Debt-Equity Analysis: A Comparative Study of Four Public Companies

VerifiedAdded on 2023/06/05

|16

|3427

|284

Report

AI Summary

This report offers a comparative analysis of the debt and equity positions of four public companies: BHP Billiton Ltd, Telstra, Suncorp Group Limited, and AGL Energy Limited. It evaluates key financial metrics such as share capital, reserves, and retained earnings over four consecutive years (2014-2017). The report also discusses the significance of financial information disclosure, the role of accounting standards (AASB and IASB), and the benefits and drawbacks of disclosing financial information to stakeholders and competitors. The analysis reveals varying trends in the owner's funds and equity components for each company, highlighting the importance of sustainable capital worth enhancement.

CORPORATE AND FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING: 1

Executive summary

The report brings out the comparison between the four public companies especially related to

debt and equity. The four public companies are BHP Billiton Ltd, Telstra, Suncorp group

limited, and AGL energy limited. Moreover, the each subheading of equity and shareholders

is being evaluated by making a comparison table of four consecutive years.

Executive summary

The report brings out the comparison between the four public companies especially related to

debt and equity. The four public companies are BHP Billiton Ltd, Telstra, Suncorp group

limited, and AGL energy limited. Moreover, the each subheading of equity and shareholders

is being evaluated by making a comparison table of four consecutive years.

CORPORATE AND FINANCIAL ACCOUNTING: 2

Contents

Answer to question 1-................................................................................................................2

Answer to Q.2)...........................................................................................................................3

Owner`s fund..............................................................................................................................4

Ordinary Share Capital...............................................................................................................7

Reserves.....................................................................................................................................8

Retain earnings...........................................................................................................................8

Comparative analysis of debt-equity position of the four firms that are selected......................9

References................................................................................................................................11

Contents

Answer to question 1-................................................................................................................2

Answer to Q.2)...........................................................................................................................3

Owner`s fund..............................................................................................................................4

Ordinary Share Capital...............................................................................................................7

Reserves.....................................................................................................................................8

Retain earnings...........................................................................................................................8

Comparative analysis of debt-equity position of the four firms that are selected......................9

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING: 3

Answer to question 1-

Declaration of Financial information of any company have significance in the corporate

world over the last few years because of increased complex business operations. Fair

financial statement of the company is the way to communicate to the stakeholders and

convince the shareholders to invest in their company. A manager should take step forward to

share the financial statements voluntarily to its stakeholders especially external stakeholders.

Disclosure of Annual report to the public would help the company to build trust and

confidence among the shareholders. The external stakeholders would use the information

provided in the annual reports to make the rational decisions. Legal regulations have enforced

the companies to act on the behalf of creditors, employees, and shareholders to derive the

relevant information that governs the financial reporting (Alhazaimeh, Palaniappan, and

Almsafir, 2014).

After 1990, Accounting Standards Board has made necessary the implementation of Financial

Reporting Standards. In case the manager do not access information regarding organisation`s

working, he will not able to publish information of financial statements. The disclosure

requirements reduce the tendency of the companies to commit unethical deeds. Disclosure

would asymmetry the information between the director and the other external user groups.

The availability of financial statements to the users enables the external users to compare the

actual performance of the company. The act not only requires the managed to represent

financial statements to the stakeholders every year. However, it also requires the team of

independent auditors to revise, examine, and check whether the reporting of financial

statements presented to the stakeholders are accurate or not (Alhazaimeh, Palaniappan, and

Almsafir, 2014).

Answer to question 1-

Declaration of Financial information of any company have significance in the corporate

world over the last few years because of increased complex business operations. Fair

financial statement of the company is the way to communicate to the stakeholders and

convince the shareholders to invest in their company. A manager should take step forward to

share the financial statements voluntarily to its stakeholders especially external stakeholders.

Disclosure of Annual report to the public would help the company to build trust and

confidence among the shareholders. The external stakeholders would use the information

provided in the annual reports to make the rational decisions. Legal regulations have enforced

the companies to act on the behalf of creditors, employees, and shareholders to derive the

relevant information that governs the financial reporting (Alhazaimeh, Palaniappan, and

Almsafir, 2014).

After 1990, Accounting Standards Board has made necessary the implementation of Financial

Reporting Standards. In case the manager do not access information regarding organisation`s

working, he will not able to publish information of financial statements. The disclosure

requirements reduce the tendency of the companies to commit unethical deeds. Disclosure

would asymmetry the information between the director and the other external user groups.

The availability of financial statements to the users enables the external users to compare the

actual performance of the company. The act not only requires the managed to represent

financial statements to the stakeholders every year. However, it also requires the team of

independent auditors to revise, examine, and check whether the reporting of financial

statements presented to the stakeholders are accurate or not (Alhazaimeh, Palaniappan, and

Almsafir, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING: 4

The law provides a general framework for everything that is being accounted and recorded in

the financial statements. The accounting profession ensures that the financial reports follow

the accounting standards and principles. Moreover, the manager prepares the financial

requirements voluntarily not just to fulfil the external needs but also the internal compliances.

Such financial reporting disclosures would bring contractual, reputational, and legal penalties

for misleading and low cost accuracy of auditing. When verification cost exceeds,

organisations utilises the intermediaries such as underwriters, credit rating agency and

auditors that helps the company to certify the quality of information. The discussion above

clearly focuses on benefits and necessities of disclosure. However, managers considers the

market-wide effect of disclosure. Managers and directors may feel a bit hesitated to

disclosure the information to the competitors. Such choices to remain rigid towards not

revealing the proprietary information that depends on firm, but it would not support and

incorporate potential benefits. Such disclosures will allow the company to collect the

knowledge of how to allocate the capital to high value projects and encourage competition

among the organisations that can promote improvements that will ultimately benefit the

customers (Dumay, 2016).

