Corporate Accounting: Financial Analysis of BHP, Rio, Ausdrill

VerifiedAdded on 2023/04/20

|23

|4909

|209

Report

AI Summary

This report provides a comprehensive analysis of the financial statements of three ASX-listed companies: BHP Billiton, Rio Tinto, and Ausdrill Limited. The analysis covers key areas such as debt and equity positions, cash flow statements, other comprehensive income statements, and corporate taxation. The debt and equity structures of each company are contrasted using debt-to-equity ratios, revealing their financial leverage. Cash flow statements are examined to understand the companies' operating, investing, and financing activities, highlighting trends in cash generation and usage. Additionally, the report explores the components of other comprehensive income and delves into the intricacies of corporate income tax accounting, including deferred tax liabilities and tax payments. The report concludes by summarizing the financial health and strategies of each organization based on the analysis of their financial statements.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Executive Summary:

The report is focused on analysing the various items listed in the financial statements of BHP

Billiton, Rio Tinto and Ausdrill Limited. The objective is to evaluate their cash flow position,

other comprehensive income statement, debt and equity positions along with corporate taxation.

The initial section of the report has emphasised on the debt and equity aspects of the three above-

mentioned organisations. After this, the cash flow positions of the organisations are evaluated

effectively. The next section has dealt with assessing the other comprehensive income statements

of the organisations. Finally, the report has shed light on evaluating the different aspects of

taxation of the organisations.

Executive Summary:

The report is focused on analysing the various items listed in the financial statements of BHP

Billiton, Rio Tinto and Ausdrill Limited. The objective is to evaluate their cash flow position,

other comprehensive income statement, debt and equity positions along with corporate taxation.

The initial section of the report has emphasised on the debt and equity aspects of the three above-

mentioned organisations. After this, the cash flow positions of the organisations are evaluated

effectively. The next section has dealt with assessing the other comprehensive income statements

of the organisations. Finally, the report has shed light on evaluating the different aspects of

taxation of the organisations.

2CORPORATE ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................4

Equity and liability:.........................................................................................................................5

Question (i):.................................................................................................................................5

Question (ii):................................................................................................................................6

Question (iii):...............................................................................................................................7

Cash flow statement:........................................................................................................................8

Question (iv):...............................................................................................................................8

Question (v):..............................................................................................................................10

Question (vi):.............................................................................................................................13

Other comprehensive income statement:.......................................................................................14

Question (vii):............................................................................................................................14

Question (viii):...........................................................................................................................14

Question (ix):.............................................................................................................................14

Question (x):..............................................................................................................................15

Accounting for corporate income tax:...........................................................................................15

Question (xi):.............................................................................................................................15

Question (xii):............................................................................................................................16

Question (xiii):...........................................................................................................................17

Table of Contents

Introduction:....................................................................................................................................4

Equity and liability:.........................................................................................................................5

Question (i):.................................................................................................................................5

Question (ii):................................................................................................................................6

Question (iii):...............................................................................................................................7

Cash flow statement:........................................................................................................................8

Question (iv):...............................................................................................................................8

Question (v):..............................................................................................................................10

Question (vi):.............................................................................................................................13

Other comprehensive income statement:.......................................................................................14

Question (vii):............................................................................................................................14

Question (viii):...........................................................................................................................14

Question (ix):.............................................................................................................................14

Question (x):..............................................................................................................................15

Accounting for corporate income tax:...........................................................................................15

Question (xi):.............................................................................................................................15

Question (xii):............................................................................................................................16

Question (xiii):...........................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Question (xiv):...........................................................................................................................17

Question (xv):............................................................................................................................18

Question (xvi):...........................................................................................................................18

Question (xvii):..........................................................................................................................18

Conclusion:....................................................................................................................................19

References and Bibliographies:.....................................................................................................20

Question (xiv):...........................................................................................................................17

Question (xv):............................................................................................................................18

Question (xvi):...........................................................................................................................18

Question (xvii):..........................................................................................................................18

Conclusion:....................................................................................................................................19

References and Bibliographies:.....................................................................................................20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

Introduction:

The report intends to analyse the financial statements of three ASX listed organisations

functioning in the same industrial sector. The organisations chosen include BHP Billiton, Rio

Tinto and Ausdrill Limited, as they operate in the Australian mining sector. The report takes into

account the evaluation of the latest annual reports of the three organisations including the

assessment of segments such as equity and liability, other comprehensive income statement and

corporate income tax.

