DecaSport Project: Financial Analysis, Capital Structure, and WACC

VerifiedAdded on 2023/04/23

|18

|3830

|62

Report

AI Summary

This report presents a comprehensive financial analysis of DecaSport's new sport shoe project, evaluating its financial viability through various metrics. The analysis includes the calculation of Net Present Value (NPV), payback period, and profitability index under base, best-case, and worst-case scenarios. It also examines the company's capital structure, focusing on the weighted average cost of capital (WACC) and comparing it with a competitor, Common Wealth Bank. The report further discusses different payment options for the new production machines, recommending the quarterly payment option based on the lowest net payment. Additionally, it assesses ANZ Bank's capital structure, financial performance, and liquidity position, highlighting improvements in profitability and liquidity coverage.

Assessment 3

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

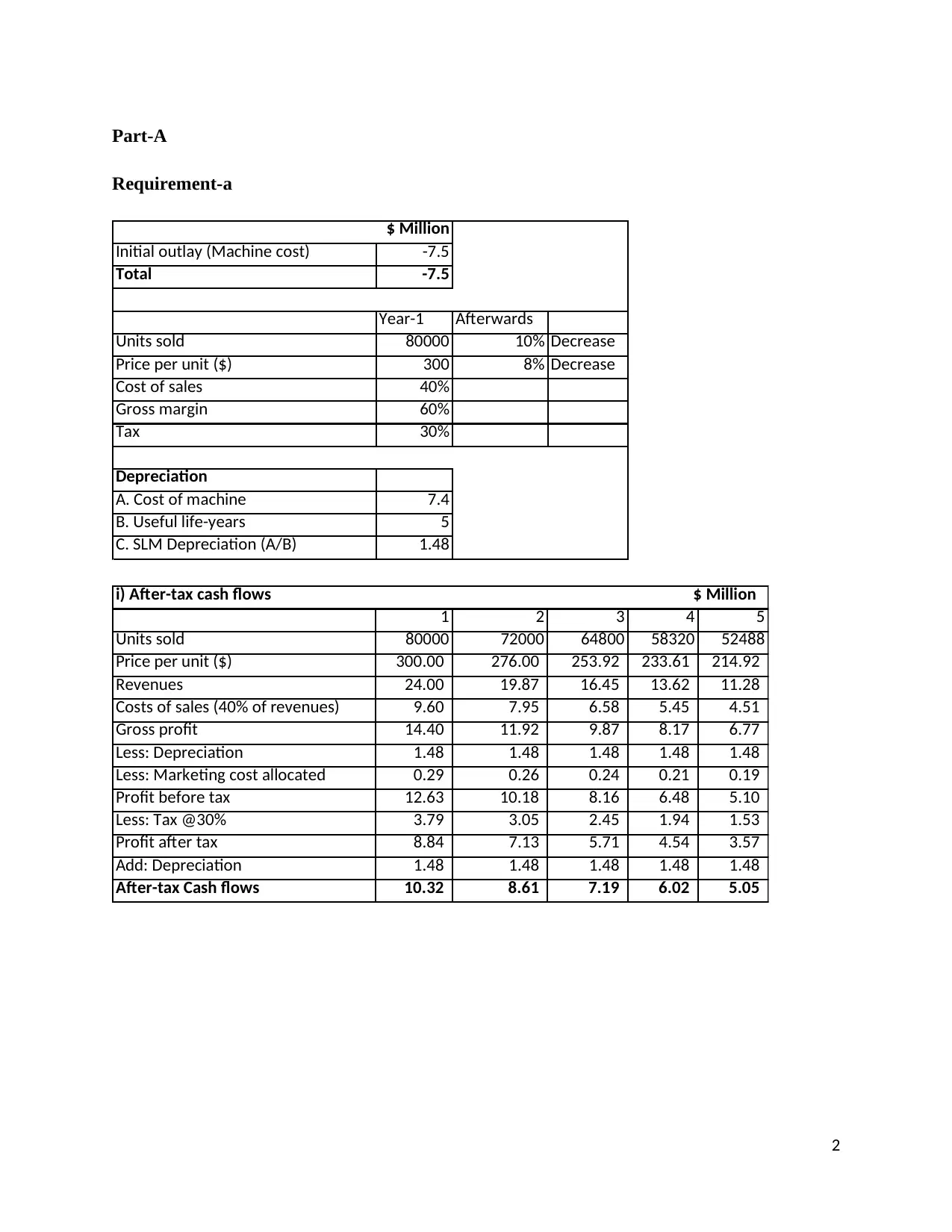

Part-A

Requirement-a

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Year-1 Afterwards

Units sold 80000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 80000 72000 64800 58320 52488

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 24.00 19.87 16.45 13.62 11.28

Costs of sales (40% of revenues) 9.60 7.95 6.58 5.45 4.51

Gross profit 14.40 11.92 9.87 8.17 6.77

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Marketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 12.63 10.18 8.16 6.48 5.10

Less: Tax @30% 3.79 3.05 2.45 1.94 1.53

Profit after tax 8.84 7.13 5.71 4.54 3.57

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 10.32 8.61 7.19 6.02 5.05

i) After-tax cash flows $ Million

2

Requirement-a

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Year-1 Afterwards

Units sold 80000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 80000 72000 64800 58320 52488

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 24.00 19.87 16.45 13.62 11.28

Costs of sales (40% of revenues) 9.60 7.95 6.58 5.45 4.51

Gross profit 14.40 11.92 9.87 8.17 6.77

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Marketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 12.63 10.18 8.16 6.48 5.10