Nevertheless, it is very necessary to regulate the functions of financial reporting and

accounting. The accounting principles and regulation is the platform through where different

firms are based on different business are evaluated on the same basis. Disclosure decisions

can lead to under or over production of people information. Disclosure of financial statements

may reveal information of other firms. The disclosing organisation does not get benefit from

information and this may result in producing information (Bhat, Callen, and Segal, 2016).

The law provides a general framework for everything that is being accounted and recorded in

the financial statements. The accounting profession ensures that the financial reports follow

the accounting standards and principles. Moreover, the manager prepares the financial

requirements voluntarily not just to fulfil the external needs but also the internal compliances.

Such financial reporting disclosures would bring contractual, reputational, and legal penalties

for misleading and low cost accuracy of auditing. When verification cost exceeds,

organisations utilises the intermediaries such as underwriters, credit rating agency and

auditors that helps the company to certify the quality of information. The discussion above

clearly focuses on benefits and necessities of disclosure. However, managers considers the

market-wide effect of disclosure. Managers and directors may feel a bit hesitated to

disclosure the information to the competitors. Such choices to remain rigid towards not

revealing the proprietary information that depends on firm, but it would not support and

incorporate potential benefits. Such disclosures will allow the company to collect the

knowledge of how to allocate the capital to high value projects and encourage competition

among the organisations that can promote improvements that will ultimately benefit the

customers (Dumay, 2016).

Nevertheless, it is very necessary to regulate the functions of financial reporting and

accounting. The accounting principles and regulation is the platform through where different

firms are based on different business are evaluated on the same basis. Disclosure decisions

can lead to under or over production of people information. Disclosure of financial statements

may reveal information of other firms. The disclosing organisation does not get benefit from

information and this may result in producing information (Bhat, Callen, and Segal, 2016).

CORPORATE AND FINANCIAL ACCOUNTING: 5

Answer to Q.2).

Accounting standards are the authorised standards to guide the financial reporting.

Accounting standards are the primary source of (GAAPs) generally accepted accounting

principles. Accounting standards are common set of principles, procedures, and standards,

which define the basis of accounting principles and policies. Australian Accounting standard

Board develops, issues, and maintains the Australian Accounting standards and

pronouncements (Rainsbury, 2017). It contributes to development of global financial

reporting standards and it enables the participation of Australian community in global setting.

The functions of AASB are set out by Australian securities and Investments Commission Act

(ASIC), 2001. The aim of ASIC is to enforce and regulate the company and its financial

service laws that would protect Australian consumers, creditors, and investors.

Accounting standard board of Australia (AASB) is a governmental agency that would

regulate the accounting standards especially for the Australian companies. It is responsible

for developing and maintaining the accounting standards and ensure that whether the

company follows the required compliance (Nicoleta, and Victor, 2014). The international

standard board (IASB) is private sector independent body that is committed to implement the

accounting standards throughout the world in order to control the manipulation of accounts

that hampers the public interest. Moreover, IASB co-operates with various national

accounting bodies that could achieve the convergence of accounting standards throughout the

world (Bhat, Callen, and Segal, 2016).

The regulations under AASB considers the strategy that determines how the association can

accomplish and fulfil its role to set better accounting standards in the fast changing

environment. The strategy of AASB helps the IASB to identify the technical issues based on

which accounting standards are formulated (Mowry et al., 2016).

Answer to Q.2).

Accounting standards are the authorised standards to guide the financial reporting.

Accounting standards are the primary source of (GAAPs) generally accepted accounting

principles. Accounting standards are common set of principles, procedures, and standards,

which define the basis of accounting principles and policies. Australian Accounting standard

Board develops, issues, and maintains the Australian Accounting standards and

pronouncements (Rainsbury, 2017). It contributes to development of global financial

reporting standards and it enables the participation of Australian community in global setting.

The functions of AASB are set out by Australian securities and Investments Commission Act

(ASIC), 2001. The aim of ASIC is to enforce and regulate the company and its financial

service laws that would protect Australian consumers, creditors, and investors.

Accounting standard board of Australia (AASB) is a governmental agency that would

regulate the accounting standards especially for the Australian companies. It is responsible

for developing and maintaining the accounting standards and ensure that whether the

company follows the required compliance (Nicoleta, and Victor, 2014). The international

standard board (IASB) is private sector independent body that is committed to implement the

accounting standards throughout the world in order to control the manipulation of accounts

that hampers the public interest. Moreover, IASB co-operates with various national

accounting bodies that could achieve the convergence of accounting standards throughout the

world (Bhat, Callen, and Segal, 2016).

The regulations under AASB considers the strategy that determines how the association can

accomplish and fulfil its role to set better accounting standards in the fast changing

environment. The strategy of AASB helps the IASB to identify the technical issues based on

which accounting standards are formulated (Mowry et al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING: 6

