ANZ Bank Financial Analysis & DecaSport Project Viability

VerifiedAdded on 2023/04/21

|14

|2486

|447

Report

AI Summary

This report provides a comprehensive financial analysis of two distinct entities: ANZ Bank and DecaSport. For ANZ Bank, the report examines its capital structure, calculates the weighted average cost of capital (WACC), compares its capital structure with Westpac, and evaluates its financial performance using various ratios like debt-to-equity, return on assets, return on equity, net profit ratio, and earnings per share. The analysis also touches upon corporate governance principles, integrity, and accountability in light of the Royal Commission findings. For DecaSport, the report assesses the viability of a new sport shoe model by calculating after-tax cash flows, net present value, payback period, and profitability index, and also analyzes the impact of varying sales units on cash flows and evaluates different payment options. The report concludes with recommendations based on the financial analysis of both entities.

Running head: ACCOUNTING AND FINANCE

Accounting and finance

Name of the student

Name of the university

Student ID

Author note

Accounting and finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Part A.........................................................................................................................................2

Requirement (a)......................................................................................................................2

Requirement (b).....................................................................................................................3

Part B..........................................................................................................................................6

Executive summary................................................................................................................6

Introduction............................................................................................................................6

Answer 1................................................................................................................................6

Answer 2................................................................................................................................8

Answer 3..............................................................................................................................10

Answer 4..............................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Part A.........................................................................................................................................2

Requirement (a)......................................................................................................................2

Requirement (b).....................................................................................................................3

Part B..........................................................................................................................................6

Executive summary................................................................................................................6

Introduction............................................................................................................................6

Answer 1................................................................................................................................6

Answer 2................................................................................................................................8

Answer 3..............................................................................................................................10

Answer 4..............................................................................................................................11

Reference..................................................................................................................................12

2ACCOUNTING AND FINANCE

Part A

Requirement (a)

1. After tax cash flows

After tax cash flows is the measure used for measuring the entity’s ability to generate

the positive cash flow after deducting the taxes. After tax cash flows of the company are

calculated as follows –

Total amount of after tax cash flows is $ 34,213,332.19.

2. Net present value

Net present value is present value of the investment’s projected cash inflows reduced

by initial cost expenses for acquiring the asset. The project is generally accepted if the net

present value is positive and is rejected if the net present value is negative (DeFusco et al.,

2015). From the above it can be identified that the net present value of the project is $

11,590,351. Hence, based on the NPV the project shall be accepted.

3. Payback period

Part A

Requirement (a)

1. After tax cash flows

After tax cash flows is the measure used for measuring the entity’s ability to generate

the positive cash flow after deducting the taxes. After tax cash flows of the company are

calculated as follows –

Total amount of after tax cash flows is $ 34,213,332.19.

2. Net present value

Net present value is present value of the investment’s projected cash inflows reduced

by initial cost expenses for acquiring the asset. The project is generally accepted if the net

present value is positive and is rejected if the net present value is negative (DeFusco et al.,

2015). From the above it can be identified that the net present value of the project is $

11,590,351. Hence, based on the NPV the project shall be accepted.

3. Payback period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

Payback period is the time required by the project to recover the initial investment

cost. It is an important determinant while deciding regarding acceptance of any project. From

the calculation it can be identified that the payback period of the project is 0.86 years that is

the initial investment related to the project will be recovered in 0.86 years and hence the

project is acceptable (Chandra, 2017).

4. Profitability index

It measures the ratio among the present value of the future cash flows and initial

investment. It is considered as an important tool to rank the projects and selecting one

particular project based on the rank. From the calculation it can be identified that the

profitability index of the project is 2.40. As the profitability index is more than 1 it is

indicating that the project will be able to recover its initial outlay amount and therefore

acceptable (Boyd, Epanchin-Niell & Siikamäki, 2015).

5. Viability of project

From all the measures used above it is identified that the project is acceptable from all

the aspects. Hence, the project will be considered as viable.

Requirement (b)

(i) After tax cash flows if sales units are 10% higher

Payback period is the time required by the project to recover the initial investment

cost. It is an important determinant while deciding regarding acceptance of any project. From

the calculation it can be identified that the payback period of the project is 0.86 years that is

the initial investment related to the project will be recovered in 0.86 years and hence the

project is acceptable (Chandra, 2017).

4. Profitability index

It measures the ratio among the present value of the future cash flows and initial

investment. It is considered as an important tool to rank the projects and selecting one

particular project based on the rank. From the calculation it can be identified that the

profitability index of the project is 2.40. As the profitability index is more than 1 it is

indicating that the project will be able to recover its initial outlay amount and therefore

acceptable (Boyd, Epanchin-Niell & Siikamäki, 2015).