Less: Tax @30% 3.79 3.05 2.45 1.94 1.53

Profit after tax 8.84 7.13 5.71 4.54 3.57

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 10.32 8.61 7.19 6.02 5.05

i) After-tax cash flows $ Million

2

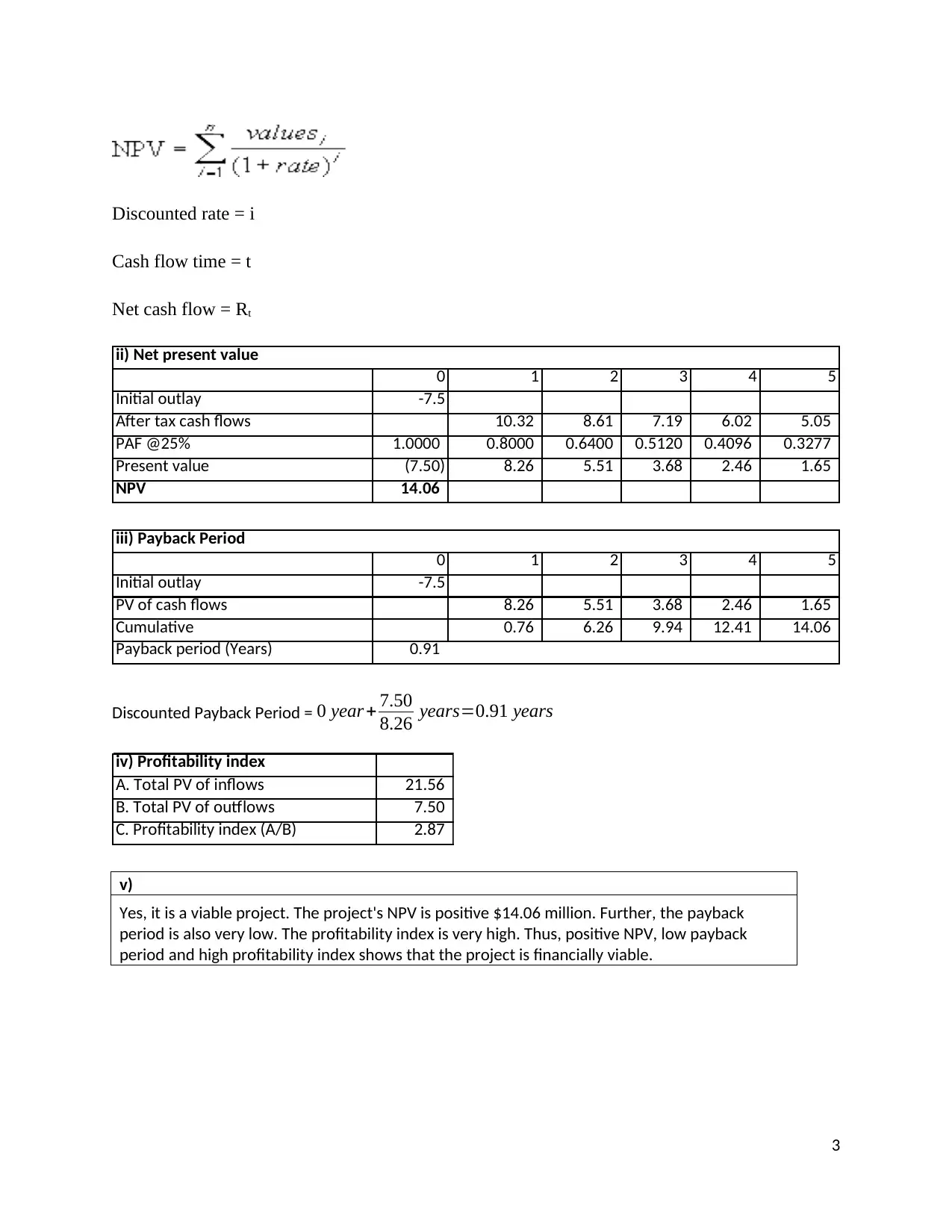

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 10.32 8.61 7.19 6.02 5.05

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 8.26 5.51 3.68 2.46 1.65

NPV 14.06

ii) Net present value

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 8.26 5.51 3.68 2.46 1.65

Cumulative 0.76 6.26 9.94 12.41 14.06

Payback period (Years) 0.91

iii) Payback Period

Discounted Payback Period = 0 year+ 7.50

8.26 years=0.91 years

iv) Profitability index

A. Total PV of inflows 21.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.87

v)

Yes, it is a viable project. The project's NPV is positive $14.06 million. Further, the payback

period is also very low. The profitability index is very high. Thus, positive NPV, low payback

period and high profitability index shows that the project is financially viable.

3

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 10.32 8.61 7.19 6.02 5.05

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 8.26 5.51 3.68 2.46 1.65

NPV 14.06

ii) Net present value

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 8.26 5.51 3.68 2.46 1.65

Cumulative 0.76 6.26 9.94 12.41 14.06

Payback period (Years) 0.91

iii) Payback Period

Discounted Payback Period = 0 year+ 7.50

8.26 years=0.91 years

iv) Profitability index

A. Total PV of inflows 21.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.87

v)

Yes, it is a viable project. The project's NPV is positive $14.06 million. Further, the payback

period is also very low. The profitability index is very high. Thus, positive NPV, low payback

period and high profitability index shows that the project is financially viable.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