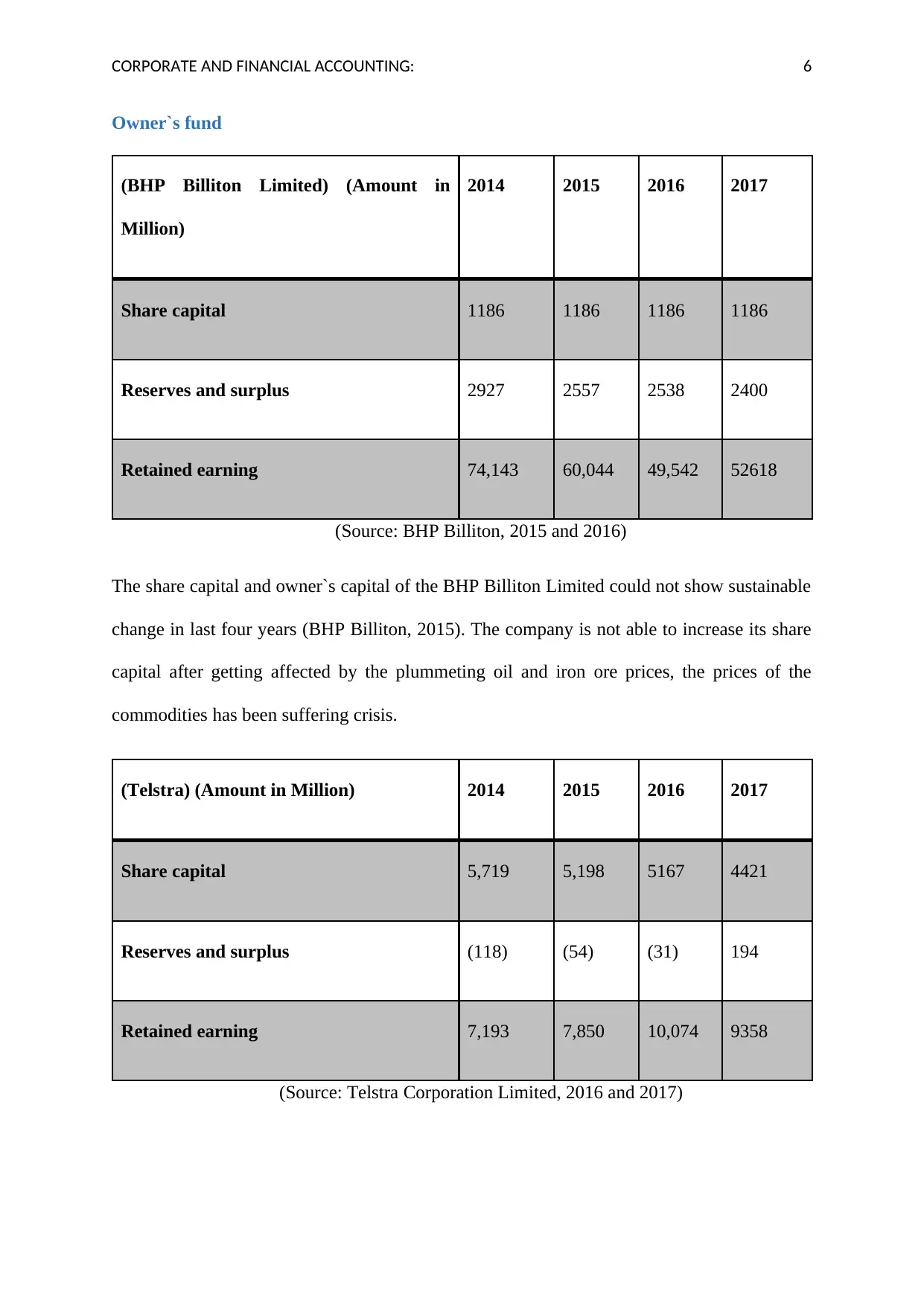

Owner`s fund

(BHP Billiton Limited) (Amount in

Million)

2014 2015 2016 2017

Share capital 1186 1186 1186 1186

Reserves and surplus 2927 2557 2538 2400

Retained earning 74,143 60,044 49,542 52618

(Source: BHP Billiton, 2015 and 2016)

The share capital and owner`s capital of the BHP Billiton Limited could not show sustainable

change in last four years (BHP Billiton, 2015). The company is not able to increase its share

capital after getting affected by the plummeting oil and iron ore prices, the prices of the

commodities has been suffering crisis.

(Telstra) (Amount in Million) 2014 2015 2016 2017

Share capital 5,719 5,198 5167 4421

Reserves and surplus (118) (54) (31) 194

Retained earning 7,193 7,850 10,074 9358

(Source: Telstra Corporation Limited, 2016 and 2017)

Owner`s fund

(BHP Billiton Limited) (Amount in

Million)

2014 2015 2016 2017

Share capital 1186 1186 1186 1186

Reserves and surplus 2927 2557 2538 2400

Retained earning 74,143 60,044 49,542 52618

(Source: BHP Billiton, 2015 and 2016)

The share capital and owner`s capital of the BHP Billiton Limited could not show sustainable

change in last four years (BHP Billiton, 2015). The company is not able to increase its share

capital after getting affected by the plummeting oil and iron ore prices, the prices of the

commodities has been suffering crisis.

(Telstra) (Amount in Million) 2014 2015 2016 2017

Share capital 5,719 5,198 5167 4421

Reserves and surplus (118) (54) (31) 194

Retained earning 7,193 7,850 10,074 9358

(Source: Telstra Corporation Limited, 2016 and 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING: 7

