Capital Structure: Debt/Equity Ratio of Tesco, Morrisons, Sainsbury

VerifiedAdded on 2022/12/28

|39

|12029

|22

Report

AI Summary

This report provides an in-depth analysis of the capital structures of three major UK retail companies: Tesco, Morrisons, and Sainsbury. It begins with an introduction to capital structure, explaining the concepts of debt and equity, and the debt/equity ratio. A comprehensive literature review explores existing research on capital structure theories, including the trade-off theory, agency cost hypothesis, and pecking order theory. The methodology section outlines the approach to be taken, which involves calculating financial ratios using data from the companies' financial statements over three consecutive years. The research questions focus on understanding the concept of capital structure, the factors affecting it, and the relationship between capital structure and profitability. The analysis includes the calculation and interpretation of relevant financial ratios. The report also includes a discussion of alternative research and future perspectives on capital structure. The report concludes with a summary of the findings and a list of references.

Capital Structure- Debt

Equity Ratio of Tesco

Morrisons and Sainsbury

Equity Ratio of Tesco

Morrisons and Sainsbury

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Types of Capital Structure:..........................................................................................................3

Debt / Equity Ratio:.....................................................................................................................3

Literature review..............................................................................................................................6

Methodology..................................................................................................................................11

Calculation of all ratios..............................................................................................................11

Research questions.....................................................................................................................17

Analysis of questions and three consecutive years of data analysis..........................................17

Results of Analysis....................................................................................................................23

Alternative research...................................................................................................................28

Future perspective on Capital structure.....................................................................................30

Conclusion.....................................................................................................................................31

References......................................................................................................................................34

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Types of Capital Structure:..........................................................................................................3

Debt / Equity Ratio:.....................................................................................................................3

Literature review..............................................................................................................................6

Methodology..................................................................................................................................11

Calculation of all ratios..............................................................................................................11

Research questions.....................................................................................................................17

Analysis of questions and three consecutive years of data analysis..........................................17

Results of Analysis....................................................................................................................23

Alternative research...................................................................................................................28

Future perspective on Capital structure.....................................................................................30

Conclusion.....................................................................................................................................31

References......................................................................................................................................34

INTRODUCTION

Background

Capital structure is the mixture of debt and equity that a company used to finance its activity. Equity

include equity share, preferred share, retained earnings and other long term debt while debt include

bonds and loan. It includes the way a company funds its operations and growth. Debt is external

source of the company and it is due to the money lender with interest. Equity is owner's own capital

and is not burden for the company. By issuing equity, firm get investment by giving ownership to

investor in the company without the need to payback (Abdulla, 2017).

Types of Capital Structure:

Equity Capital: Equity capital is shareholders own capital and include equity share, preference

share, retained earning etc. These fund increase the creditworthiness of the firm and does not create

burden of interest on firm as the firm is not bound to give them dividends on shares. The cost of

these funds are low as compare to debt funds. Equity shareholders get dividend for their investment

and also get ownership in the business.

Debt Capital: Debt funds are outsider's fund as these include loan and bonds. The cost of these funds

are high and it decrease the creditworthiness of the firm. They are liability for the firm and create

burden of interest on the firm. Debt capital holders cannot become owner of the company, they are

just creditor for the company and get interest for their investment. They are preference for the

company as they get interest before the shareholders.

Debt / Equity Ratio:

It is the financial ratio that show proportion of debt and equity used to fund company's operation and

growth. Calculation is done by dividing company liability with equity (An, Li and Yu, 2016). The

components needed for calculation are financial statement and balance sheet of the company. The

calculation is done on market value of both equity and capital. The debt includes only long term

debt to calculate financial leverage of the company. This ratio measures the firm's debt to the value

of its assets. The reason behind this is to know that to what extent a company is taking debt to

leverage of assets. Higher debt / equity ratio indicates higher risk as it shows that company is

financing its growth with debt capital. If the company is using debt to finance growth and could

generate profit than it has without that finance. If the leverage increases more profit than the cost or

interest than shareholders would get benefit. But if the cost is more than the profit than it leads to

decrease the value of shares. The cost of debt is depending on the market conditions. The economist

refers all the liabilities as debt and addition of equity and liabilities are equals to total value of

Background

Capital structure is the mixture of debt and equity that a company used to finance its activity. Equity

include equity share, preferred share, retained earnings and other long term debt while debt include

bonds and loan. It includes the way a company funds its operations and growth. Debt is external

source of the company and it is due to the money lender with interest. Equity is owner's own capital

and is not burden for the company. By issuing equity, firm get investment by giving ownership to

investor in the company without the need to payback (Abdulla, 2017).