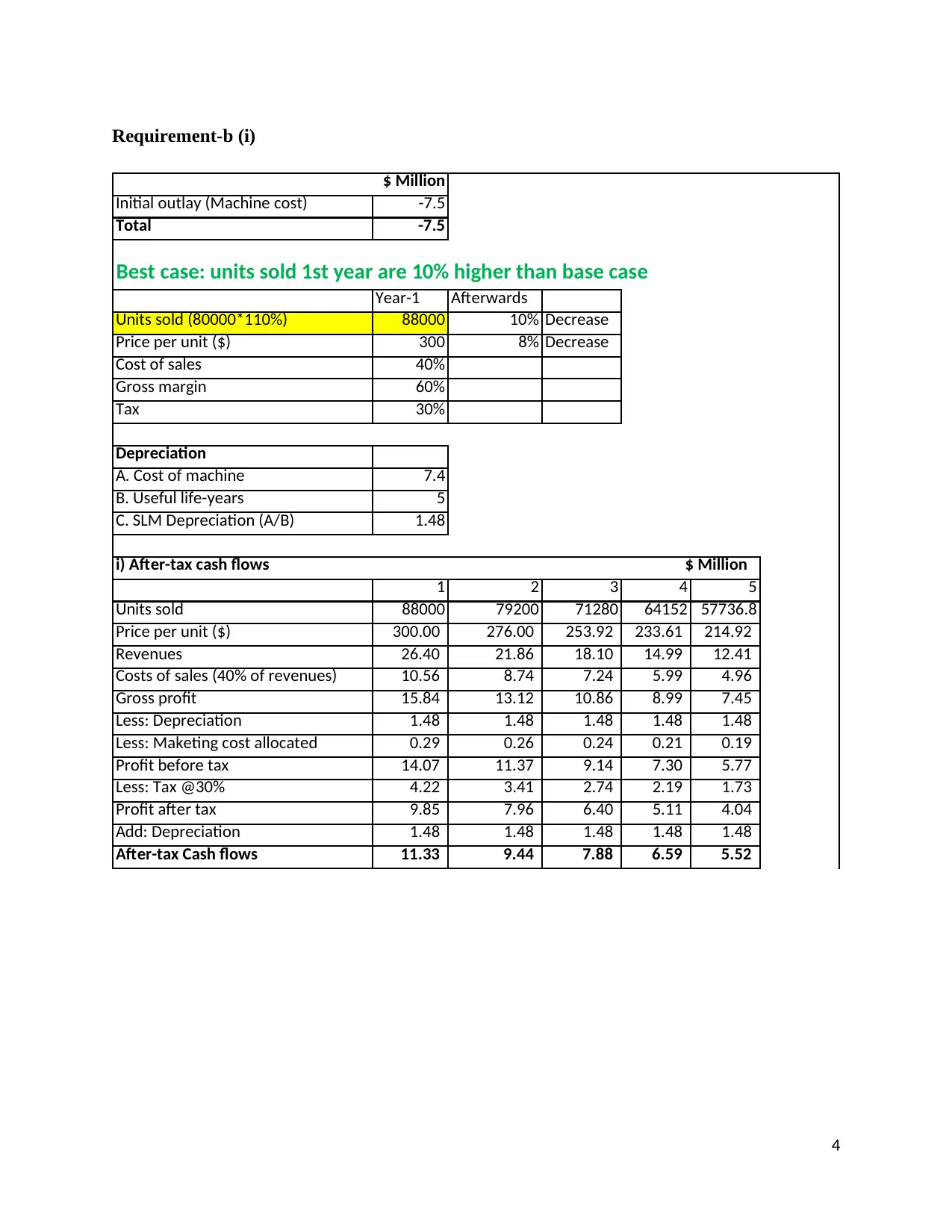

Requirement-b (i)

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Best case: units sold 1st year are 10% higher than base case

Year-1 Afterwards

Units sold (80000*110%) 88000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 88000 79200 71280 64152 57736.8

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 26.40 21.86 18.10 14.99 12.41

Costs of sales (40% of revenues) 10.56 8.74 7.24 5.99 4.96

Gross profit 15.84 13.12 10.86 8.99 7.45

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 14.07 11.37 9.14 7.30 5.77

Less: Tax @30% 4.22 3.41 2.74 2.19 1.73

Profit after tax 9.85 7.96 6.40 5.11 4.04

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 11.33 9.44 7.88 6.59 5.52

i) After-tax cash flows $ Million

4

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Best case: units sold 1st year are 10% higher than base case

Year-1 Afterwards

Units sold (80000*110%) 88000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 88000 79200 71280 64152 57736.8

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 26.40 21.86 18.10 14.99 12.41

