Optimal Hedging Strategies for Swiss Exporters Post Franc De-pegging

VerifiedAdded on 2023/06/04

|9

|1617

|214

Report

AI Summary

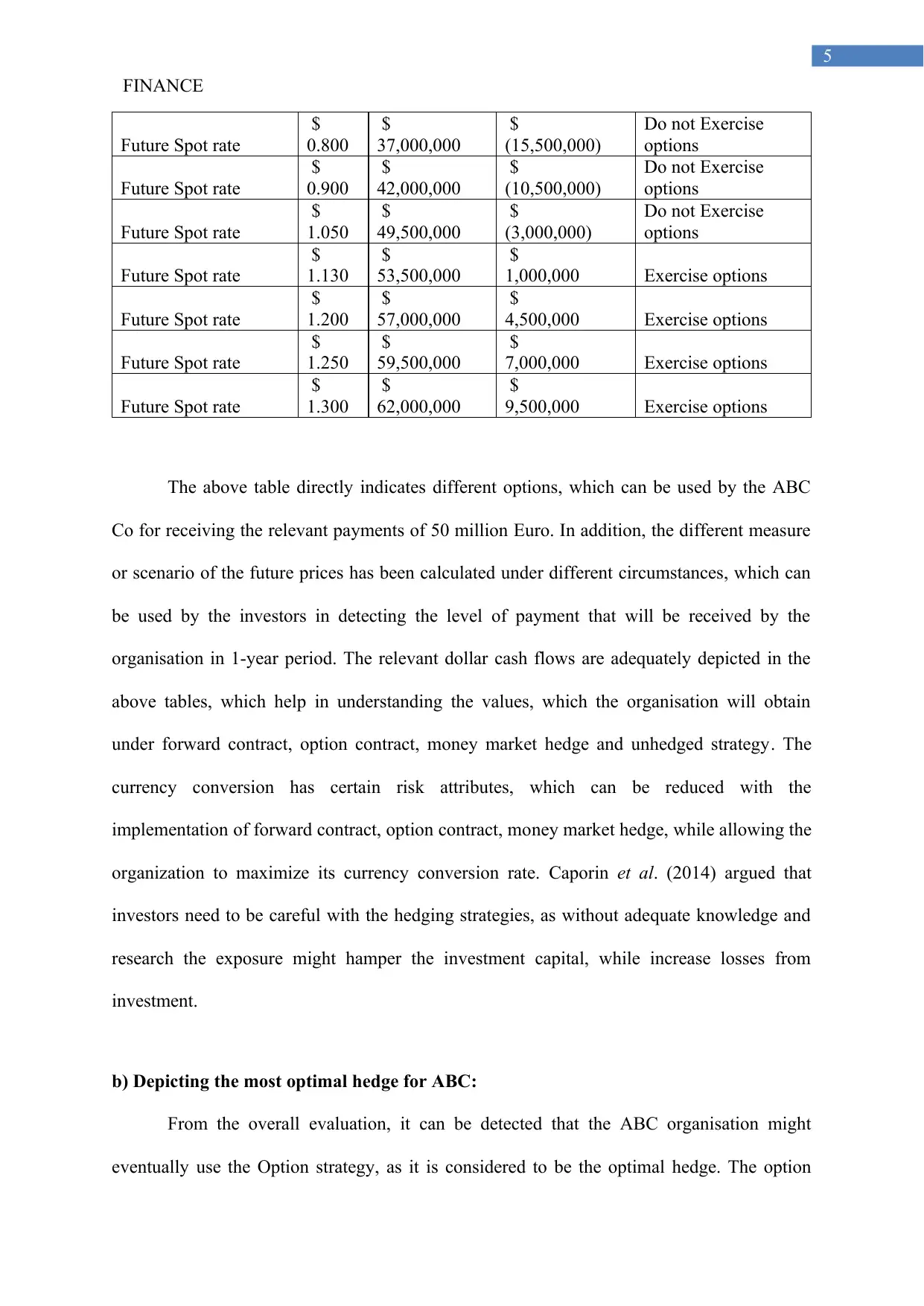

This report analyzes the Swiss Franc's de-pegging in 2015, triggered by the Swiss Central Bank's devaluation strategy and citizen protests. It examines the impact on Swiss exporters and domestic firms, evaluating various hedging strategies including unhedged, forward contract, money market hedge, and option hedge approaches. The analysis assesses each strategy's profitability and risk under different future spot rate scenarios. Ultimately, the report identifies the option strategy as the most optimal hedge for ABC Co, minimizing potential losses compared to other methods. Desklib offers a wide array of solved assignments and past papers for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.