

and increase the flow of funds from investors to borrowers. Foreign investment can increase the

profitability of the bank as the foreign investors can contribute to the bank by selling their bank

products in Singapore. Faster economic development and rise in interest rates of the bank can

and De Peretti, 2016). The investment in technology of OCBC Bank is not at parity with the

vision of the firm.

40% of the customers of the bank are either cancelling or stopping their banking services due to

the poor customer experience. The repetition of the same information is the main reason for

cancelling the present relation with the OCBC Bank. Many customers have complained that the

banking staffs lack the ability to remember their previous interaction with the customer (Keffala,

2016). As a result, seamless handovers led to frustration among the consumers as they have to

repeat their queries several times. 45% of the customers have to contact the bank at least twice to

solve one problem whereas 40% have to utilize more than one channel to solve the same problem

(Shaban and James, 2018)

The impact of improvement in these areas are as follows:

Profitability – The financial strategies of the bank must be taken care and occasionally changed

so that it is capable of adapting the downturns and emergencies and it can take advantage of the

substantial changes in the global economy (Rasheed and Chauhan, 2016). New marketing

policies can be an excellent break for OCBC Bank to determine its advantage in new technology.

Moreover, the expansion of the market can lead to the weakening of the benefit of competitors,

and thus OCBC Bank can increase its profitability as compared to other competitors (Khaliq et

al., 2017).

Implementation of an efficient financial system by the OCBC Bank can improve its profitability,

and increase the flow of funds from investors to borrowers. Foreign investment can increase the

profitability of the bank as the foreign investors can contribute to the bank by selling their bank

products in Singapore. Faster economic development and rise in interest rates of the bank can

5

push up the borrowing costs (Winarso and Salim, 2017). Strong economic expansion indicates

that the bank might see growth in loans. Strong economic development and increasing rates can

allow the bank to charge more for loans. As a result, the total interest income of the bank can

grow and improve the profitability of OCBC Bank.

Customer Satisfaction –New trends in customer behavior can provide an excellent opportunity

for OCBC Bank to expand into new product classes and build different revenue streams. The

head of human resource planning of OCBC bank, Ms. Jacinta Low said that Professional

Conversion Program (PCP) allows the organization to explore the alternative sources of banking

services to build the customer-centric policies (Shaban and James, 2018). The technical glitch

could be improved by properly investigating the reason and restoring the services as quickly as

possible to reduce the harassment of the customers. Increase in spending on customers and

economic uptick can increase the market share and capture new customers (Wanke, Azad and

Barros, 2016).

OCBC Bank has to improve the aspects of its business and its banking services and try to

improvise them for better customer services. The bank must take the initiative to learn the best

its competitors of the service provider in the banking industry (Rashid, Ramachandran and

Fawzy, 2017). The customer care is the best method to build a better and long term customer

relationship. The bank has to make its customers feel like having personalized experience and

personal relation while speaking with the staffs of the bank (Saha, Ahmad and Dash, 2015). It

could improve the customer satisfaction of the OCBC Bank.

push up the borrowing costs (Winarso and Salim, 2017). Strong economic expansion indicates

that the bank might see growth in loans. Strong economic development and increasing rates can

allow the bank to charge more for loans. As a result, the total interest income of the bank can

grow and improve the profitability of OCBC Bank.

Customer Satisfaction –New trends in customer behavior can provide an excellent opportunity

for OCBC Bank to expand into new product classes and build different revenue streams. The

head of human resource planning of OCBC bank, Ms. Jacinta Low said that Professional

Conversion Program (PCP) allows the organization to explore the alternative sources of banking

services to build the customer-centric policies (Shaban and James, 2018). The technical glitch

could be improved by properly investigating the reason and restoring the services as quickly as

possible to reduce the harassment of the customers. Increase in spending on customers and

economic uptick can increase the market share and capture new customers (Wanke, Azad and

Barros, 2016).