Costs of sales (40% of revenues) 10.56 8.74 7.24 5.99 4.96

Gross profit 15.84 13.12 10.86 8.99 7.45

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.29 0.26 0.24 0.21 0.19

Profit before tax 14.07 11.37 9.14 7.30 5.77

Less: Tax @30% 4.22 3.41 2.74 2.19 1.73

Profit after tax 9.85 7.96 6.40 5.11 4.04

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 11.33 9.44 7.88 6.59 5.52

i) After-tax cash flows $ Million

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

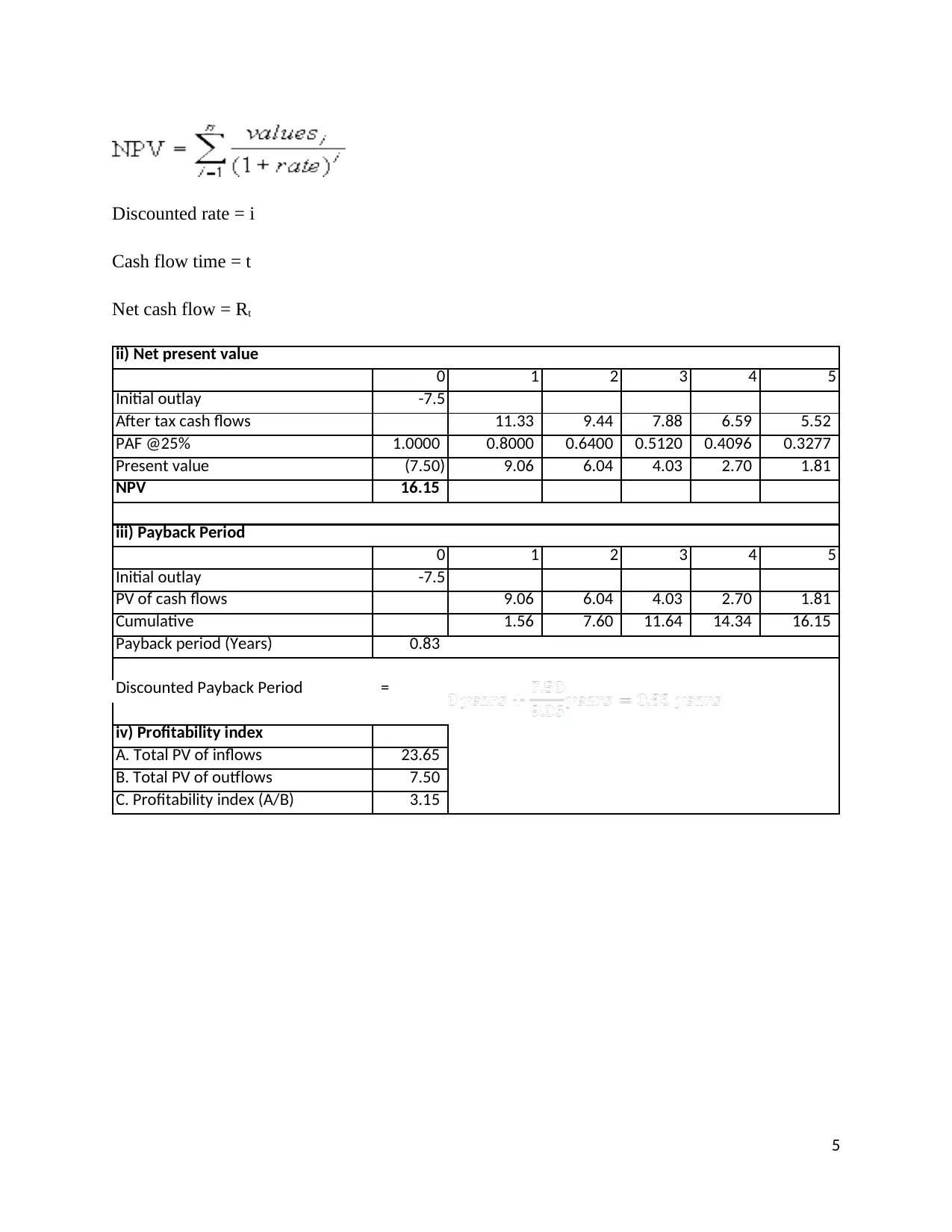

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 11.33 9.44 7.88 6.59 5.52

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 9.06 6.04 4.03 2.70 1.81

NPV 16.15

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 9.06 6.04 4.03 2.70 1.81

Cumulative 1.56 7.60 11.64 14.34 16.15

Payback period (Years) 0.83

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 23.65

B. Total PV of outflows 7.50

C. Profitability index (A/B) 3.15

ii) Net present value

iii) Payback Period

5

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 11.33 9.44 7.88 6.59 5.52

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 9.06 6.04 4.03 2.70 1.81

NPV 16.15

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 9.06 6.04 4.03 2.70 1.81

Cumulative 1.56 7.60 11.64 14.34 16.15

Payback period (Years) 0.83

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 23.65

B. Total PV of outflows 7.50

C. Profitability index (A/B) 3.15

ii) Net present value

iii) Payback Period

5

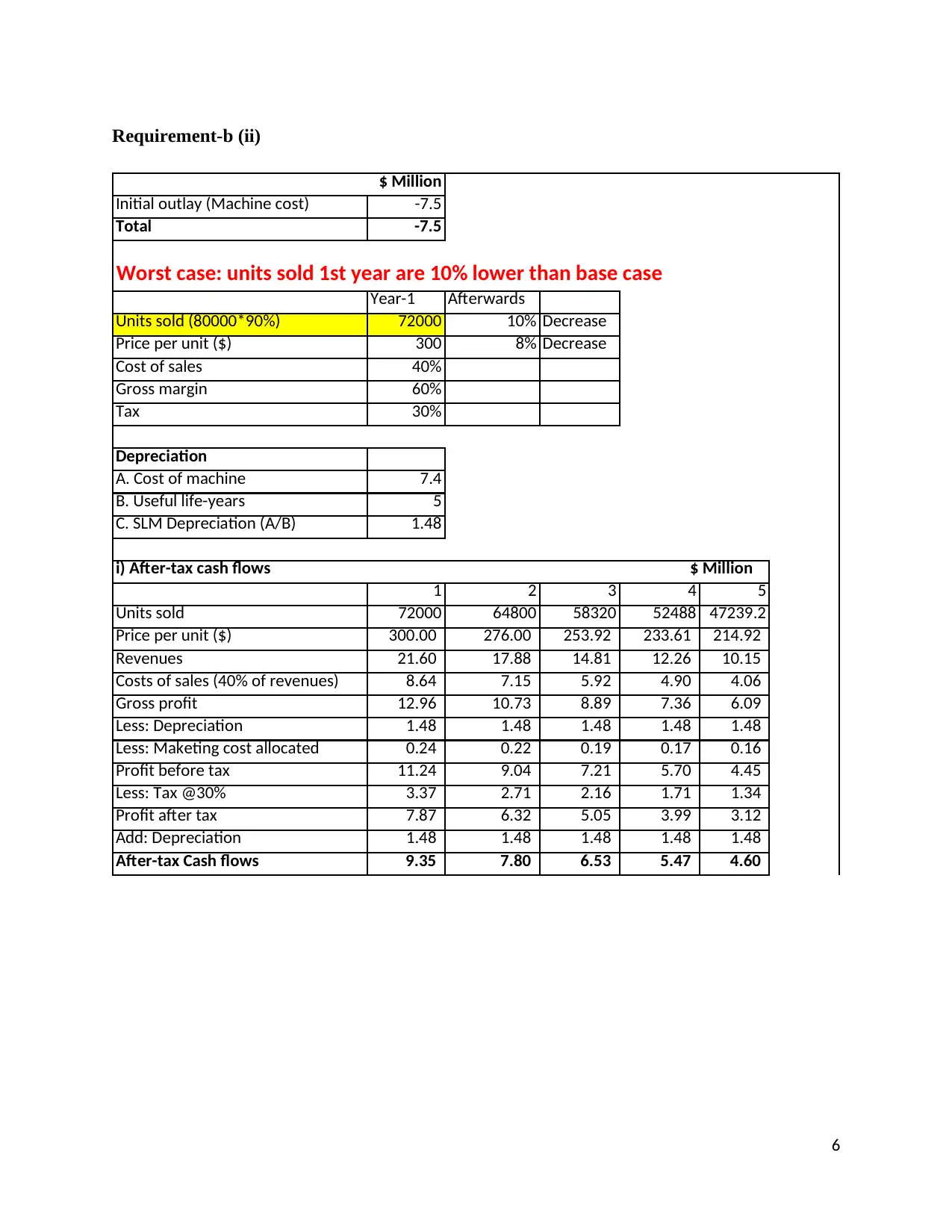

Requirement-b (ii)

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Worst case: units sold 1st year are 10% lower than base case

Year-1 Afterwards

Units sold (80000*90%) 72000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 72000 64800 58320 52488 47239.2

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 21.60 17.88 14.81 12.26 10.15

