DB125 Taxation & Money: Income Analysis, Debt, and Finance Report

VerifiedAdded on 2022/09/09

|21

|4391

|21

Homework Assignment

AI Summary

This assignment solution provides a detailed analysis of taxation and financial planning concepts. It includes calculations of income tax and national insurance for employees at Crossdigital Ltd, comparing the progressivity of tax systems in England and Scotland. The assignment explores the impact of inflation on living standards and calculates equalized net income for households using the modified OECD scale. It also analyzes monthly cash flow statements, evaluates borrowing options, and discusses the advantages and disadvantages of different loan repayment plans. The solution further examines unsecured debt and factors contributing to household debt levels. Desklib offers this and many other solved assignments and past papers to aid students in their studies.

RUNNING HEAD: - Taxation and provisions 0 | P a g e

TMA 02

TMA 02

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 1 | P a g e

Contents

Part A..........................................................................................................................................................2

Answer to question no. – 1......................................................................................................................2

Answer to question no. – 2......................................................................................................................6

Answer to question no. – 3....................................................................................................................10

Part B.........................................................................................................................................................14

Introduction...........................................................................................................................................14

Unsecured Debt.....................................................................................................................................15

Different types of unsecured borrowing:...............................................................................................15

Factors which may have contributed to the level of unsecured household debt:....................................16

Part C.........................................................................................................................................................17

Team Work:...........................................................................................................................................17

References.................................................................................................................................................19

1 | P a g e

Contents

Part A..........................................................................................................................................................2

Answer to question no. – 1......................................................................................................................2

Answer to question no. – 2......................................................................................................................6

Answer to question no. – 3....................................................................................................................10

Part B.........................................................................................................................................................14

Introduction...........................................................................................................................................14

Unsecured Debt.....................................................................................................................................15

Different types of unsecured borrowing:...............................................................................................15

Factors which may have contributed to the level of unsecured household debt:....................................16

Part C.........................................................................................................................................................17

Team Work:...........................................................................................................................................17

References.................................................................................................................................................19

1 | P a g e

Taxation and provisions 2 | P a g e

Part A

Answer to question no. – 1

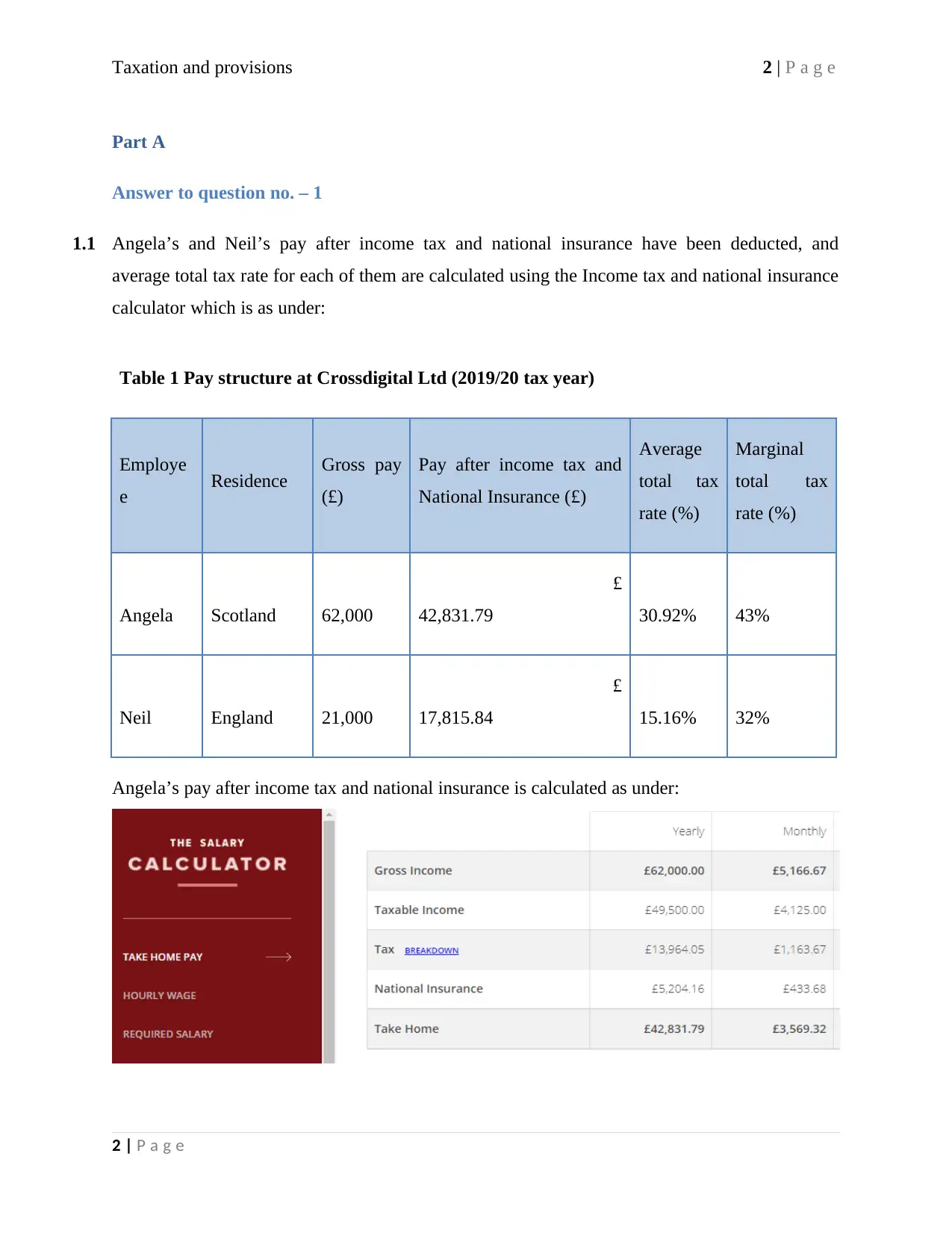

1.1 Angela’s and Neil’s pay after income tax and national insurance have been deducted, and

average total tax rate for each of them are calculated using the Income tax and national insurance

calculator which is as under:

Table 1 Pay structure at Crossdigital Ltd (2019/20 tax year)

Employe

e Residence Gross pay

(£)

Pay after income tax and

National Insurance (£)

Average

total tax

rate (%)

Marginal

total tax

rate (%)

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Neil England 21,000

£

17,815.84 15.16% 32%

Angela’s pay after income tax and national insurance is calculated as under:

2 | P a g e

Part A

Answer to question no. – 1

1.1 Angela’s and Neil’s pay after income tax and national insurance have been deducted, and

average total tax rate for each of them are calculated using the Income tax and national insurance

calculator which is as under:

