Financial Analysis: Angel Investor, Debt Financing, and Tax Impact

VerifiedAdded on 2023/05/29

|4

|855

|286

Case Study

AI Summary

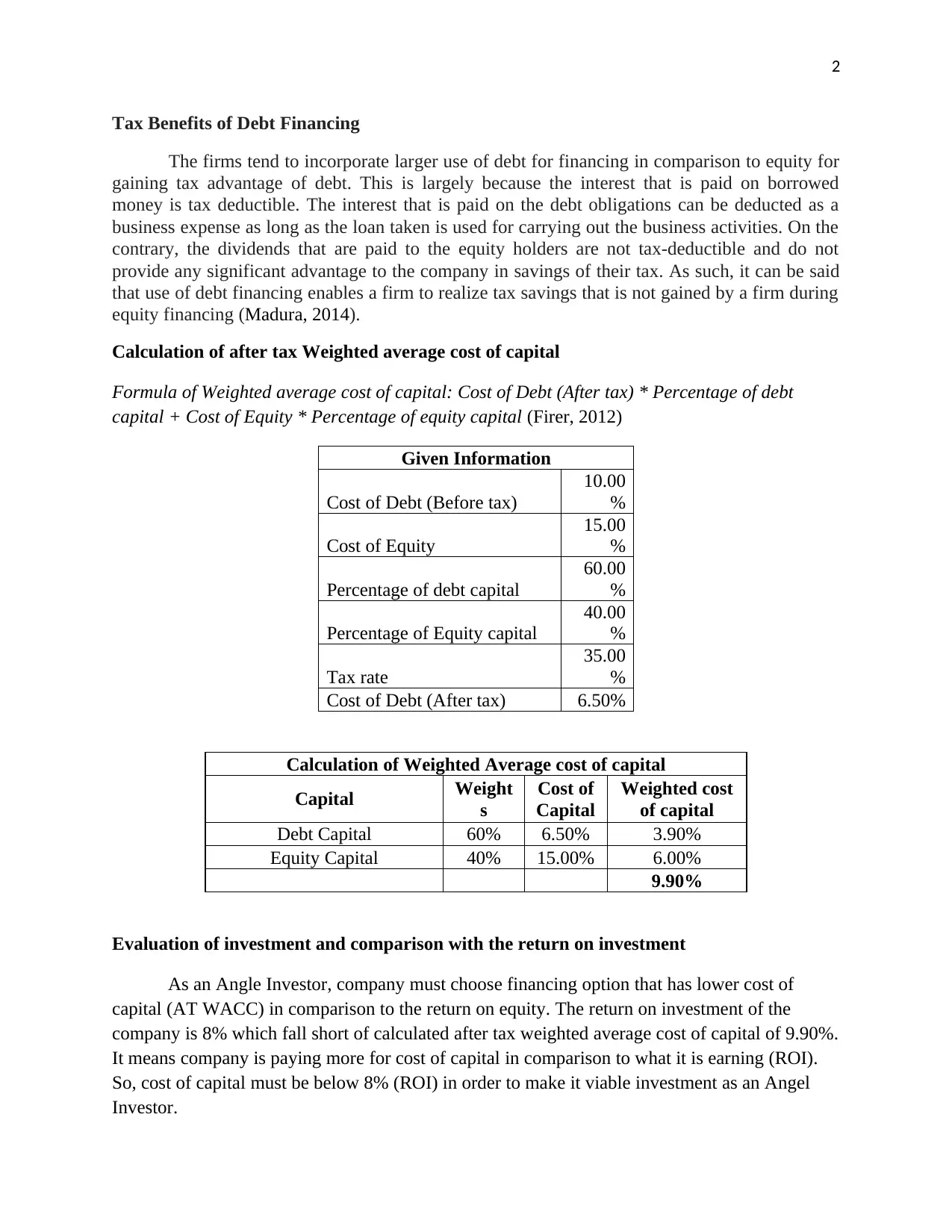

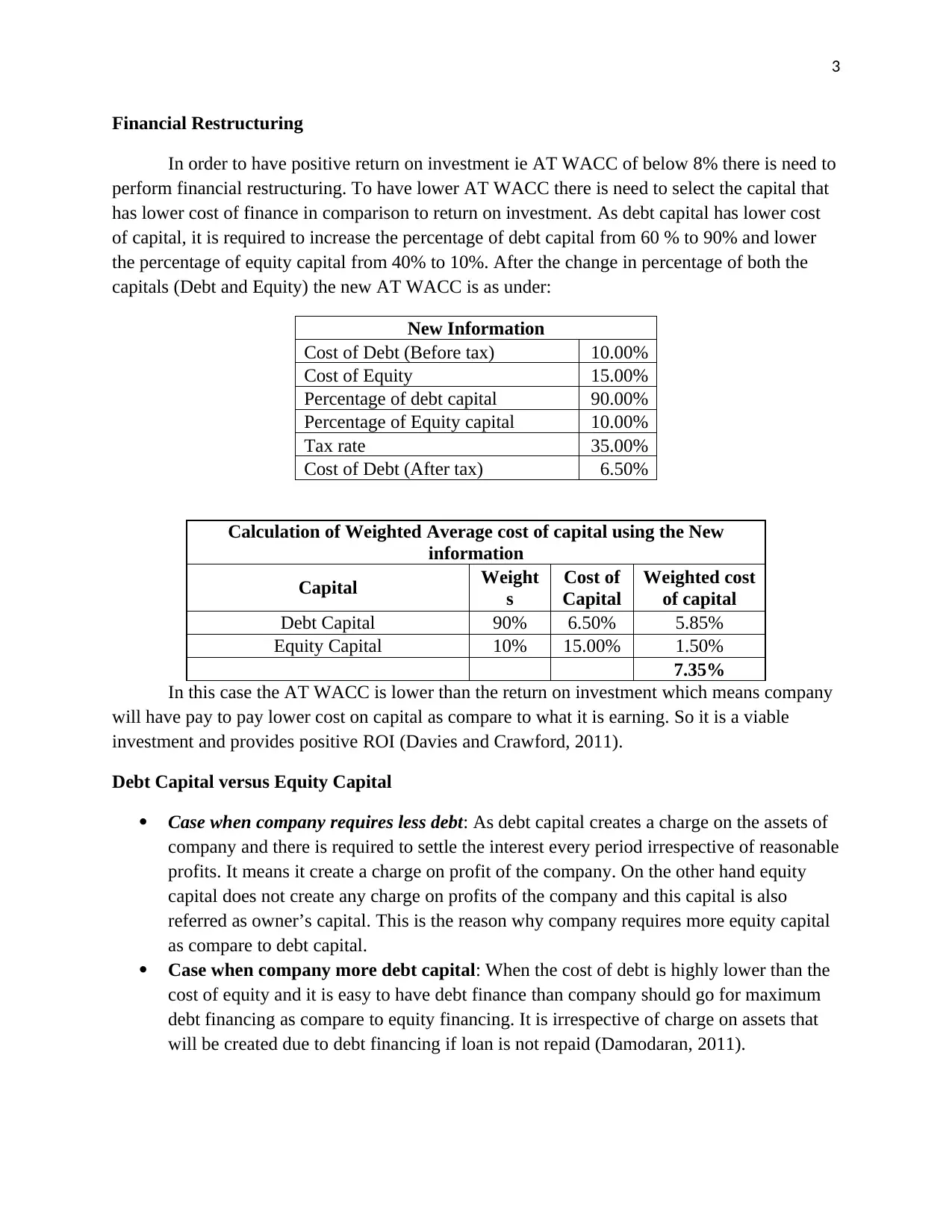

This case study analyzes the financial implications of debt financing for an angel investor, focusing on the tax benefits derived from using debt over equity. It includes a calculation of the after-tax weighted average cost of capital (WACC) and evaluates an investment's viability by comparing the return on investment (ROI) with the calculated WACC. The study finds that the initial ROI falls short of the WACC, necessitating financial restructuring to increase the proportion of debt capital and decrease the equity capital to achieve a positive ROI. The case further discusses the conditions under which a company should prefer debt over equity and vice versa, considering factors like cost of capital and the impact on the company's assets and profitability. Desklib provides similar solved assignments and past papers for students.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.