Types of Capital Structure:

Equity Capital: Equity capital is shareholders own capital and include equity share, preference

share, retained earning etc. These fund increase the creditworthiness of the firm and does not create

burden of interest on firm as the firm is not bound to give them dividends on shares. The cost of

these funds are low as compare to debt funds. Equity shareholders get dividend for their investment

and also get ownership in the business.

Debt Capital: Debt funds are outsider's fund as these include loan and bonds. The cost of these funds

are high and it decrease the creditworthiness of the firm. They are liability for the firm and create

burden of interest on the firm. Debt capital holders cannot become owner of the company, they are

just creditor for the company and get interest for their investment. They are preference for the

company as they get interest before the shareholders.

Debt / Equity Ratio:

It is the financial ratio that show proportion of debt and equity used to fund company's operation and

growth. Calculation is done by dividing company liability with equity (An, Li and Yu, 2016). The

components needed for calculation are financial statement and balance sheet of the company. The

calculation is done on market value of both equity and capital. The debt includes only long term

debt to calculate financial leverage of the company. This ratio measures the firm's debt to the value

of its assets. The reason behind this is to know that to what extent a company is taking debt to

leverage of assets. Higher debt / equity ratio indicates higher risk as it shows that company is

financing its growth with debt capital. If the company is using debt to finance growth and could

generate profit than it has without that finance. If the leverage increases more profit than the cost or

interest than shareholders would get benefit. But if the cost is more than the profit than it leads to

decrease the value of shares. The cost of debt is depending on the market conditions. The economist

refers all the liabilities as debt and addition of equity and liabilities are equals to total value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assets. Hence it an accounting identity. It is calculated by previous year data and used to assess the

financial soundness of the firm.

About companies

Morrison’s is the fourth largest retail supermarkets in United Kingdom. It is public limited

company. This company is founded by William Morrison and founded in 1899. Headquarters in

Bradford, England, UK. Till 2020 there are 494 stores across Wales, England and Scotland. Number

of employees work in this company is 110000. Morrison start with butter and egg stall in Rawson

Market in England. This company is a part of FTSE 100 Index on London Stock Exchange.

Recently, in last summer Amazon tie-up a wholesale deal with Morrison supermarket. Current

operations in this company is store format, online retail and home delivery service. Slogan of

Morrison is 'Morrison’s Make it' to create brand heritage with new logo. Main business of this

company is offering grocery and fresh food. This company offers products and manufacture food

like World foods, Nutmeg clothing, meat, fish, bakery and flowers.

Sainsbury's is the second largest retail supermarket in the United Kingdom. This company is

founded by John James Sainsbury in year 1869 in Holborn, London, United Kingdom. It is public

limited company. Headquarters in London, England, UK. As of March 2019, there are 1428 shops

across London. Holding company of Sainsbury is Sainsbury's Supermarkets, Sainsbury's Bank and

Sainsbury's Argos. The revenue of the company is 2900.7 crore in 2019. number of employees in

this organisation is 116400. Share price of Sainsbury's is 244 and is part of FTSE 100 Index on

London stock exchange. The purpose of Asda and Sainsbury's is to merge their company but due to

increase in price, the Competition and Markets Authority not allowed them to merge (Ardalan,

2017). In Novemeber 2020, company stated to close their supermarket and the 3500 job were at risk.

Some of the Sainsbury's supermarket selling fuel, operates cafe, local market and internet shopping.

Aim - “To investigate the impact of capital structure on firm's profitability in the context of retail

sector – A study on Tesco, Morrisons and Sainsbury.”

Objectives –

To analyse the concept of capital structure of the organization.

To evaluate the factors that affects capital structure of the companies.

To evaluate the ways to attain optimum capital structure of the business.

To analyse the interrelationship between capital structure and profitability of the

organization.

Research Questions:

What is the concept of capital structure of the firm?

What are the factors affecting capital structure of organization?

financial soundness of the firm.

About companies

Morrison’s is the fourth largest retail supermarkets in United Kingdom. It is public limited

company. This company is founded by William Morrison and founded in 1899. Headquarters in

Bradford, England, UK. Till 2020 there are 494 stores across Wales, England and Scotland. Number

of employees work in this company is 110000. Morrison start with butter and egg stall in Rawson

Market in England. This company is a part of FTSE 100 Index on London Stock Exchange.

Recently, in last summer Amazon tie-up a wholesale deal with Morrison supermarket. Current

operations in this company is store format, online retail and home delivery service. Slogan of

Morrison is 'Morrison’s Make it' to create brand heritage with new logo. Main business of this

company is offering grocery and fresh food. This company offers products and manufacture food

like World foods, Nutmeg clothing, meat, fish, bakery and flowers.