OCBC Bank has to improve the aspects of its business and its banking services and try to

improvise them for better customer services. The bank must take the initiative to learn the best

its competitors of the service provider in the banking industry (Rashid, Ramachandran and

Fawzy, 2017). The customer care is the best method to build a better and long term customer

relationship. The bank has to make its customers feel like having personalized experience and

personal relation while speaking with the staffs of the bank (Saha, Ahmad and Dash, 2015). It

could improve the customer satisfaction of the OCBC Bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Solution to the Challenges

ODBC Bank needs to address its challenges of profitability and customer satisfaction. There is a

need to find out such systems that do not depend on like-system migration and the challenges of

the bank could be solved without any interruption. The banking sector has been slow in

implementing cloud computing as they fear the issues of consistency, regulatory and security

risks (Sufian and Kamarudin, 2016). But this technology is slowly changing the banking and

finance sector. It can increase the efficiency of the bank and can create an infrastructure to

deliver the best services to its customers.

The technology of cloud computing can create opportunities for OCBC Bank to directly connect

with their customers (Yip and Bocken, 2018). The cloud computing can help in providing the

digital services for maintaining the customer relationships anywhere and anytime. Internet helps

in several services such as to store, manage and access the information and so it has become

easier for both the bank and its customers (Sufian, Kamarudin and Md. Nassir, 2017). The cloud

computing is a technique which can help to organize and combine all the services and challenges

of the bank and decrease the time and effort of both the bank and its customers.

The development of cloud computing can enable the bank to be more customer-centric and

digitalize its business and wealth. This technology can build a multi-channel relation with the

consumers at every phase of its service. It can help to store, backup and recover large data of the

customers of the OCBC Bank and solve the issues of cybercrime. The cloud computing could

not only the store data but can also help in various other services such as to deliver the software,

transfer the data, update and recovery of data (Sulaiman@ Mohamad, Mohamad and Hashim,

2018). It can also increase the turnover of OCBC Bank by providing cost-effective cloud

solutions. The cyber-attacks by the hackers can be reduced with the help of cloud computing.

Solution to the Challenges

ODBC Bank needs to address its challenges of profitability and customer satisfaction. There is a

need to find out such systems that do not depend on like-system migration and the challenges of

the bank could be solved without any interruption. The banking sector has been slow in

implementing cloud computing as they fear the issues of consistency, regulatory and security

risks (Sufian and Kamarudin, 2016). But this technology is slowly changing the banking and

finance sector. It can increase the efficiency of the bank and can create an infrastructure to

deliver the best services to its customers.

The technology of cloud computing can create opportunities for OCBC Bank to directly connect

with their customers (Yip and Bocken, 2018). The cloud computing can help in providing the

digital services for maintaining the customer relationships anywhere and anytime. Internet helps

in several services such as to store, manage and access the information and so it has become

easier for both the bank and its customers (Sufian, Kamarudin and Md. Nassir, 2017). The cloud

computing is a technique which can help to organize and combine all the services and challenges

of the bank and decrease the time and effort of both the bank and its customers.

The development of cloud computing can enable the bank to be more customer-centric and

digitalize its business and wealth. This technology can build a multi-channel relation with the

consumers at every phase of its service. It can help to store, backup and recover large data of the

customers of the OCBC Bank and solve the issues of cybercrime. The cloud computing could

not only the store data but can also help in various other services such as to deliver the software,

transfer the data, update and recovery of data (Sulaiman@ Mohamad, Mohamad and Hashim,

2018). It can also increase the turnover of OCBC Bank by providing cost-effective cloud

solutions. The cyber-attacks by the hackers can be reduced with the help of cloud computing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

OCBC Bank already uses the Fintech technology named as The Open Vault. The cloud

computing technology can help the Fintech technology to continually maintain the substantial

growth of the bank. The most vital aspect of this technology is to reduce the challenges of the

bank related to its profitability. It can completely secure the confidential data of the bank which

can further reduce the cybercrime (Uribe, Chuliá and Guillén, 2017). It also helps to analyze the

risk factors of the bank’s business so that the main focus will be on its business and the crucial

data. The cloud computing technology can help the OCBC Bank in managing various challenges

and demands of the banking world.

