MAA262 Report: Cost Analysis of Barbeque & Balloons Business

VerifiedAdded on 2022/11/13

|18

|2598

|337

Report

AI Summary

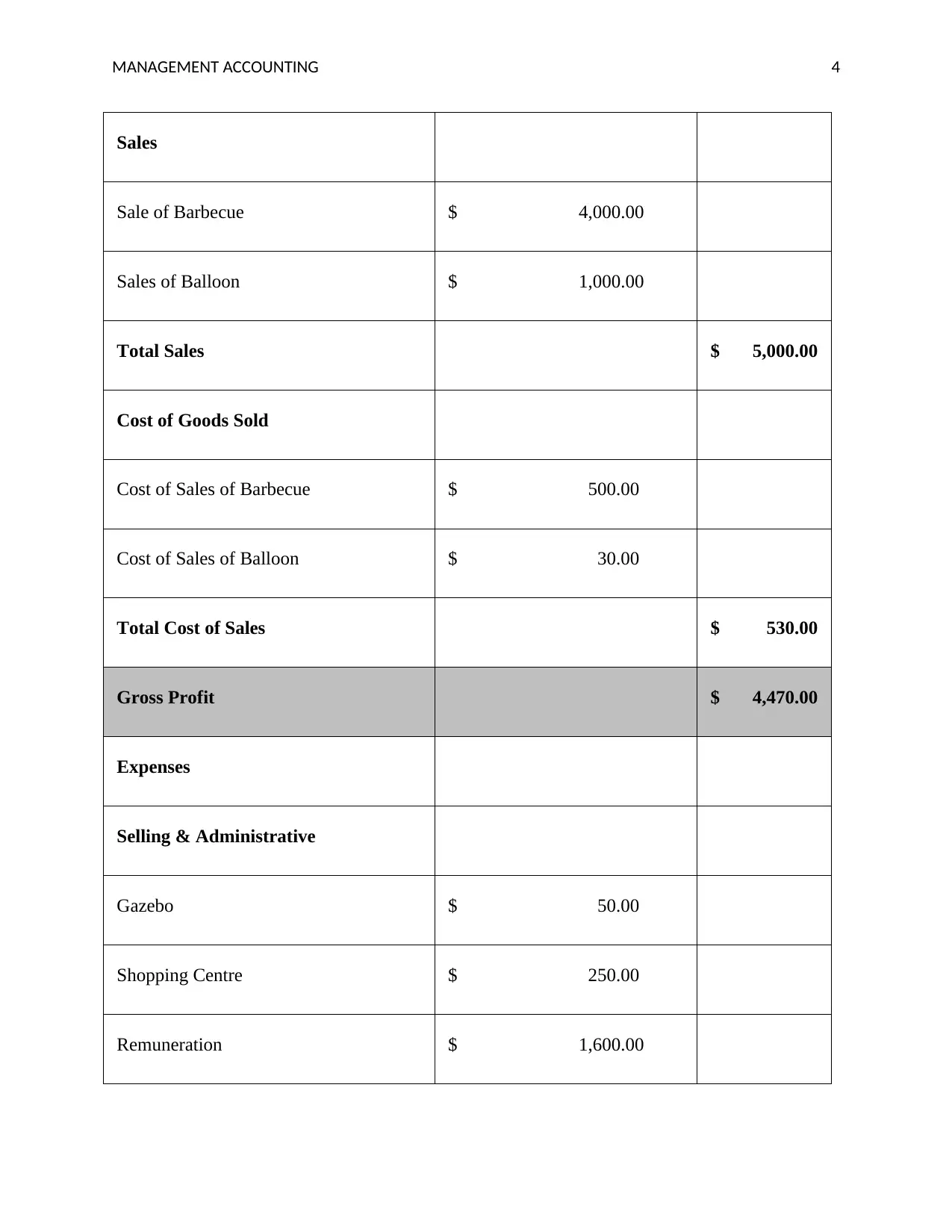

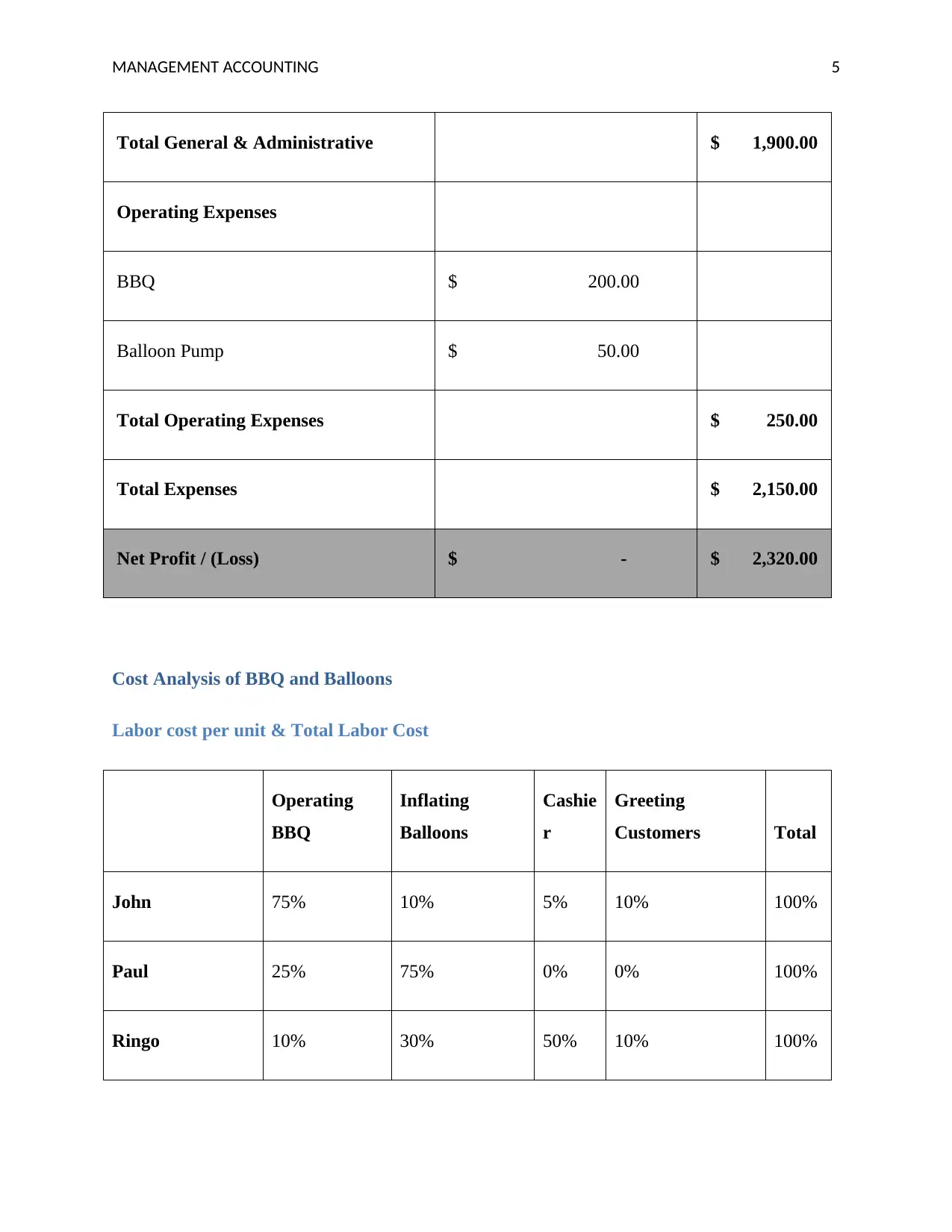