Sainsbury's is the second largest retail supermarket in the United Kingdom. This company is

founded by John James Sainsbury in year 1869 in Holborn, London, United Kingdom. It is public

limited company. Headquarters in London, England, UK. As of March 2019, there are 1428 shops

across London. Holding company of Sainsbury is Sainsbury's Supermarkets, Sainsbury's Bank and

Sainsbury's Argos. The revenue of the company is 2900.7 crore in 2019. number of employees in

this organisation is 116400. Share price of Sainsbury's is 244 and is part of FTSE 100 Index on

London stock exchange. The purpose of Asda and Sainsbury's is to merge their company but due to

increase in price, the Competition and Markets Authority not allowed them to merge (Ardalan,

2017). In Novemeber 2020, company stated to close their supermarket and the 3500 job were at risk.

Some of the Sainsbury's supermarket selling fuel, operates cafe, local market and internet shopping.

Aim - “To investigate the impact of capital structure on firm's profitability in the context of retail

sector – A study on Tesco, Morrisons and Sainsbury.”

Objectives –

To analyse the concept of capital structure of the organization.

To evaluate the factors that affects capital structure of the companies.

To evaluate the ways to attain optimum capital structure of the business.

To analyse the interrelationship between capital structure and profitability of the

organization.

Research Questions:

What is the concept of capital structure of the firm?

What are the factors affecting capital structure of organization?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

What are the ways to attain optimum capital structure of the business?

What is the interrelationship between profitability and capital structure of the organization?

What is the interrelationship between profitability and capital structure of the organization?

Literature review

Modigliani and Miller performed an innovative study regarding theories of capital structure,

however suggested that perhaps the it was the concept that the firm’s capital structure has little to do

with the company's value throughout the entire economy (Armenter and Hnatkovska, 2017).

Scholars have extensively researched the issue of the firm’s capital structure. The trade-off

hypothesis was suggested by Robichek and others. If businesses determine the capital structure,

potential tax evasion impact and the liability insolvency cost should be weighed. The agency's

expense hypothesis was suggested by Jesen and Mecklingas it divides the expense of equity

agencies, which are induced by improprieties between board and stakeholders, between two firms

and the expense of a loan agency which is induced by improprieties between borrowers and

stakeholders. In its first behaviour of the building of assets, Ross introduced asymmetric details.

Ross recommended that individuals had internal knowledge about potential business incomes and

investment costs, while analysts are not aware of the scheme of rewards for management because

then stakeholders can determine the company's stock valuation only implicitly by means from the

management. The organizational debt ratio or arrangement of asset-liability seems to be a signalling

device that transmits internal market knowledge. The risk of bankruptcy is adjusted with the

performance of the service and positively linked to the equity size, the higher indebtedness ratio is

considered an indication of great quality by foreign buyers, The company's worth and the debt share

are compared positively. The priority funding hypothesis was suggested, assuming that equity

investment would communicate unfavourable market knowledge and that foreign financing would

pay for different expenses in greater part. Companies are typically funded by international finance,

debt finance and financing decision. Giannetti argued that perhaps the working capital of firms in

some developing countries is influenced by another element at business level, mostly in light of the

business's effect on the financial performance. They claim that the key considerations impacting the

financial organizational culture are the valuation including its company's properties, the scale as

well as the rate of tax towards non-debt. As per Frank and Goyal, medium corporate leverage, book

capital requirements, debt protection capacity, productivity, dividend payments, asset regression

coefficients, as well as the fixed influence of a firm or management are all factors influencing the

corporation's leverage (Bandyopadhyay and Barua, 2016).

Their analysis in 2008 indicates that a strong link occurs between income, development as

well as other metrics and composition of resources again from viewpoint of company-level

parameters. From a business point of view, there are reciprocal effects between the level of

performance across commodity markets as well as the capital structure of various industries. In the

words they feel that debt protection potential (net assets / Total Assets Book), risk (point difference

Modigliani and Miller performed an innovative study regarding theories of capital structure,

however suggested that perhaps the it was the concept that the firm’s capital structure has little to do

with the company's value throughout the entire economy (Armenter and Hnatkovska, 2017).

Scholars have extensively researched the issue of the firm’s capital structure. The trade-off

hypothesis was suggested by Robichek and others. If businesses determine the capital structure,

potential tax evasion impact and the liability insolvency cost should be weighed. The agency's

expense hypothesis was suggested by Jesen and Mecklingas it divides the expense of equity

agencies, which are induced by improprieties between board and stakeholders, between two firms

and the expense of a loan agency which is induced by improprieties between borrowers and

stakeholders. In its first behaviour of the building of assets, Ross introduced asymmetric details.

