Deakin Uni MAA262 - Management Accounting: Costing & Ethics Report

VerifiedAdded on 2023/04/19

|15

|2799

|421

Report

AI Summary

This report provides an overview of various management accounting concepts, including ethical standards provided by the IMA, classification of quality costs, calculation of predetermined overhead rates, application of the high-low method, and pricing techniques. It analyzes the ethical standards of competence, confidentiality, integrity, and credibility, using a statement by the founder of Virgin Groups as an example. The report also classifies costs into prevention, appraisal, internal failure, and external failure categories, analyzing their behavior over time. Furthermore, it calculates predetermined overhead rates for assembly and painting, determines total manufacturing costs, and applies the high-low method to shipping expenses. The report concludes by discussing the limitations of cost-plus pricing and the advantages of value-based pricing, offering a comprehensive understanding of management accounting principles. Desklib offers a range of study tools and resources for students.

Accounting 1

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 2

Table of Contents

Introduction......................................................................................................................................3

Question 1: Ethical Standards Provided by IMA............................................................................4

Question 2: Quality Costs................................................................................................................5

(a) Classification of Costs into Four Types of Quality Costs......................................................5

(b) Example of an Appraisal Cost................................................................................................6

(c) Analysis of behavior of Four Types of Costs.........................................................................6

Question 3: Valuation of Overheads Rates......................................................................................7

(a) Calculation of Predetermined Overhead Rates used for Assembly and Painting...................7

(b) Valuation of Total Overhead Cost for Job 105......................................................................7

(c) Valuation of Total Manufacturing Cost for Job 105..............................................................7

(d) Calculation of Unit Product Cost for Job 105........................................................................8

(e) Impact of Change in Manufacturing Overhead for Painting..................................................8

Question 4: Application of High-Low Method...............................................................................8

(a) Cost Formula for Shipping Expense using High-Low Method..............................................8

(b) Reasons of Difference between Actual Delivery Expenses and Estimated Delivery

Expenses.......................................................................................................................................9

(c) Contribution Format Income Statement...............................................................................10

Question 5:.....................................................................................................................................10

(a) Valuation of Predetermined Overhead Rate.........................................................................10

(b) Amount of Over-applied or Under-applied Overheads........................................................10

(c) Implications of Having Large Over-applied or Under-applied Overheads..........................11

Question 6: Pricing Techniques.....................................................................................................11

(a) Limitations of Cost-plus Pricing...........................................................................................11

(b) Value Based Pricing Technique...........................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................3

Question 1: Ethical Standards Provided by IMA............................................................................4

Question 2: Quality Costs................................................................................................................5

(a) Classification of Costs into Four Types of Quality Costs......................................................5

(b) Example of an Appraisal Cost................................................................................................6

(c) Analysis of behavior of Four Types of Costs.........................................................................6

Question 3: Valuation of Overheads Rates......................................................................................7

(a) Calculation of Predetermined Overhead Rates used for Assembly and Painting...................7

(b) Valuation of Total Overhead Cost for Job 105......................................................................7

(c) Valuation of Total Manufacturing Cost for Job 105..............................................................7

(d) Calculation of Unit Product Cost for Job 105........................................................................8

(e) Impact of Change in Manufacturing Overhead for Painting..................................................8

Question 4: Application of High-Low Method...............................................................................8

(a) Cost Formula for Shipping Expense using High-Low Method..............................................8

(b) Reasons of Difference between Actual Delivery Expenses and Estimated Delivery

Expenses.......................................................................................................................................9

(c) Contribution Format Income Statement...............................................................................10

Question 5:.....................................................................................................................................10

(a) Valuation of Predetermined Overhead Rate.........................................................................10

(b) Amount of Over-applied or Under-applied Overheads........................................................10

(c) Implications of Having Large Over-applied or Under-applied Overheads..........................11

Question 6: Pricing Techniques.....................................................................................................11

(a) Limitations of Cost-plus Pricing...........................................................................................11

(b) Value Based Pricing Technique...........................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Accounting 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 4

Introduction

The purpose of this report is development of secondary knowledge about different concepts

related to management accounting. This report will help to understand ethical standard provided

by IMA. Further the report focus on developing practical knowledge about classification of

available different types of activities into four types of quality costs. It will facilitate example of

an appraisal cost. Further section of this report will focus on understanding about calculation of

predetermined overhead rates for given data. Apart from this, the report will also focus on

application of high-low method for cost valuation. Final section of this report will focus on

identifying different limitations of cost plus pricing method. It will also help to understand the

value based pricing technique adopted by different organizations.

Introduction

The purpose of this report is development of secondary knowledge about different concepts

related to management accounting. This report will help to understand ethical standard provided

by IMA. Further the report focus on developing practical knowledge about classification of

available different types of activities into four types of quality costs. It will facilitate example of

an appraisal cost. Further section of this report will focus on understanding about calculation of

predetermined overhead rates for given data. Apart from this, the report will also focus on

application of high-low method for cost valuation. Final section of this report will focus on

identifying different limitations of cost plus pricing method. It will also help to understand the

value based pricing technique adopted by different organizations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 5

Question 1: Ethical Standards Provided by IMA

The detailed analysis of ethical standards provided by IMA for code of conduct of management

accountants is as below:

Competence: According to this standard, all the management accountants have to perform their

duties and responsibilities in accordance to technical standards, regulations and laws. They

should maintain proper efforts and professional expertise for consistent development of skills

and knowledge (IMA, 2019).