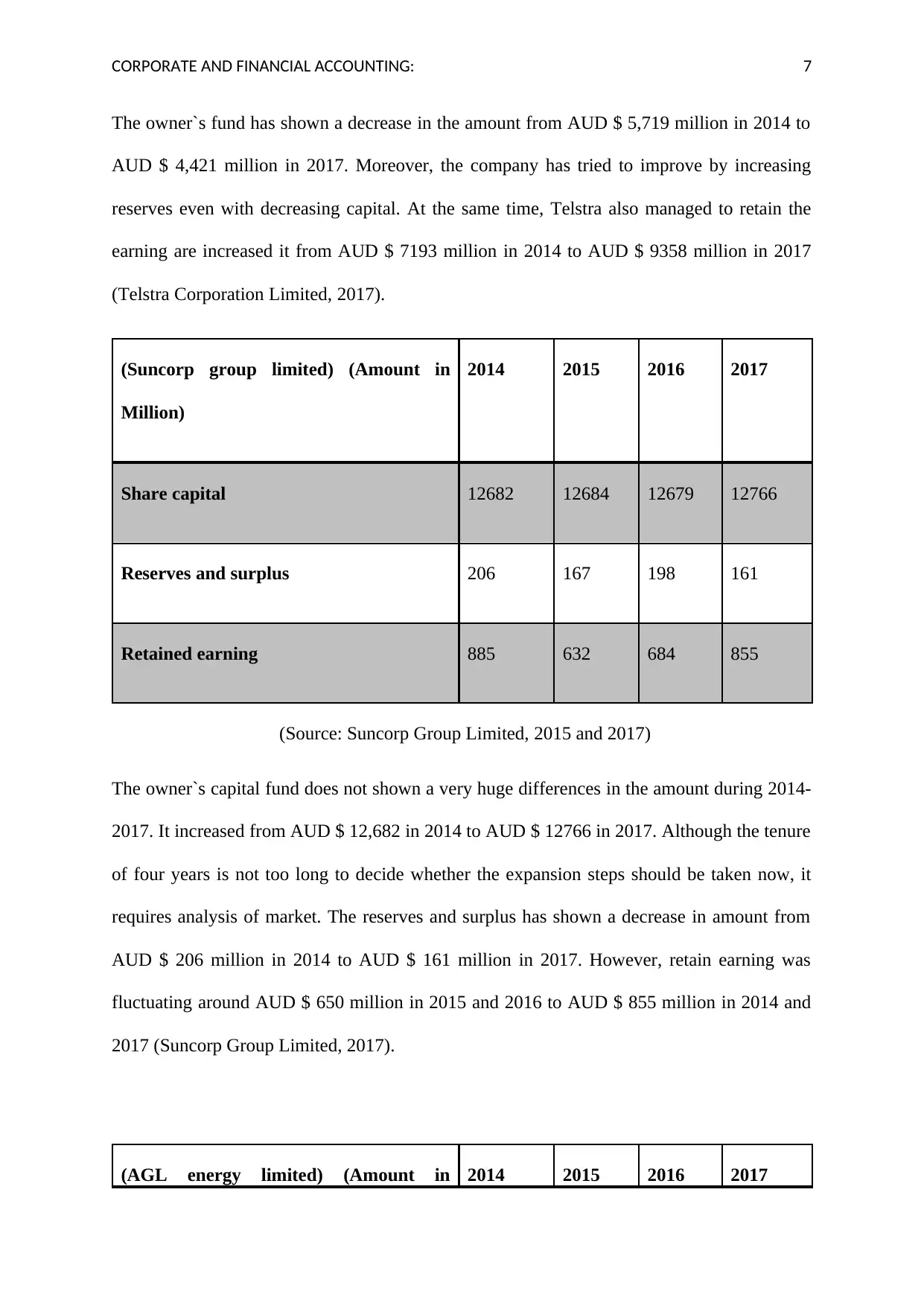

The owner`s fund has shown a decrease in the amount from AUD $ 5,719 million in 2014 to

AUD $ 4,421 million in 2017. Moreover, the company has tried to improve by increasing

reserves even with decreasing capital. At the same time, Telstra also managed to retain the

earning are increased it from AUD $ 7193 million in 2014 to AUD $ 9358 million in 2017

(Telstra Corporation Limited, 2017).

(Suncorp group limited) (Amount in

Million)

2014 2015 2016 2017

Share capital 12682 12684 12679 12766

Reserves and surplus 206 167 198 161

Retained earning 885 632 684 855

(Source: Suncorp Group Limited, 2015 and 2017)

The owner`s capital fund does not shown a very huge differences in the amount during 2014-

2017. It increased from AUD $ 12,682 in 2014 to AUD $ 12766 in 2017. Although the tenure

of four years is not too long to decide whether the expansion steps should be taken now, it

requires analysis of market. The reserves and surplus has shown a decrease in amount from

AUD $ 206 million in 2014 to AUD $ 161 million in 2017. However, retain earning was

fluctuating around AUD $ 650 million in 2015 and 2016 to AUD $ 855 million in 2014 and

2017 (Suncorp Group Limited, 2017).

(AGL energy limited) (Amount in 2014 2015 2016 2017

The owner`s fund has shown a decrease in the amount from AUD $ 5,719 million in 2014 to

AUD $ 4,421 million in 2017. Moreover, the company has tried to improve by increasing

reserves even with decreasing capital. At the same time, Telstra also managed to retain the

earning are increased it from AUD $ 7193 million in 2014 to AUD $ 9358 million in 2017

(Telstra Corporation Limited, 2017).

(Suncorp group limited) (Amount in

Million)

2014 2015 2016 2017

Share capital 12682 12684 12679 12766

Reserves and surplus 206 167 198 161

Retained earning 885 632 684 855

(Source: Suncorp Group Limited, 2015 and 2017)

The owner`s capital fund does not shown a very huge differences in the amount during 2014-

2017. It increased from AUD $ 12,682 in 2014 to AUD $ 12766 in 2017. Although the tenure

of four years is not too long to decide whether the expansion steps should be taken now, it

requires analysis of market. The reserves and surplus has shown a decrease in amount from

AUD $ 206 million in 2014 to AUD $ 161 million in 2017. However, retain earning was

fluctuating around AUD $ 650 million in 2015 and 2016 to AUD $ 855 million in 2014 and

2017 (Suncorp Group Limited, 2017).