Table 1 Pay structure at Crossdigital Ltd (2019/20 tax year)

Employe

e Residence Gross pay

(£)

Pay after income tax and

National Insurance (£)

Average

total tax

rate (%)

Marginal

total tax

rate (%)

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Neil England 21,000

£

17,815.84 15.16% 32%

Angela’s pay after income tax and national insurance is calculated as under:

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation and provisions 3 | P a g e

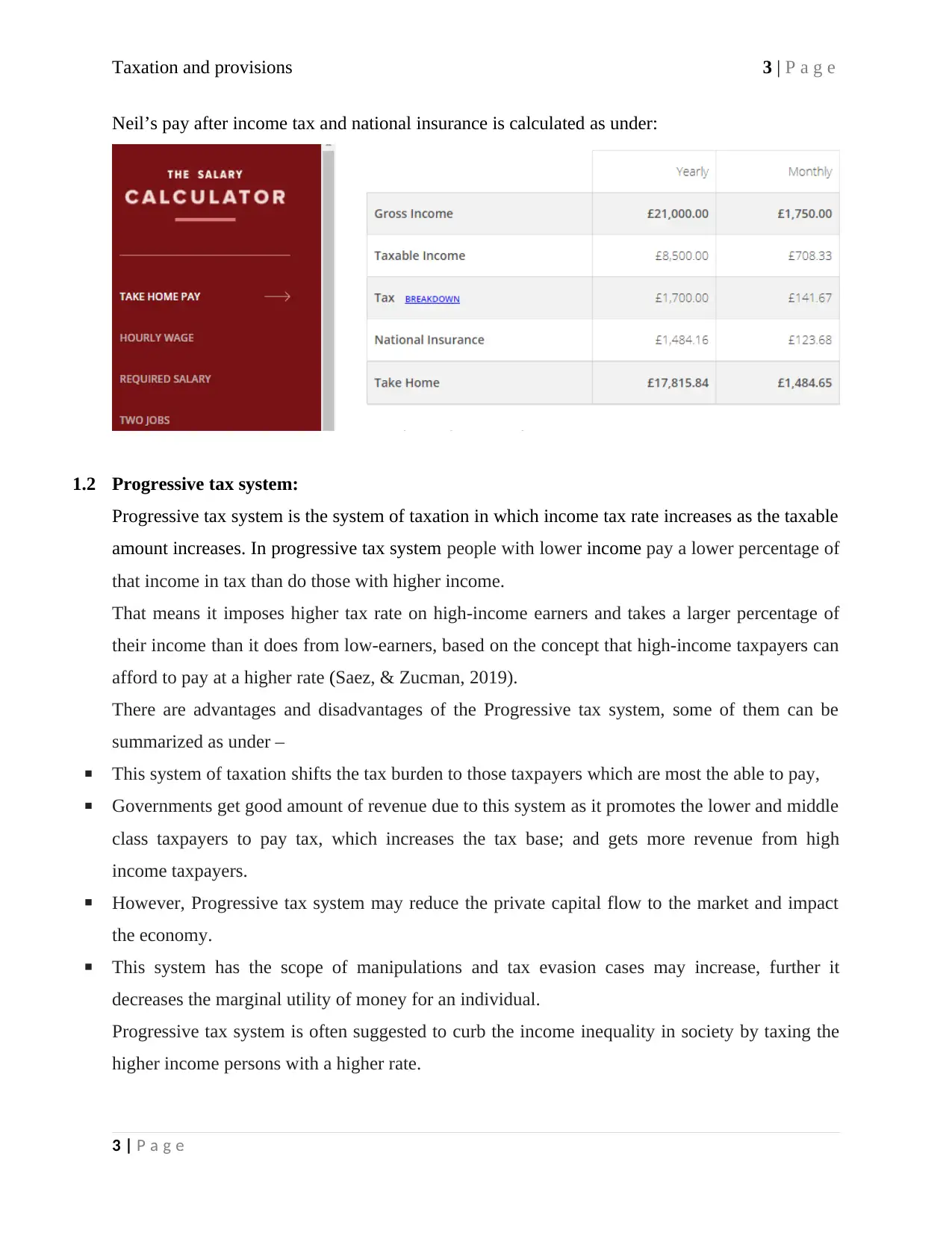

Neil’s pay after income tax and national insurance is calculated as under:

1.2 Progressive tax system:

Progressive tax system is the system of taxation in which income tax rate increases as the taxable

amount increases. In progressive tax system people with lower income pay a lower percentage of

that income in tax than do those with higher income.

That means it imposes higher tax rate on high-income earners and takes a larger percentage of

their income than it does from low-earners, based on the concept that high-income taxpayers can

afford to pay at a higher rate (Saez, & Zucman, 2019).

There are advantages and disadvantages of the Progressive tax system, some of them can be

summarized as under –

This system of taxation shifts the tax burden to those taxpayers which are most the able to pay,

Governments get good amount of revenue due to this system as it promotes the lower and middle

class taxpayers to pay tax, which increases the tax base; and gets more revenue from high

income taxpayers.

However, Progressive tax system may reduce the private capital flow to the market and impact

the economy.

This system has the scope of manipulations and tax evasion cases may increase, further it

decreases the marginal utility of money for an individual.

Progressive tax system is often suggested to curb the income inequality in society by taxing the

higher income persons with a higher rate.

3 | P a g e

Neil’s pay after income tax and national insurance is calculated as under:

1.2 Progressive tax system:

Progressive tax system is the system of taxation in which income tax rate increases as the taxable

amount increases. In progressive tax system people with lower income pay a lower percentage of

that income in tax than do those with higher income.

That means it imposes higher tax rate on high-income earners and takes a larger percentage of

their income than it does from low-earners, based on the concept that high-income taxpayers can

afford to pay at a higher rate (Saez, & Zucman, 2019).

There are advantages and disadvantages of the Progressive tax system, some of them can be

summarized as under –

This system of taxation shifts the tax burden to those taxpayers which are most the able to pay,

Governments get good amount of revenue due to this system as it promotes the lower and middle

class taxpayers to pay tax, which increases the tax base; and gets more revenue from high

income taxpayers.

However, Progressive tax system may reduce the private capital flow to the market and impact

the economy.

This system has the scope of manipulations and tax evasion cases may increase, further it

decreases the marginal utility of money for an individual.