Ross recommended that individuals had internal knowledge about potential business incomes and

investment costs, while analysts are not aware of the scheme of rewards for management because

then stakeholders can determine the company's stock valuation only implicitly by means from the

management. The organizational debt ratio or arrangement of asset-liability seems to be a signalling

device that transmits internal market knowledge. The risk of bankruptcy is adjusted with the

performance of the service and positively linked to the equity size, the higher indebtedness ratio is

considered an indication of great quality by foreign buyers, The company's worth and the debt share

are compared positively. The priority funding hypothesis was suggested, assuming that equity

investment would communicate unfavourable market knowledge and that foreign financing would

pay for different expenses in greater part. Companies are typically funded by international finance,

debt finance and financing decision. Giannetti argued that perhaps the working capital of firms in

some developing countries is influenced by another element at business level, mostly in light of the

business's effect on the financial performance. They claim that the key considerations impacting the

financial organizational culture are the valuation including its company's properties, the scale as

well as the rate of tax towards non-debt. As per Frank and Goyal, medium corporate leverage, book

capital requirements, debt protection capacity, productivity, dividend payments, asset regression

coefficients, as well as the fixed influence of a firm or management are all factors influencing the

corporation's leverage (Bandyopadhyay and Barua, 2016).

Their analysis in 2008 indicates that a strong link occurs between income, development as

well as other metrics and composition of resources again from viewpoint of company-level

parameters. From a business point of view, there are reciprocal effects between the level of

performance across commodity markets as well as the capital structure of various industries. In the

words they feel that debt protection potential (net assets / Total Assets Book), risk (point difference

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

throughout the operating income/total assets book) and corporate size are now the firm's

management variables which decide the framework of resources (logarithm of total sales). Tax rate

(annual effective tax rate), growth potential (assets ratio relative to the book value), revenue (total

assets proportion to income), liquidity (to existing assets ratio) and business indicator in dummy.

The Business's corporate-level factors include: MTB(asset valuation to purchase price ration),

profitability(((pre-tax benefit + interest)/total asset value book), size(total asset value ledger)

Logarithm, collateral value(collateral) dummy contingent dividend payments(or 1 special dividend

throughout the current year) as well as the fluctuating period and c changing fixed impact (Baum,

Caglayan and Rashid, 2017).

From the viewpoint of national impacts of the capital system, Korajczyk and Levy was using the

company's gross turnover, short-term inflation rates, maturity allocation as well as credit extensions

in order to calculate market stability. The adjustment of the market financial leverage is now in the

economic cyclical mode, which really is aligned with either the finance order principle; whereas in

the business cycle version that liquidity position is in line with commercial theory, also with

economically tightened company responsible for 10 percent of the random sample. It also argue that

in lots of countries the regulatory climate has a direct effect on the financial structure of a business.

In particular, key perspectives consider the impact on capital system directly and indirectly from the

organizational characteristics (financial sector structures) – bond production, creditors power

security, compliance perfection, stock control security, stock position ratio, financial speculation

rate, including GNP rate of increase (Bulathsinhalage and Pathirawasam, 2017). As per the

organization expense hypothesis, scientists have done a great deal of study from the viewpoint of the

effect of management share capital on financial performance, as well as the findings are not similar.

Negative associations can sometimes be substantially positive and could also appear in a U-shape.

This is the respective research literature. The relationship between controlling shares and

responsibilities as well as results demonstrated a detrimental relationship to the leverage ratio in the

managing shareholder, R&D, performance, interest rate risk and executive compensation. The debt

ratio is positively related. The effect of the corporate strategy on the organisational working capital

was analysed. The findings indicate that management, business governance, performance

outcomes, R&D as well as strategic equity have a significant negative relationship to the financial

leverage. A significant relationship mostly with financial leverage lies in the amount of capital

allocation. This has also been noticed that major shareholders and financial leverage of management

are U-shaped. It indicates that managers own just under 1% of securities and leverages would rose

as shareholdings go up, while managers hold many as 5%. The growth in management stakes would

management variables which decide the framework of resources (logarithm of total sales). Tax rate

(annual effective tax rate), growth potential (assets ratio relative to the book value), revenue (total

assets proportion to income), liquidity (to existing assets ratio) and business indicator in dummy.

The Business's corporate-level factors include: MTB(asset valuation to purchase price ration),

profitability(((pre-tax benefit + interest)/total asset value book), size(total asset value ledger)

Logarithm, collateral value(collateral) dummy contingent dividend payments(or 1 special dividend

throughout the current year) as well as the fluctuating period and c changing fixed impact (Baum,

Caglayan and Rashid, 2017).

From the viewpoint of national impacts of the capital system, Korajczyk and Levy was using the

company's gross turnover, short-term inflation rates, maturity allocation as well as credit extensions

in order to calculate market stability. The adjustment of the market financial leverage is now in the

economic cyclical mode, which really is aligned with either the finance order principle; whereas in

the business cycle version that liquidity position is in line with commercial theory, also with

economically tightened company responsible for 10 percent of the random sample. It also argue that

in lots of countries the regulatory climate has a direct effect on the financial structure of a business.