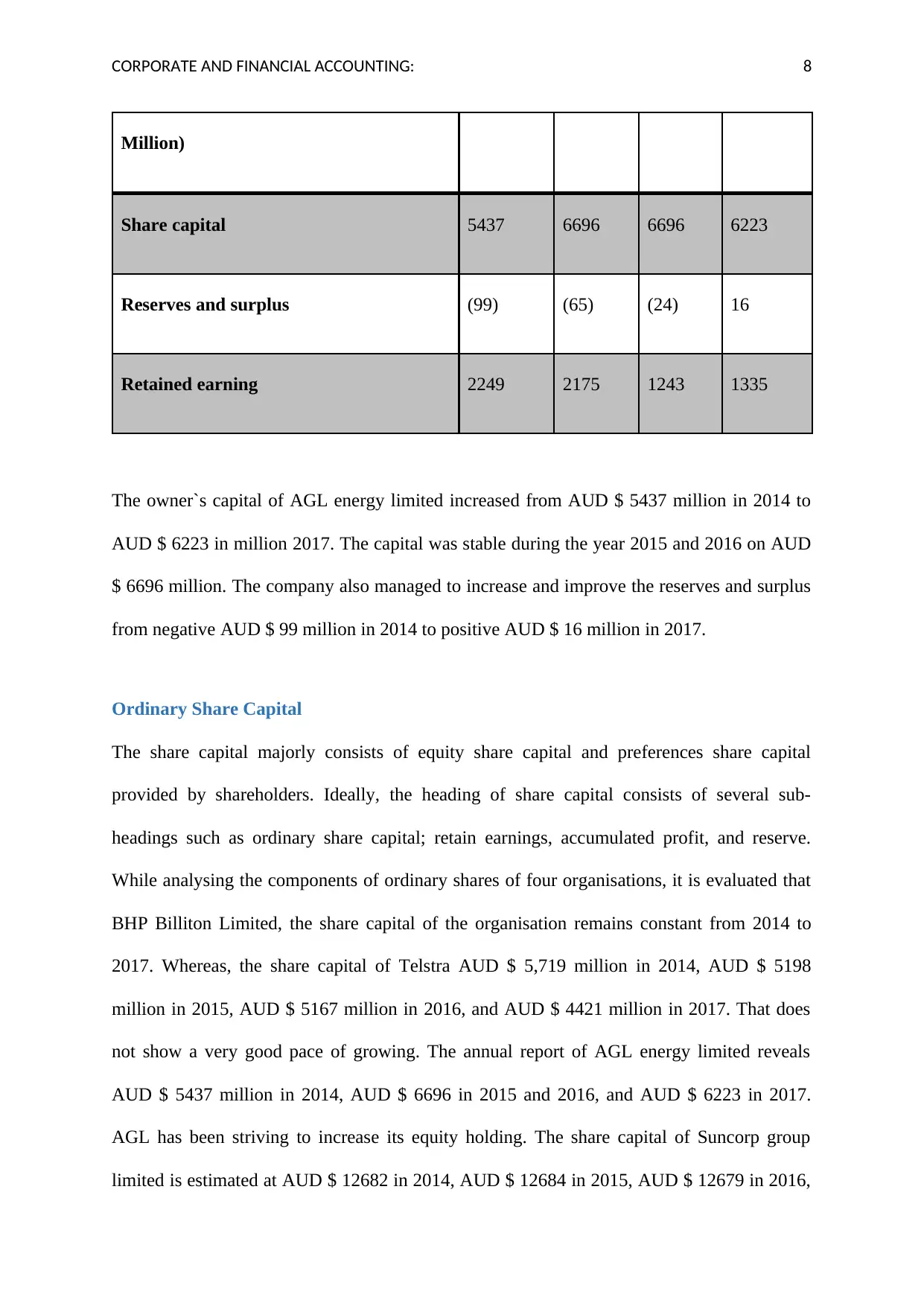

(AGL energy limited) (Amount in 2014 2015 2016 2017

CORPORATE AND FINANCIAL ACCOUNTING: 8

Million)

Share capital 5437 6696 6696 6223

Reserves and surplus (99) (65) (24) 16

Retained earning 2249 2175 1243 1335

The owner`s capital of AGL energy limited increased from AUD $ 5437 million in 2014 to

AUD $ 6223 in million 2017. The capital was stable during the year 2015 and 2016 on AUD

$ 6696 million. The company also managed to increase and improve the reserves and surplus

from negative AUD $ 99 million in 2014 to positive AUD $ 16 million in 2017.

Ordinary Share Capital

The share capital majorly consists of equity share capital and preferences share capital

provided by shareholders. Ideally, the heading of share capital consists of several sub-

headings such as ordinary share capital; retain earnings, accumulated profit, and reserve.

While analysing the components of ordinary shares of four organisations, it is evaluated that

BHP Billiton Limited, the share capital of the organisation remains constant from 2014 to

2017. Whereas, the share capital of Telstra AUD $ 5,719 million in 2014, AUD $ 5198

million in 2015, AUD $ 5167 million in 2016, and AUD $ 4421 million in 2017. That does

not show a very good pace of growing. The annual report of AGL energy limited reveals

AUD $ 5437 million in 2014, AUD $ 6696 in 2015 and 2016, and AUD $ 6223 in 2017.

AGL has been striving to increase its equity holding. The share capital of Suncorp group

limited is estimated at AUD $ 12682 in 2014, AUD $ 12684 in 2015, AUD $ 12679 in 2016,

Million)

Share capital 5437 6696 6696 6223

Reserves and surplus (99) (65) (24) 16

Retained earning 2249 2175 1243 1335

The owner`s capital of AGL energy limited increased from AUD $ 5437 million in 2014 to

AUD $ 6223 in million 2017. The capital was stable during the year 2015 and 2016 on AUD

$ 6696 million. The company also managed to increase and improve the reserves and surplus

from negative AUD $ 99 million in 2014 to positive AUD $ 16 million in 2017.

