Auditing and Assurance Report: DecaSport Financial Statement Analysis

VerifiedAdded on 2023/01/19

|11

|2275

|79

Report

AI Summary

This report provides a detailed analysis of the auditing and assurance processes applied to DecaSport, a listed company producing luxury sport shoes. The report begins with an overview of the company and addresses threats to auditor independence as per APES110, along with potential safeguards. It then delves into risk assessment, differentiating between inherent and control risks and their potential impact on the financial statements. The report also includes an examination of DecaSport's internal controls and the identification of control weaknesses. Finally, it covers the calculation of planning materiality, using total assets as the base, and concludes with a summary of the audit process and its implications for financial decision-making by stakeholders. The report highlights the importance of independent audits in ensuring the accuracy and reliability of financial statements.

Running head: Auditing and Assurance

Auditing and Assurance

Name of the Student

Name of the University

Author Note

Auditing and Assurance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Auditing and Assurance

Executive Summary

The report includes details of the auditing process in the company. It show how the audit

help the company to analysis the financial statement of the company and give opinion in

regards with the true and fair view of the company. Lastly the report contain details of the

company internal control and inherent risk of the company and how the company can

overcome those risk it also contain the planning materiality of the company and also have the

calculation taking the total asset as the base for the calculation of the planning materiality.

Auditing and Assurance

Executive Summary

The report includes details of the auditing process in the company. It show how the audit

help the company to analysis the financial statement of the company and give opinion in

regards with the true and fair view of the company. Lastly the report contain details of the

company internal control and inherent risk of the company and how the company can

overcome those risk it also contain the planning materiality of the company and also have the

calculation taking the total asset as the base for the calculation of the planning materiality.

2

Auditing and Assurance

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Company.....................................................................................................3

Threats to auditor Independence as per APES110.................................................................3

Safeguard which can be taken to remove the threats.............................................................4

Risk Assessment – Inherent risk............................................................................................4

Risk Assessment – Control risk.............................................................................................6

Planning Materiality...............................................................................................................7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Auditing and Assurance

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Company.....................................................................................................3

Threats to auditor Independence as per APES110.................................................................3

Safeguard which can be taken to remove the threats.............................................................4

Risk Assessment – Inherent risk............................................................................................4

Risk Assessment – Control risk.............................................................................................6

Planning Materiality...............................................................................................................7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Auditing and Assurance

Introduction

Audit is the process in which the individual check the financial statement of the

company and then gives its opinion regarding whether the financial statements are showing

true and fair view or not (Abu Naser, Al Shobaki & Ammar 2017) . It is done so that the

financial user can know whether the financial statement which is been made by the company

is free from any material misstatement and the user can easily invest in the same . As the

public company involves huge amount of public cash so to overcome the loss of the public

money this procedure have been introduced as this show the real position of the company and

also help the investors and other financial users to take their economic decision in regards

with the finance position of the company (Agyei-Mensah 2016). The process of the audit is

been carried out by the individual termed as auditor and it is the one who carry the audit

process in the company and give its independent view upon the financial statement of the

company that whether the financial statement are showing true and fair view or not.

Discussion

Overview of the Company

The assignment is based upon the company named DecaSport. It is a listed company

in Australia. The products in which the company deals is sport shoes, it deals with all kind of

luxury and high-tech sport shoes. It current purchase its product from the suppliers of china

and sale it products in Australia and it do its business by having a low margin of profit.

Threats to auditor Independence as per APES110

Self-Interest threat – This threat signify the financial interest which the auditor have

with the company as it able to get a good amount of the money from the client so this can

affect the auditor independence as the auditor may found out that the by giving them correct

opinion can affect their financial relationship with the company and to stop that the auditor

Auditing and Assurance

Introduction

Audit is the process in which the individual check the financial statement of the

company and then gives its opinion regarding whether the financial statements are showing

true and fair view or not (Abu Naser, Al Shobaki & Ammar 2017) . It is done so that the

financial user can know whether the financial statement which is been made by the company

is free from any material misstatement and the user can easily invest in the same . As the

public company involves huge amount of public cash so to overcome the loss of the public

money this procedure have been introduced as this show the real position of the company and

also help the investors and other financial users to take their economic decision in regards

with the finance position of the company (Agyei-Mensah 2016). The process of the audit is

been carried out by the individual termed as auditor and it is the one who carry the audit

process in the company and give its independent view upon the financial statement of the

company that whether the financial statement are showing true and fair view or not.