Financial Feasibility

In the year 2017, OCBC Bank has launched #OCBCCares Fund for the Environment and has

aimed to provide S$100,000 every year. This was planned to support the projects that will

improve the environmental landscape of Singapore. On 2018, OCBC Bank has declared that it

will provide S$87,000 to six projects which will address the issues of environmental

sustainability in Singapore. The fact that the bank could fund six projects at an amount less than

their fund commitment is a positive signal that their initiatives for protecting the environment of

Singapore are not expensive missions.

The bank has hoped that the other firms of Singapore also come on board to provide support in

these projects. The bank has received 28 proposals for fund between S$2,000 to S$150,000.

Moreover, the applicants are from different backgrounds and ages between 20 years to 69 years.

OCBC Malaysia has still not released its 2018 financial report. But, on the basis of the data on

the website of its parent company, in 2nd Quarter of 2018, the total profit of OCBC has fallen

12% from the previous year to RM207 million. It has indicated its profit of 1st Half of 2018 has

OCBC Bank already uses the Fintech technology named as The Open Vault. The cloud

computing technology can help the Fintech technology to continually maintain the substantial

growth of the bank. The most vital aspect of this technology is to reduce the challenges of the

bank related to its profitability. It can completely secure the confidential data of the bank which

can further reduce the cybercrime (Uribe, Chuliá and Guillén, 2017). It also helps to analyze the

risk factors of the bank’s business so that the main focus will be on its business and the crucial

data. The cloud computing technology can help the OCBC Bank in managing various challenges

and demands of the banking world.

Financial Feasibility

In the year 2017, OCBC Bank has launched #OCBCCares Fund for the Environment and has

aimed to provide S$100,000 every year. This was planned to support the projects that will

improve the environmental landscape of Singapore. On 2018, OCBC Bank has declared that it

will provide S$87,000 to six projects which will address the issues of environmental

sustainability in Singapore. The fact that the bank could fund six projects at an amount less than

their fund commitment is a positive signal that their initiatives for protecting the environment of

Singapore are not expensive missions.

The bank has hoped that the other firms of Singapore also come on board to provide support in

these projects. The bank has received 28 proposals for fund between S$2,000 to S$150,000.

Moreover, the applicants are from different backgrounds and ages between 20 years to 69 years.

OCBC Malaysia has still not released its 2018 financial report. But, on the basis of the data on

the website of its parent company, in 2nd Quarter of 2018, the total profit of OCBC has fallen

12% from the previous year to RM207 million. It has indicated its profit of 1st Half of 2018 has

8

declined 2% to RM451 million. But the net income in 1st Half has increased 3% to RM1.24

billion.

declined 2% to RM451 million. But the net income in 1st Half has increased 3% to RM1.24