Ordinary Share Capital

The share capital majorly consists of equity share capital and preferences share capital

provided by shareholders. Ideally, the heading of share capital consists of several sub-

headings such as ordinary share capital; retain earnings, accumulated profit, and reserve.

While analysing the components of ordinary shares of four organisations, it is evaluated that

BHP Billiton Limited, the share capital of the organisation remains constant from 2014 to

2017. Whereas, the share capital of Telstra AUD $ 5,719 million in 2014, AUD $ 5198

million in 2015, AUD $ 5167 million in 2016, and AUD $ 4421 million in 2017. That does

not show a very good pace of growing. The annual report of AGL energy limited reveals

AUD $ 5437 million in 2014, AUD $ 6696 in 2015 and 2016, and AUD $ 6223 in 2017.

AGL has been striving to increase its equity holding. The share capital of Suncorp group

limited is estimated at AUD $ 12682 in 2014, AUD $ 12684 in 2015, AUD $ 12679 in 2016,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING: 9

AUD $ 12766 in 2017. Among all four companies, Suncorp group limited has the largest

capital share. After the comparison of share capital of four organisations, it will be inferred

that Telstra is growing at a low pace.

Other Equity Instruments and retained earning

Mainly equity has two components recognised as equity instrument and retain earnings.

Equity instruments is more like a document that serve as an evidence of ownership in an

organisation such as a share certificate or a warrant. Equity instruments are issued to

shareholders of the company and the fund generated is used to invest in business. Moreover,

none among the chosen four organisation offers any of the equity instrument except equity

shares.

Reserves

Reserves in the balance sheet is a subheading in the shareholders fund heading in the balance

sheet. Reserve is the part of profit apportioned for a particular purpose from the company’s

total profit. The reserve of BHP Billiton Ltd has been around AUD $ 2500 million for all the

four years from 2014 to 2017. However, the surplus kept decreasing as the years passed from

AUS $ 2927 million in 2014 to AUD $ 2557 million in 2015 to AUD $ 2400 million in 2017.

Although, the reserve amount of Telstra was negative in 2014, but it improved at a high pace.

The reserves of AGL energy limited follows the same path as of Telstra, its reserves were

also negative. However, it strived to improve and achieve a positive surplus. Among all the

four companies, the reserves of BHP Billiton ltd is highest.

Retain earnings

Retain earning is the portion of surplus earning that end up to invest the earnings in order to

increase the capital worth. These earnings are not distributed among the shareholders rather

AUD $ 12766 in 2017. Among all four companies, Suncorp group limited has the largest

capital share. After the comparison of share capital of four organisations, it will be inferred

that Telstra is growing at a low pace.

Other Equity Instruments and retained earning

Mainly equity has two components recognised as equity instrument and retain earnings.

Equity instruments is more like a document that serve as an evidence of ownership in an

organisation such as a share certificate or a warrant. Equity instruments are issued to

shareholders of the company and the fund generated is used to invest in business. Moreover,

none among the chosen four organisation offers any of the equity instrument except equity

shares.

Reserves

Reserves in the balance sheet is a subheading in the shareholders fund heading in the balance

sheet. Reserve is the part of profit apportioned for a particular purpose from the company’s

total profit. The reserve of BHP Billiton Ltd has been around AUD $ 2500 million for all the

four years from 2014 to 2017. However, the surplus kept decreasing as the years passed from

AUS $ 2927 million in 2014 to AUD $ 2557 million in 2015 to AUD $ 2400 million in 2017.

Although, the reserve amount of Telstra was negative in 2014, but it improved at a high pace.

The reserves of AGL energy limited follows the same path as of Telstra, its reserves were

also negative. However, it strived to improve and achieve a positive surplus. Among all the

four companies, the reserves of BHP Billiton ltd is highest.

Retain earnings

Retain earning is the portion of surplus earning that end up to invest the earnings in order to

increase the capital worth. These earnings are not distributed among the shareholders rather

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING: 10

they are vested in the any capital project so that the shareholders would ripe the profit in the

form of future dividends (Cahan, 2016). When the retain earnings of all four companies are

compared, it is found that BHP Billiton ltd could maintain the highest retain earning in 2014

as an amount of AUD $ 74,143 million. Retained earnings of Telstra was not so good in 2014

and 2015, nevertheless it improved in the year 2016 as AUD $ 10,074 million and as AUD $

9358 million in 2017. Somehow, Suncorp group limited maintained an average amount AUD

$ 855 million from 2014 to 2017. The crux of financial analysis is that each company has its

own way of working and figure out how this working would enhance and strengthen the

overall capital worth in a sustainable manner.