Progressive tax system is often suggested to curb the income inequality in society by taxing the

higher income persons with a higher rate.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 4 | P a g e

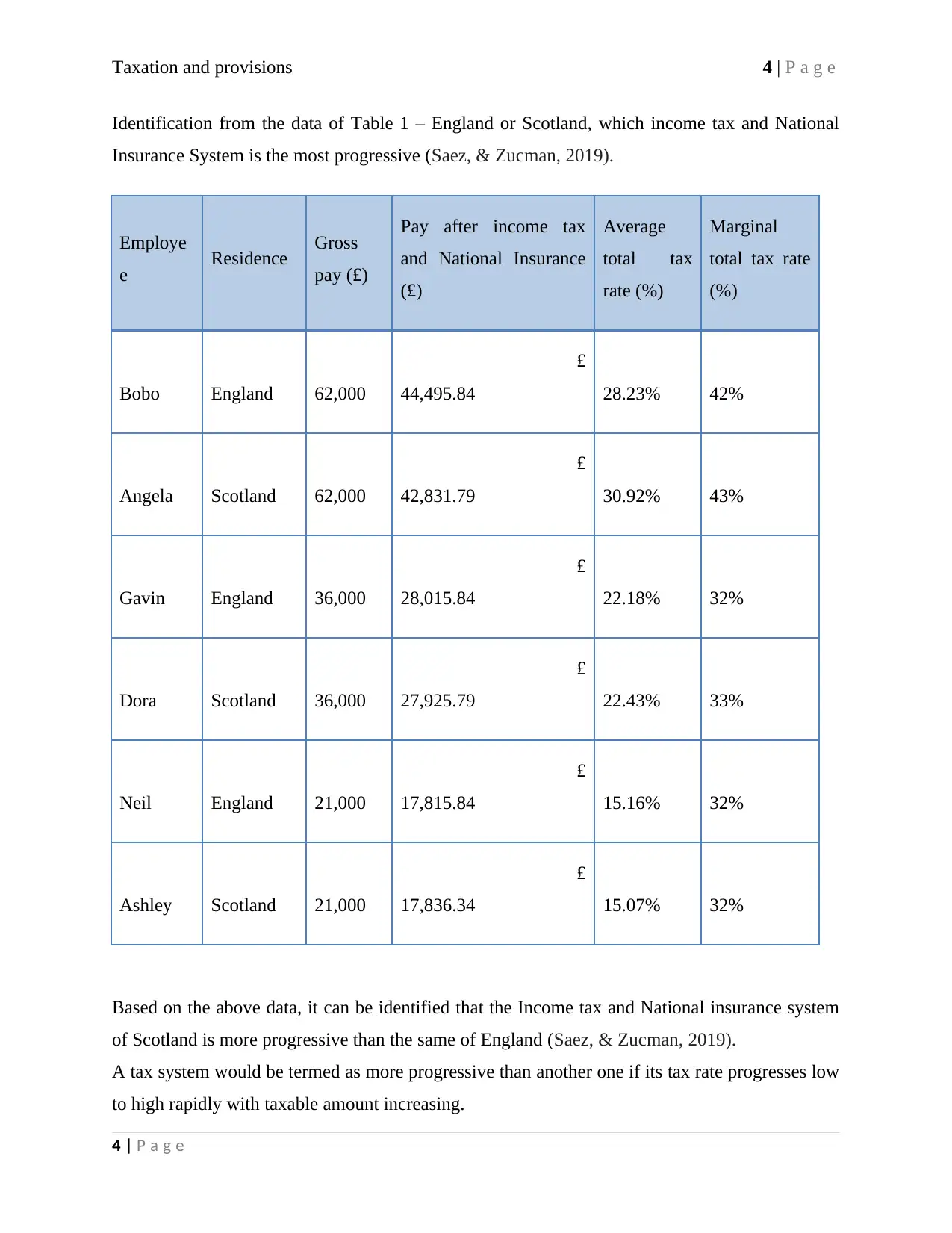

Identification from the data of Table 1 – England or Scotland, which income tax and National

Insurance System is the most progressive (Saez, & Zucman, 2019).

Employe

e Residence Gross

pay (£)

Pay after income tax

and National Insurance

(£)

Average

total tax

rate (%)

Marginal

total tax rate

(%)

Bobo England 62,000

£

44,495.84 28.23% 42%

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Gavin England 36,000

£

28,015.84 22.18% 32%

Dora Scotland 36,000

£

27,925.79 22.43% 33%

Neil England 21,000

£

17,815.84 15.16% 32%

Ashley Scotland 21,000

£

17,836.34 15.07% 32%

Based on the above data, it can be identified that the Income tax and National insurance system

of Scotland is more progressive than the same of England (Saez, & Zucman, 2019).

A tax system would be termed as more progressive than another one if its tax rate progresses low

to high rapidly with taxable amount increasing.

4 | P a g e

Identification from the data of Table 1 – England or Scotland, which income tax and National

Insurance System is the most progressive (Saez, & Zucman, 2019).

Employe

e Residence Gross

pay (£)

Pay after income tax

and National Insurance

(£)

Average

total tax

rate (%)

Marginal

total tax rate

(%)

Bobo England 62,000

£

44,495.84 28.23% 42%

Angela Scotland 62,000

£

42,831.79 30.92% 43%

Gavin England 36,000

£

28,015.84 22.18% 32%

Dora Scotland 36,000

£

27,925.79 22.43% 33%

Neil England 21,000

£

17,815.84 15.16% 32%

Ashley Scotland 21,000

£

17,836.34 15.07% 32%

Based on the above data, it can be identified that the Income tax and National insurance system

of Scotland is more progressive than the same of England (Saez, & Zucman, 2019).

A tax system would be termed as more progressive than another one if its tax rate progresses low

to high rapidly with taxable amount increasing.

4 | P a g e

Taxation and provisions 5 | P a g e

It can be observed from the above table that with the income increasing from £21000 to £36000,

average and marginal tax rates of Scotland progresses more than that of England. Further, tax

rate progresses again for employees with the gross annual salary of £62000, and employee

residing in Scotland pays tax at a higher average rate than the employee residing in England and

gap is wider at this higher income slab.

1.3 Median value of the gross earnings of the company’s employees in today’s money:

Median salary is the center of a range of employee’s salary arranged in order from least to

greatest.

Median gross earnings of the employees of Crossdigital Ltd is as follows-

Total number of employees: 6.

Average of 3rd and 4th amount in arranged range of data: £ 36.000.

In case of even number of employees, to calculate median salary, average of earnings is required

of the two middle employees arranged in least to greatest order on the basis of pay.

In case of Crossdigital Ltd, Average of 3rd and 4th earning data arranged accordingly, would be

the median gross pay i.e. £36,000 per annum.