5. Viability of project

From all the measures used above it is identified that the project is acceptable from all

the aspects. Hence, the project will be considered as viable.

Requirement (b)

(i) After tax cash flows if sales units are 10% higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

(ii) After tax cash flows if sales units are 10% lower

(iii) Findings

It can be identified from above that total cash flows generated when the sales level is

10% higher as compared to estimation for the 1st year is $ 37,522,165.41. On the other hand,

total cash flows generated when the sales level is 10% lower as compared to estimation for

(ii) After tax cash flows if sales units are 10% lower

(iii) Findings

It can be identified from above that total cash flows generated when the sales level is

10% higher as compared to estimation for the 1st year is $ 37,522,165.41. On the other hand,

total cash flows generated when the sales level is 10% lower as compared to estimation for

5ACCOUNTING AND FINANCE

the 1st year is $ 30,904,498.97. Hence, cash flow is highest when the sales level is 10% higher

as compared to estimation for the 1st year (Gaudard, 2015).

(iv) Decision regarding payment option

If the payment is paid in full at the time of purchase the payment required to be made

is $ 71,25,000 after getting 5% discount. If the payment is monthly the total amount required

to be paid is $ 71,06,724 and if the payment is made on quarterly basis in 3 years the amount

required to be paid is $ 69,06,360. Hence, the payment is lowest if it is made on quarterly

basis for 3 years. Hence, the company shall choose quarterly payment option.

the 1st year is $ 30,904,498.97. Hence, cash flow is highest when the sales level is 10% higher

as compared to estimation for the 1st year (Gaudard, 2015).

(iv) Decision regarding payment option

If the payment is paid in full at the time of purchase the payment required to be made

is $ 71,25,000 after getting 5% discount. If the payment is monthly the total amount required

to be paid is $ 71,06,724 and if the payment is made on quarterly basis in 3 years the amount

required to be paid is $ 69,06,360. Hence, the payment is lowest if it is made on quarterly

basis for 3 years. Hence, the company shall choose quarterly payment option.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

Part B

Executive summary

The purpose of the report is to review the capital structure of ANZ bank and reporting

on the ability of the company to generate return for its shareholders. The report will focus on

the debt and equity component of the company’s capital structure for the year ended 2017. It

will further compute the after tax weighted average cost of capital and will compare its

capital structure with any other firm in the same industry. Further, the report will evaluate the

performance of the company through computing the financial ratios. Any significant changes

in the capital structure of the company will also be discussed in the report.

Introduction

Australia and New Zealand Banking Group Limited offers wide range of financial and

banking services and products. The bank’s segments include New Zealand, Australia,

institutional, Wealth Australia, Asia Retail & Pacific, technology, service, operations and the

group centre. Operation span of the bank is in New Zealand, Australia and various countries

in Asia Pacific region, United Kingdom, Germany, France, and United States. It offers

savings, current, premium call, cal deposits, solicitors trust, trust management and other

accounts for international payment, foreign currency and credit and debit cards. It further

offers mortgages, personal loans, overdrafts, home loans, flexible facilities, commercial and

business loans, investment services, rural finances, house, contents, boats, car, credit card

payment, firm and equipment and business (Anz.com, 2019).

Answer 1

(a) Capital structure

Part B

Executive summary

The purpose of the report is to review the capital structure of ANZ bank and reporting

on the ability of the company to generate return for its shareholders. The report will focus on

the debt and equity component of the company’s capital structure for the year ended 2017. It

will further compute the after tax weighted average cost of capital and will compare its

capital structure with any other firm in the same industry. Further, the report will evaluate the

performance of the company through computing the financial ratios. Any significant changes

in the capital structure of the company will also be discussed in the report.

Introduction

Australia and New Zealand Banking Group Limited offers wide range of financial and

banking services and products. The bank’s segments include New Zealand, Australia,

institutional, Wealth Australia, Asia Retail & Pacific, technology, service, operations and the

group centre. Operation span of the bank is in New Zealand, Australia and various countries

in Asia Pacific region, United Kingdom, Germany, France, and United States. It offers

savings, current, premium call, cal deposits, solicitors trust, trust management and other

accounts for international payment, foreign currency and credit and debit cards. It further

offers mortgages, personal loans, overdrafts, home loans, flexible facilities, commercial and

business loans, investment services, rural finances, house, contents, boats, car, credit card

payment, firm and equipment and business (Anz.com, 2019).