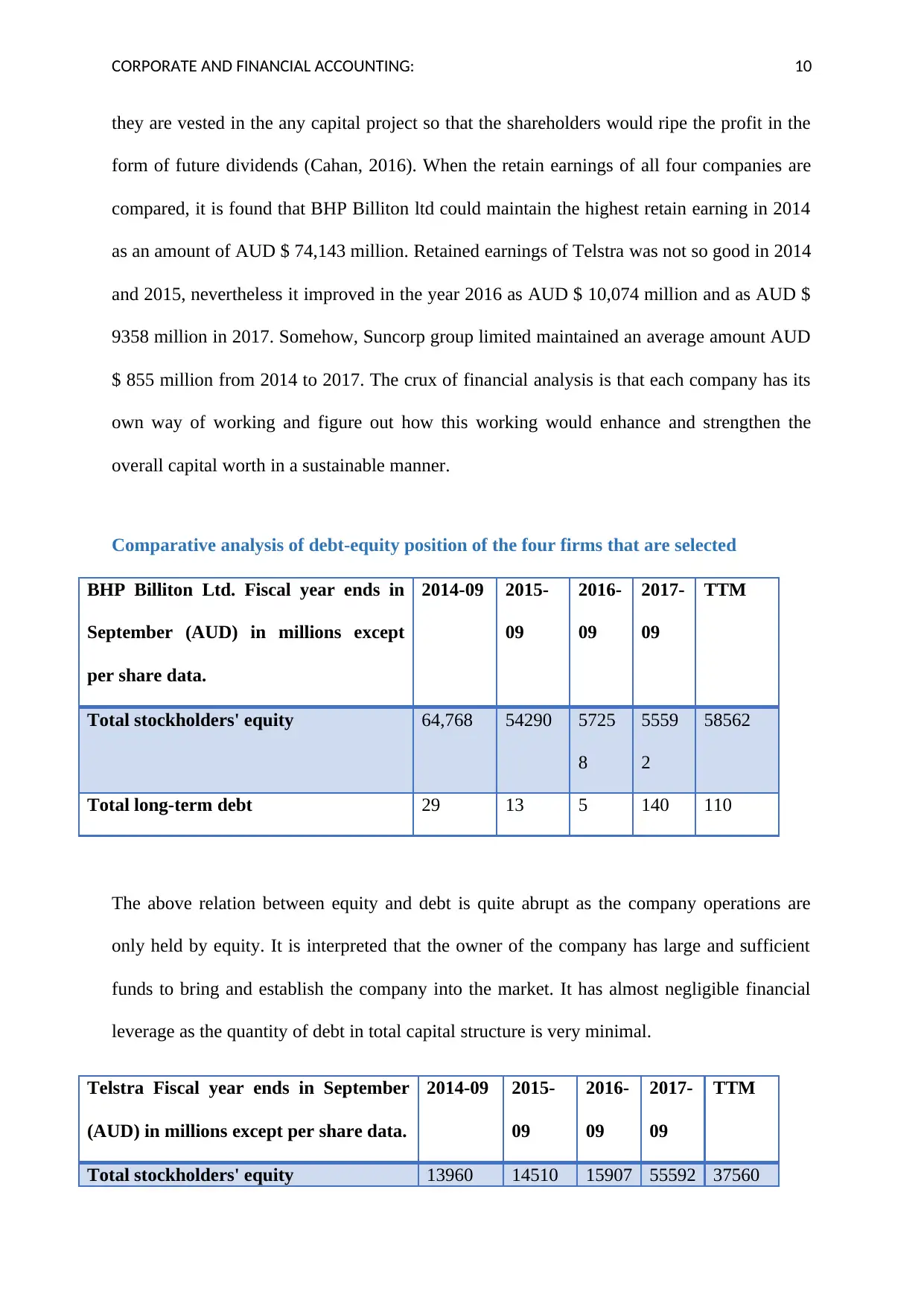

Comparative analysis of debt-equity position of the four firms that are selected

BHP Billiton Ltd. Fiscal year ends in

September (AUD) in millions except

per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 64,768 54290 5725

8

5559

2

58562

Total long-term debt 29 13 5 140 110

The above relation between equity and debt is quite abrupt as the company operations are

only held by equity. It is interpreted that the owner of the company has large and sufficient

funds to bring and establish the company into the market. It has almost negligible financial

leverage as the quantity of debt in total capital structure is very minimal.

Telstra Fiscal year ends in September

(AUD) in millions except per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 13960 14510 15907 55592 37560

they are vested in the any capital project so that the shareholders would ripe the profit in the

form of future dividends (Cahan, 2016). When the retain earnings of all four companies are

compared, it is found that BHP Billiton ltd could maintain the highest retain earning in 2014

as an amount of AUD $ 74,143 million. Retained earnings of Telstra was not so good in 2014

and 2015, nevertheless it improved in the year 2016 as AUD $ 10,074 million and as AUD $

9358 million in 2017. Somehow, Suncorp group limited maintained an average amount AUD

$ 855 million from 2014 to 2017. The crux of financial analysis is that each company has its

own way of working and figure out how this working would enhance and strengthen the

overall capital worth in a sustainable manner.

Comparative analysis of debt-equity position of the four firms that are selected

BHP Billiton Ltd. Fiscal year ends in

September (AUD) in millions except

per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 64,768 54290 5725

8

5559

2

58562

Total long-term debt 29 13 5 140 110

The above relation between equity and debt is quite abrupt as the company operations are

only held by equity. It is interpreted that the owner of the company has large and sufficient

funds to bring and establish the company into the market. It has almost negligible financial

leverage as the quantity of debt in total capital structure is very minimal.

Telstra Fiscal year ends in September

(AUD) in millions except per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 13960 14510 15907 55592 37560

CORPORATE AND FINANCIAL ACCOUNTING: 11

Total long-term debt 16716 17806 18191 17171 15258

As it is already well established that the ideal ratio of debt-equity is 2:1. The capital structure

consists of mainly two things named equity and debt. Telstra also have approximately 1.5:1

in all the four years from 2014 to 2017 (Telstra Corporation Limited, 2016).