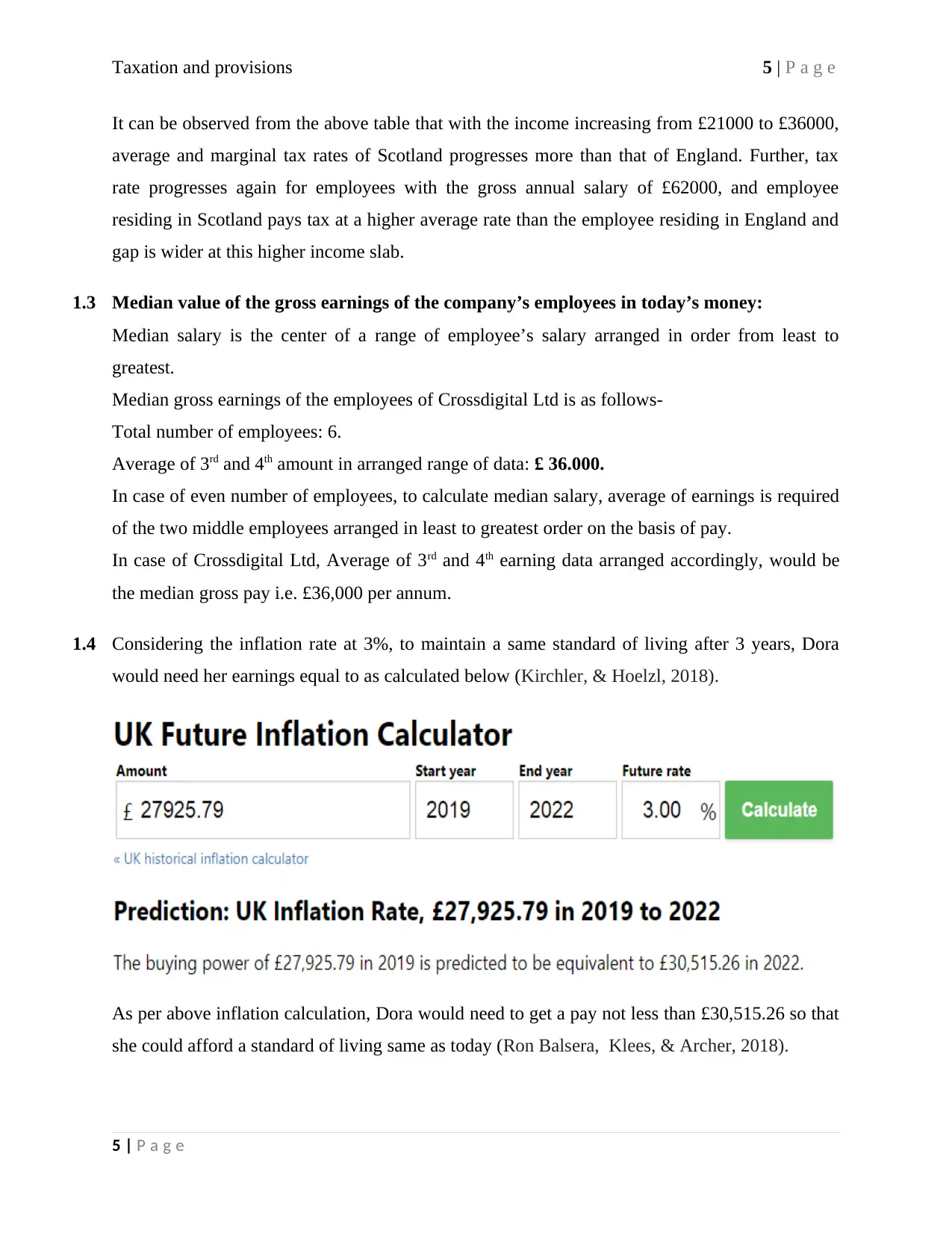

1.4 Considering the inflation rate at 3%, to maintain a same standard of living after 3 years, Dora

would need her earnings equal to as calculated below (Kirchler, & Hoelzl, 2018).

As per above inflation calculation, Dora would need to get a pay not less than £30,515.26 so that

she could afford a standard of living same as today (Ron Balsera, Klees, & Archer, 2018).

5 | P a g e

It can be observed from the above table that with the income increasing from £21000 to £36000,

average and marginal tax rates of Scotland progresses more than that of England. Further, tax

rate progresses again for employees with the gross annual salary of £62000, and employee

residing in Scotland pays tax at a higher average rate than the employee residing in England and

gap is wider at this higher income slab.

1.3 Median value of the gross earnings of the company’s employees in today’s money:

Median salary is the center of a range of employee’s salary arranged in order from least to

greatest.

Median gross earnings of the employees of Crossdigital Ltd is as follows-

Total number of employees: 6.

Average of 3rd and 4th amount in arranged range of data: £ 36.000.

In case of even number of employees, to calculate median salary, average of earnings is required

of the two middle employees arranged in least to greatest order on the basis of pay.

In case of Crossdigital Ltd, Average of 3rd and 4th earning data arranged accordingly, would be

the median gross pay i.e. £36,000 per annum.

1.4 Considering the inflation rate at 3%, to maintain a same standard of living after 3 years, Dora

would need her earnings equal to as calculated below (Kirchler, & Hoelzl, 2018).

As per above inflation calculation, Dora would need to get a pay not less than £30,515.26 so that

she could afford a standard of living same as today (Ron Balsera, Klees, & Archer, 2018).

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation and provisions 6 | P a g e

As per available data, Dora’s pay in 2022/23 after income tax and national insurance would rise

to £29,881, with this pay Dora could not maintain the purchasing power of £27,925.79 as that

would require a pay equivalent to £30,515.26 as calculated above; so it can be concluded that

Dora could afford a standard of living lower than as today.