In particular, key perspectives consider the impact on capital system directly and indirectly from the

organizational characteristics (financial sector structures) – bond production, creditors power

security, compliance perfection, stock control security, stock position ratio, financial speculation

rate, including GNP rate of increase (Bulathsinhalage and Pathirawasam, 2017). As per the

organization expense hypothesis, scientists have done a great deal of study from the viewpoint of the

effect of management share capital on financial performance, as well as the findings are not similar.

Negative associations can sometimes be substantially positive and could also appear in a U-shape.

This is the respective research literature. The relationship between controlling shares and

responsibilities as well as results demonstrated a detrimental relationship to the leverage ratio in the

managing shareholder, R&D, performance, interest rate risk and executive compensation. The debt

ratio is positively related. The effect of the corporate strategy on the organisational working capital

was analysed. The findings indicate that management, business governance, performance

outcomes, R&D as well as strategic equity have a significant negative relationship to the financial

leverage. A significant relationship mostly with financial leverage lies in the amount of capital

allocation. This has also been noticed that major shareholders and financial leverage of management

are U-shaped. It indicates that managers own just under 1% of securities and leverages would rose

as shareholdings go up, while managers hold many as 5%. The growth in management stakes would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

limit corporate leverage. There are no important ties between management portfolios as well as the

leverage level while managers possess upwards of 1% but much less under 5%.

Cash compensation responsiveness, shares, shares, firing and allowance for stock awards and

choices available is significantly higher than the salary incentives and promotions. Pension funding

sensitivity In order to determine the exposure to compensation results, stocks as well as options,

from Core and Guay are being used and adjustments in managers' real assets are proportional to

changes in market linked assets (Chadha and Sharma, 2016). Frank and Goyal maintain that the

association between PPS and corps leverage is substantially negative, but also that manager equity

portfolios contribute to business leveraging to different degrees. Company profits influences

managers' propensity for risk by executive fund exposure to market and market income volatility

that indicate that the sensitivity of their investments is adversely linked to short-term leverage and

also that portfolios are affected by stock income. The sensitivity to short-term debt is strongly

correlated. They claim that the compensation success sensitivity (PPS) is highly negatively linked to

corporate leveraging however because of the interaction among PPS including individual firms'

bankruptcy costs. The effect wherein the management' equity ratio as well as the percentage of

government stocks are associated greatly with the financial leverage. The research also shows what

the development, size, debt-free tax security and productivity of the group are major factors

determining the financial performance of listed companies in UK. It has shown that coded business

administrators are responsible for adjusting the amount of debt capital to self-interest. Legal

personal shares have a limiting influence on top executives' freedom to adapt their economic

position in compliance with their own purpose, albeit at a high degree. Where the top business

seems to have a significant level of equity, shareholdings of the legal individual often have a

significant role to play in supporting the self-interest of managers as well as the rights of other

shareholders (Daskalakis, Balios and Dalla, 2017). Group authorities are responsible for focusing on

financial performance. Capital value and composition of capital are relational partnerships that

affect each other. Many books have explored the effect on manager compensation of the capital

system. Theories and observational research were taken by researchers. In particular, there is a

strong connection between the financial structure and also the management salaries, which is driven

by excessive borrowing costs that raise the company's insolvency costs, which contributes to

unfavourable rewards for managers. These research support the assertion that perhaps the capital

system impacts executive pay by its effect on the cost of financial distress of intellectual resources.

From such an executive salaries effect on the organisational structure, it has been shown by Meng

Science that the organisation is controlled by the compensation packages and the corporate balance

sheet. The endogenously linked considerations are primarily the viability and business of the group.

leverage level while managers possess upwards of 1% but much less under 5%.

Cash compensation responsiveness, shares, shares, firing and allowance for stock awards and

choices available is significantly higher than the salary incentives and promotions. Pension funding

sensitivity In order to determine the exposure to compensation results, stocks as well as options,

from Core and Guay are being used and adjustments in managers' real assets are proportional to

changes in market linked assets (Chadha and Sharma, 2016). Frank and Goyal maintain that the

association between PPS and corps leverage is substantially negative, but also that manager equity

portfolios contribute to business leveraging to different degrees. Company profits influences

managers' propensity for risk by executive fund exposure to market and market income volatility

that indicate that the sensitivity of their investments is adversely linked to short-term leverage and

also that portfolios are affected by stock income. The sensitivity to short-term debt is strongly

correlated. They claim that the compensation success sensitivity (PPS) is highly negatively linked to

corporate leveraging however because of the interaction among PPS including individual firms'