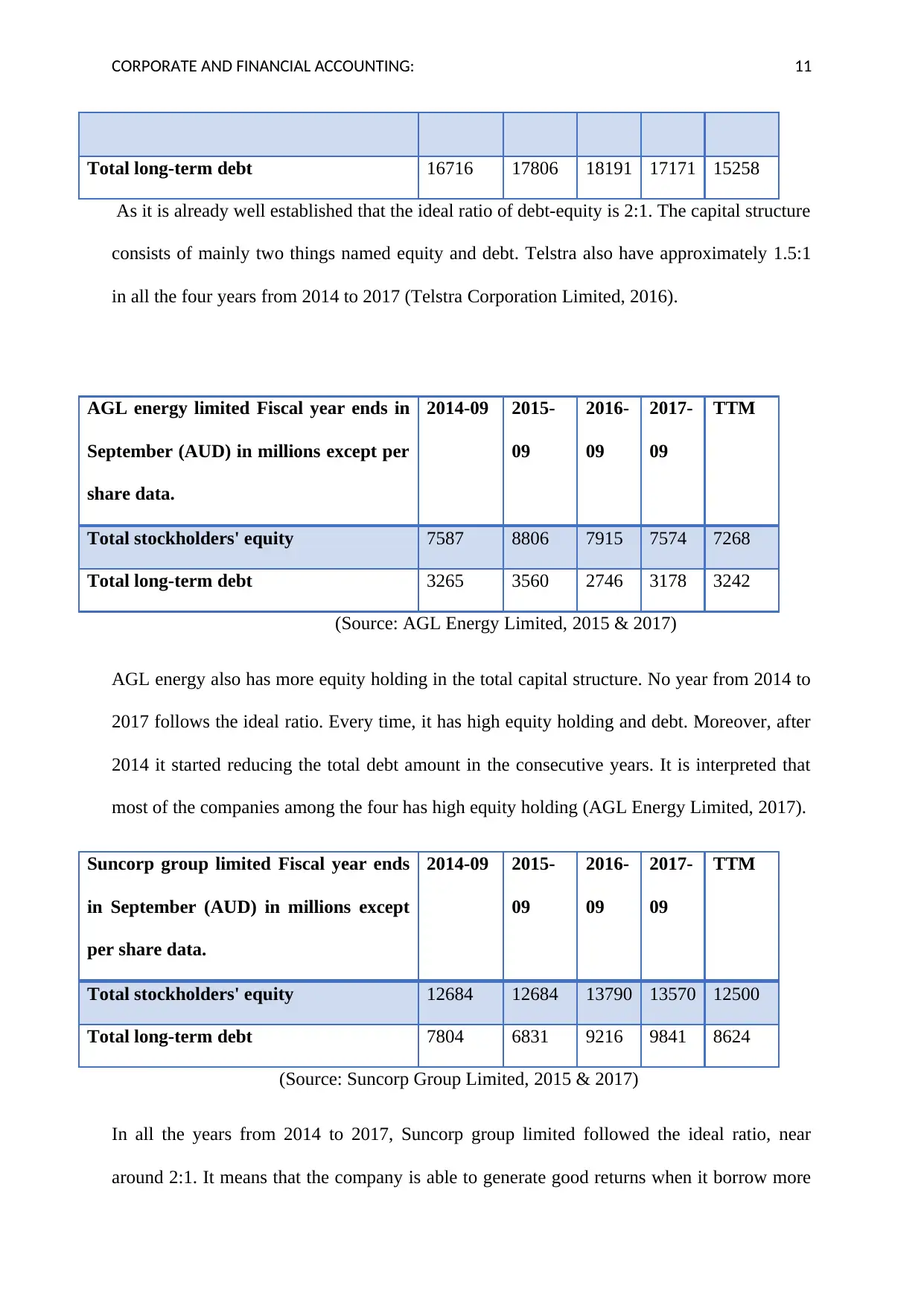

AGL energy limited Fiscal year ends in

September (AUD) in millions except per

share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 7587 8806 7915 7574 7268

Total long-term debt 3265 3560 2746 3178 3242

(Source: AGL Energy Limited, 2015 & 2017)

AGL energy also has more equity holding in the total capital structure. No year from 2014 to

2017 follows the ideal ratio. Every time, it has high equity holding and debt. Moreover, after

2014 it started reducing the total debt amount in the consecutive years. It is interpreted that

most of the companies among the four has high equity holding (AGL Energy Limited, 2017).

Suncorp group limited Fiscal year ends

in September (AUD) in millions except

per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 12684 12684 13790 13570 12500

Total long-term debt 7804 6831 9216 9841 8624

(Source: Suncorp Group Limited, 2015 & 2017)

In all the years from 2014 to 2017, Suncorp group limited followed the ideal ratio, near

around 2:1. It means that the company is able to generate good returns when it borrow more

Total long-term debt 16716 17806 18191 17171 15258

As it is already well established that the ideal ratio of debt-equity is 2:1. The capital structure

consists of mainly two things named equity and debt. Telstra also have approximately 1.5:1

in all the four years from 2014 to 2017 (Telstra Corporation Limited, 2016).

AGL energy limited Fiscal year ends in

September (AUD) in millions except per

share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 7587 8806 7915 7574 7268

Total long-term debt 3265 3560 2746 3178 3242

(Source: AGL Energy Limited, 2015 & 2017)

AGL energy also has more equity holding in the total capital structure. No year from 2014 to

2017 follows the ideal ratio. Every time, it has high equity holding and debt. Moreover, after

2014 it started reducing the total debt amount in the consecutive years. It is interpreted that

most of the companies among the four has high equity holding (AGL Energy Limited, 2017).

Suncorp group limited Fiscal year ends

in September (AUD) in millions except

per share data.

2014-09 2015-

09

2016-

09

2017-

09

TTM

Total stockholders' equity 12684 12684 13790 13570 12500

Total long-term debt 7804 6831 9216 9841 8624

(Source: Suncorp Group Limited, 2015 & 2017)

In all the years from 2014 to 2017, Suncorp group limited followed the ideal ratio, near

around 2:1. It means that the company is able to generate good returns when it borrow more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.