Deakin University MAA303 Audit and Assurance Case Study: Morris Ltd

VerifiedAdded on 2022/08/29

|10

|1554

|13

Case Study

AI Summary

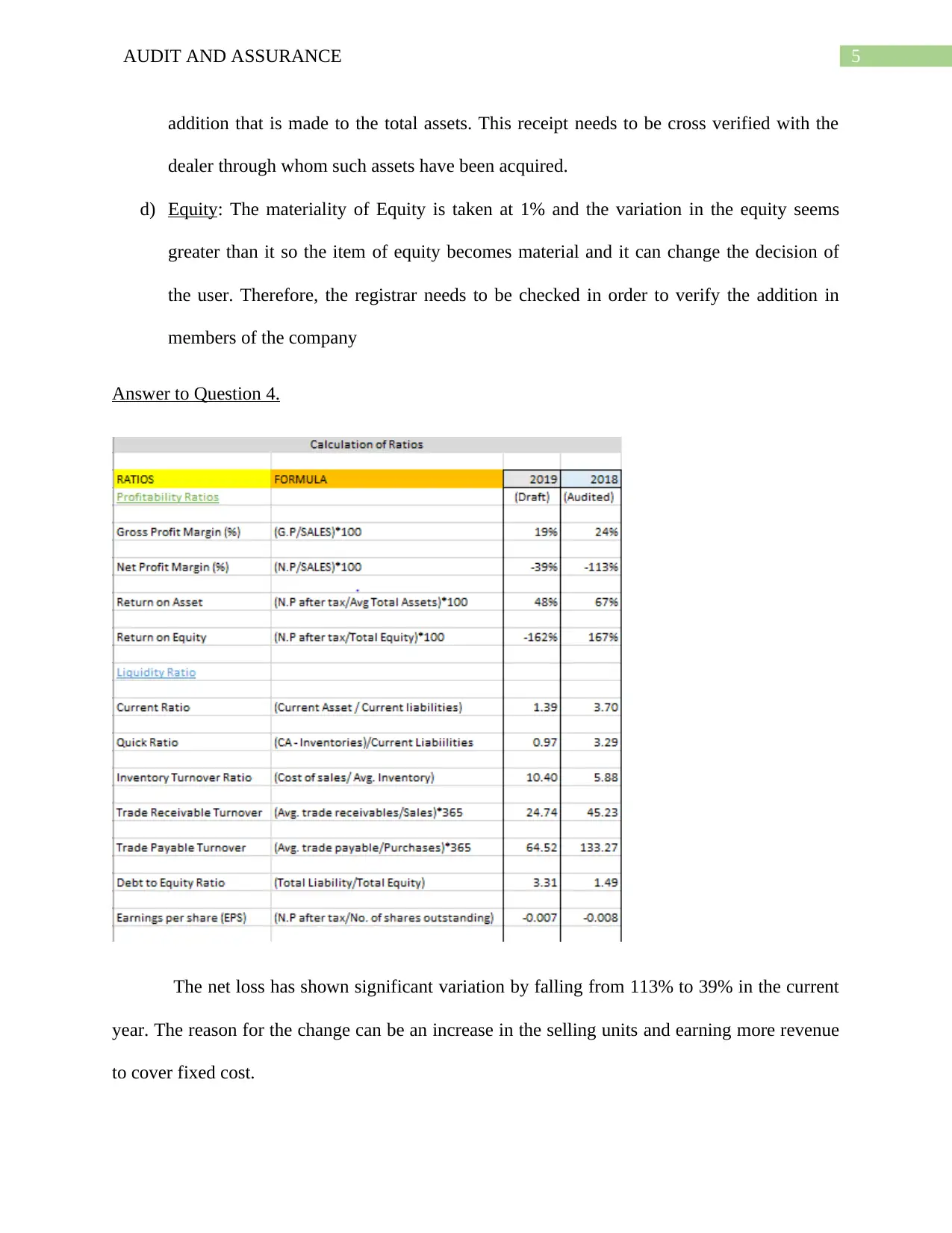

This case study analyzes the audit and assurance aspects of Morris Ltd, a company dealing in herbal medicines experiencing financial losses. The report examines the company's efforts to expand, including bonus schemes and capital raising, and assesses its current performance. It applies auditing standards, particularly ASA 315, and discusses analytical procedures, professional skepticism, and materiality in the context of the audit. The case study evaluates key financial ratios, the going concern assumption, and potential risks like contingent liabilities and inadequate accounting records. The report concludes that while the company faces challenges, management is taking steps to improve its financial position. The analysis includes recommendations for the auditor regarding risk assessment, materiality levels, and evaluation of the company's ability to continue as a going concern. The report uses financial data and analytical procedures to assess the company's financial health and potential for future success.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.