Discussion

Overview of the Company

The assignment is based upon the company named DecaSport. It is a listed company

in Australia. The products in which the company deals is sport shoes, it deals with all kind of

luxury and high-tech sport shoes. It current purchase its product from the suppliers of china

and sale it products in Australia and it do its business by having a low margin of profit.

Threats to auditor Independence as per APES110

Self-Interest threat – This threat signify the financial interest which the auditor have

with the company as it able to get a good amount of the money from the client so this can

affect the auditor independence as the auditor may found out that the by giving them correct

opinion can affect their financial relationship with the company and to stop that the auditor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Auditing and Assurance

may give decision as per the company so that it can get the financial interest from the

company (Chen et al., 2014). In the given case it can be seen that the auditor also provides

many non-audit services to the company so they have a financial interest in the company so if

they did not give the report as per the client wish than they may lose the financial interest so

it can affect the auditor opinion in regards with the financial reporting of the company. So as

the auditor have the earning from the company by the non-audit service so this will directly

affect the auditor opinion and also it can happen that the auditor gives decision as per the

management which can affect the interest of the financial user who takes decision in regards

with the audited financial statements (De Simone, Ege & Stomberg 2014).

Safeguard which can be taken to remove the threats

The auditor can keep the work as per the professional requirement as it should

stay in the education training given by the profession and should develop it

requirement without changing its opinion as it should keep aside its financial

interest while doing the audit of the company as while doing the audit it should

stay as per the corporate governance and also with the professional standard so

that it can give a better view upon the financial statements (DeFond & Zhang

2014)

It should keep a distance from the management while providing the auditing

services and also should act in professional behaviour while doing the auditing

process so that it can manage the audit process more effectively and also should

stick to the work and should interact for some other services with the

management so this will help auditor to give an proper and correct opinion on the

financial statements (Donelson, Ege & McInnis 2016).

Auditing and Assurance

may give decision as per the company so that it can get the financial interest from the

company (Chen et al., 2014). In the given case it can be seen that the auditor also provides

many non-audit services to the company so they have a financial interest in the company so if

they did not give the report as per the client wish than they may lose the financial interest so

it can affect the auditor opinion in regards with the financial reporting of the company. So as

the auditor have the earning from the company by the non-audit service so this will directly

affect the auditor opinion and also it can happen that the auditor gives decision as per the

management which can affect the interest of the financial user who takes decision in regards

with the audited financial statements (De Simone, Ege & Stomberg 2014).

Safeguard which can be taken to remove the threats

The auditor can keep the work as per the professional requirement as it should

stay in the education training given by the profession and should develop it

requirement without changing its opinion as it should keep aside its financial

interest while doing the audit of the company as while doing the audit it should

stay as per the corporate governance and also with the professional standard so

that it can give a better view upon the financial statements (DeFond & Zhang

2014)

It should keep a distance from the management while providing the auditing

services and also should act in professional behaviour while doing the auditing

process so that it can manage the audit process more effectively and also should

stick to the work and should interact for some other services with the

management so this will help auditor to give an proper and correct opinion on the

financial statements (Donelson, Ege & McInnis 2016).

