Corporate Financial Management: Analysis of DDR Stock Performance

VerifiedAdded on 2023/01/03

|10

|1142

|43

Report

AI Summary

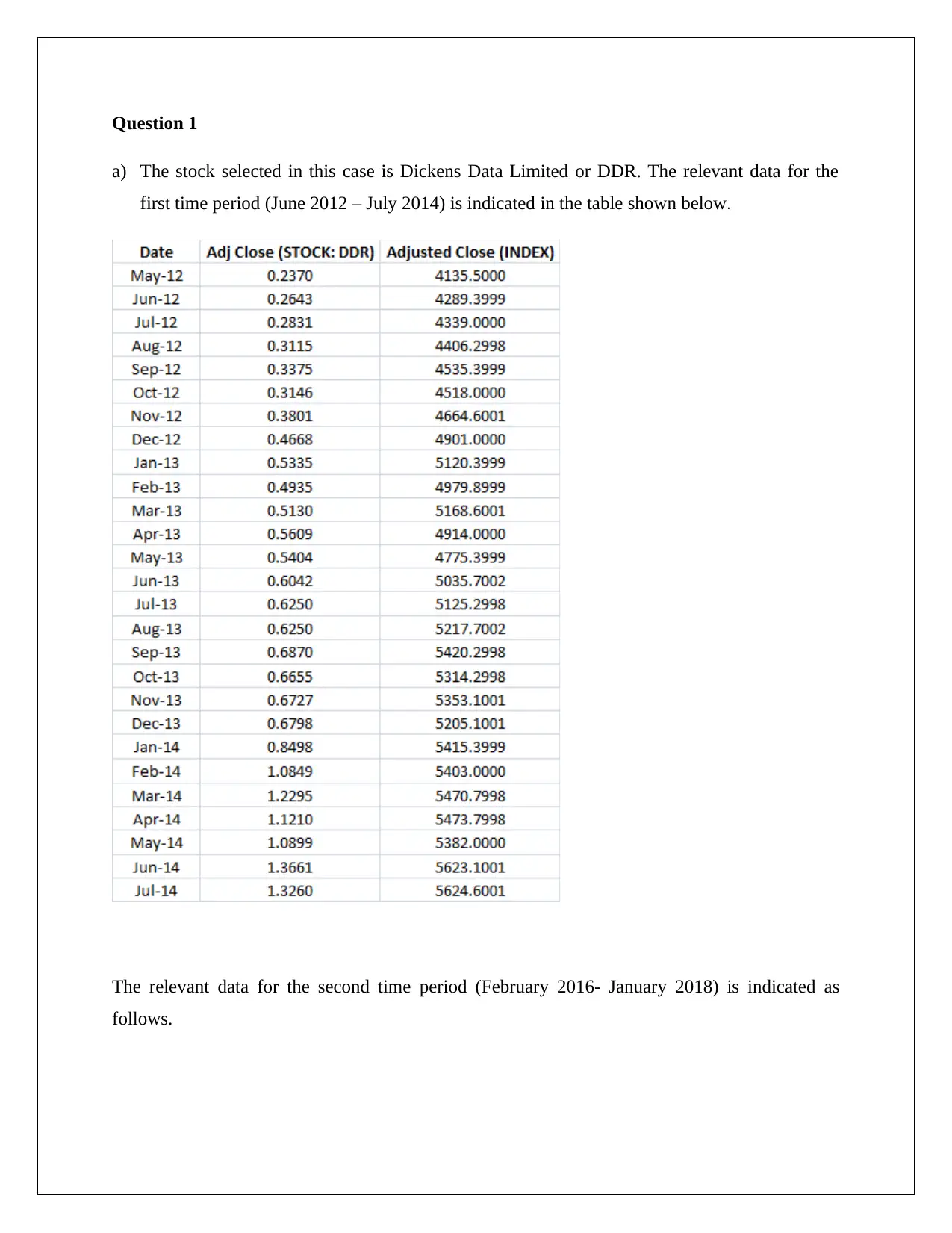

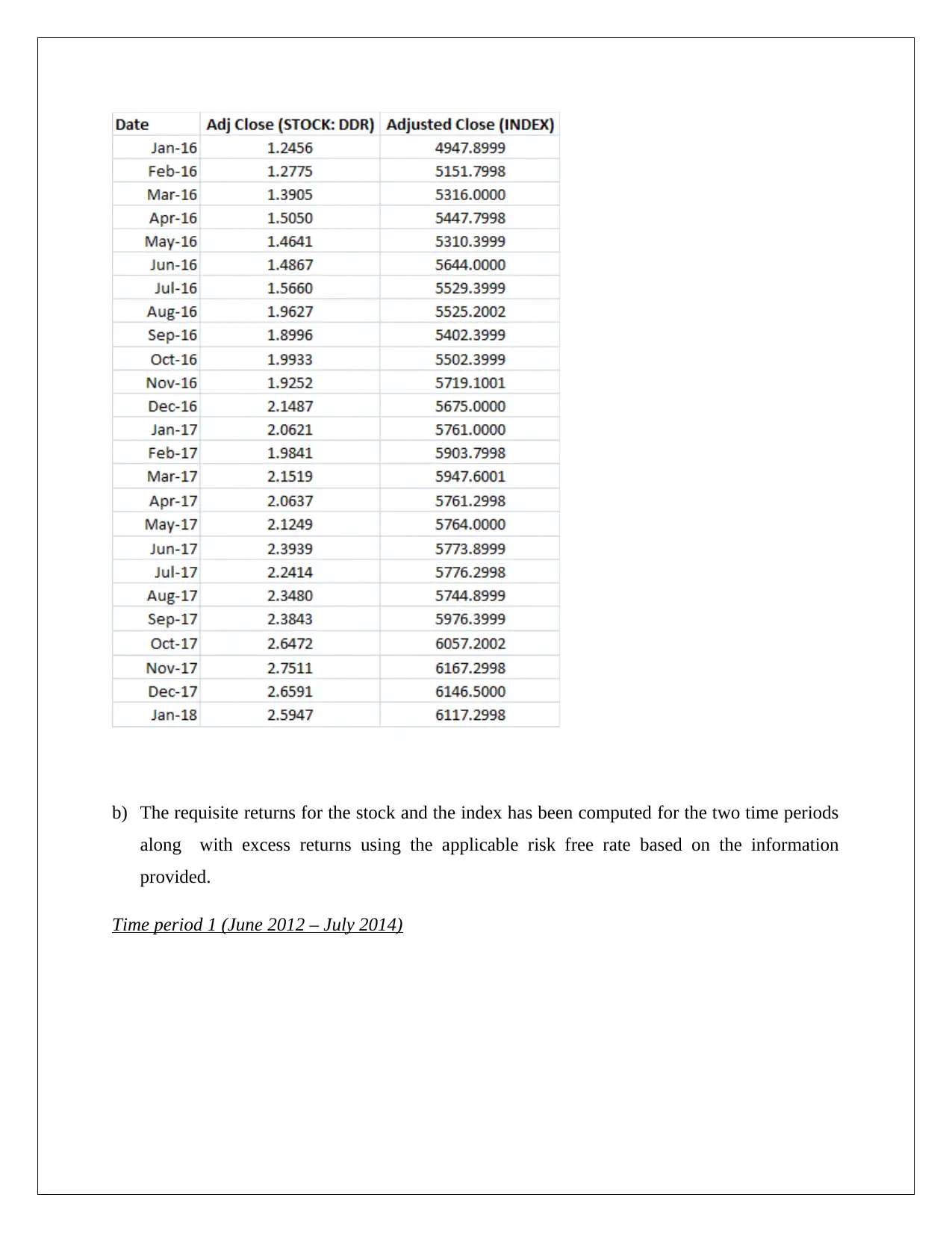

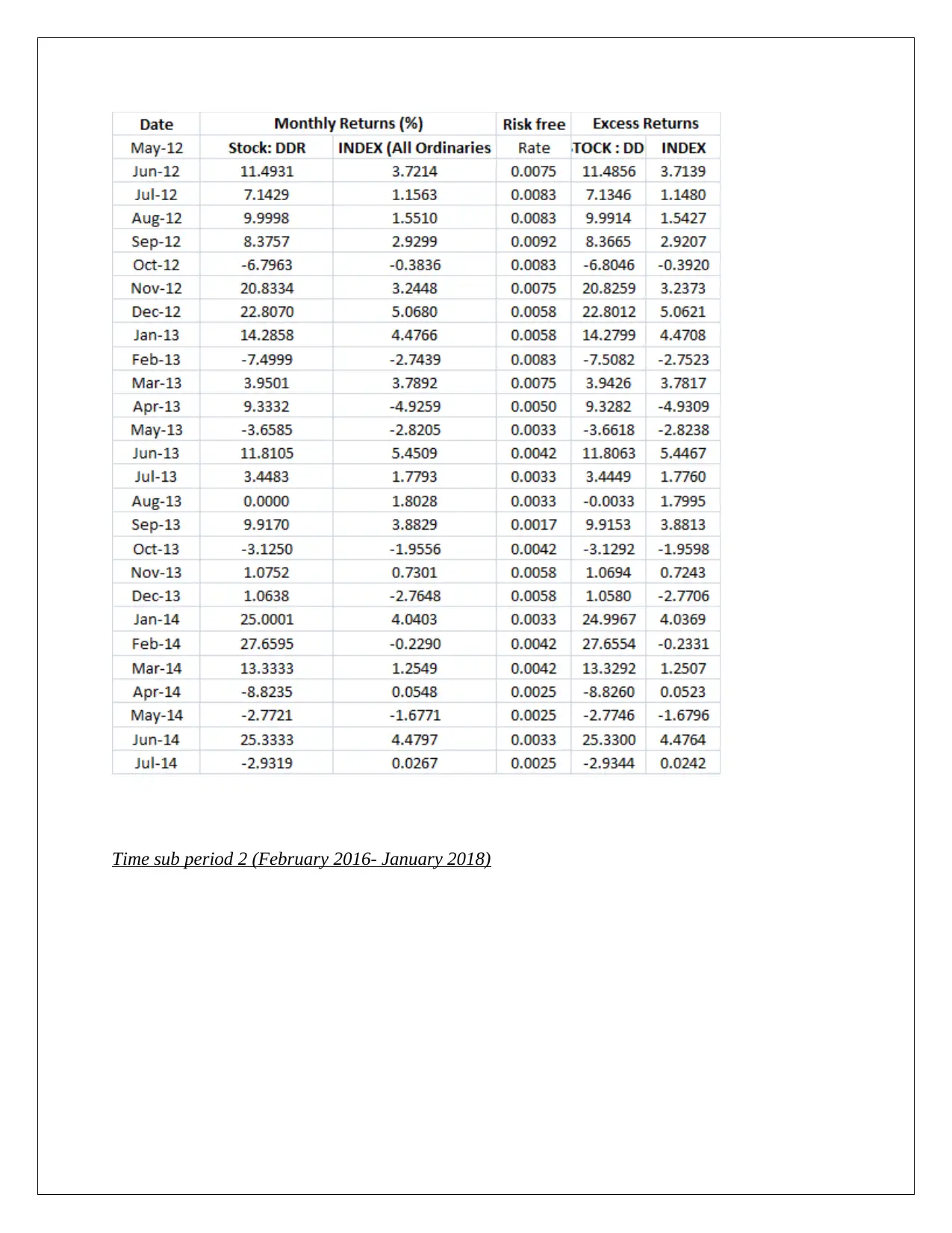