BHP Billiton is one of the leading mining companies in Australia, which is involved in

inventing, acquiring, developing and marketing natural resources globally. The main products of

the organisation include copper, petroleum, coal and iron ore. It has been founded in 1851 with

an employee base of 27,161 staffs (BHP 2018).

Rio Tinto is engaged in mining, finding along with processing mineral resources globally.

The organisation provides copper, aluminium, molybdenum, silver, industrial minerals, gold,

titanium dioxide, borates, iron ore, salt, uranium, metallurgical coal and iron ore. It is an Anglo-

Australian organisation established in 1973 with workforce of around 46,807 staffs

(Riotinto.com 2018).

Ausdrill Limited functions as a global mining services organisation. The main operations

include Drilling Services Australia, Contract Mining Services Africa, Equipment Services and

Supplies and other segments. The organisation is engaged in reverse circulation, rotary air blast,

diamond drilling, bores production and monitoring, surface hole drilling, rotary air blast and

Introduction:

The report intends to analyse the financial statements of three ASX listed organisations

functioning in the same industrial sector. The organisations chosen include BHP Billiton, Rio

Tinto and Ausdrill Limited, as they operate in the Australian mining sector. The report takes into

account the evaluation of the latest annual reports of the three organisations including the

assessment of segments such as equity and liability, other comprehensive income statement and

corporate income tax.

BHP Billiton is one of the leading mining companies in Australia, which is involved in

inventing, acquiring, developing and marketing natural resources globally. The main products of

the organisation include copper, petroleum, coal and iron ore. It has been founded in 1851 with

an employee base of 27,161 staffs (BHP 2018).

Rio Tinto is engaged in mining, finding along with processing mineral resources globally.

The organisation provides copper, aluminium, molybdenum, silver, industrial minerals, gold,

titanium dioxide, borates, iron ore, salt, uranium, metallurgical coal and iron ore. It is an Anglo-

Australian organisation established in 1973 with workforce of around 46,807 staffs

(Riotinto.com 2018).

Ausdrill Limited functions as a global mining services organisation. The main operations

include Drilling Services Australia, Contract Mining Services Africa, Equipment Services and

Supplies and other segments. The organisation is engaged in reverse circulation, rotary air blast,

diamond drilling, bores production and monitoring, surface hole drilling, rotary air blast and

5CORPORATE ACCOUNTING

others. The organisation is founded in 1987 having employee base of around 5,278

(Ausdrill.com.au 2018).

Equity and liability:

Question (i):

From the annual reports of the three chosen organisations, it is apparent that all of them

have certain equity items in their balance sheet statement.

As per the annual reports of Rio Tinto, there are three main equity items, which include

share capital, reserves and retained earnings. The share capital of the organisation has increased

from $4,174 million in 2015 to $4,360 million in 2017 owing to the rise in number of equity

shares. Increase in reserves could be observed from $9,139 million in 2015 to $12,284 million in

2017 owing to the increase in foreign currency translation reserve, hedge reserve and others

(Brigham et al. 2016). Finally, increase in retained earnings could be observed from $19,736

million in 2015 to $23,761 million in 2017, as it has managed to increase its profit over margin

over the years (Riotinto.com 2018).

For BHP Billiton, the main equity items include share capital, treasury shares, reserved

and retained earnings. No change could be observed in share capital from 2015 to 2017, as the

organisation has not issued additional equity shares in the market (Miller-Nobles, Mattison and

Matsumura 2016). Treasury shares are observed to decline significantly from $76 million in

2015 to $3 million in 2017, as it has minimised its share buyback strategy. Reserves are observed

to decline from $2,557 million in 2015 to $2,400 million in 2017 due to the fall in hedge reserve

and foreign currency translation reserve (Marshall 2016). Finally, retained earnings have fallen

others. The organisation is founded in 1987 having employee base of around 5,278

(Ausdrill.com.au 2018).

Equity and liability:

Question (i):

From the annual reports of the three chosen organisations, it is apparent that all of them

have certain equity items in their balance sheet statement.

As per the annual reports of Rio Tinto, there are three main equity items, which include

share capital, reserves and retained earnings. The share capital of the organisation has increased

from $4,174 million in 2015 to $4,360 million in 2017 owing to the rise in number of equity

shares. Increase in reserves could be observed from $9,139 million in 2015 to $12,284 million in

2017 owing to the increase in foreign currency translation reserve, hedge reserve and others

(Brigham et al. 2016). Finally, increase in retained earnings could be observed from $19,736

million in 2015 to $23,761 million in 2017, as it has managed to increase its profit over margin

over the years (Riotinto.com 2018).