5

Auditing and Assurance

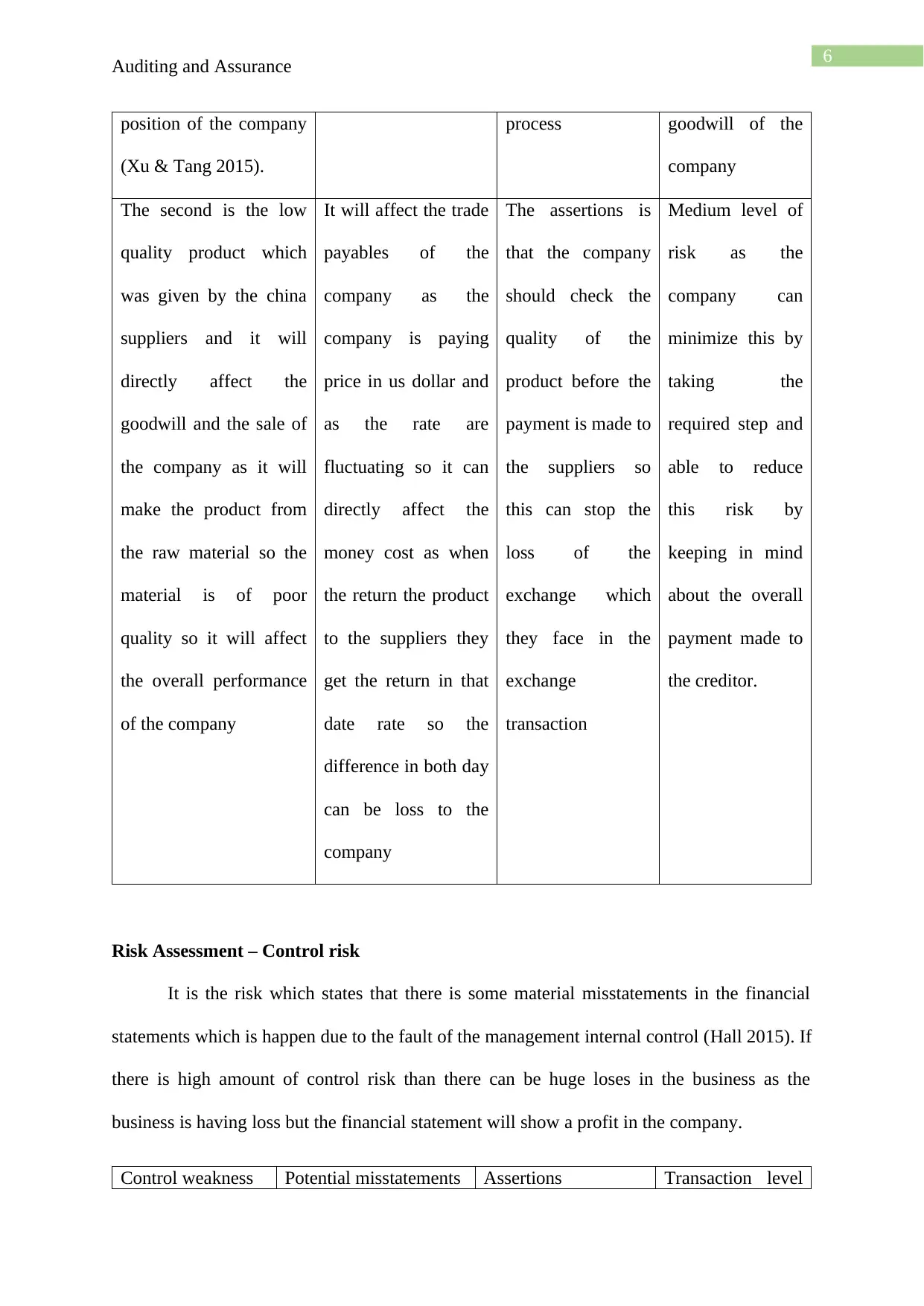

Risk Assessment – Inherent risk

Inherent risk are the risk which is found in the financial statements which is done by

the error of transaction which is out of the control of the management. This risk occurs in the

transaction which is very hard and require high level of professional judgement. This risk is

found higher when the company does not have a proper internal department regarding the

auditing of the internal control (Furnham & Gunter 2015). It also happen when there is

complex transaction so this make the value of inherent risk very high and it can affect in the

financial statements of the company and also misled the financial user who take decision in

regards of the financial statement of the company (Griffiths 2016). .

Potential risk –

Description

Account Assertions Level of Inherent

risk

Technical problem

which arise in the

product and due to these

many people are

returning back the

product so this can be

termed as inherent risk

as the company is

unable to control the

technical risk even if

they have a better

accounting and internal

control system so it can

affect the financial

It will affect the

turnover of the

company as if there

will be high return of

the goods so it will

decrease the turnover

of the company and

can also decrease the

overall profit of the

company.