Costs of sales (40% of revenues) 8.64 7.15 5.92 4.90 4.06

Gross profit 12.96 10.73 8.89 7.36 6.09

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.24 0.22 0.19 0.17 0.16

Profit before tax 11.24 9.04 7.21 5.70 4.45

Less: Tax @30% 3.37 2.71 2.16 1.71 1.34

Profit after tax 7.87 6.32 5.05 3.99 3.12

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 9.35 7.80 6.53 5.47 4.60

i) After-tax cash flows $ Million

6

$ Million

Initial outlay (Machine cost) -7.5

Total -7.5

Worst case: units sold 1st year are 10% lower than base case

Year-1 Afterwards

Units sold (80000*90%) 72000 10% Decrease

Price per unit ($) 300 8% Decrease

Cost of sales 40%

Gross margin 60%

Tax 30%

Depreciation

A. Cost of machine 7.4

B. Useful life-years 5

C. SLM Depreciation (A/B) 1.48

1 2 3 4 5

Units sold 72000 64800 58320 52488 47239.2

Price per unit ($) 300.00 276.00 253.92 233.61 214.92

Revenues 21.60 17.88 14.81 12.26 10.15

Costs of sales (40% of revenues) 8.64 7.15 5.92 4.90 4.06

Gross profit 12.96 10.73 8.89 7.36 6.09

Less: Depreciation 1.48 1.48 1.48 1.48 1.48

Less: Maketing cost allocated 0.24 0.22 0.19 0.17 0.16

Profit before tax 11.24 9.04 7.21 5.70 4.45

Less: Tax @30% 3.37 2.71 2.16 1.71 1.34

Profit after tax 7.87 6.32 5.05 3.99 3.12

Add: Depreciation 1.48 1.48 1.48 1.48 1.48

After-tax Cash flows 9.35 7.80 6.53 5.47 4.60

i) After-tax cash flows $ Million

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

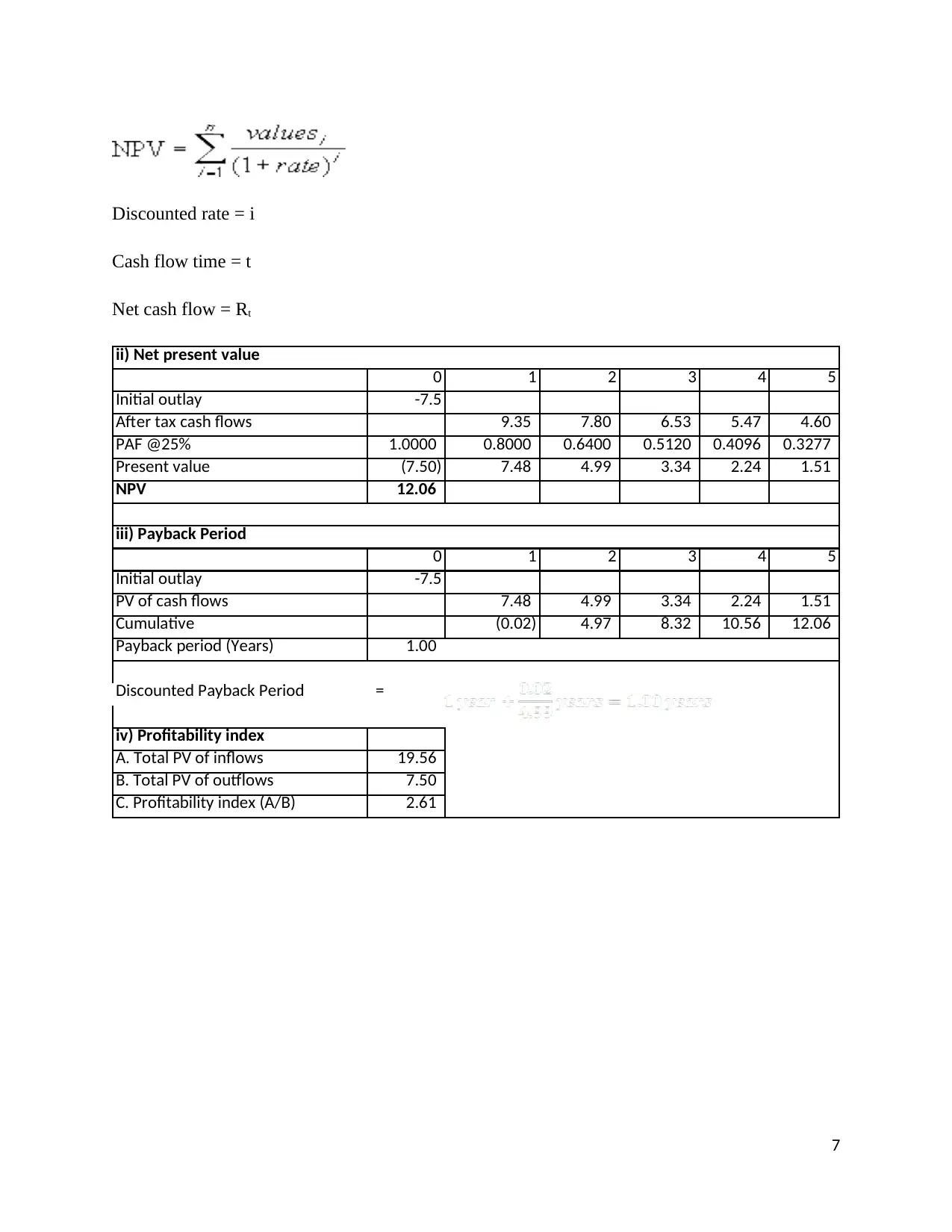

Discounted rate = i

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 9.35 7.80 6.53 5.47 4.60

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 7.48 4.99 3.34 2.24 1.51

NPV 12.06

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 7.48 4.99 3.34 2.24 1.51

Cumulative (0.02) 4.97 8.32 10.56 12.06

Payback period (Years) 1.00

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 19.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.61

ii) Net present value

iii) Payback Period

7

Cash flow time = t

Net cash flow = Rt

0 1 2 3 4 5

Initial outlay -7.5

After tax cash flows 9.35 7.80 6.53 5.47 4.60

PAF @25% 1.0000 0.8000 0.6400 0.5120 0.4096 0.3277

Present value (7.50) 7.48 4.99 3.34 2.24 1.51

NPV 12.06

0 1 2 3 4 5

Initial outlay -7.5

PV of cash flows 7.48 4.99 3.34 2.24 1.51

Cumulative (0.02) 4.97 8.32 10.56 12.06

Payback period (Years) 1.00

Discounted Payback Period =

iv) Profitability index

A. Total PV of inflows 19.56

B. Total PV of outflows 7.50

C. Profitability index (A/B) 2.61

ii) Net present value

iii) Payback Period

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part-A (b) (iii)

Under the best case scenario, the NPV of the project increases from $14.06 million to $16.15 million.

The increased sales increase the after tax cash flows which causes increase in the NPV. Further, due to

increase in the after tax cash flows, the payback period reduces from 0.91 years to 0.83 year. The

profitability index is also improved from 2.86 times to 3.15 times. Under the worst case scenario, the

after tax cash flows reduces which reduction in the NPV to $12.06 million. The payback period

increases a little reaching to 1 year and profitability index shrinks to 2.61 times.