Answer to question no. – 2

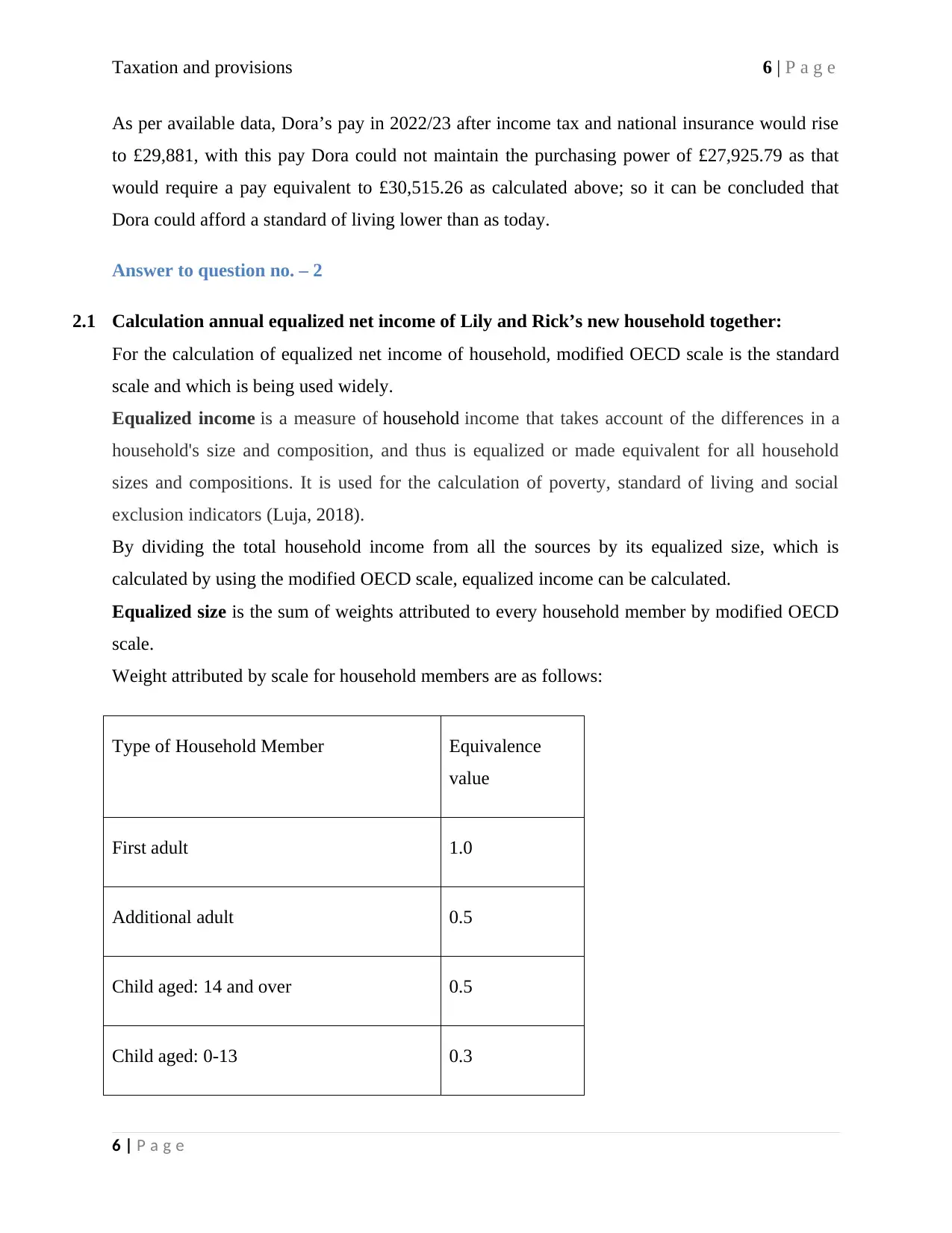

2.1 Calculation annual equalized net income of Lily and Rick’s new household together:

For the calculation of equalized net income of household, modified OECD scale is the standard

scale and which is being used widely.

Equalized income is a measure of household income that takes account of the differences in a

household's size and composition, and thus is equalized or made equivalent for all household

sizes and compositions. It is used for the calculation of poverty, standard of living and social

exclusion indicators (Luja, 2018).

By dividing the total household income from all the sources by its equalized size, which is

calculated by using the modified OECD scale, equalized income can be calculated.

Equalized size is the sum of weights attributed to every household member by modified OECD

scale.

Weight attributed by scale for household members are as follows:

Type of Household Member Equivalence

value

First adult 1.0

Additional adult 0.5

Child aged: 14 and over 0.5

Child aged: 0-13 0.3

6 | P a g e

As per available data, Dora’s pay in 2022/23 after income tax and national insurance would rise

to £29,881, with this pay Dora could not maintain the purchasing power of £27,925.79 as that

would require a pay equivalent to £30,515.26 as calculated above; so it can be concluded that

Dora could afford a standard of living lower than as today.

Answer to question no. – 2

2.1 Calculation annual equalized net income of Lily and Rick’s new household together:

For the calculation of equalized net income of household, modified OECD scale is the standard

scale and which is being used widely.

Equalized income is a measure of household income that takes account of the differences in a

household's size and composition, and thus is equalized or made equivalent for all household

sizes and compositions. It is used for the calculation of poverty, standard of living and social

exclusion indicators (Luja, 2018).

By dividing the total household income from all the sources by its equalized size, which is

calculated by using the modified OECD scale, equalized income can be calculated.

Equalized size is the sum of weights attributed to every household member by modified OECD

scale.

Weight attributed by scale for household members are as follows:

Type of Household Member Equivalence

value

First adult 1.0

Additional adult 0.5

Child aged: 14 and over 0.5

Child aged: 0-13 0.3

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 7 | P a g e

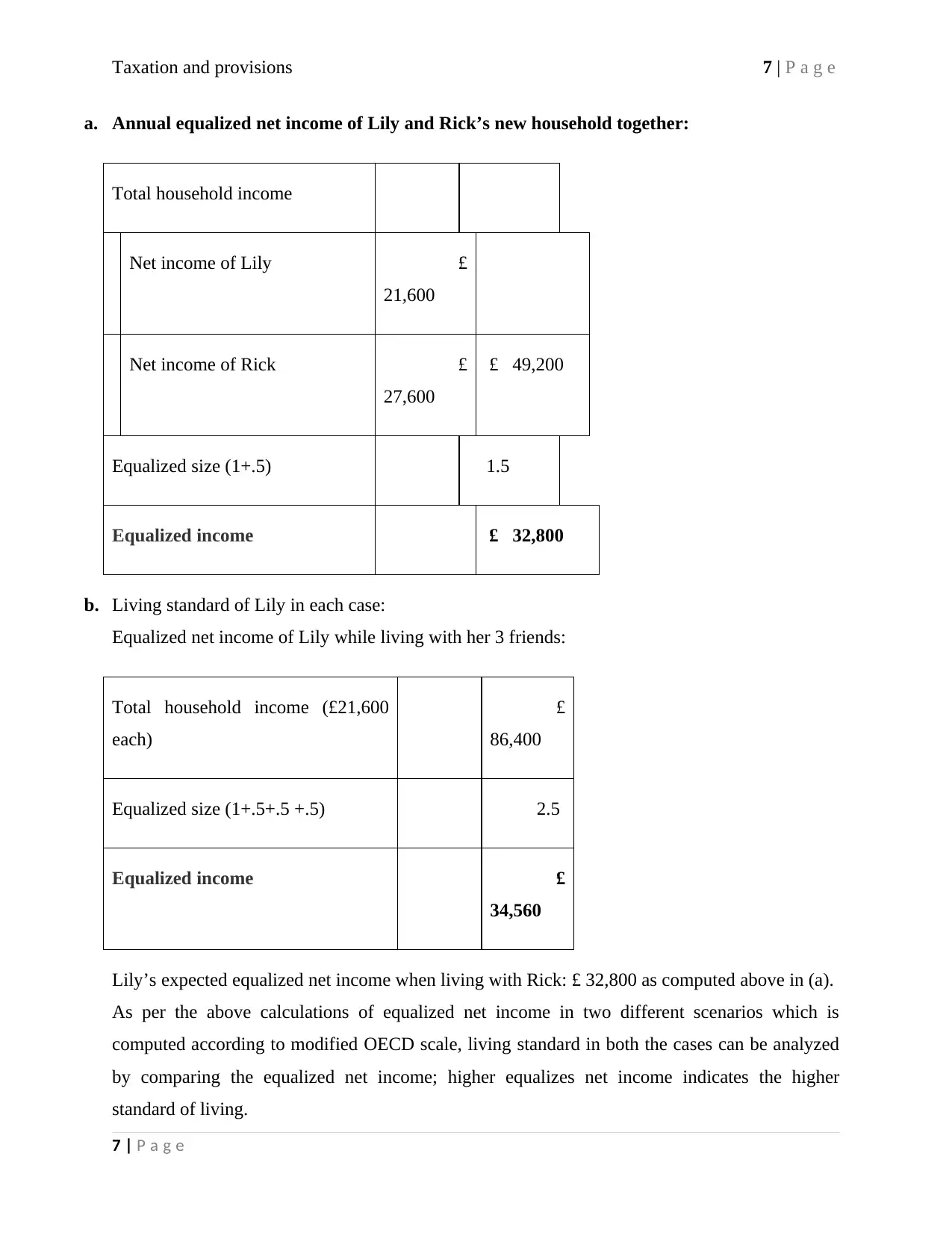

a. Annual equalized net income of Lily and Rick’s new household together:

Total household income

Net income of Lily £

21,600

Net income of Rick £

27,600

£ 49,200

Equalized size (1+.5) 1.5

Equalized income £ 32,800

b. Living standard of Lily in each case:

Equalized net income of Lily while living with her 3 friends:

Total household income (£21,600

each)

£

86,400

Equalized size (1+.5+.5 +.5) 2.5

Equalized income £

34,560

Lily’s expected equalized net income when living with Rick: £ 32,800 as computed above in (a).

As per the above calculations of equalized net income in two different scenarios which is

computed according to modified OECD scale, living standard in both the cases can be analyzed

by comparing the equalized net income; higher equalizes net income indicates the higher

standard of living.

7 | P a g e

a. Annual equalized net income of Lily and Rick’s new household together:

Total household income

Net income of Lily £

21,600

Net income of Rick £

27,600

£ 49,200

Equalized size (1+.5) 1.5

Equalized income £ 32,800

b. Living standard of Lily in each case:

Equalized net income of Lily while living with her 3 friends:

Total household income (£21,600

each)

£

86,400

Equalized size (1+.5+.5 +.5) 2.5

Equalized income £

34,560

Lily’s expected equalized net income when living with Rick: £ 32,800 as computed above in (a).

As per the above calculations of equalized net income in two different scenarios which is

computed according to modified OECD scale, living standard in both the cases can be analyzed

by comparing the equalized net income; higher equalizes net income indicates the higher

standard of living.

7 | P a g e

Taxation and provisions 8 | P a g e

As Lily’s equalized net income is higher while living with her friends (£34,560 compared to

£32,800), Lily has higher living standard than she could afford when living with Rick (Jalan, &

Vaidyanathan, 2017)