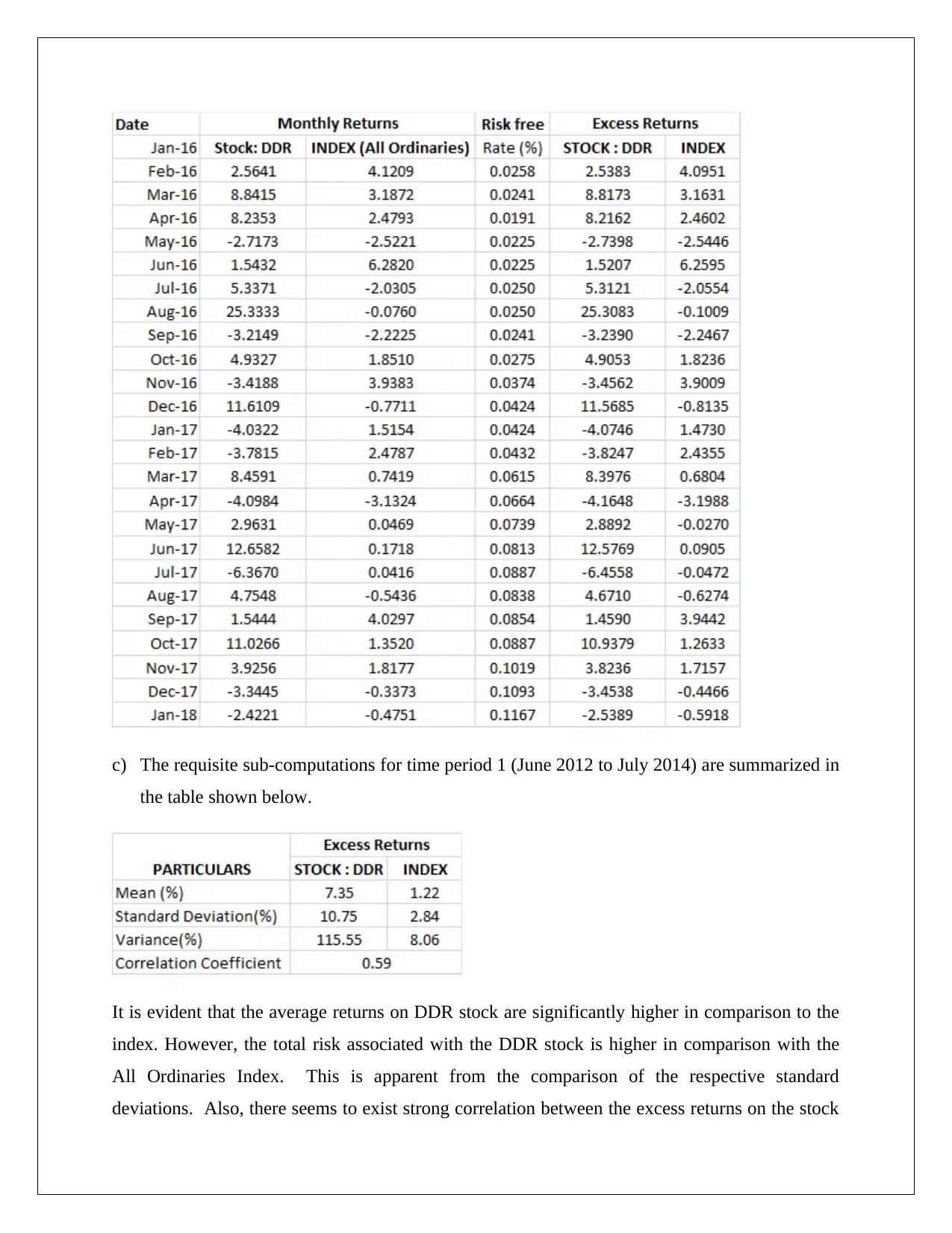

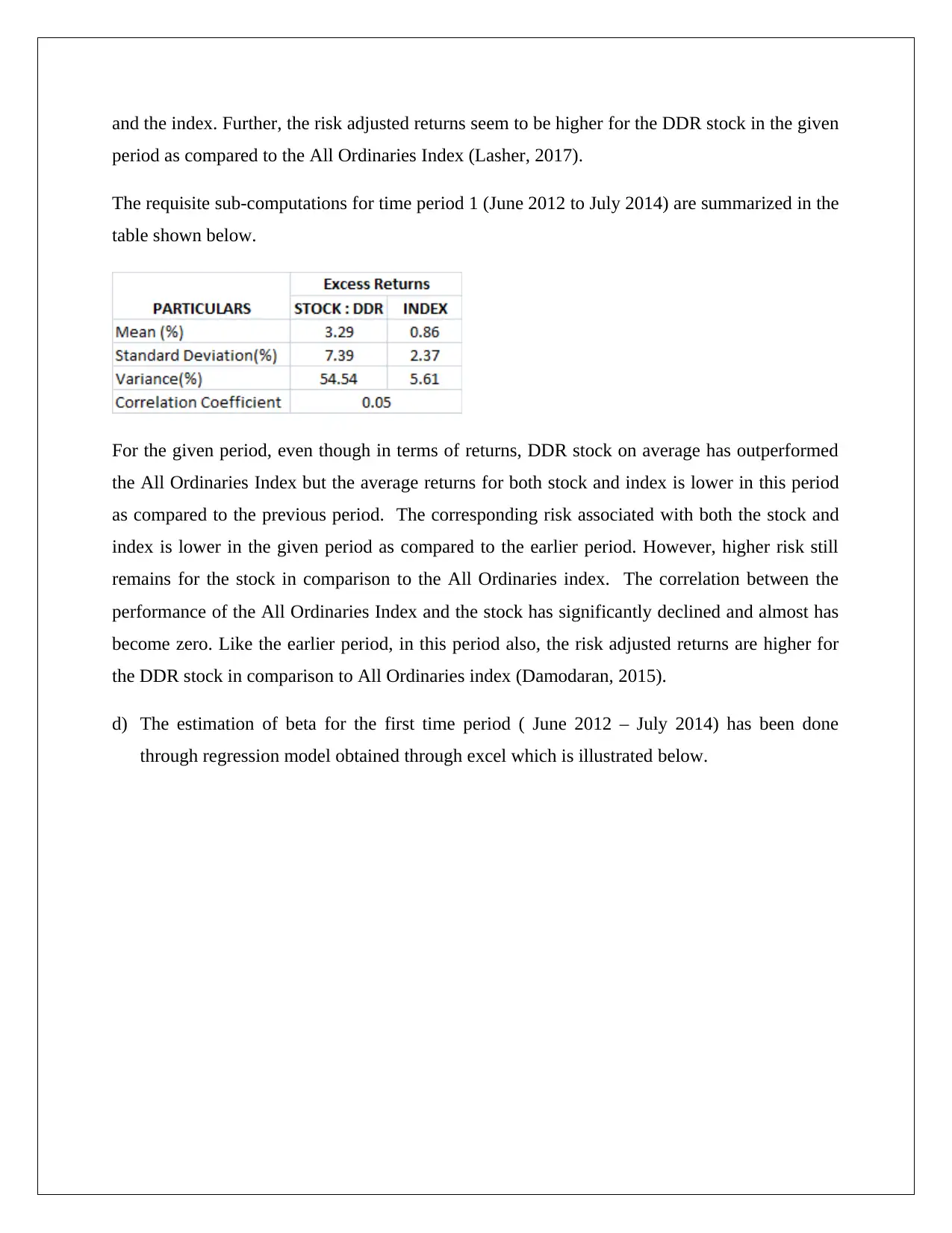

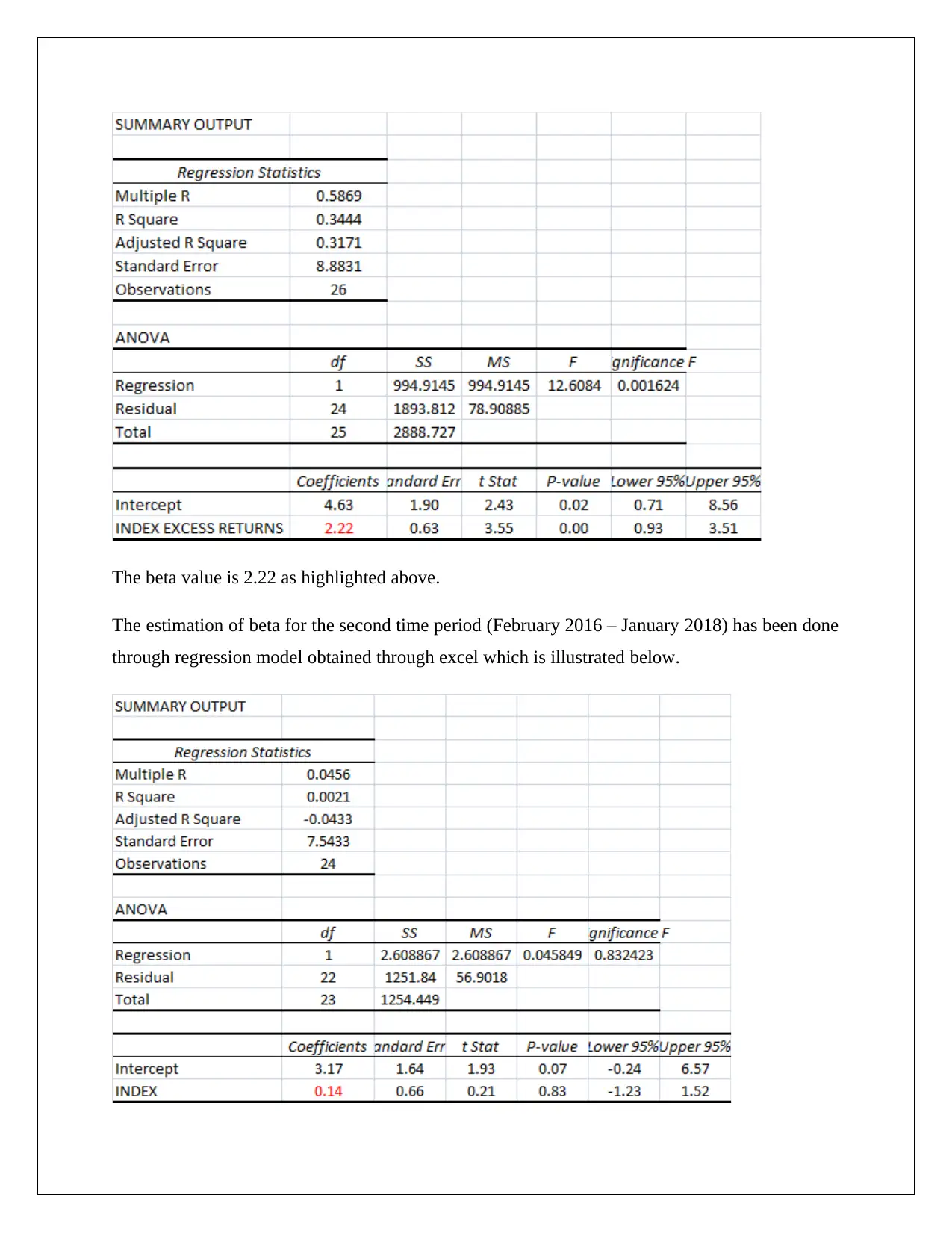

This report analyzes the performance of Dickens Data Limited (DDR) stock over two time periods: June 2012 – July 2014 and February 2016 – January 2018. The analysis includes calculating stock and market returns, excess returns, and risk-free rates. The report computes mean, standard deviation, variance, and correlation coefficients for DDR stock and the All Ordinaries Index. It also estimates the beta for both periods using regression analysis and interprets the results in terms of systematic risk and stock behavior. The report provides an overview of DickerData Limited's business, market capitalization, and its relationship with branded product vendors. Finally, it discusses the limitations of the CAPM model and the implications of the changing beta values across the two periods, emphasizing the importance of considering unsystematic risk and correlation between market and stock returns. The report concludes that the beta value in the second case is not correct, since the correlation between the market returns and the stock returns are close to zero.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.