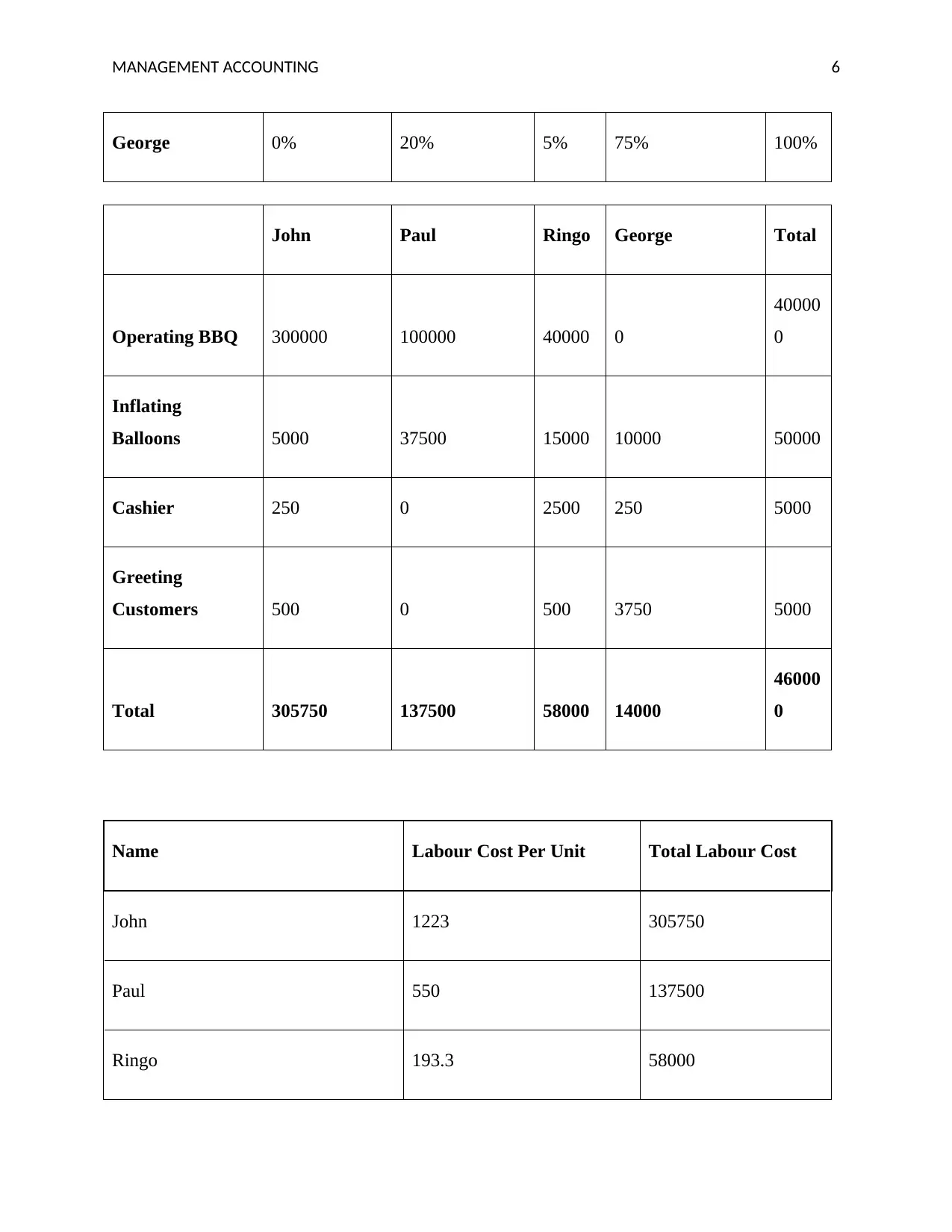

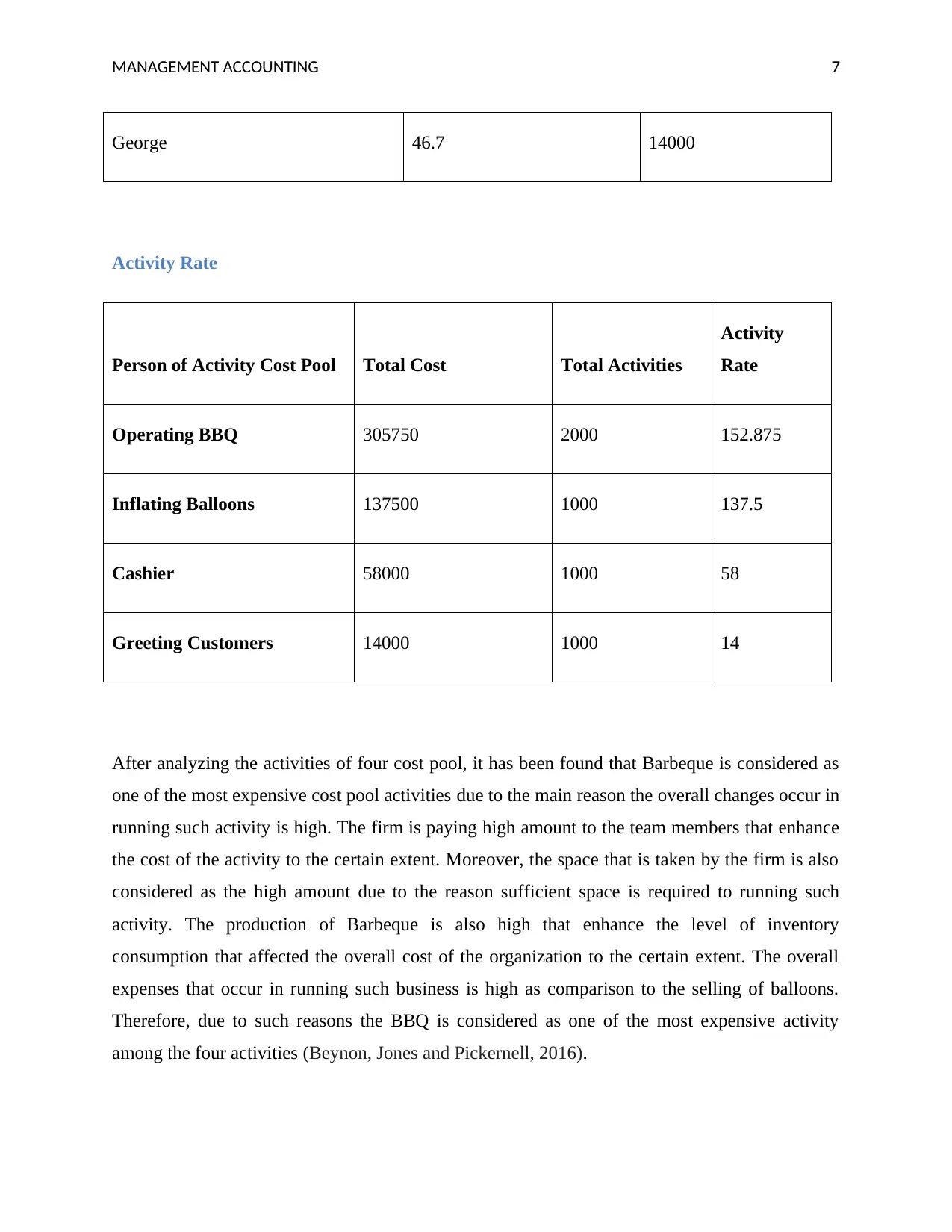

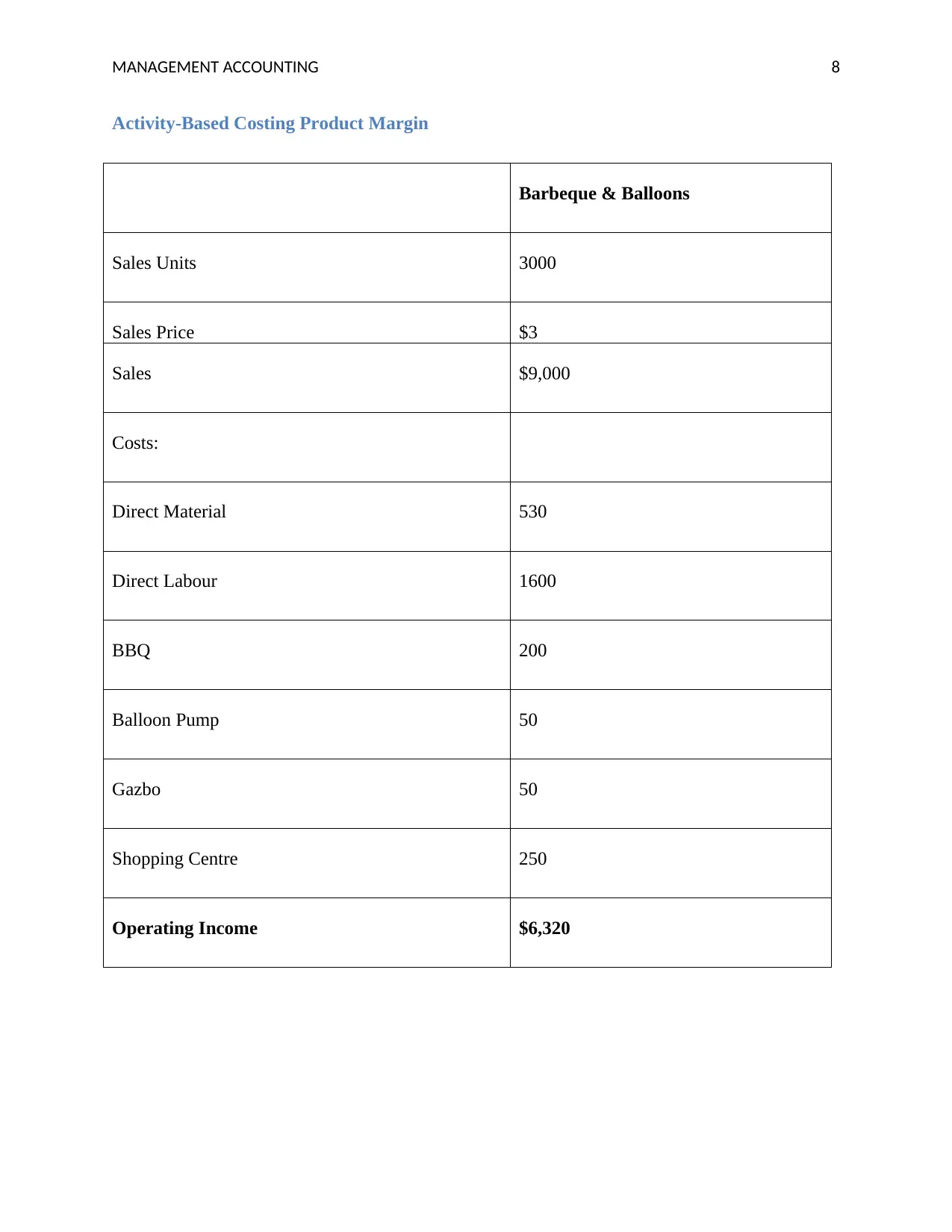

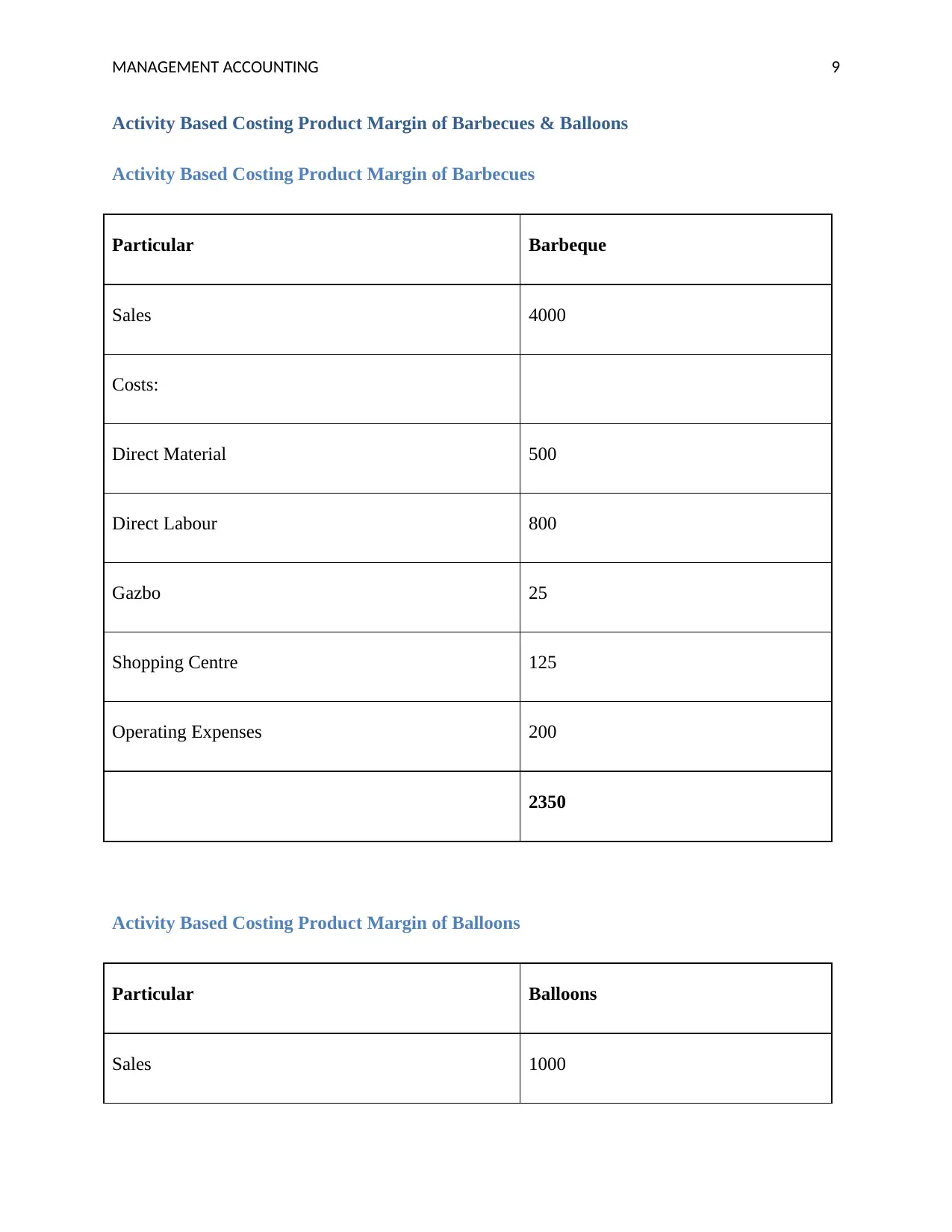

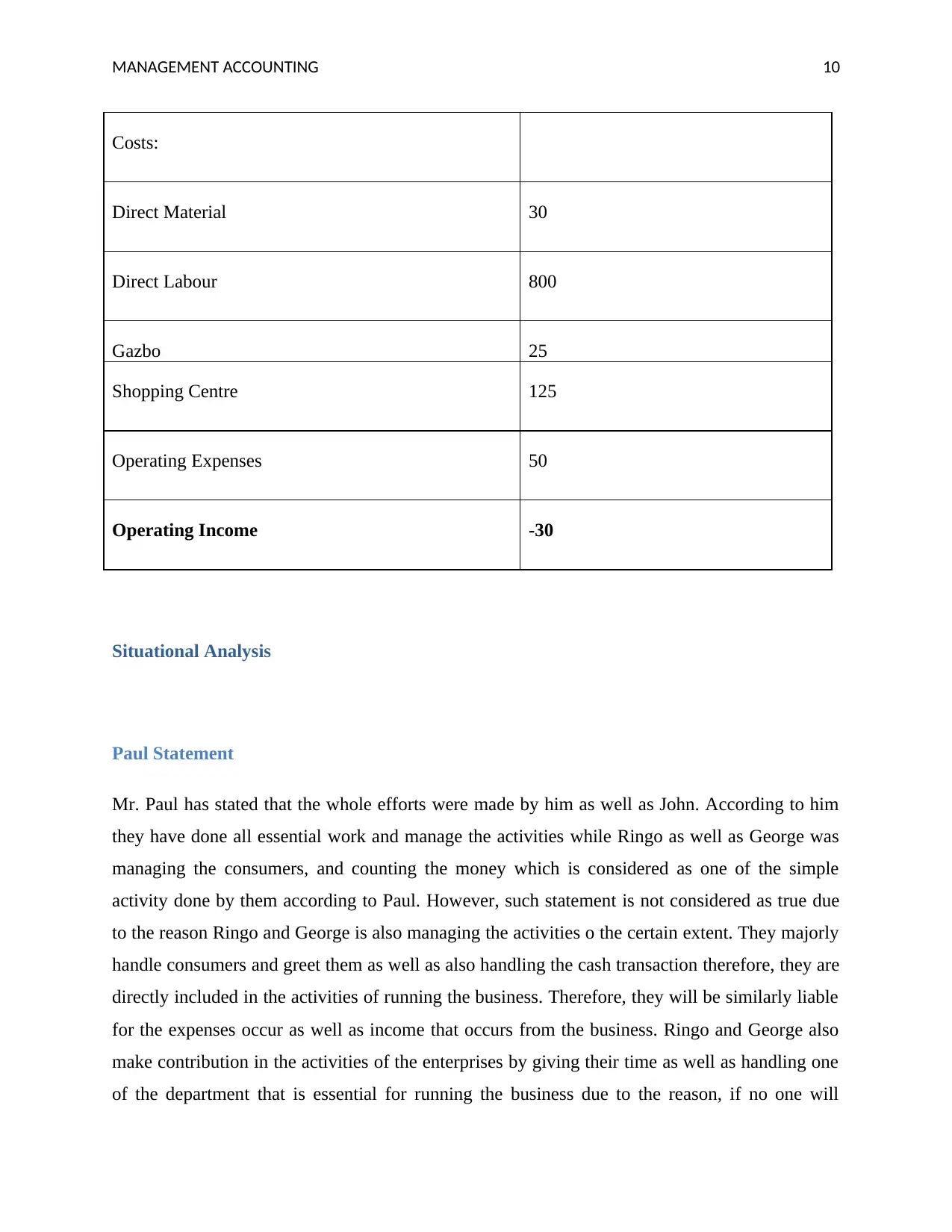

This report provides a comprehensive analysis of a BBQ and Balloons business, focusing on management accounting principles. It begins with an introduction to the importance of financial analysis and its role in business success. The report includes an income statement, detailed cost analysis of labor, and activity-based costing to determine product margins for both BBQ and balloons. A situational analysis examines the perspectives of team members regarding their contributions and the challenges faced. The report further explores the need for structured performance evaluations and compares planning and actual budgets, highlighting variances in revenue and spending. Finally, it calculates and analyzes material, quantity, and total variances for both BBQ and balloons, concluding with key insights into the financial performance and areas for improvement in the business. This report covers essential aspects of cost accounting, variance analysis, and budgeting, offering a practical application of management accounting concepts.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.