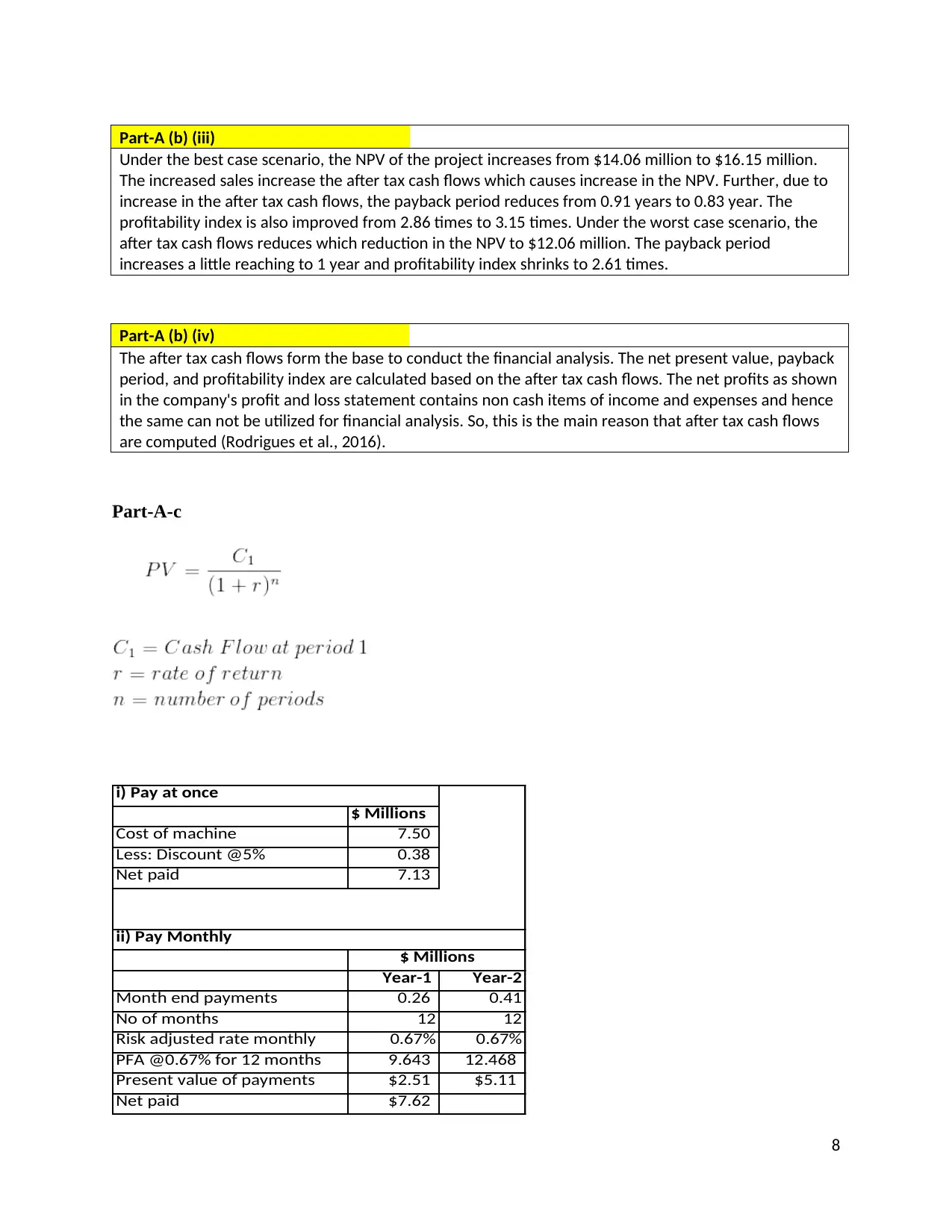

Part-A (b) (iv)

The after tax cash flows form the base to conduct the financial analysis. The net present value, payback

period, and profitability index are calculated based on the after tax cash flows. The net profits as shown

in the company's profit and loss statement contains non cash items of income and expenses and hence

the same can not be utilized for financial analysis. So, this is the main reason that after tax cash flows

are computed (Rodrigues et al., 2016).

Part-A-c

$ Millions

Cost of machine 7.50

Less: Discount @5% 0.38

Net paid 7.13

Year-1 Year-2

Month end payments 0.26 0.41

No of months 12 12

Risk adjusted rate monthly 0.67% 0.67%

PFA @0.67% for 12 months 9.643 12.468

Present value of payments $2.51 $5.11

Net paid $7.62

i) Pay at once

$ Millions

ii) Pay Monthly

8

Under the best case scenario, the NPV of the project increases from $14.06 million to $16.15 million.

The increased sales increase the after tax cash flows which causes increase in the NPV. Further, due to

increase in the after tax cash flows, the payback period reduces from 0.91 years to 0.83 year. The

profitability index is also improved from 2.86 times to 3.15 times. Under the worst case scenario, the

after tax cash flows reduces which reduction in the NPV to $12.06 million. The payback period

increases a little reaching to 1 year and profitability index shrinks to 2.61 times.

Part-A (b) (iv)

The after tax cash flows form the base to conduct the financial analysis. The net present value, payback

period, and profitability index are calculated based on the after tax cash flows. The net profits as shown

in the company's profit and loss statement contains non cash items of income and expenses and hence

the same can not be utilized for financial analysis. So, this is the main reason that after tax cash flows

are computed (Rodrigues et al., 2016).

Part-A-c

$ Millions

Cost of machine 7.50

Less: Discount @5% 0.38

Net paid 7.13

Year-1 Year-2

Month end payments 0.26 0.41

No of months 12 12

Risk adjusted rate monthly 0.67% 0.67%

PFA @0.67% for 12 months 9.643 12.468

Present value of payments $2.51 $5.11

Net paid $7.62

i) Pay at once

$ Millions

ii) Pay Monthly

8

Year-1: $ 0.26 million∗PVF @ 0.67 % for 12 periods ¿ 1 st ¿ 12th=$ 0.26∗9.643=$ 2.51 million

Year-2:

$ 0.41 million∗PVF @ 0.67 % for 12 periods ¿ 11th ¿ 24 th=$ 0.41∗12.468=$ 5.11 million

iii) Pay Quarterly

$ Millions

Quarter end payments 0.67

No of quarters 12

Risk adjusted rate quarterly 2.00%

PFA 2% for 12 quarters 10.575

Present value of payments $7.09

$ 0.67 million∗PVF @2 % for 12 periods=$ 0.67∗10.575=$ 7.09 million

Decision:

As the net payment is lowest in case of quarterly payments ($7.09 million) so it should be

the preferred payment option.

Part-B

9

Year-2:

$ 0.41 million∗PVF @ 0.67 % for 12 periods ¿ 11th ¿ 24 th=$ 0.41∗12.468=$ 5.11 million

iii) Pay Quarterly

$ Millions

Quarter end payments 0.67

No of quarters 12

Risk adjusted rate quarterly 2.00%

PFA 2% for 12 quarters 10.575

Present value of payments $7.09

$ 0.67 million∗PVF @2 % for 12 periods=$ 0.67∗10.575=$ 7.09 million

Decision:

As the net payment is lowest in case of quarterly payments ($7.09 million) so it should be

the preferred payment option.

Part-B

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Executive Summary

This report presents an analysis of the capital structure and financial performance of ANZ

Bank. The capital structure of the bank has been static with little or few changes in the

composition of debt and equity. More or less, the debt equity ratio of the bank has been found to

be 0.86:1, which indicates that the bank is using more debt than equity. Further, the return on

equity ratio (11.90%) and EPS (237.1 cents) show improvement in the profitability. The liquidity

position of the bank is also good as shown by the improved liquidity coverage ratio (135%).

Introduction

The report presented here deals with the financial analysis of ANZ Bank. The ANZ Bank

is one of the top most banks operating in Australia and New Zealand. The report presents an

analysis of the capital structure and cost of capital of the bank. Further, the report also puts light

on the financial performance of the bank.

Analysis of the Capital Structure of ANZ

The capital structure of a firm shows the composition of its capital funds. A firm may

arrange funds from various sources which mainly fall in two primary categories such as equity

and debt. Different sources of funds have incurs different costs and have different risk

characteristics. Therefore, it becomes essential for a firm to analyze its capital structure and

optimize the cost of capital and risk.