Answer 1

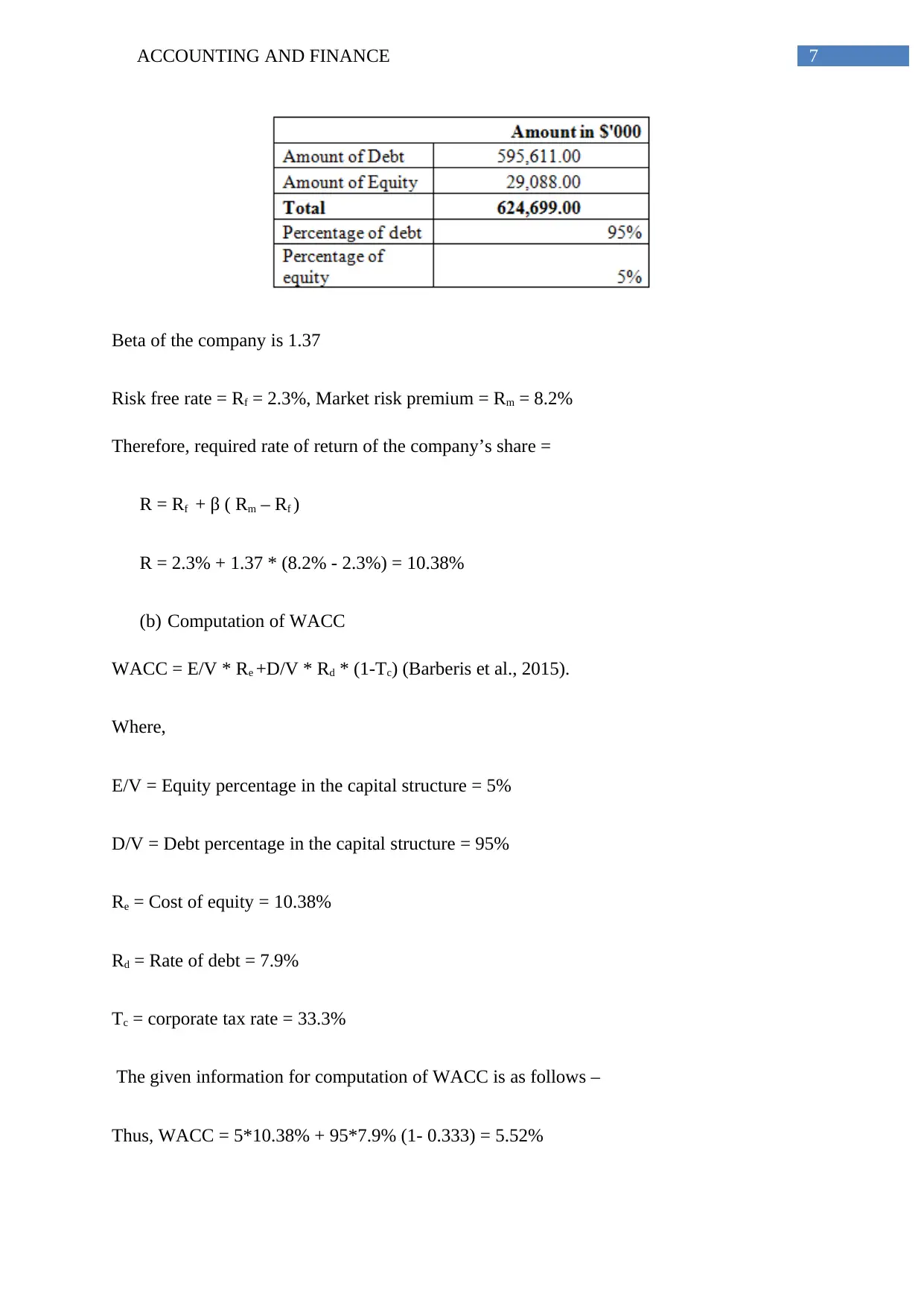

(a) Capital structure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

Beta of the company is 1.37

Risk free rate = Rf = 2.3%, Market risk premium = Rm = 8.2%

Therefore, required rate of return of the company’s share =

R = Rf + β ( Rm – Rf )

R = 2.3% + 1.37 * (8.2% - 2.3%) = 10.38%

(b) Computation of WACC

WACC = E/V * Re +D/V * Rd * (1-Tc) (Barberis et al., 2015).