billion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

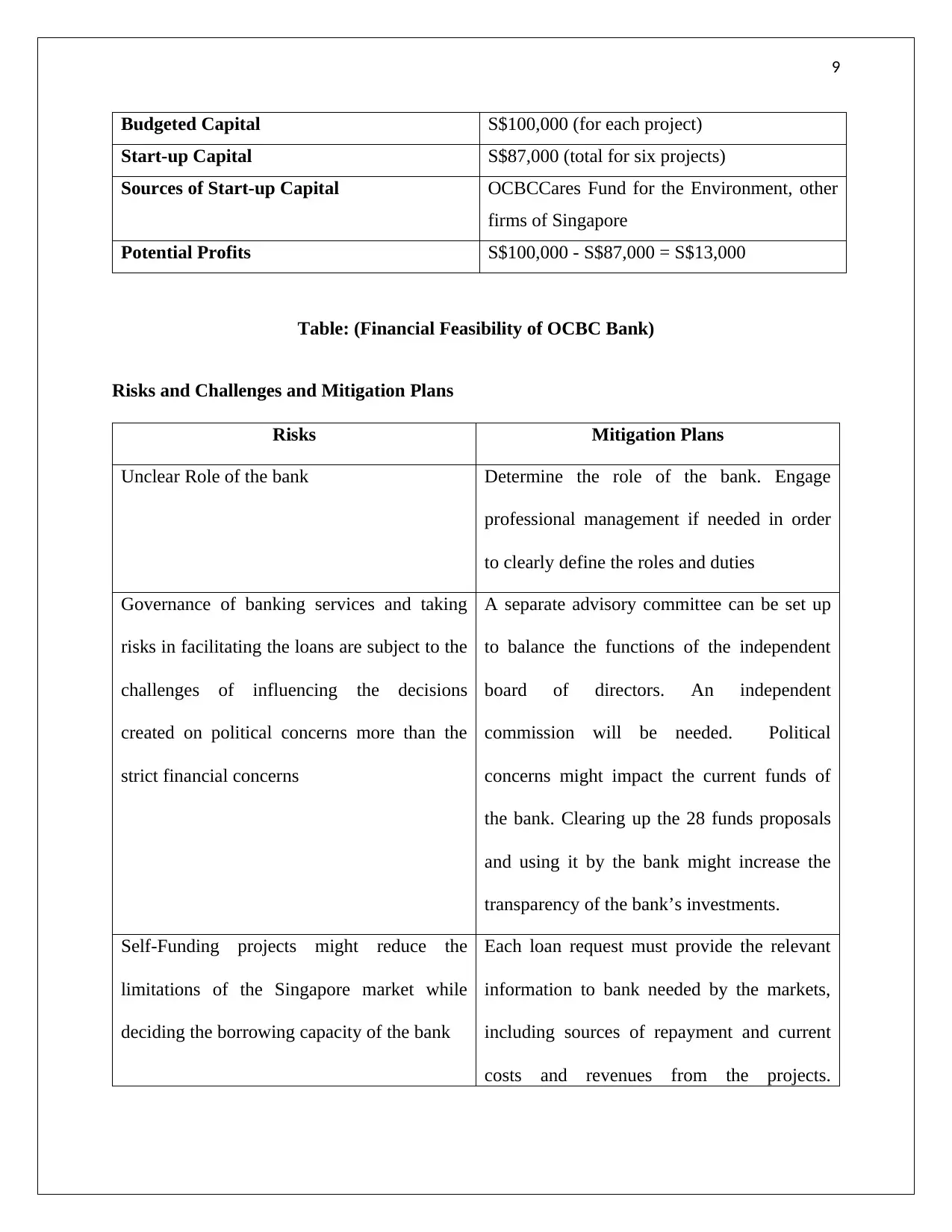

Budgeted Capital S$100,000 (for each project)

Start-up Capital S$87,000 (total for six projects)

Sources of Start-up Capital OCBCCares Fund for the Environment, other

firms of Singapore

Potential Profits S$100,000 - S$87,000 = S$13,000

Table: (Financial Feasibility of OCBC Bank)

Risks and Challenges and Mitigation Plans

Risks Mitigation Plans

Unclear Role of the bank Determine the role of the bank. Engage

professional management if needed in order

to clearly define the roles and duties

Governance of banking services and taking

risks in facilitating the loans are subject to the

challenges of influencing the decisions

created on political concerns more than the

strict financial concerns

A separate advisory committee can be set up

to balance the functions of the independent

board of directors. An independent

commission will be needed. Political

concerns might impact the current funds of

the bank. Clearing up the 28 funds proposals

and using it by the bank might increase the

transparency of the bank’s investments.

Self-Funding projects might reduce the

limitations of the Singapore market while

deciding the borrowing capacity of the bank

Each loan request must provide the relevant

information to bank needed by the markets,

including sources of repayment and current

costs and revenues from the projects.

Budgeted Capital S$100,000 (for each project)

Start-up Capital S$87,000 (total for six projects)

Sources of Start-up Capital OCBCCares Fund for the Environment, other

firms of Singapore

Potential Profits S$100,000 - S$87,000 = S$13,000

Table: (Financial Feasibility of OCBC Bank)

Risks and Challenges and Mitigation Plans

Risks Mitigation Plans

Unclear Role of the bank Determine the role of the bank. Engage

professional management if needed in order

to clearly define the roles and duties

Governance of banking services and taking

risks in facilitating the loans are subject to the

challenges of influencing the decisions

created on political concerns more than the

strict financial concerns

A separate advisory committee can be set up

to balance the functions of the independent

board of directors. An independent

commission will be needed. Political

concerns might impact the current funds of

the bank. Clearing up the 28 funds proposals

and using it by the bank might increase the

transparency of the bank’s investments.

