Report: Derivative and Fixed Income Securities Analysis - MAF308

VerifiedAdded on 2023/06/07

|6

|639

|381

Report

AI Summary

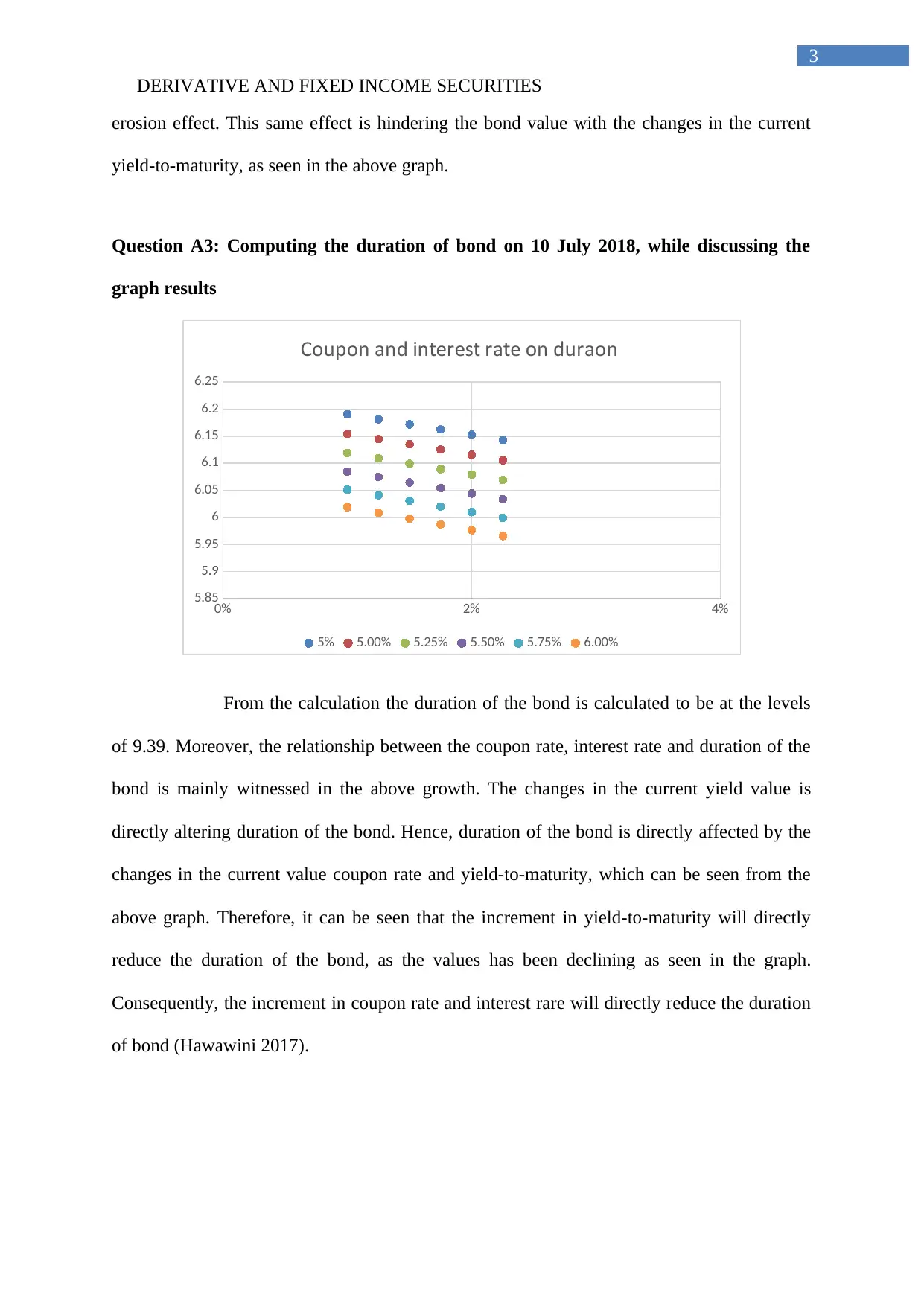

This report analyzes derivative and fixed income securities, focusing on bond pricing, yield-to-maturity, and duration. It begins with calculating the cash price of a bond on specific dates, followed by a graphical representation and discussion of the relationship between bond price and yield. The report also computes the duration of the bond, considering the effects of coupon rates and interest rates. The analysis uses calculations to determine the duration of the bond and how these factors affect the bond's value, referencing academic literature to support its findings. The report aims to demonstrate an understanding of key concepts in fixed income securities within the context of a MAF308 assignment at Deakin University.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.