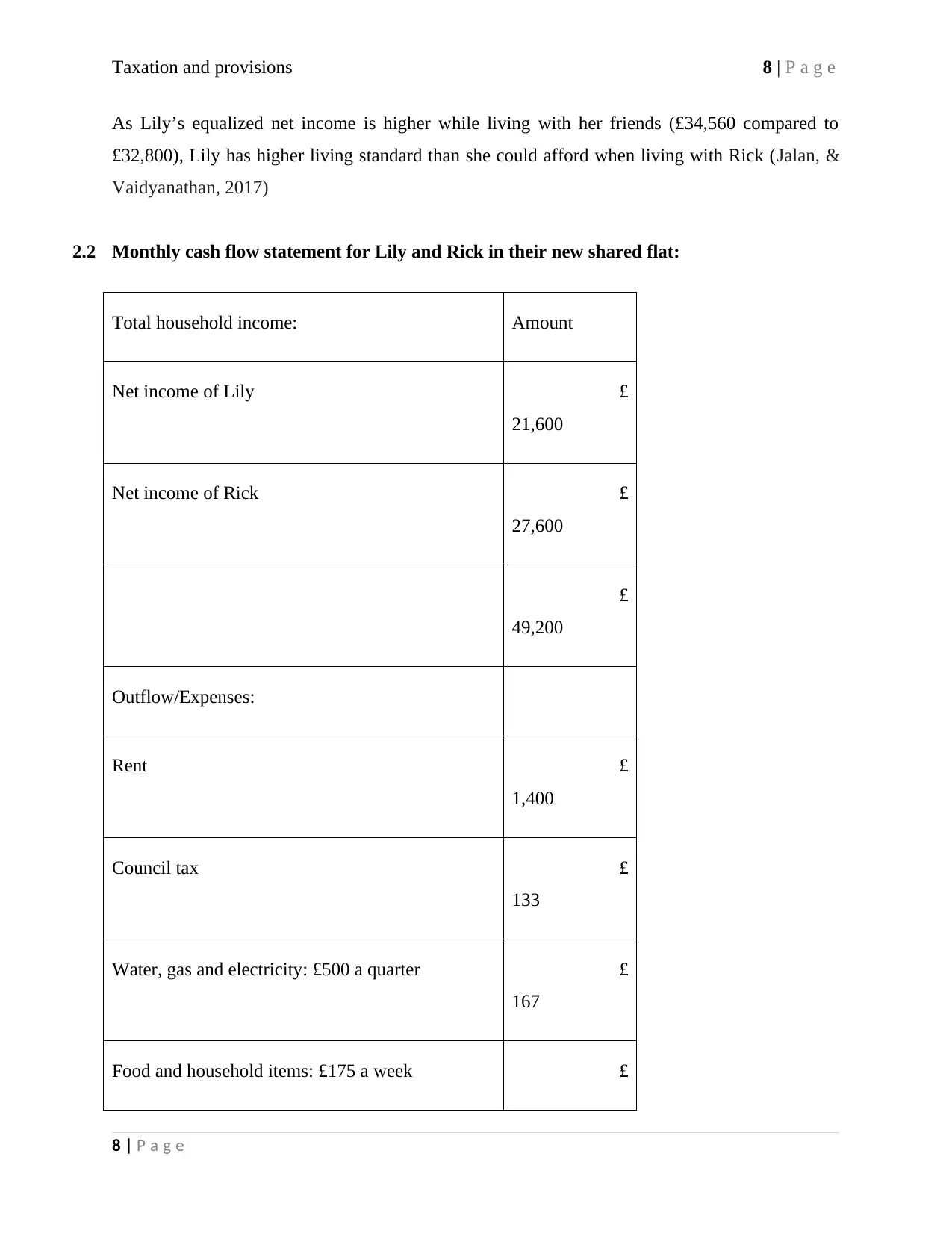

2.2 Monthly cash flow statement for Lily and Rick in their new shared flat:

Total household income: Amount

Net income of Lily £

21,600

Net income of Rick £

27,600

£

49,200

Outflow/Expenses:

Rent £

1,400

Council tax £

133

Water, gas and electricity: £500 a quarter £

167

Food and household items: £175 a week £

8 | P a g e

As Lily’s equalized net income is higher while living with her friends (£34,560 compared to

£32,800), Lily has higher living standard than she could afford when living with Rick (Jalan, &

Vaidyanathan, 2017)

2.2 Monthly cash flow statement for Lily and Rick in their new shared flat:

Total household income: Amount

Net income of Lily £

21,600

Net income of Rick £

27,600

£

49,200

Outflow/Expenses:

Rent £

1,400

Council tax £

133

Water, gas and electricity: £500 a quarter £

167

Food and household items: £175 a week £

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation and provisions 9 | P a g e

758

Alcohol, going out, leisure activities: £480 a

month

£

480

Phones and broadband: £108 a month £

108

Transport: £709 a month £

709

Other essentials: £262 a month £

262

£

4,017

Cash balance at the end of the month £

83

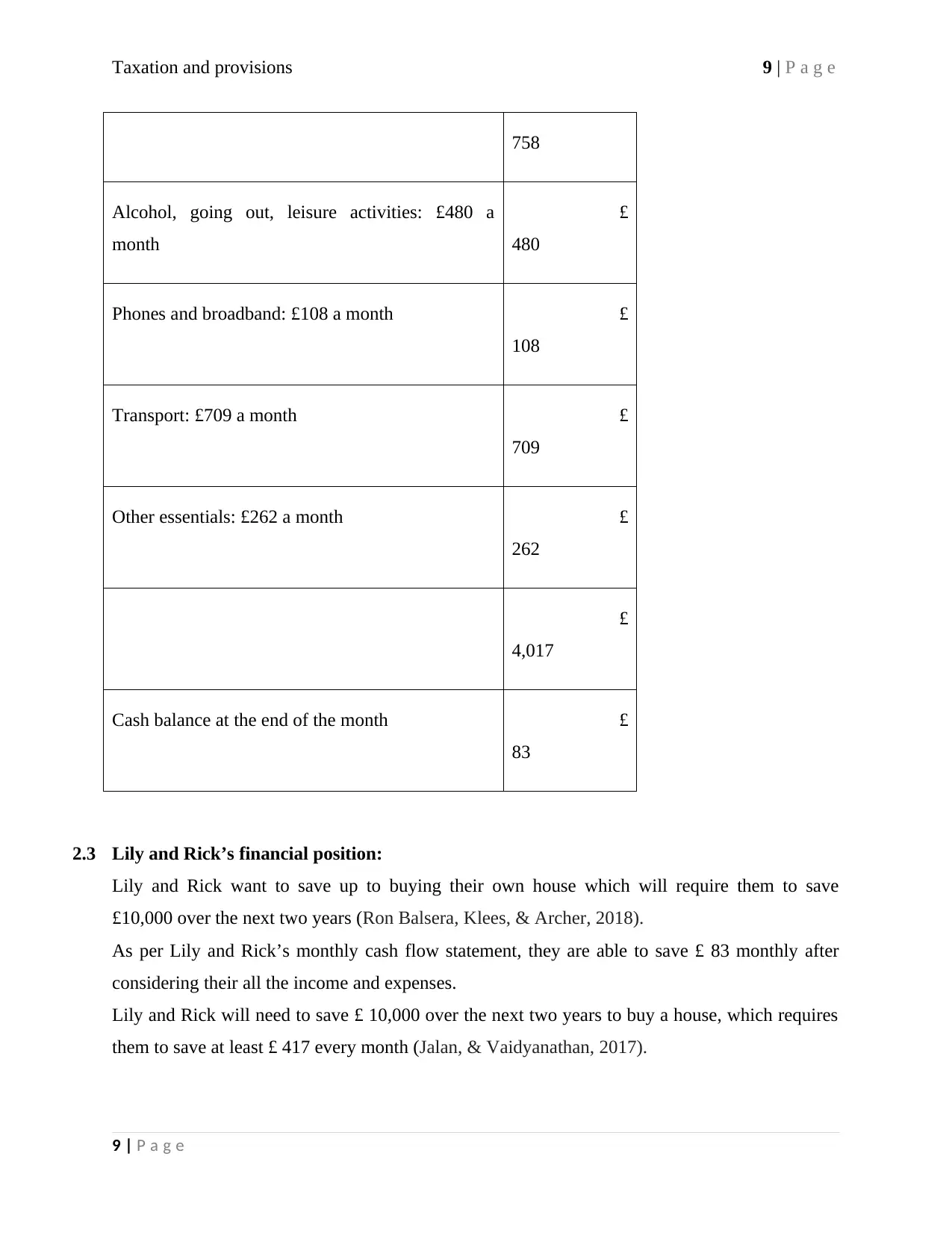

2.3 Lily and Rick’s financial position:

Lily and Rick want to save up to buying their own house which will require them to save

£10,000 over the next two years (Ron Balsera, Klees, & Archer, 2018).

As per Lily and Rick’s monthly cash flow statement, they are able to save £ 83 monthly after

considering their all the income and expenses.

Lily and Rick will need to save £ 10,000 over the next two years to buy a house, which requires

them to save at least £ 417 every month (Jalan, & Vaidyanathan, 2017).