Confidentiality: According to this standard, it is duty of management accountants to ensure

confidentiality of any facts or information unless they are authorized to disclose it. They should

never use any confidential information for illegal or unethical advantage (IMA, 2019). They

should also communicate activities of subordinates and others to use the confidential information

in proper way.

Integrity: According to standard of integrity, proper communication is important with the

business associates for avoiding any conflict of interest (IMA, 2019). They should not support

any activity, which supports the discredit of profession.

Credibility: Every information should be communicated objectively and credibly. It is important

to disclose every fact and information, which may affect understanding of the user of a report or

document. It is also important to disclose the deficiencies or delays of processing’s, timelines,

information or internal controls in accordance to applicable laws and policies of the

organizations (IMA, 2019).

The founder of Virgin Groups has provided statement that “If somebody offers you an amazing

opportunity but you are not sure you can do it, say yes – then learn how to do it later! ”. In this

Question 1: Ethical Standards Provided by IMA

The detailed analysis of ethical standards provided by IMA for code of conduct of management

accountants is as below:

Competence: According to this standard, all the management accountants have to perform their

duties and responsibilities in accordance to technical standards, regulations and laws. They

should maintain proper efforts and professional expertise for consistent development of skills

and knowledge (IMA, 2019).

Confidentiality: According to this standard, it is duty of management accountants to ensure

confidentiality of any facts or information unless they are authorized to disclose it. They should

never use any confidential information for illegal or unethical advantage (IMA, 2019). They

should also communicate activities of subordinates and others to use the confidential information

in proper way.

Integrity: According to standard of integrity, proper communication is important with the

business associates for avoiding any conflict of interest (IMA, 2019). They should not support

any activity, which supports the discredit of profession.

Credibility: Every information should be communicated objectively and credibly. It is important

to disclose every fact and information, which may affect understanding of the user of a report or

document. It is also important to disclose the deficiencies or delays of processing’s, timelines,

information or internal controls in accordance to applicable laws and policies of the

organizations (IMA, 2019).

The founder of Virgin Groups has provided statement that “If somebody offers you an amazing

opportunity but you are not sure you can do it, say yes – then learn how to do it later! ”. In this

Accounting 6

statement, different ethical standards of IMA are jeopardized such as standard of competence,

standard of integrity and the standard of credibility. Standard of competence is jeopardized,

because statement is asking people to say yes to a job, even if they don’t have competence

required for a particular job. In addition to this standard of integrity is also jeopardized, because

there is lack of communication about real facts between the two parties (IMA, 2019). This type

of communication can cause conflict of interest in upcoming period, when the actual work is

required from people. Similar to this, the standard of credibility if also jeopardized in above

statement, which it fails to disclose every fact and information, which can affect understanding

and decision of another party.