For BHP Billiton, the main equity items include share capital, treasury shares, reserved

and retained earnings. No change could be observed in share capital from 2015 to 2017, as the

organisation has not issued additional equity shares in the market (Miller-Nobles, Mattison and

Matsumura 2016). Treasury shares are observed to decline significantly from $76 million in

2015 to $3 million in 2017, as it has minimised its share buyback strategy. Reserves are observed

to decline from $2,557 million in 2015 to $2,400 million in 2017 due to the fall in hedge reserve

and foreign currency translation reserve (Marshall 2016). Finally, retained earnings have fallen

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

from $60,044 million in 2015 to $52,618 million in 2017 due to decline in overall profit level of

the organisation (BHP 2018).

In case of Ausdrill Limited, the three equity items include contributed equity, reserves

and retained earnings. Like BHP Billiton, no change could be observed in contributed equity of

the organisation due to no additional shares issued in the meantime. However, there are

significant fall in reserves over the three-year period. Finally, significant rise in retained earnings

could be witnessed from 2015 to 2017 due to considerable increase in profitability

(Ausdrill.com.au 2018).

Question (ii):

From the annual report of Rio Tinto in 2017, there is presence of both current and non-

current liabilities. The current liabilities include borrowings and other financial liabilities, trade

payables, tax payable and provisions comprising of post-retirement benefits. The total current

liabilities have increased mainly due to rise in trade payables. Non-current liabilities comprise of

borrowings and other financial liabilities, trade payables, deferred tax liabilities, tax payables and

provisions comprising of post-retirement benefits. However, non-current liabilities have

decreased owing to considerable decline in long-term borrowings and other financial liabilities

(Riotinto.com 2018). As a result, the total liabilities have decreased from 2015 to 2017 for Rio

Tinto.

In case of BHP Billiton, the current liabilities constitute of trade payables, interest

bearing liabilities, other financial liabilities, current tax payable, provisions and deferred income.

The current liabilities have declined from $12,853 million in 2015 to $11,366 million in 2017

due to fall in trade payables. On the other hand, the non-current liabilities include trade payables,

from $60,044 million in 2015 to $52,618 million in 2017 due to decline in overall profit level of

the organisation (BHP 2018).

In case of Ausdrill Limited, the three equity items include contributed equity, reserves

and retained earnings. Like BHP Billiton, no change could be observed in contributed equity of

the organisation due to no additional shares issued in the meantime. However, there are

significant fall in reserves over the three-year period. Finally, significant rise in retained earnings

could be witnessed from 2015 to 2017 due to considerable increase in profitability

(Ausdrill.com.au 2018).

Question (ii):

From the annual report of Rio Tinto in 2017, there is presence of both current and non-

current liabilities. The current liabilities include borrowings and other financial liabilities, trade

payables, tax payable and provisions comprising of post-retirement benefits. The total current

liabilities have increased mainly due to rise in trade payables. Non-current liabilities comprise of

borrowings and other financial liabilities, trade payables, deferred tax liabilities, tax payables and

provisions comprising of post-retirement benefits. However, non-current liabilities have

decreased owing to considerable decline in long-term borrowings and other financial liabilities

(Riotinto.com 2018). As a result, the total liabilities have decreased from 2015 to 2017 for Rio

Tinto.

In case of BHP Billiton, the current liabilities constitute of trade payables, interest

bearing liabilities, other financial liabilities, current tax payable, provisions and deferred income.

The current liabilities have declined from $12,853 million in 2015 to $11,366 million in 2017

due to fall in trade payables. On the other hand, the non-current liabilities include trade payables,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

interest bearing liabilities, other financial liabilities, deferred tax liabilities, provisions and

deferred income. There has been significant decline in non-current liabilities from $54,035

million in 2015 to $42,914 million in 2017, as interest bearing liabilities have declined

considerably. This has resulted in decline in total liabilities of the organisation in 2017 (BHP

2018).

According to the annual reports of Ausdrill Limited, current liabilities include trade

payables, borrowings; current tax liabilities and employee benefit obligations, which have

increased owing to increase in employee benefit obligations. The non-current liabilities include

borrowings, deferred tax liabilities and employee benefit obligations. The amount has declined

from $433,300,000 in 2015 to $408,852 million in 2017 due to fall in long-term borrowings

(Ausdrill.com.au 2018).