The assertions

taken by the

auditor in regard

with the technical

problem is that it

should check the

technical process

more accurately

and also should

check the process

of that it can make

accurate problem

in the technical

It is very high as

it will decrease

the overall

revenue of the

company and also

it will decrease

the profit of the

company so it

will directly

affect the

financial position

of the company

and can also

affect the

Auditing and Assurance

Risk Assessment – Inherent risk

Inherent risk are the risk which is found in the financial statements which is done by

the error of transaction which is out of the control of the management. This risk occurs in the

transaction which is very hard and require high level of professional judgement. This risk is

found higher when the company does not have a proper internal department regarding the

auditing of the internal control (Furnham & Gunter 2015). It also happen when there is

complex transaction so this make the value of inherent risk very high and it can affect in the

financial statements of the company and also misled the financial user who take decision in

regards of the financial statement of the company (Griffiths 2016). .

Potential risk –

Description

Account Assertions Level of Inherent

risk

Technical problem

which arise in the

product and due to these

many people are

returning back the

product so this can be

termed as inherent risk

as the company is

unable to control the

technical risk even if

they have a better

accounting and internal

control system so it can

affect the financial

It will affect the

turnover of the

company as if there

will be high return of

the goods so it will

decrease the turnover

of the company and

can also decrease the

overall profit of the

company.

The assertions

taken by the

auditor in regard

with the technical

problem is that it

should check the

technical process

more accurately

and also should

check the process

of that it can make

accurate problem

in the technical

It is very high as

it will decrease

the overall

revenue of the

company and also

it will decrease

the profit of the

company so it

will directly

affect the

financial position

of the company

and can also

affect the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Auditing and Assurance

position of the company

(Xu & Tang 2015).

process goodwill of the

company

The second is the low

quality product which

was given by the china

suppliers and it will

directly affect the

goodwill and the sale of

the company as it will

make the product from

the raw material so the

material is of poor

quality so it will affect

the overall performance

of the company

It will affect the trade

payables of the

company as the

company is paying

price in us dollar and

as the rate are

fluctuating so it can

directly affect the

money cost as when

the return the product

to the suppliers they

get the return in that

date rate so the

difference in both day

can be loss to the

company

The assertions is

that the company

should check the

quality of the

product before the

payment is made to

the suppliers so

this can stop the

loss of the

exchange which

they face in the

exchange

transaction

Medium level of

risk as the

company can

minimize this by

taking the

required step and

able to reduce

this risk by

keeping in mind

about the overall

payment made to

the creditor.

Risk Assessment – Control risk

It is the risk which states that there is some material misstatements in the financial

statements which is happen due to the fault of the management internal control (Hall 2015). If

there is high amount of control risk than there can be huge loses in the business as the

business is having loss but the financial statement will show a profit in the company.

Control weakness Potential misstatements Assertions Transaction level

Auditing and Assurance

position of the company

(Xu & Tang 2015).

process goodwill of the

company

The second is the low

quality product which

was given by the china

suppliers and it will

directly affect the

goodwill and the sale of

the company as it will

make the product from

the raw material so the

material is of poor

quality so it will affect

the overall performance

of the company

It will affect the trade

payables of the

company as the

company is paying

price in us dollar and

as the rate are

fluctuating so it can

directly affect the

money cost as when

the return the product

to the suppliers they

get the return in that

date rate so the

difference in both day

can be loss to the

company

The assertions is

that the company

should check the

quality of the

product before the

payment is made to

the suppliers so

this can stop the

loss of the

exchange which

they face in the

exchange

transaction

Medium level of

risk as the

company can

minimize this by

taking the

required step and

able to reduce

this risk by

keeping in mind

about the overall

payment made to

the creditor.

Risk Assessment – Control risk

It is the risk which states that there is some material misstatements in the financial

statements which is happen due to the fault of the management internal control (Hall 2015). If

there is high amount of control risk than there can be huge loses in the business as the

business is having loss but the financial statement will show a profit in the company.