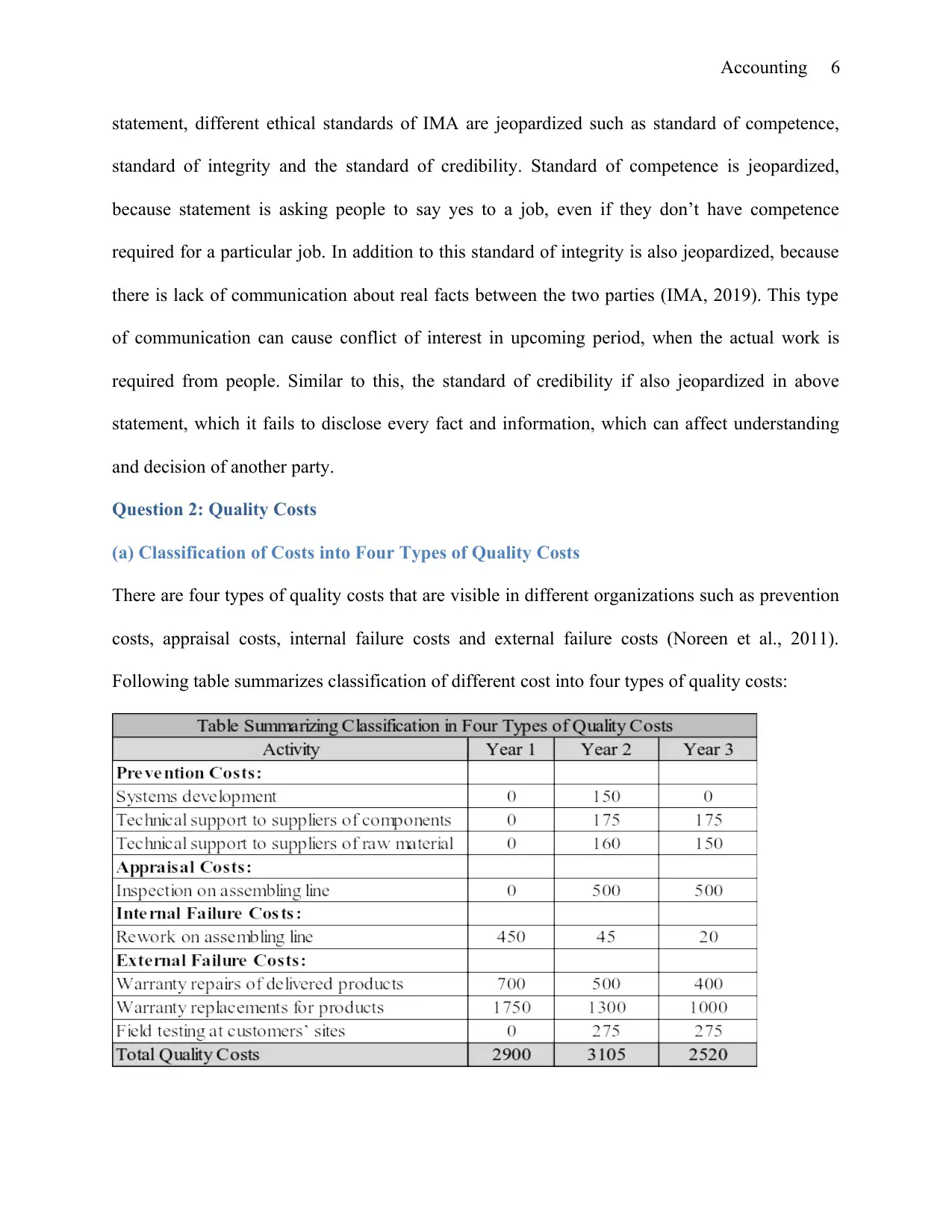

Question 2: Quality Costs

(a) Classification of Costs into Four Types of Quality Costs

There are four types of quality costs that are visible in different organizations such as prevention

costs, appraisal costs, internal failure costs and external failure costs (Noreen et al., 2011).

Following table summarizes classification of different cost into four types of quality costs:

statement, different ethical standards of IMA are jeopardized such as standard of competence,

standard of integrity and the standard of credibility. Standard of competence is jeopardized,

because statement is asking people to say yes to a job, even if they don’t have competence

required for a particular job. In addition to this standard of integrity is also jeopardized, because

there is lack of communication about real facts between the two parties (IMA, 2019). This type

of communication can cause conflict of interest in upcoming period, when the actual work is

required from people. Similar to this, the standard of credibility if also jeopardized in above

statement, which it fails to disclose every fact and information, which can affect understanding

and decision of another party.

Question 2: Quality Costs

(a) Classification of Costs into Four Types of Quality Costs

There are four types of quality costs that are visible in different organizations such as prevention

costs, appraisal costs, internal failure costs and external failure costs (Noreen et al., 2011).

Following table summarizes classification of different cost into four types of quality costs:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 7

(b) Example of an Appraisal Cost

Example of an appraisal cost is destruction of goods as part of testing process. Under testing

process at the quality check stage, different products are identified as defective products. In other

words, these products do not pass the quality check test. These products are destroyed

immediately. The cost that incurred in this testing process is considered as appraisal cost

(Hansen and Mowen, 2017). In means all the costs that are faced by organizations in the

processes that are planned and executed at workplace for diagnosis & prevention of quality

problems of defective products are considered as appraisal cost.

(c) Analysis of behavior of Four Types of Costs

From the analysis of above table, it is analyzed that system development cost has occurred in

organization for only one time (i.e. in second year). Technical support to supplier of components

cost has occurred in second year and it has remained in third year also. But the technical support

cost to suppliers of raw material has occurred in second year and is declined slightly in third

year. From the analysis of inspection of assembly line cost, it is observed that company has

continuously focused on inspection of assembly line at production site, as it has invested

continuously in both second year third year (i.e. $500). The internal failure cost (i.e. cost of

rework) of company was very high in first year (i.e. $450). This cost has declined to $45 in

second year and $20 in third year (Hansen and Mowen, 2017). It indicates increased focus of

company on supervision and inspection so that need of rework can be reduced in business.

External failure cost of company (i.e. warranty repairs of delivered products and warranty

replacement for products) is also reduced from year 1 to year 2 and year 3. It means company is

continuously trying to fix the issues of external failures in business.

(b) Example of an Appraisal Cost

Example of an appraisal cost is destruction of goods as part of testing process. Under testing

process at the quality check stage, different products are identified as defective products. In other

words, these products do not pass the quality check test. These products are destroyed

immediately. The cost that incurred in this testing process is considered as appraisal cost

(Hansen and Mowen, 2017). In means all the costs that are faced by organizations in the

processes that are planned and executed at workplace for diagnosis & prevention of quality

problems of defective products are considered as appraisal cost.

(c) Analysis of behavior of Four Types of Costs

From the analysis of above table, it is analyzed that system development cost has occurred in

organization for only one time (i.e. in second year). Technical support to supplier of components

cost has occurred in second year and it has remained in third year also. But the technical support

cost to suppliers of raw material has occurred in second year and is declined slightly in third

year. From the analysis of inspection of assembly line cost, it is observed that company has

continuously focused on inspection of assembly line at production site, as it has invested

continuously in both second year third year (i.e. $500). The internal failure cost (i.e. cost of

rework) of company was very high in first year (i.e. $450). This cost has declined to $45 in

second year and $20 in third year (Hansen and Mowen, 2017). It indicates increased focus of

company on supervision and inspection so that need of rework can be reduced in business.