Question (iii):

In order to contrast the debt and equity position of the three organisations, debt-to-equity

ratio is deemed to be the most suitable measure.

interest bearing liabilities, other financial liabilities, deferred tax liabilities, provisions and

deferred income. There has been significant decline in non-current liabilities from $54,035

million in 2015 to $42,914 million in 2017, as interest bearing liabilities have declined

considerably. This has resulted in decline in total liabilities of the organisation in 2017 (BHP

2018).

According to the annual reports of Ausdrill Limited, current liabilities include trade

payables, borrowings; current tax liabilities and employee benefit obligations, which have

increased owing to increase in employee benefit obligations. The non-current liabilities include

borrowings, deferred tax liabilities and employee benefit obligations. The amount has declined

from $433,300,000 in 2015 to $408,852 million in 2017 due to fall in long-term borrowings

(Ausdrill.com.au 2018).

Question (iii):

In order to contrast the debt and equity position of the three organisations, debt-to-equity

ratio is deemed to be the most suitable measure.

8CORPORATE ACCOUNTING

2016 2017 2018

-

0.20

0.40

0.60

0.80

1.00

1.20

0.77

0.98

0.87

1.07

0.95

0.87

1.04

0.90 0.88

Debt to Equity Ratio

BHP Billiton Rio Rinto Ausdrill Limited

From the above table and figure, it could be observed that all three organisations utilise

more debt capital rather than equity financing for meeting their capital needs. Out of these

organisations, the maximum amount of debt capital is used by Rio Tinto and Ausdrill Limited.

However, in terms of liabilities, Ausdrill Limited has the lowest liability amount compared to the

other two organisations. Thus, in terms of financial leverage, BHP Billiton has the lowest

amount of risk followed by Ausdrill Limited and Rio Tinto.

Cash flow statement:

Question (iv):

From the cash flow statements of BHP Billiton, the main items under operating cash

flows include dividends received, interest paid and interest received, income tax refund and

payment and changes in assets and liabilities. These cash flows have fallen considerably from

2015 to 2016; however, improvements could be observed in 2017. The investing cash flows of

the organisation mainly include purchase of property, plant and equipment, exploration expense,

2016 2017 2018

-

0.20

0.40

0.60

0.80

1.00

1.20

0.77

0.98

0.87

1.07

0.95

0.87

1.04

0.90 0.88

Debt to Equity Ratio

BHP Billiton Rio Rinto Ausdrill Limited

From the above table and figure, it could be observed that all three organisations utilise

more debt capital rather than equity financing for meeting their capital needs. Out of these

organisations, the maximum amount of debt capital is used by Rio Tinto and Ausdrill Limited.

However, in terms of liabilities, Ausdrill Limited has the lowest liability amount compared to the

other two organisations. Thus, in terms of financial leverage, BHP Billiton has the lowest

amount of risk followed by Ausdrill Limited and Rio Tinto.

Cash flow statement:

Question (iv):

From the cash flow statements of BHP Billiton, the main items under operating cash

flows include dividends received, interest paid and interest received, income tax refund and

payment and changes in assets and liabilities. These cash flows have fallen considerably from

2015 to 2016; however, improvements could be observed in 2017. The investing cash flows of

the organisation mainly include purchase of property, plant and equipment, exploration expense,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

proceeds from asset sale and proceeds from divestment of operations, subsidiaries and joint

operations. The investing cash flows have fallen over the year mainly due to decline in purchase

of property, plant and equipment implying less investment on fixed assets (Gordon et al. 2017).

In case of financing cash flows, the significant items include proceeds from interest bearing

liabilities, settlements or proceeds from instruments associated with debt, repayment of interest

bearing liabilities, ordinary share proceeds, share purchase for staffs and others. These cash

flows have increased significantly in 2017 owing to lower proceeds generated from interest

bearing liabilities. However, the significant rise in operating cash flows have offset such increase

due to which increase in closing cash balance could be observed in 2017 (BHP 2018).