9 | P a g e

758

Alcohol, going out, leisure activities: £480 a

month

£

480

Phones and broadband: £108 a month £

108

Transport: £709 a month £

709

Other essentials: £262 a month £

262

£

4,017

Cash balance at the end of the month £

83

2.3 Lily and Rick’s financial position:

Lily and Rick want to save up to buying their own house which will require them to save

£10,000 over the next two years (Ron Balsera, Klees, & Archer, 2018).

As per Lily and Rick’s monthly cash flow statement, they are able to save £ 83 monthly after

considering their all the income and expenses.

Lily and Rick will need to save £ 10,000 over the next two years to buy a house, which requires

them to save at least £ 417 every month (Jalan, & Vaidyanathan, 2017).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation and provisions 10 | P a g e

By comparing their expected monthly saving with required monthly saving to buy a house, it is

clear that they need to make some adjustments in their household expenses to save further £ 334

monthly. For saving £10,000 in next two years, they can consider the adjustments in non-

essential expenditures and may also consider shifting in a less expensive residence to cut short

their expenditures (Jalan, & Vaidyanathan, 2017).

The whole calculation can be understood from following table:

Required monthly saving (£ 10,000/24 months) £

417

Monthly saving according to current budget £

83

Additional monthly saving required £

334

Answer to question no. – 3

3.1 Michelle’s borrowing options:

Monthly

payment

Repaymen

t period

Total interest

paid

Option A £ 276.47 1 Year

£

317.64

Option B £ 50.00 10 Years

£

3,870.55

10 | P a g e

By comparing their expected monthly saving with required monthly saving to buy a house, it is

clear that they need to make some adjustments in their household expenses to save further £ 334

monthly. For saving £10,000 in next two years, they can consider the adjustments in non-

essential expenditures and may also consider shifting in a less expensive residence to cut short

their expenditures (Jalan, & Vaidyanathan, 2017).

The whole calculation can be understood from following table:

Required monthly saving (£ 10,000/24 months) £

417

Monthly saving according to current budget £

83

Additional monthly saving required £

334

Answer to question no. – 3

3.1 Michelle’s borrowing options:

Monthly

payment

Repaymen

t period

Total interest

paid

Option A £ 276.47 1 Year

£

317.64

Option B £ 50.00 10 Years

£

3,870.55

10 | P a g e

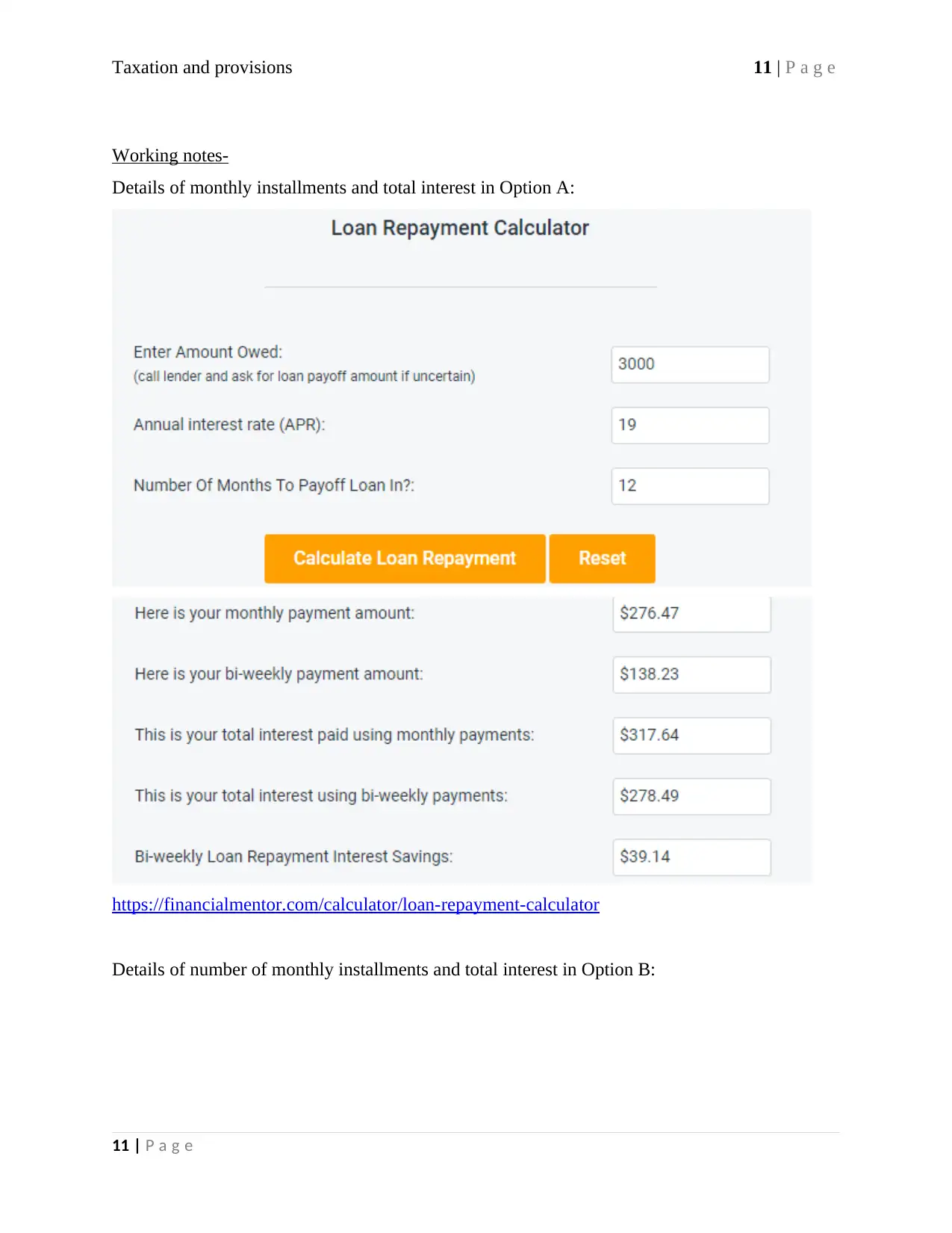

Taxation and provisions 11 | P a g e

Working notes-

Details of monthly installments and total interest in Option A:

https://financialmentor.com/calculator/loan-repayment-calculator

Details of number of monthly installments and total interest in Option B:

11 | P a g e

Working notes-

Details of monthly installments and total interest in Option A:

https://financialmentor.com/calculator/loan-repayment-calculator

Details of number of monthly installments and total interest in Option B:

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.