External failure cost of company (i.e. warranty repairs of delivered products and warranty

replacement for products) is also reduced from year 1 to year 2 and year 3. It means company is

continuously trying to fix the issues of external failures in business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 8

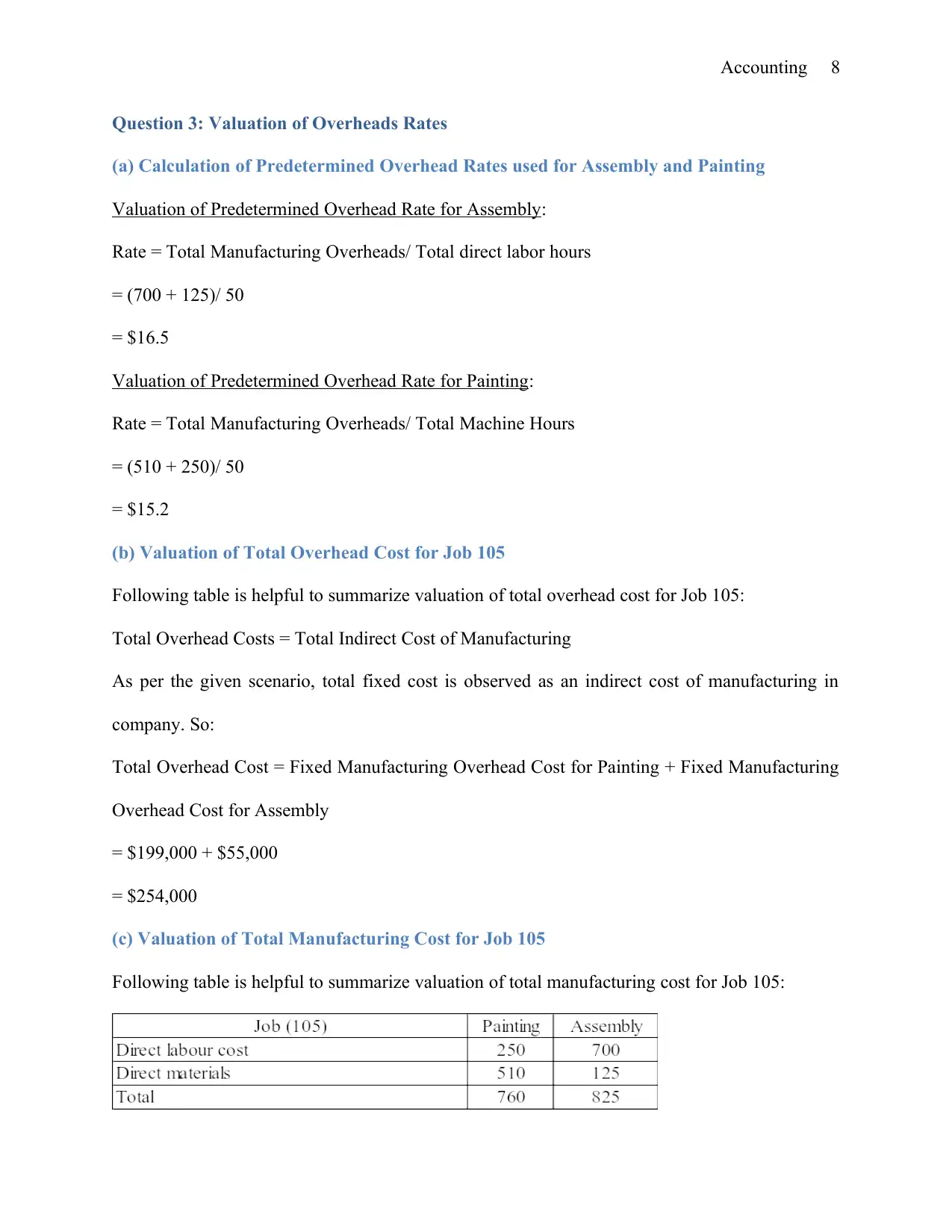

Question 3: Valuation of Overheads Rates

(a) Calculation of Predetermined Overhead Rates used for Assembly and Painting

Valuation of Predetermined Overhead Rate for Assembly:

Rate = Total Manufacturing Overheads/ Total direct labor hours

= (700 + 125)/ 50

= $16.5

Valuation of Predetermined Overhead Rate for Painting:

Rate = Total Manufacturing Overheads/ Total Machine Hours

= (510 + 250)/ 50

= $15.2

(b) Valuation of Total Overhead Cost for Job 105

Following table is helpful to summarize valuation of total overhead cost for Job 105:

Total Overhead Costs = Total Indirect Cost of Manufacturing

As per the given scenario, total fixed cost is observed as an indirect cost of manufacturing in

company. So:

Total Overhead Cost = Fixed Manufacturing Overhead Cost for Painting + Fixed Manufacturing

Overhead Cost for Assembly

= $199,000 + $55,000

= $254,000

(c) Valuation of Total Manufacturing Cost for Job 105

Following table is helpful to summarize valuation of total manufacturing cost for Job 105:

Question 3: Valuation of Overheads Rates

(a) Calculation of Predetermined Overhead Rates used for Assembly and Painting

Valuation of Predetermined Overhead Rate for Assembly:

Rate = Total Manufacturing Overheads/ Total direct labor hours

= (700 + 125)/ 50

= $16.5

Valuation of Predetermined Overhead Rate for Painting:

Rate = Total Manufacturing Overheads/ Total Machine Hours

= (510 + 250)/ 50

= $15.2

(b) Valuation of Total Overhead Cost for Job 105

Following table is helpful to summarize valuation of total overhead cost for Job 105:

Total Overhead Costs = Total Indirect Cost of Manufacturing

As per the given scenario, total fixed cost is observed as an indirect cost of manufacturing in

company. So:

Total Overhead Cost = Fixed Manufacturing Overhead Cost for Painting + Fixed Manufacturing

Overhead Cost for Assembly

= $199,000 + $55,000

= $254,000

(c) Valuation of Total Manufacturing Cost for Job 105

Following table is helpful to summarize valuation of total manufacturing cost for Job 105:

Accounting 9

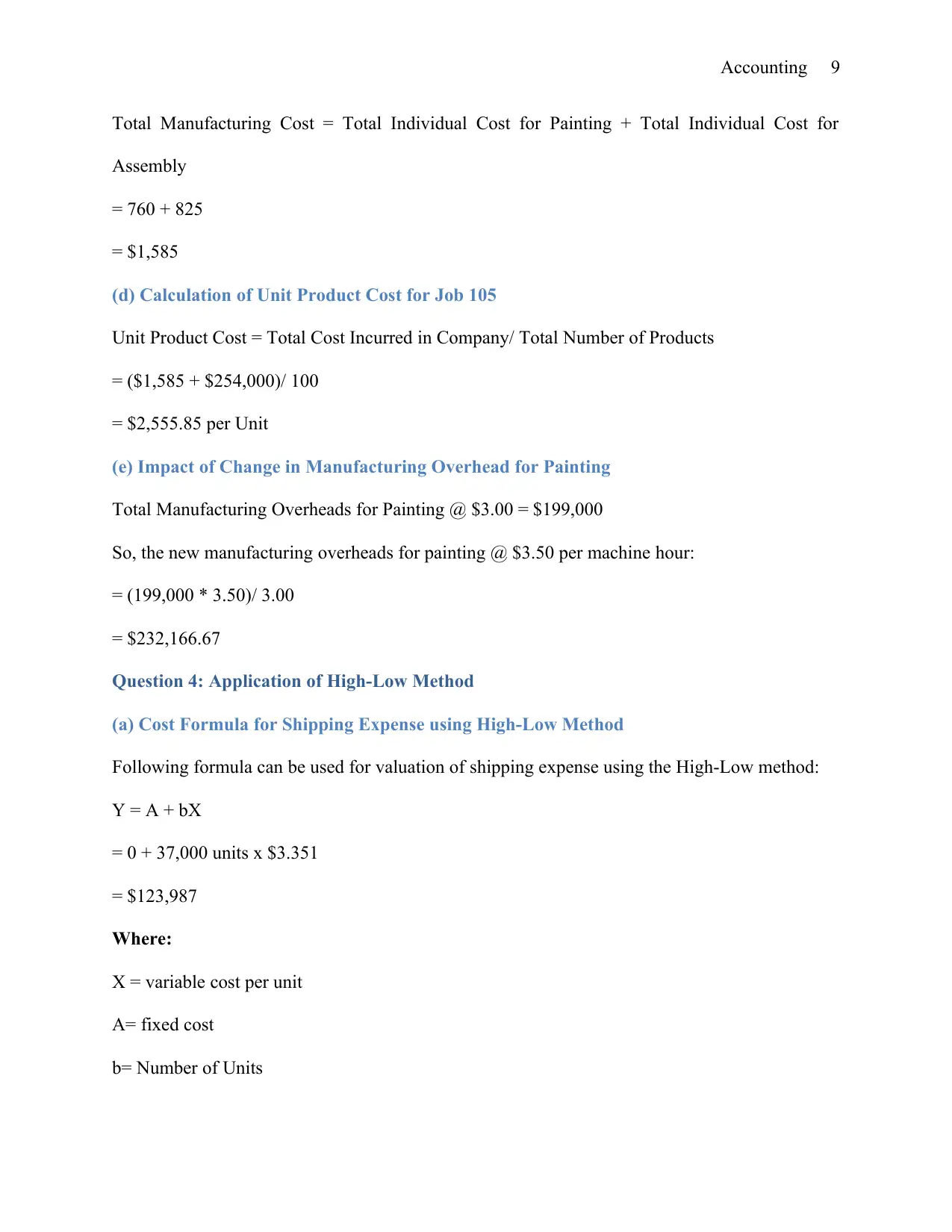

Total Manufacturing Cost = Total Individual Cost for Painting + Total Individual Cost for