Control weakness Potential misstatements Assertions Transaction level

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

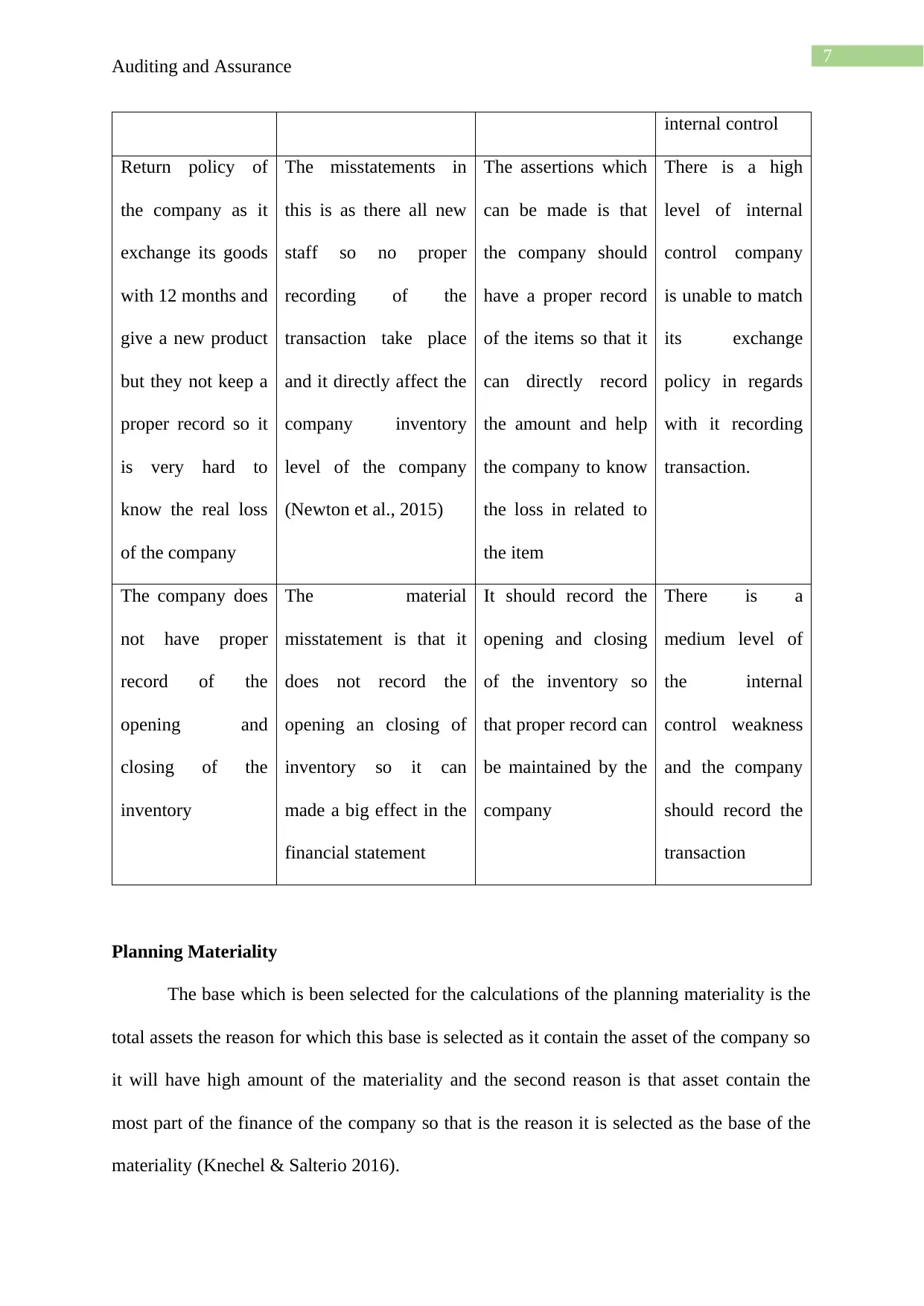

Auditing and Assurance

internal control

Return policy of

the company as it

exchange its goods

with 12 months and

give a new product

but they not keep a

proper record so it

is very hard to

know the real loss

of the company

The misstatements in

this is as there all new

staff so no proper

recording of the

transaction take place

and it directly affect the

company inventory

level of the company

(Newton et al., 2015)

The assertions which

can be made is that

the company should

have a proper record

of the items so that it

can directly record

the amount and help

the company to know

the loss in related to

the item

There is a high

level of internal

control company

is unable to match

its exchange

policy in regards

with it recording

transaction.