Self-Funding projects might reduce the

limitations of the Singapore market while

deciding the borrowing capacity of the bank

Each loan request must provide the relevant

information to bank needed by the markets,

including sources of repayment and current

costs and revenues from the projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Financial Advisors will continue to advise the

bank on its financial condition and rating

forecasts. The bank will continue to access

the markets even for the projects that were

initially funded internally.

Failing to fund the projects with long -term

funding and low-interest rates. The increase in

rates in future can risk the external financing.

The OCBC bank is currently investing its

funds at a Weighted Average Maturity for less

than a year. With internal financing, the bank

can effectively lengthen its loans to a longer

term and higher interest rate. It can offset the

concerns over the perceived market

requirements.

Internally funding the long term projects can

reduce the liquidity of the bank

An alternate way to maintain the liquidity is

low cost, particularly with local banks and

collateral repurchase contracts.

Lowering of the security needs in order to

incentivize the local organizations to lend

more can subject the bank to the increased

risk of project failure

Extra collateral can be reduced as it might

substitute the local loans, possibly by 100%

Funding for the projects might increase the

organizational costs of the bank

Most of the banking services can be turned

into a new entity. The implementation can

allow the bank to grow into complete banking

services without depending on external

Financial Advisors will continue to advise the

bank on its financial condition and rating

forecasts. The bank will continue to access

the markets even for the projects that were

initially funded internally.

Failing to fund the projects with long -term

funding and low-interest rates. The increase in

rates in future can risk the external financing.

The OCBC bank is currently investing its

funds at a Weighted Average Maturity for less

than a year. With internal financing, the bank

can effectively lengthen its loans to a longer

term and higher interest rate. It can offset the

concerns over the perceived market

requirements.

Internally funding the long term projects can

reduce the liquidity of the bank

An alternate way to maintain the liquidity is

low cost, particularly with local banks and

collateral repurchase contracts.

Lowering of the security needs in order to

incentivize the local organizations to lend

more can subject the bank to the increased

risk of project failure

Extra collateral can be reduced as it might

substitute the local loans, possibly by 100%

Funding for the projects might increase the

organizational costs of the bank

Most of the banking services can be turned

into a new entity. The implementation can

allow the bank to grow into complete banking

services without depending on external

11

consulting and staffing.

Existing commercial banks of Singapore

might view this initiative as a competitive

threat, thereby risking the state charter and

cooperative relations.

Focus at first on the intra-city loans. Look for

alternative ways for the collateral needs on

investments with the other organizations or

banks to increase their capacity to lend

locally. Need external funding to be

introduced at the request of the bank.

Unrestricted cash of the bank can be a source

of inequity for a bank.

Banking services which are not state

chartered does not need separate equity. On

chartering a bank, adequate capital can be

provided. The bank can get a high yield on

those funds. Alternate sources of investment

could also be taken like Charitable Funds,

Mini-Bond funded by the citizens and the

Bonds issued from public entities.

Involvement of the bank in environmental

projects could find one way, or another can

reduce the funds for other projects while

guaranteeing the investments for the bank.

Review the materials of investment and make

sure that disclosures are satisfactory, and does

not indicate the credit support of the bank.

consulting and staffing.

Existing commercial banks of Singapore

might view this initiative as a competitive

threat, thereby risking the state charter and

cooperative relations.

Focus at first on the intra-city loans. Look for

alternative ways for the collateral needs on

investments with the other organizations or

banks to increase their capacity to lend

locally. Need external funding to be

introduced at the request of the bank.

Unrestricted cash of the bank can be a source

of inequity for a bank.

Banking services which are not state

chartered does not need separate equity. On

chartering a bank, adequate capital can be

provided. The bank can get a high yield on

those funds. Alternate sources of investment

could also be taken like Charitable Funds,

Mini-Bond funded by the citizens and the

Bonds issued from public entities.

Involvement of the bank in environmental

projects could find one way, or another can

reduce the funds for other projects while

guaranteeing the investments for the bank.

Review the materials of investment and make

sure that disclosures are satisfactory, and does

not indicate the credit support of the bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.