Assembly

= 760 + 825

= $1,585

(d) Calculation of Unit Product Cost for Job 105

Unit Product Cost = Total Cost Incurred in Company/ Total Number of Products

= ($1,585 + $254,000)/ 100

= $2,555.85 per Unit

(e) Impact of Change in Manufacturing Overhead for Painting

Total Manufacturing Overheads for Painting @ $3.00 = $199,000

So, the new manufacturing overheads for painting @ $3.50 per machine hour:

= (199,000 * 3.50)/ 3.00

= $232,166.67

Question 4: Application of High-Low Method

(a) Cost Formula for Shipping Expense using High-Low Method

Following formula can be used for valuation of shipping expense using the High-Low method:

Y = A + bX

= 0 + 37,000 units x $3.351

= $123,987

Where:

X = variable cost per unit

A= fixed cost

b= Number of Units

Total Manufacturing Cost = Total Individual Cost for Painting + Total Individual Cost for

Assembly

= 760 + 825

= $1,585

(d) Calculation of Unit Product Cost for Job 105

Unit Product Cost = Total Cost Incurred in Company/ Total Number of Products

= ($1,585 + $254,000)/ 100

= $2,555.85 per Unit

(e) Impact of Change in Manufacturing Overhead for Painting

Total Manufacturing Overheads for Painting @ $3.00 = $199,000

So, the new manufacturing overheads for painting @ $3.50 per machine hour:

= (199,000 * 3.50)/ 3.00

= $232,166.67

Question 4: Application of High-Low Method

(a) Cost Formula for Shipping Expense using High-Low Method

Following formula can be used for valuation of shipping expense using the High-Low method:

Y = A + bX

= 0 + 37,000 units x $3.351

= $123,987

Where:

X = variable cost per unit

A= fixed cost

b= Number of Units

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 10

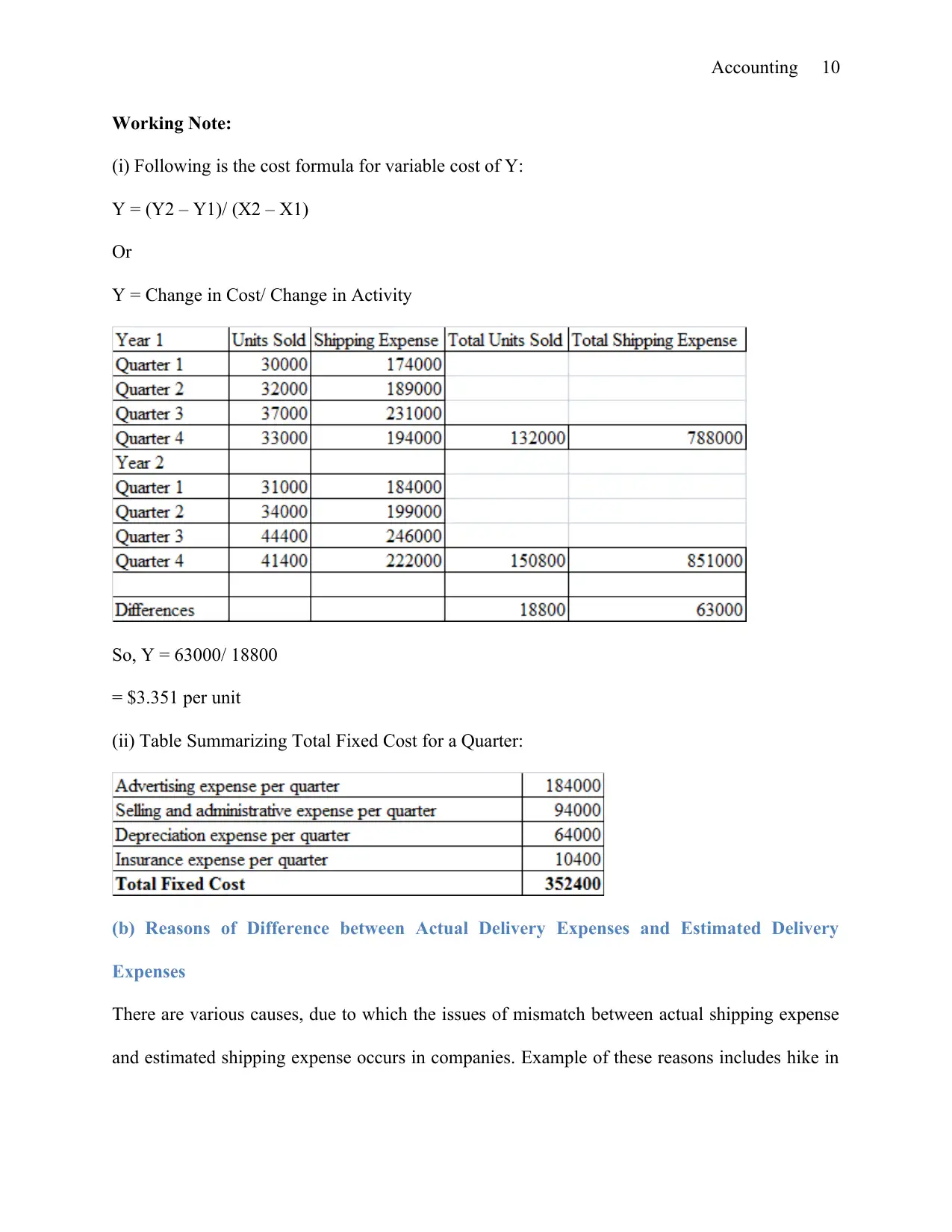

Working Note:

(i) Following is the cost formula for variable cost of Y:

Y = (Y2 – Y1)/ (X2 – X1)

Or

Y = Change in Cost/ Change in Activity

So, Y = 63000/ 18800

= $3.351 per unit

(ii) Table Summarizing Total Fixed Cost for a Quarter:

(b) Reasons of Difference between Actual Delivery Expenses and Estimated Delivery

Expenses

There are various causes, due to which the issues of mismatch between actual shipping expense

and estimated shipping expense occurs in companies. Example of these reasons includes hike in

Working Note:

(i) Following is the cost formula for variable cost of Y:

Y = (Y2 – Y1)/ (X2 – X1)

Or

Y = Change in Cost/ Change in Activity

So, Y = 63000/ 18800

= $3.351 per unit

(ii) Table Summarizing Total Fixed Cost for a Quarter:

(b) Reasons of Difference between Actual Delivery Expenses and Estimated Delivery

Expenses

There are various causes, due to which the issues of mismatch between actual shipping expense

and estimated shipping expense occurs in companies. Example of these reasons includes hike in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 11

the petrol or diesel prices, increase in tax rates by government, increase in price by transportation

or logistic partners, etc (Gilbertson et al., 2013).

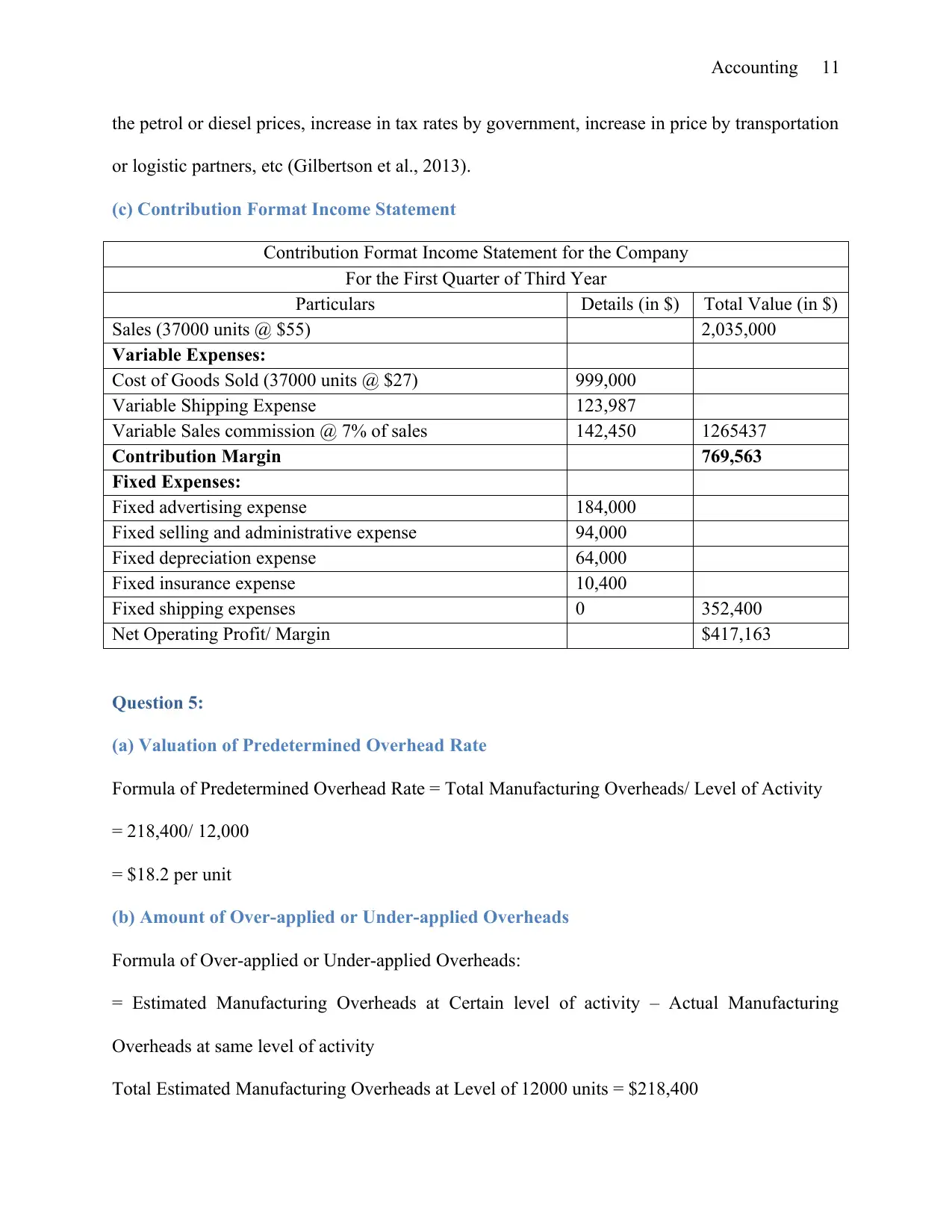

(c) Contribution Format Income Statement

Contribution Format Income Statement for the Company

For the First Quarter of Third Year

Particulars Details (in $) Total Value (in $)