In case of Rio Tinto, the major items falling under operating cash flows include dividend

from equity-accounted units, consolidated operational cash flows, payment of net interest and

dividend and tax payment. These cash flows have increased considerably from 2015 to 2017

owing to increase in consolidated operational cash flows. The investing cash flows of the

organisation constitute of purchase and sale of fixed and intangible assets, disposals of

subsidiaries, joint ventures and subsidiaries, purchase and sale of financial assets acquisitions of

subsidiaries, joint ventures and subsidiaries. These cash flows have fallen from 2015 to 2017 due

to increased earnings from disposals made. The financing cash flows include payment of equity

dividends, proceeds from and repayment of borrowings, share repurchase and others. The main

reason that these cash flows have increased in 2017 is due to share repurchase and payment of

equity dividend. As a result, positive increase in cash balance could be observed in 2017

(Riotinto.com 2018).

For Ausdrill Limited, the main items falling under operating cash flows include customer

receipts, supplier payments, interest receipt and payment, income tax refund and payment along

proceeds from asset sale and proceeds from divestment of operations, subsidiaries and joint

operations. The investing cash flows have fallen over the year mainly due to decline in purchase

of property, plant and equipment implying less investment on fixed assets (Gordon et al. 2017).

In case of financing cash flows, the significant items include proceeds from interest bearing

liabilities, settlements or proceeds from instruments associated with debt, repayment of interest

bearing liabilities, ordinary share proceeds, share purchase for staffs and others. These cash

flows have increased significantly in 2017 owing to lower proceeds generated from interest

bearing liabilities. However, the significant rise in operating cash flows have offset such increase

due to which increase in closing cash balance could be observed in 2017 (BHP 2018).

In case of Rio Tinto, the major items falling under operating cash flows include dividend

from equity-accounted units, consolidated operational cash flows, payment of net interest and

dividend and tax payment. These cash flows have increased considerably from 2015 to 2017

owing to increase in consolidated operational cash flows. The investing cash flows of the

organisation constitute of purchase and sale of fixed and intangible assets, disposals of

subsidiaries, joint ventures and subsidiaries, purchase and sale of financial assets acquisitions of

subsidiaries, joint ventures and subsidiaries. These cash flows have fallen from 2015 to 2017 due

to increased earnings from disposals made. The financing cash flows include payment of equity

dividends, proceeds from and repayment of borrowings, share repurchase and others. The main

reason that these cash flows have increased in 2017 is due to share repurchase and payment of

equity dividend. As a result, positive increase in cash balance could be observed in 2017

(Riotinto.com 2018).

For Ausdrill Limited, the main items falling under operating cash flows include customer

receipts, supplier payments, interest receipt and payment, income tax refund and payment along

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

with receipt of management fee. These cash flows have decreased from 2015 to 2017 due to fall

in receipts from customers. The investing cash flow items primarily include payments for fixed

assets and investments, proceeds from fixed assets and business sale and others. The reason that

these cash flows have increased from 2015 to 2017 is due to considerable payment for fixed

assets, particularly, property, plant and equipment. The financing cash flow items include

repayment of hire purchase, secured borrowings and lease liabilities, dividend payment to

shareholders and proceeds from and repayment of unsecured borrowings. These cash flows have

decreased considerably due to repayment of secured borrowings. Due to this, increase in cash

balance could be observed in 2017 compared to 2016 (Ausdrill.com.au 2018).

Question (v):

BHP Billion:

with receipt of management fee. These cash flows have decreased from 2015 to 2017 due to fall

in receipts from customers. The investing cash flow items primarily include payments for fixed

assets and investments, proceeds from fixed assets and business sale and others. The reason that

these cash flows have increased from 2015 to 2017 is due to considerable payment for fixed

assets, particularly, property, plant and equipment. The financing cash flow items include

repayment of hire purchase, secured borrowings and lease liabilities, dividend payment to

shareholders and proceeds from and repayment of unsecured borrowings. These cash flows have

decreased considerably due to repayment of secured borrowings. Due to this, increase in cash

balance could be observed in 2017 compared to 2016 (Ausdrill.com.au 2018).