bankruptcy costs. The effect wherein the management' equity ratio as well as the percentage of

government stocks are associated greatly with the financial leverage. The research also shows what

the development, size, debt-free tax security and productivity of the group are major factors

determining the financial performance of listed companies in UK. It has shown that coded business

administrators are responsible for adjusting the amount of debt capital to self-interest. Legal

personal shares have a limiting influence on top executives' freedom to adapt their economic

position in compliance with their own purpose, albeit at a high degree. Where the top business

seems to have a significant level of equity, shareholdings of the legal individual often have a

significant role to play in supporting the self-interest of managers as well as the rights of other

shareholders (Daskalakis, Balios and Dalla, 2017). Group authorities are responsible for focusing on

financial performance. Capital value and composition of capital are relational partnerships that

affect each other. Many books have explored the effect on manager compensation of the capital

system. Theories and observational research were taken by researchers. In particular, there is a

strong connection between the financial structure and also the management salaries, which is driven

by excessive borrowing costs that raise the company's insolvency costs, which contributes to

unfavourable rewards for managers. These research support the assertion that perhaps the capital

system impacts executive pay by its effect on the cost of financial distress of intellectual resources.

From such an executive salaries effect on the organisational structure, it has been shown by Meng

Science that the organisation is controlled by the compensation packages and the corporate balance

sheet. The endogenously linked considerations are primarily the viability and business of the group.

Structure of governance and appropriate development risk assessment expertise. Executive pay even

has an effect on the capitalistic system where there is board protection.

In short, there really is no research on the effect of executive pay on the domestic capital system but

mostly on the influence of the employment structure mostly on compensation packages, although

the interaction among employee pay and capital structures is discussed in current domestic and

international language. Effect is primarily upon on cash balance impacts of management equity

holdings, particularly domestic research barely affects the financial performance by the manager pay

structure. When a leadership defence exists, the management which strives to optimise the resources

about its own prefers a more restrictive financial performance, in order to escape the possibility of

default of intellectual capital. Between executive pay standard and financial leverage there seems to

be a strong negative association (Detthamrong, Chancharat and Vithessonthi, 2017). The

organisation has a governance defensive conduct where the monitoring of shareholders is

challenging or unregulated. Reducing the composition of the capital, instead, raises the amount of its

own wages and maximises its very own interest. The administration of state-owned corporations

seems to have a higher level of defence, relative to private firms. The annual pay is relatively

constant and is an appraisal and acknowledgment of the efforts of senior management over the year.

The holder of equity is a long-term reward relative to the yearly salary, encouraging management to

give greater attention to that same stock valuation of the company. If senior managers' shareholder

ratios are reasonably large, their priorities can to a degree align with investor objectives. Focus on

long-term growth and business success of the organisation. The annual compensation ensures that

executives earned both annual salaries as well as the securities pay their commitment to the success

of the company over a certain period and the stock often prevents short-term actions at the cost of

the potential growth. The salaries of coted bank managements are essentially the annual

compensation and bonuses for shareholding. Through both the literature analysis, it can be observed

that the key variables are focused on business size, debt assured power, non-debt tax cover,

profitability, prospects for growth, etc. as academic journals the factors that influence the financial

performance. There really is no literary knowledge on the effect on national capital system of

executive pay, but more about the influence on employee pay of capital systems, while recent

national and international literature examines the impacts of corporate governance mostly on

stakeholders ’ perception. Particularly the domestic discourse rarely includes the effect of the

management equity system on capital structure, even on the discount rate (Devos, Rahman and

Tsang, 2017). As businesses expand, so many more real assets are accumulated. For outside persons

to provide worth better than intangible assets, measurable properties, such as land, plant and

machinery, including the acquisition's goodwill value, which minimise the estimated distress

has an effect on the capitalistic system where there is board protection.

In short, there really is no research on the effect of executive pay on the domestic capital system but

mostly on the influence of the employment structure mostly on compensation packages, although

the interaction among employee pay and capital structures is discussed in current domestic and

international language. Effect is primarily upon on cash balance impacts of management equity

holdings, particularly domestic research barely affects the financial performance by the manager pay

structure. When a leadership defence exists, the management which strives to optimise the resources

about its own prefers a more restrictive financial performance, in order to escape the possibility of

default of intellectual capital. Between executive pay standard and financial leverage there seems to

be a strong negative association (Detthamrong, Chancharat and Vithessonthi, 2017). The

organisation has a governance defensive conduct where the monitoring of shareholders is

challenging or unregulated. Reducing the composition of the capital, instead, raises the amount of its

own wages and maximises its very own interest. The administration of state-owned corporations

seems to have a higher level of defence, relative to private firms. The annual pay is relatively

constant and is an appraisal and acknowledgment of the efforts of senior management over the year.