Sales (37000 units @ $55) 2,035,000

Variable Expenses:

Cost of Goods Sold (37000 units @ $27) 999,000

Variable Shipping Expense 123,987

Variable Sales commission @ 7% of sales 142,450 1265437

Contribution Margin 769,563

Fixed Expenses:

Fixed advertising expense 184,000

Fixed selling and administrative expense 94,000

Fixed depreciation expense 64,000

Fixed insurance expense 10,400

Fixed shipping expenses 0 352,400

Net Operating Profit/ Margin $417,163

Question 5:

(a) Valuation of Predetermined Overhead Rate

Formula of Predetermined Overhead Rate = Total Manufacturing Overheads/ Level of Activity

= 218,400/ 12,000

= $18.2 per unit

(b) Amount of Over-applied or Under-applied Overheads

Formula of Over-applied or Under-applied Overheads:

= Estimated Manufacturing Overheads at Certain level of activity – Actual Manufacturing

Overheads at same level of activity

Total Estimated Manufacturing Overheads at Level of 12000 units = $218,400

the petrol or diesel prices, increase in tax rates by government, increase in price by transportation

or logistic partners, etc (Gilbertson et al., 2013).

(c) Contribution Format Income Statement

Contribution Format Income Statement for the Company

For the First Quarter of Third Year

Particulars Details (in $) Total Value (in $)

Sales (37000 units @ $55) 2,035,000

Variable Expenses:

Cost of Goods Sold (37000 units @ $27) 999,000

Variable Shipping Expense 123,987

Variable Sales commission @ 7% of sales 142,450 1265437

Contribution Margin 769,563

Fixed Expenses:

Fixed advertising expense 184,000

Fixed selling and administrative expense 94,000

Fixed depreciation expense 64,000

Fixed insurance expense 10,400

Fixed shipping expenses 0 352,400

Net Operating Profit/ Margin $417,163

Question 5:

(a) Valuation of Predetermined Overhead Rate

Formula of Predetermined Overhead Rate = Total Manufacturing Overheads/ Level of Activity

= 218,400/ 12,000

= $18.2 per unit

(b) Amount of Over-applied or Under-applied Overheads

Formula of Over-applied or Under-applied Overheads:

= Estimated Manufacturing Overheads at Certain level of activity – Actual Manufacturing

Overheads at same level of activity

Total Estimated Manufacturing Overheads at Level of 12000 units = $218,400

Accounting 12

So, estimated manufacturing overheads at level of 11,500 units = 218,400 x 11,500/ 12,000

= $209,300

Total Actual Manufacturing Overheads at level of 11,500 units = $215,000

So, value of over-applied or under-applied overheads:

= $209,300 - $215,000

= ($5,700)

So, it can be said that the manufacturing cost is over-applied by organization by amount of

$5,700. It means, the company has faced issue of cost overrun. This situation is dangerous for

profitability position of company.

(c) Implications of Having Large Over-applied or Under-applied Overheads

The situation of large over-applied overhead can adversely affect the management planning of

organization. It may face financial problem due to cost overrun issue in business. This will lead

to increase product cost per unit. In contrast to this, large under-applied overhead is favorable for

the company. This will affect management planning positively, as additional funds will be

available for further financial needs in business (Warren, 2012). In addition to thins, under-

applied overhead situation will result in reduction in product cost per unit to the company. It will

also increase profit margin per unit for the company.

Question 6: Pricing Techniques

(a) Limitations of Cost-plus Pricing

(i) Cost-plus pricing technique discourages cost-containment and efficiency within the

organization. In this situation, company has lack of focus on controlling or reducing cost factor

over products. It is so because profit margin per product is fixed in nature (Dholakia, 2018). Due

So, estimated manufacturing overheads at level of 11,500 units = 218,400 x 11,500/ 12,000

= $209,300

Total Actual Manufacturing Overheads at level of 11,500 units = $215,000

So, value of over-applied or under-applied overheads:

= $209,300 - $215,000

= ($5,700)

So, it can be said that the manufacturing cost is over-applied by organization by amount of

$5,700. It means, the company has faced issue of cost overrun. This situation is dangerous for

profitability position of company.

(c) Implications of Having Large Over-applied or Under-applied Overheads

The situation of large over-applied overhead can adversely affect the management planning of

organization. It may face financial problem due to cost overrun issue in business. This will lead

to increase product cost per unit. In contrast to this, large under-applied overhead is favorable for

the company. This will affect management planning positively, as additional funds will be

available for further financial needs in business (Warren, 2012). In addition to thins, under-

applied overhead situation will result in reduction in product cost per unit to the company. It will

also increase profit margin per unit for the company.

Question 6: Pricing Techniques

(a) Limitations of Cost-plus Pricing

(i) Cost-plus pricing technique discourages cost-containment and efficiency within the

organization. In this situation, company has lack of focus on controlling or reducing cost factor

over products. It is so because profit margin per product is fixed in nature (Dholakia, 2018). Due

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.