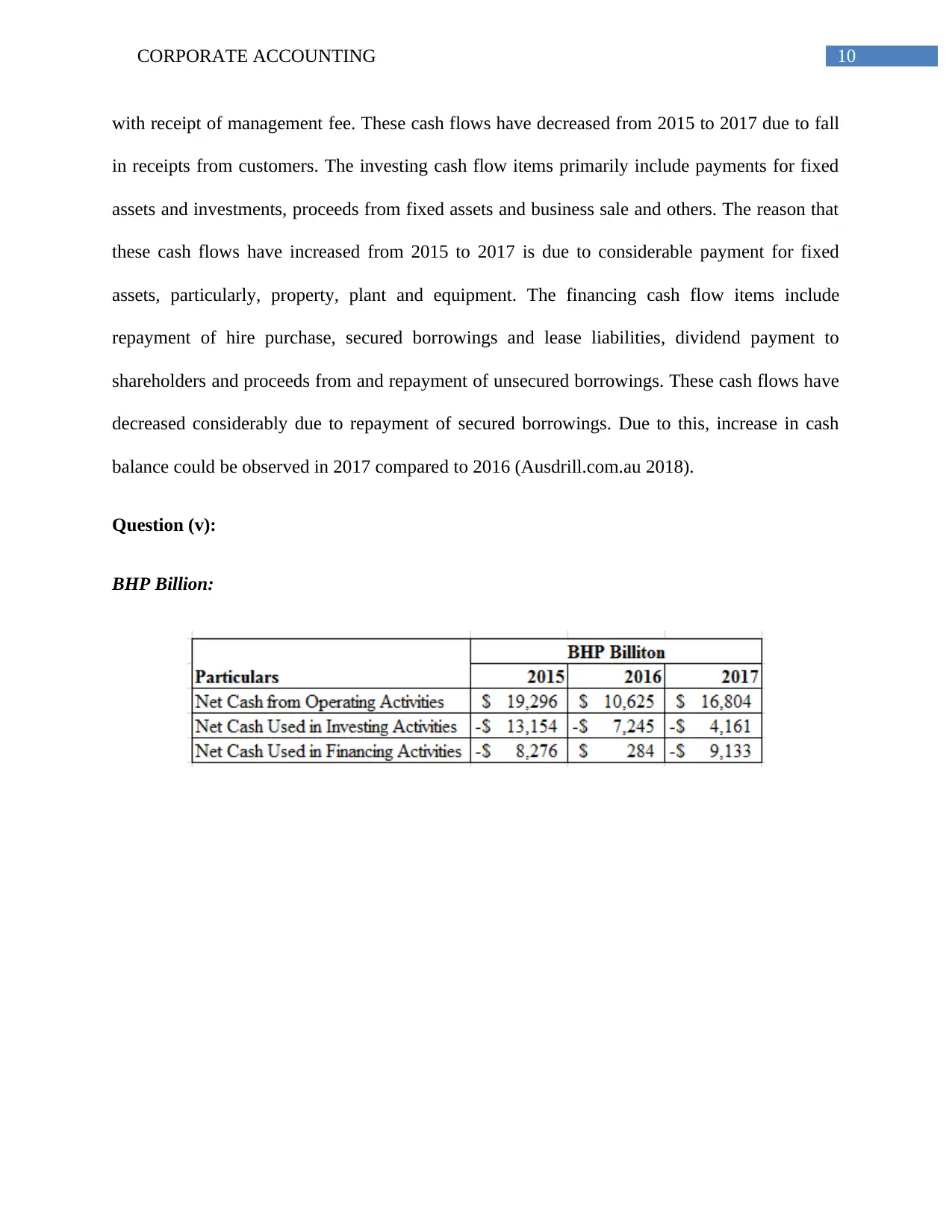

Question (v):

BHP Billion:

11CORPORATE ACCOUNTING

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$19,296

$10,625

$16,804

-$13,154

-$7,245

-$4,161

-$8,276

$284

-$9,133

BHP Billiton

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

It could be observed from the above figure that the operating cash flows of the

organisation have declined from 2015 to 2017 and this denotes falling business income from

operational business functions (Khansalar and Namazi 2017). After this, the organisation has

decreased its investment over the years by minimising the payment of fixed assets. However, it

has incurred huge expenses for repaying interest bearing liabilities (BHP 2018).

Rio Tinto:

2015 2016 2017

-$15,000

-$10,000

-$5,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$19,296

$10,625

$16,804

-$13,154

-$7,245

-$4,161

-$8,276

$284

-$9,133

BHP Billiton

Net Cash from Operating Activities Net Cash Used in Investing Activities

Net Cash Used in Financing Activities

It could be observed from the above figure that the operating cash flows of the

organisation have declined from 2015 to 2017 and this denotes falling business income from

operational business functions (Khansalar and Namazi 2017). After this, the organisation has

decreased its investment over the years by minimising the payment of fixed assets. However, it

has incurred huge expenses for repaying interest bearing liabilities (BHP 2018).

Rio Tinto:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.