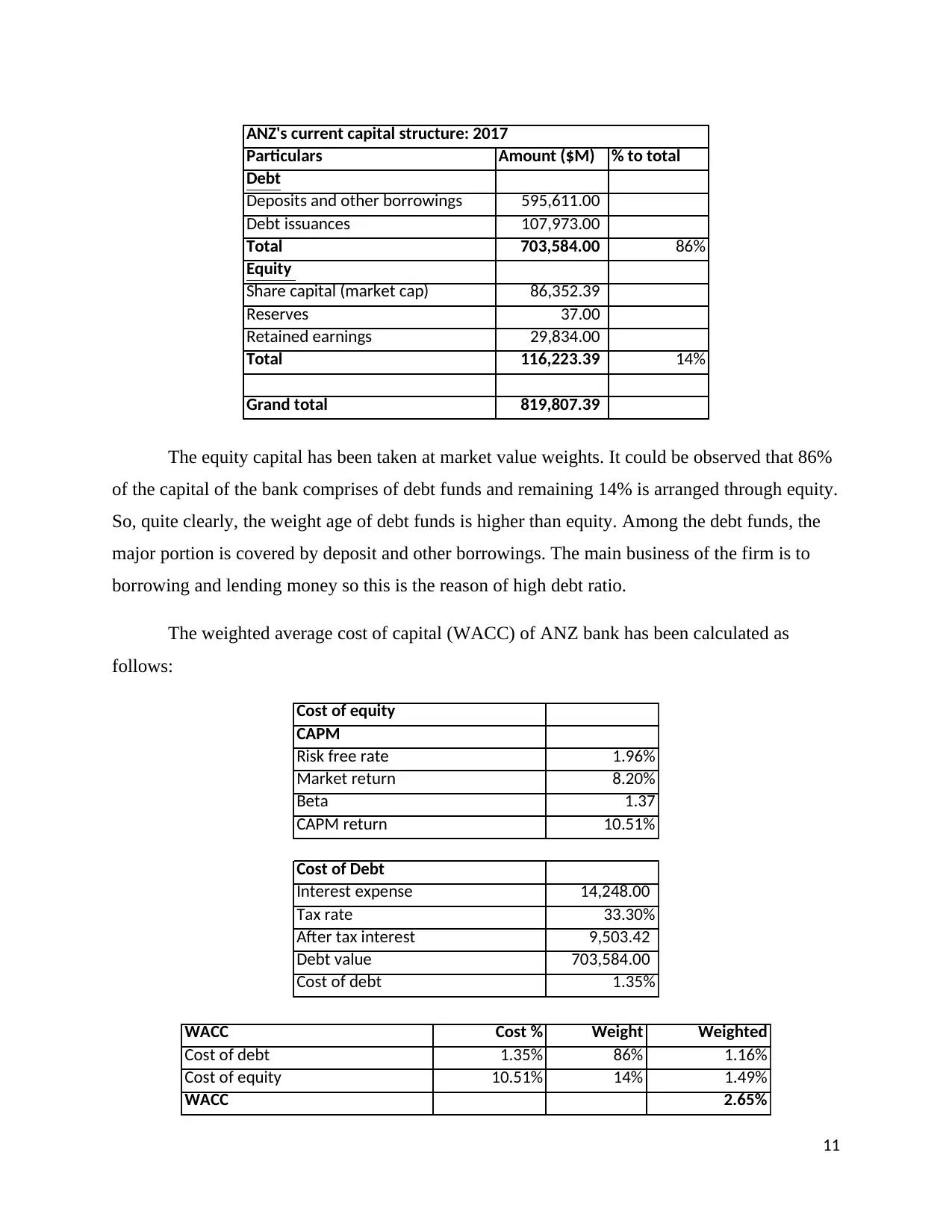

The capital structure of ANZ Bank for the year 2017 has been analyzed as under:

10

This report presents an analysis of the capital structure and financial performance of ANZ

Bank. The capital structure of the bank has been static with little or few changes in the

composition of debt and equity. More or less, the debt equity ratio of the bank has been found to

be 0.86:1, which indicates that the bank is using more debt than equity. Further, the return on

equity ratio (11.90%) and EPS (237.1 cents) show improvement in the profitability. The liquidity

position of the bank is also good as shown by the improved liquidity coverage ratio (135%).

Introduction

The report presented here deals with the financial analysis of ANZ Bank. The ANZ Bank

is one of the top most banks operating in Australia and New Zealand. The report presents an

analysis of the capital structure and cost of capital of the bank. Further, the report also puts light

on the financial performance of the bank.

Analysis of the Capital Structure of ANZ

The capital structure of a firm shows the composition of its capital funds. A firm may

arrange funds from various sources which mainly fall in two primary categories such as equity

and debt. Different sources of funds have incurs different costs and have different risk

characteristics. Therefore, it becomes essential for a firm to analyze its capital structure and

optimize the cost of capital and risk.

The capital structure of ANZ Bank for the year 2017 has been analyzed as under:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00

Debt issuances 107,973.00

Total 703,584.00 86%

Equity

Share capital (market cap) 86,352.39

Reserves 37.00

Retained earnings 29,834.00

Total 116,223.39 14%

Grand total 819,807.39

ANZ's current capital structure: 2017

The equity capital has been taken at market value weights. It could be observed that 86%

of the capital of the bank comprises of debt funds and remaining 14% is arranged through equity.

So, quite clearly, the weight age of debt funds is higher than equity. Among the debt funds, the

major portion is covered by deposit and other borrowings. The main business of the firm is to

borrowing and lending money so this is the reason of high debt ratio.

The weighted average cost of capital (WACC) of ANZ bank has been calculated as

follows:

Cost of equity

CAPM

Risk free rate 1.96%

Market return 8.20%

Beta 1.37

CAPM return 10.51%

Cost of Debt

Interest expense 14,248.00

Tax rate 33.30%

After tax interest 9,503.42

Debt value 703,584.00

Cost of debt 1.35%

WACC Cost % Weight Weighted

Cost of debt 1.35% 86% 1.16%

Cost of equity 10.51% 14% 1.49%

WACC 2.65%

11

Debt

Deposits and other borrowings 595,611.00

Debt issuances 107,973.00

Total 703,584.00 86%

Equity

Share capital (market cap) 86,352.39

Reserves 37.00

Retained earnings 29,834.00

Total 116,223.39 14%

Grand total 819,807.39

ANZ's current capital structure: 2017

The equity capital has been taken at market value weights. It could be observed that 86%

of the capital of the bank comprises of debt funds and remaining 14% is arranged through equity.

So, quite clearly, the weight age of debt funds is higher than equity. Among the debt funds, the

major portion is covered by deposit and other borrowings. The main business of the firm is to

borrowing and lending money so this is the reason of high debt ratio.

The weighted average cost of capital (WACC) of ANZ bank has been calculated as

follows:

Cost of equity

CAPM

Risk free rate 1.96%

Market return 8.20%

Beta 1.37

CAPM return 10.51%

Cost of Debt

Interest expense 14,248.00

Tax rate 33.30%

After tax interest 9,503.42

Debt value 703,584.00

Cost of debt 1.35%

WACC Cost % Weight Weighted

Cost of debt 1.35% 86% 1.16%

Cost of equity 10.51% 14% 1.49%

WACC 2.65%

11

The cost of equity has been computed applying the CAPM model. The cost of equity is

10.51% which is higher than the cost of debt of 1.35%. The weight of debt in the total capital of

the bank is 86%. So, the bank is using low cost funds more than the equity which incurs high

cost. Due to this composition, the weighted average cost of capital of the bank is 2.65% which

can be said to be quite low.