The company does

not have proper

record of the

opening and

closing of the

inventory

The material

misstatement is that it

does not record the

opening an closing of

inventory so it can

made a big effect in the

financial statement

It should record the

opening and closing

of the inventory so

that proper record can

be maintained by the

company

There is a

medium level of

the internal

control weakness

and the company

should record the

transaction

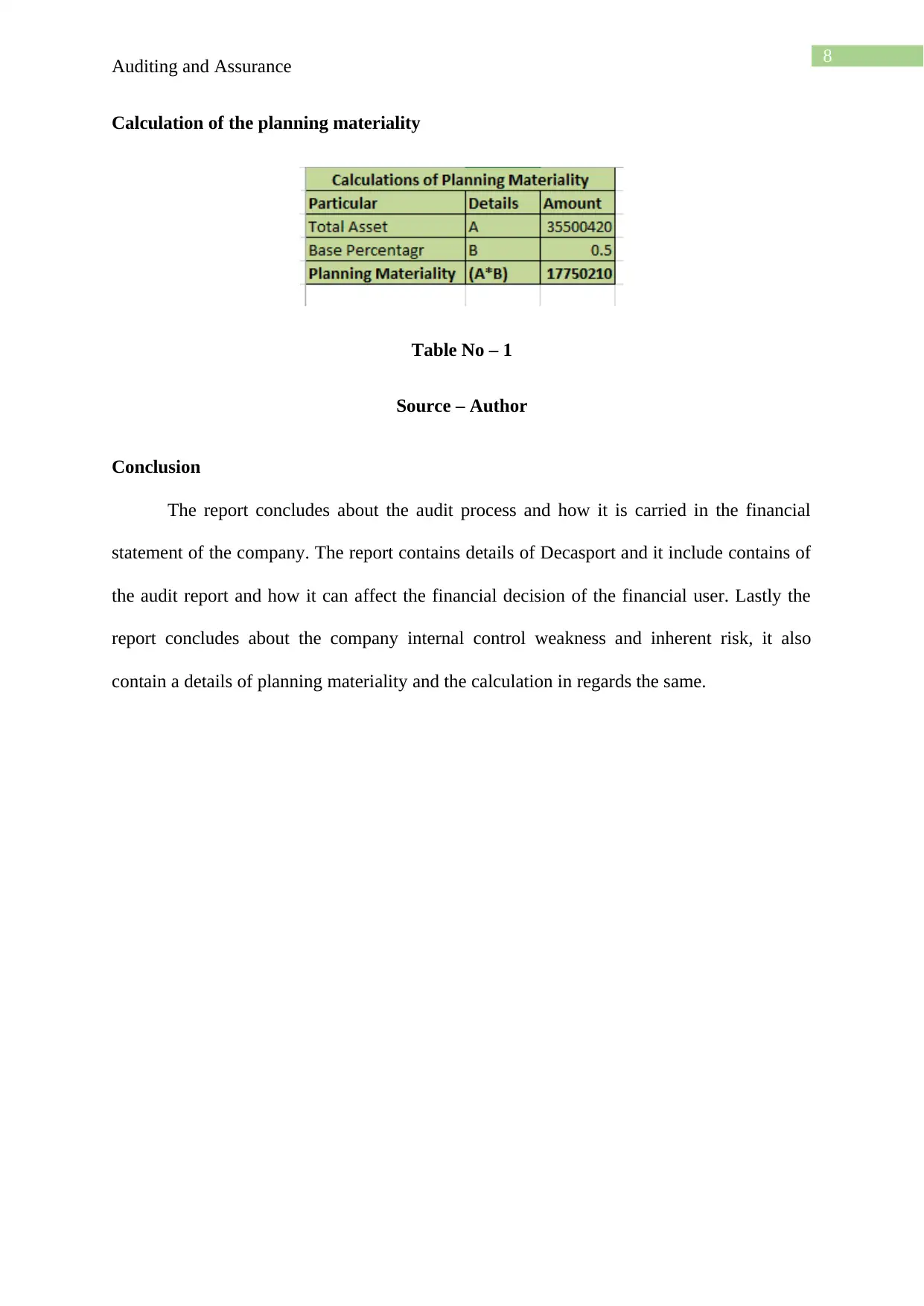

Planning Materiality

The base which is been selected for the calculations of the planning materiality is the

total assets the reason for which this base is selected as it contain the asset of the company so

it will have high amount of the materiality and the second reason is that asset contain the

most part of the finance of the company so that is the reason it is selected as the base of the

materiality (Knechel & Salterio 2016).