The holder of equity is a long-term reward relative to the yearly salary, encouraging management to

give greater attention to that same stock valuation of the company. If senior managers' shareholder

ratios are reasonably large, their priorities can to a degree align with investor objectives. Focus on

long-term growth and business success of the organisation. The annual compensation ensures that

executives earned both annual salaries as well as the securities pay their commitment to the success

of the company over a certain period and the stock often prevents short-term actions at the cost of

the potential growth. The salaries of coted bank managements are essentially the annual

compensation and bonuses for shareholding. Through both the literature analysis, it can be observed

that the key variables are focused on business size, debt assured power, non-debt tax cover,

profitability, prospects for growth, etc. as academic journals the factors that influence the financial

performance. There really is no literary knowledge on the effect on national capital system of

executive pay, but more about the influence on employee pay of capital systems, while recent

national and international literature examines the impacts of corporate governance mostly on

stakeholders ’ perception. Particularly the domestic discourse rarely includes the effect of the

management equity system on capital structure, even on the discount rate (Devos, Rahman and

Tsang, 2017). As businesses expand, so many more real assets are accumulated. For outside persons

to provide worth better than intangible assets, measurable properties, such as land, plant and

machinery, including the acquisition's goodwill value, which minimise the estimated distress

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses. In addition, where a substantial majority of the company's assets is observable, assets can

act as leverage, minimising the likelihood that the lender will incur the financial risk of that same

Agency (like risk shifting). In liquidation, properties can still hold more value. The higher the

amount of real assets mostly on budget (fixed assets split by total assets). The borrowers need to be

more eager and the collateral must be more expensive to provide loans. Moreover, it is hard for

lenders to swap high risk assets with highly risky assets in terms of tangibility. A favourable

association among tangibility and equity is projected by lower estimated distress costs and less debt-

related organisation issues. Besides that, while lending from banking firms such concrete properties

may be guaranteed as leverage.

act as leverage, minimising the likelihood that the lender will incur the financial risk of that same

Agency (like risk shifting). In liquidation, properties can still hold more value. The higher the

amount of real assets mostly on budget (fixed assets split by total assets). The borrowers need to be

more eager and the collateral must be more expensive to provide loans. Moreover, it is hard for

lenders to swap high risk assets with highly risky assets in terms of tangibility. A favourable

association among tangibility and equity is projected by lower estimated distress costs and less debt-

related organisation issues. Besides that, while lending from banking firms such concrete properties

may be guaranteed as leverage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Methodology

In this research, secondary sources are used to collect the reliable data such as balance sheet, income

statement as well as cash flow statement (Di Pietro, Palacín Sánchez and Roldán, 2017). In order to

make research more effective and valuable some important other sources of information are also

used such as government journals, articles, academic books etc. which gives the clear understanding

about capital structure. For more authenticity about research researcher also implement the primary

sources of data collection in which 25 respondents from both companies were asked the same

questions which gives the results regarding their understanding about capital structure of Morrison’s

and Sainsbury.

Timeline.

Activity 1th

Wee

k

nd

2

Wee

k

rd

3

Wee

k

4th

Wee

k

th

5

Wee

k

6th

Wee

k

th

7

Wee

k

8th

Wee

k

th

9

Wee

k

th

10

Week

11t

h

W

ee

k

Selecting

the

research

topic

Literature

Review

Conducting

research

Methodolo

gy

Identified

factors

In this research, secondary sources are used to collect the reliable data such as balance sheet, income

statement as well as cash flow statement (Di Pietro, Palacín Sánchez and Roldán, 2017). In order to

make research more effective and valuable some important other sources of information are also

used such as government journals, articles, academic books etc. which gives the clear understanding

about capital structure. For more authenticity about research researcher also implement the primary

sources of data collection in which 25 respondents from both companies were asked the same

questions which gives the results regarding their understanding about capital structure of Morrison’s

and Sainsbury.

Timeline.

Activity 1th

Wee

k

nd

2

Wee

k

rd

3

Wee

k

4th

Wee

k

th

5

Wee

k

6th

Wee

k

th

7

Wee

k

8th

Wee

k

th

9

Wee

k

th

10

Week

11t

h

W

ee

k

Selecting

the

research

topic

Literature

Review

Conducting

research

Methodolo

gy

Identified

factors

Preparing

Questionna

ire

Facts and

data are

collected

Analysed

the

collected

data

Rechecked

the

information

before

submitting.

Submit the

report.