Where,

E/V = Equity percentage in the capital structure = 5%

D/V = Debt percentage in the capital structure = 95%

Re = Cost of equity = 10.38%

Rd = Rate of debt = 7.9%

Tc = corporate tax rate = 33.3%

The given information for computation of WACC is as follows –

Thus, WACC = 5*10.38% + 95*7.9% (1- 0.333) = 5.52%

Beta of the company is 1.37

Risk free rate = Rf = 2.3%, Market risk premium = Rm = 8.2%

Therefore, required rate of return of the company’s share =

R = Rf + β ( Rm – Rf )

R = 2.3% + 1.37 * (8.2% - 2.3%) = 10.38%

(b) Computation of WACC

WACC = E/V * Re +D/V * Rd * (1-Tc) (Barberis et al., 2015).

Where,

E/V = Equity percentage in the capital structure = 5%

D/V = Debt percentage in the capital structure = 95%

Re = Cost of equity = 10.38%

Rd = Rate of debt = 7.9%

Tc = corporate tax rate = 33.3%

The given information for computation of WACC is as follows –

Thus, WACC = 5*10.38% + 95*7.9% (1- 0.333) = 5.52%

8ACCOUNTING AND FINANCE

(c) Return as compared to risk

The actual return from the stock of the company is 1.50% whereas the expected return

as per CAPM is 10.38%. Hence, it can be determined that the company’s stock is

underperforming and is not generating given its risk (In.finance.yahoo.com, 2019).

(d) Comparison of capital structure

Capital structure of Westpac bank

Comparing the capital structure of ANZ bank with Westpac bank it can be identified

that both the banks are aggressively depended on debt as compared to equity. However, it can

be stated that Westpac bank is slightly less depended on debt as compared to ANZ as the debt

component of ANZ is 95% whereas the same for Westpac bank is 94%.

Answer 2

Ratio analysis

(c) Return as compared to risk

The actual return from the stock of the company is 1.50% whereas the expected return

as per CAPM is 10.38%. Hence, it can be determined that the company’s stock is

underperforming and is not generating given its risk (In.finance.yahoo.com, 2019).

(d) Comparison of capital structure

Capital structure of Westpac bank

Comparing the capital structure of ANZ bank with Westpac bank it can be identified

that both the banks are aggressively depended on debt as compared to equity. However, it can

be stated that Westpac bank is slightly less depended on debt as compared to ANZ as the debt

component of ANZ is 95% whereas the same for Westpac bank is 94%.

Answer 2

Ratio analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

Ratio interpretation –

Debt equity ratio – debt to equity ratio is the solvency ratio used for measuring the

percentages of fund raised through debt and percentage raised through equity. It determines

that leverage position of the company as higher debt equity ratio determines that the company

is using aggressive funding from outside for its business operation. Looking into the debt

equity ratio of the company it can be identified that though the debt dependency of the

company has been reduced over the years from 2016 to 2017, significantly high debt equity

ratio of the company is indicating that the company is highly leveraged (Minnis &

Sutherland, 2017).

Return on assets – return on asset is used to indicate the profitability of the entity as

compared to the assets. It provides the analyst, investors and manager an idea regarding how

efficient the management of the company can be in using the assets for generating earnings.

Return on assets for the company is significantly low and has not been improved in 2017 as

compared to 2016. For both the years the return on asset is 0.1 (Brigham et al., 2016)

Return on equity – it is an important ratio as it measures the return rate received by the

owners of company’s common stock received for their shareholdings. It signifies how

efficient the company is with regard to generation of returns on investment received from the

Ratio interpretation –

Debt equity ratio – debt to equity ratio is the solvency ratio used for measuring the

percentages of fund raised through debt and percentage raised through equity. It determines

that leverage position of the company as higher debt equity ratio determines that the company

is using aggressive funding from outside for its business operation. Looking into the debt

equity ratio of the company it can be identified that though the debt dependency of the

company has been reduced over the years from 2016 to 2017, significantly high debt equity

ratio of the company is indicating that the company is highly leveraged (Minnis &

Sutherland, 2017).

Return on assets – return on asset is used to indicate the profitability of the entity as

compared to the assets. It provides the analyst, investors and manager an idea regarding how

efficient the management of the company can be in using the assets for generating earnings.

Return on assets for the company is significantly low and has not been improved in 2017 as

compared to 2016. For both the years the return on asset is 0.1 (Brigham et al., 2016)

Return on equity – it is an important ratio as it measures the return rate received by the

owners of company’s common stock received for their shareholdings. It signifies how

efficient the company is with regard to generation of returns on investment received from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

shareholders. Looking into the return on equity ratio of the company it can be identified that

though the ratio of the company has been increased slightly over the years from 2016 to

2017, significantly low return ratio is indicating that the company is not able to provide

sufficient return to its shareholders (Weygandt, Kimmel & Kieso, 2015).