Auditing and Assurance

internal control

Return policy of

the company as it

exchange its goods

with 12 months and

give a new product

but they not keep a

proper record so it

is very hard to

know the real loss

of the company

The misstatements in

this is as there all new

staff so no proper

recording of the

transaction take place

and it directly affect the

company inventory

level of the company

(Newton et al., 2015)

The assertions which

can be made is that

the company should

have a proper record

of the items so that it

can directly record

the amount and help

the company to know

the loss in related to

the item

There is a high

level of internal

control company

is unable to match

its exchange

policy in regards

with it recording

transaction.

The company does

not have proper

record of the

opening and

closing of the

inventory

The material

misstatement is that it

does not record the

opening an closing of

inventory so it can

made a big effect in the

financial statement

It should record the

opening and closing

of the inventory so

that proper record can

be maintained by the

company

There is a

medium level of

the internal

control weakness

and the company

should record the

transaction

Planning Materiality

The base which is been selected for the calculations of the planning materiality is the

total assets the reason for which this base is selected as it contain the asset of the company so

it will have high amount of the materiality and the second reason is that asset contain the

most part of the finance of the company so that is the reason it is selected as the base of the

materiality (Knechel & Salterio 2016).

8

Auditing and Assurance

Calculation of the planning materiality

Table No – 1

Source – Author

Conclusion

The report concludes about the audit process and how it is carried in the financial

statement of the company. The report contains details of Decasport and it include contains of

the audit report and how it can affect the financial decision of the financial user. Lastly the

report concludes about the company internal control weakness and inherent risk, it also

contain a details of planning materiality and the calculation in regards the same.

Auditing and Assurance

Calculation of the planning materiality

Table No – 1

Source – Author

Conclusion

The report concludes about the audit process and how it is carried in the financial

statement of the company. The report contains details of Decasport and it include contains of

the audit report and how it can affect the financial decision of the financial user. Lastly the

report concludes about the company internal control weakness and inherent risk, it also

contain a details of planning materiality and the calculation in regards the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Auditing and Assurance

References

Abu Naser, S. S., Al Shobaki, M. J., & Ammar, T. M. (2017). Impact of Communication and

Information on the Internal Control Environment in Palestinian

Universities. Available at SSRN 3085429.

Agyei-Mensah, B. K. (2016). Internal control information disclosure and corporate

governance: evidence from an emerging market. Corporate Governance: The

international journal of business in society, 16(1), 79-95.

Chen, Y., Smith, A. L., Cao, J., & Xia, W. (2014). Information technology capability, internal

control effectiveness, and audit fees and delays. Journal of Information

Systems, 28(2), 149-180.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), 45-69.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Auditing and Assurance

References

Abu Naser, S. S., Al Shobaki, M. J., & Ammar, T. M. (2017). Impact of Communication and

Information on the Internal Control Environment in Palestinian

Universities. Available at SSRN 3085429.

Agyei-Mensah, B. K. (2016). Internal control information disclosure and corporate

governance: evidence from an emerging market. Corporate Governance: The

international journal of business in society, 16(1), 79-95.

Chen, Y., Smith, A. L., Cao, J., & Xia, W. (2014). Information technology capability, internal

control effectiveness, and audit fees and delays. Journal of Information

Systems, 28(2), 149-180.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), 45-69.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Auditing and Assurance

Newton, N. J., Persellin, J. S., Wang, D., & Wilkins, M. S. (2015). Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), 603-623.

Xu, L., & Tang, A. P. (2015). Internal control material weakness, analysts accuracy and bias,

and brokerage reputation. Handbook of Financial Econometrics and Statistics, 1719-

1751.

Auditing and Assurance

Newton, N. J., Persellin, J. S., Wang, D., & Wilkins, M. S. (2015). Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), 603-623.

Xu, L., & Tang, A. P. (2015). Internal control material weakness, analysts accuracy and bias,

and brokerage reputation. Handbook of Financial Econometrics and Statistics, 1719-

1751.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.