The CAPM return provides an approximation to the minimum required rate of return for

the equity investors. The equity investors can analyze that whether the firm is able to provide

them adequate return by comparing the CAPM return with the actual return on equity (ROE) of

the firm (Hou & Van Dijk, 2018). In the case of ANZ Bank, the CAPM return is 10.51% while

the return on equity is 11.90% (ANZ Bank, 2017), which indicates that the bank has been able to

provide adequate return to its equity investors.

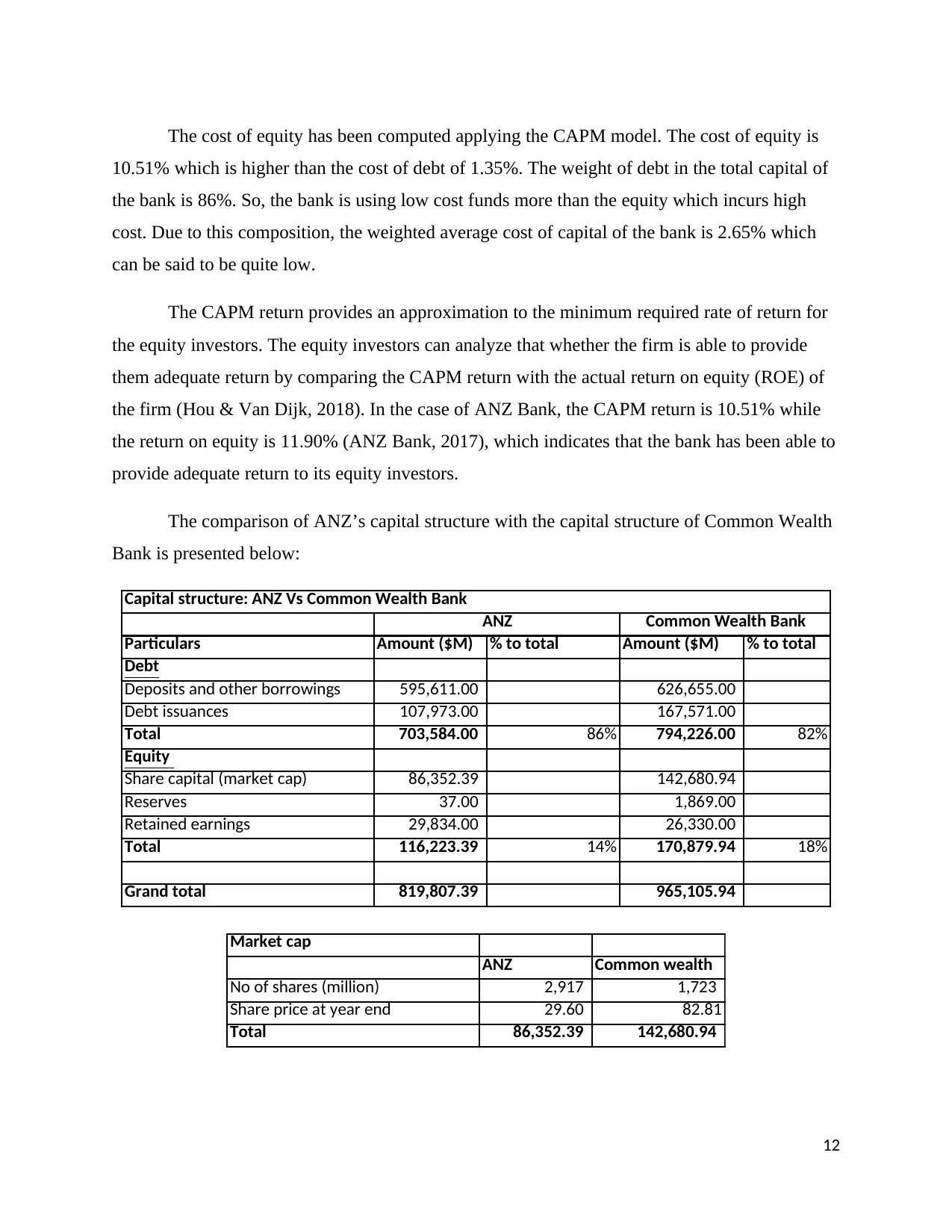

The comparison of ANZ’s capital structure with the capital structure of Common Wealth

Bank is presented below:

Particulars Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 626,655.00

Debt issuances 107,973.00 167,571.00

Total 703,584.00 86% 794,226.00 82%

Equity

Share capital (market cap) 86,352.39 142,680.94

Reserves 37.00 1,869.00

Retained earnings 29,834.00 26,330.00

Total 116,223.39 14% 170,879.94 18%

Grand total 819,807.39 965,105.94

Capital structure: ANZ Vs Common Wealth Bank

ANZ Common Wealth Bank

Market cap

ANZ Common wealth

No of shares (million) 2,917 1,723

Share price at year end 29.60 82.81

Total 86,352.39 142,680.94

12

10.51% which is higher than the cost of debt of 1.35%. The weight of debt in the total capital of

the bank is 86%. So, the bank is using low cost funds more than the equity which incurs high

cost. Due to this composition, the weighted average cost of capital of the bank is 2.65% which

can be said to be quite low.

The CAPM return provides an approximation to the minimum required rate of return for

the equity investors. The equity investors can analyze that whether the firm is able to provide

them adequate return by comparing the CAPM return with the actual return on equity (ROE) of

the firm (Hou & Van Dijk, 2018). In the case of ANZ Bank, the CAPM return is 10.51% while

the return on equity is 11.90% (ANZ Bank, 2017), which indicates that the bank has been able to

provide adequate return to its equity investors.

The comparison of ANZ’s capital structure with the capital structure of Common Wealth

Bank is presented below:

Particulars Amount ($M) % to total Amount ($M) % to total

Debt

Deposits and other borrowings 595,611.00 626,655.00

Debt issuances 107,973.00 167,571.00

Total 703,584.00 86% 794,226.00 82%

Equity

Share capital (market cap) 86,352.39 142,680.94

Reserves 37.00 1,869.00

Retained earnings 29,834.00 26,330.00

Total 116,223.39 14% 170,879.94 18%

Grand total 819,807.39 965,105.94

Capital structure: ANZ Vs Common Wealth Bank

ANZ Common Wealth Bank

Market cap

ANZ Common wealth

No of shares (million) 2,917 1,723

Share price at year end 29.60 82.81

Total 86,352.39 142,680.94

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.