Net profit ratio – it establishes the relationship among net profit after taxes and revenues. It is

considered as a major profitability ratio as it assists in determining overall efficiency of

business operation. Further, it indicates how well the trading activities of the company are

performing. Looking into the net profit ratio of the company it can be identified that the net

profit of the company has been increased from 27.84% to 31.67%. Hence, it can be stated that

the profitability position of the company has been improved over the years from 2016 to

2017.

Earnings per share – it represents proportion of the entity’s earnings left with the entity after

paying the taxes, preferred stock dividend and it is allocated to each common stock. Looking

into the EPS of the company it can be identified that it has been increased from 197.40 to

220.10. Hence, it can be stated that the earning position of the company has been improved

over the years from 2016 to 2017 (Gitman, Juchau & Flanagan, 2015).

Answer 3

Changes in capital structure

shareholders. Looking into the return on equity ratio of the company it can be identified that

though the ratio of the company has been increased slightly over the years from 2016 to

2017, significantly low return ratio is indicating that the company is not able to provide

sufficient return to its shareholders (Weygandt, Kimmel & Kieso, 2015).

Net profit ratio – it establishes the relationship among net profit after taxes and revenues. It is

considered as a major profitability ratio as it assists in determining overall efficiency of

business operation. Further, it indicates how well the trading activities of the company are

performing. Looking into the net profit ratio of the company it can be identified that the net

profit of the company has been increased from 27.84% to 31.67%. Hence, it can be stated that

the profitability position of the company has been improved over the years from 2016 to

2017.

Earnings per share – it represents proportion of the entity’s earnings left with the entity after

paying the taxes, preferred stock dividend and it is allocated to each common stock. Looking

into the EPS of the company it can be identified that it has been increased from 197.40 to

220.10. Hence, it can be stated that the earning position of the company has been improved

over the years from 2016 to 2017 (Gitman, Juchau & Flanagan, 2015).

Answer 3

Changes in capital structure

11ACCOUNTING AND FINANCE

It can be seen from the above table that for all previous 3 years the debt component of

the capital structure was 95% and the equity component was 5%. Hence, there were no

changes in the capital structure of the company.

Answer 4

Conclusion regarding the integrity and accountability

Principle of integrity states that the management are adhered to strict ethical or moral

code notwithstanding from any pressure regarding acting otherwise. It is important concept of

corporate governance as integrity deals with the principle of equitable and fair dealings with

the shareholders. On the other hand accountability and transparency are inter-connected.

Though all the decisions can be shared outside of the business the management are obliged to

use right tone while communicating the shareholders. The shareholders must be able to

understand the decision making process of the board, its challenges, responsibility and its

plan to address the shareholders.

Some of the key findings of Royal Commission were – (i) lenders were preferring

pursuit of the profit over everything else (ii) financial advice ignored the basis standards for

honesty (iii) reluctant upon the changes to the small business laws for lending (iv) basis

transactions made for confusing the indigenous customers (ABC News, 2018). Owing to the

scandal the bank face significant fell in its share value that took a year to recover the pre-

raising value fir A$ 32.58. Looking into the management’s style of operating the business it

can be concluded that the entity is not following the integrity and accountability concept of

corporate governance and they are not successful in managing the operational risks.

It can be seen from the above table that for all previous 3 years the debt component of

the capital structure was 95% and the equity component was 5%. Hence, there were no

changes in the capital structure of the company.

Answer 4

Conclusion regarding the integrity and accountability

Principle of integrity states that the management are adhered to strict ethical or moral

code notwithstanding from any pressure regarding acting otherwise. It is important concept of

corporate governance as integrity deals with the principle of equitable and fair dealings with

the shareholders. On the other hand accountability and transparency are inter-connected.

Though all the decisions can be shared outside of the business the management are obliged to

use right tone while communicating the shareholders. The shareholders must be able to

understand the decision making process of the board, its challenges, responsibility and its

plan to address the shareholders.

Some of the key findings of Royal Commission were – (i) lenders were preferring

pursuit of the profit over everything else (ii) financial advice ignored the basis standards for

honesty (iii) reluctant upon the changes to the small business laws for lending (iv) basis

transactions made for confusing the indigenous customers (ABC News, 2018). Owing to the

scandal the bank face significant fell in its share value that took a year to recover the pre-

raising value fir A$ 32.58. Looking into the management’s style of operating the business it

can be concluded that the entity is not following the integrity and accountability concept of

corporate governance and they are not successful in managing the operational risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.