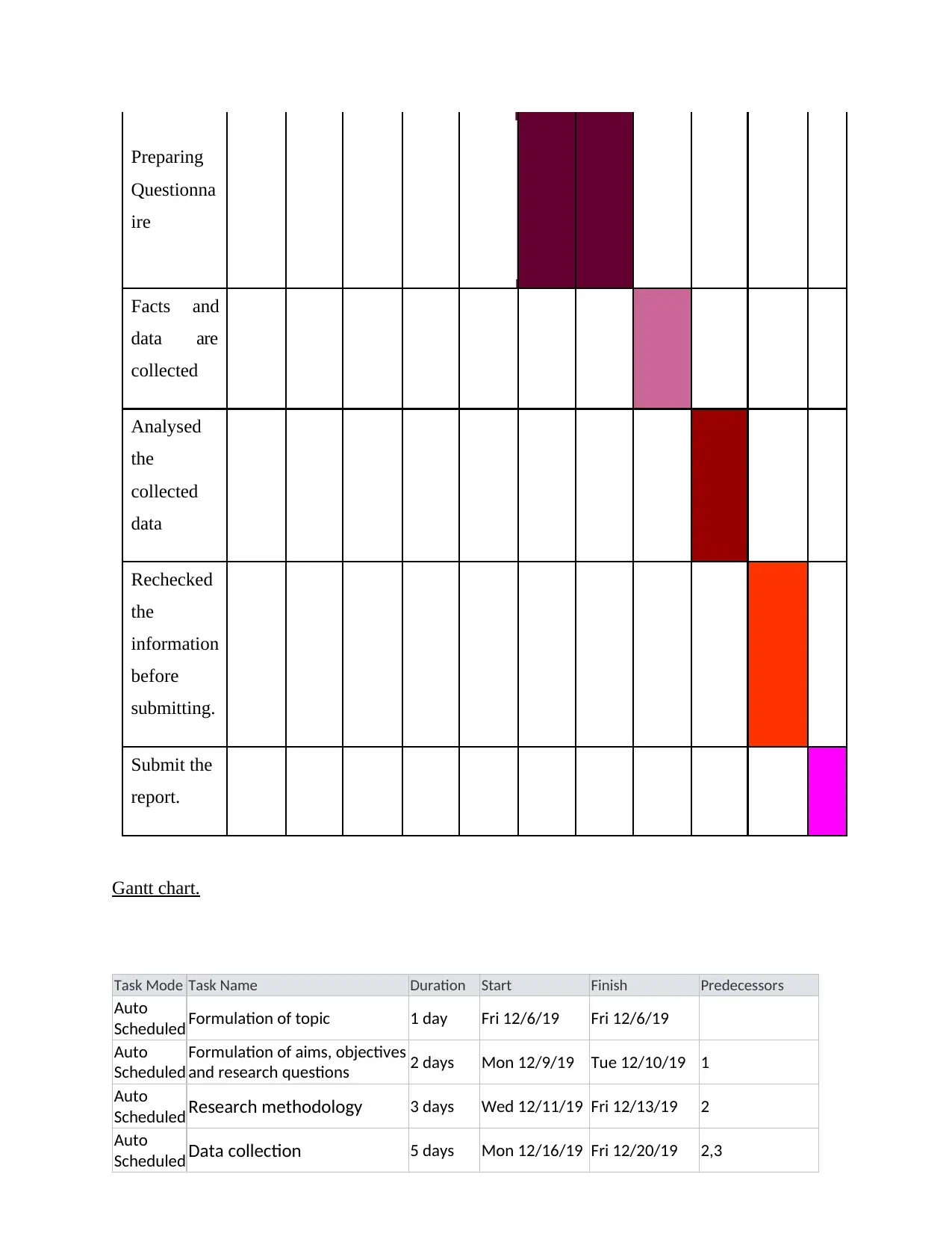

Gantt chart.

Task Mode Task Name Duration Start Finish Predecessors

Auto

Scheduled Formulation of topic 1 day Fri 12/6/19 Fri 12/6/19

Auto

Scheduled

Formulation of aims, objectives

and research questions 2 days Mon 12/9/19 Tue 12/10/19 1

Auto

Scheduled Research methodology 3 days Wed 12/11/19 Fri 12/13/19 2

Auto

Scheduled Data collection 5 days Mon 12/16/19 Fri 12/20/19 2,3

Questionna

ire

Facts and

data are

collected

Analysed

the

collected

data

Rechecked

the

information

before

submitting.

Submit the

report.

Gantt chart.

Task Mode Task Name Duration Start Finish Predecessors

Auto

Scheduled Formulation of topic 1 day Fri 12/6/19 Fri 12/6/19

Auto

Scheduled

Formulation of aims, objectives

and research questions 2 days Mon 12/9/19 Tue 12/10/19 1

Auto

Scheduled Research methodology 3 days Wed 12/11/19 Fri 12/13/19 2

Auto

Scheduled Data collection 5 days Mon 12/16/19 Fri 12/20/19 2,3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.