Management Accounting Case Study: Situational Analysis for Airlines

VerifiedAdded on 2020/05/16

|5

|755

|157

Case Study

AI Summary

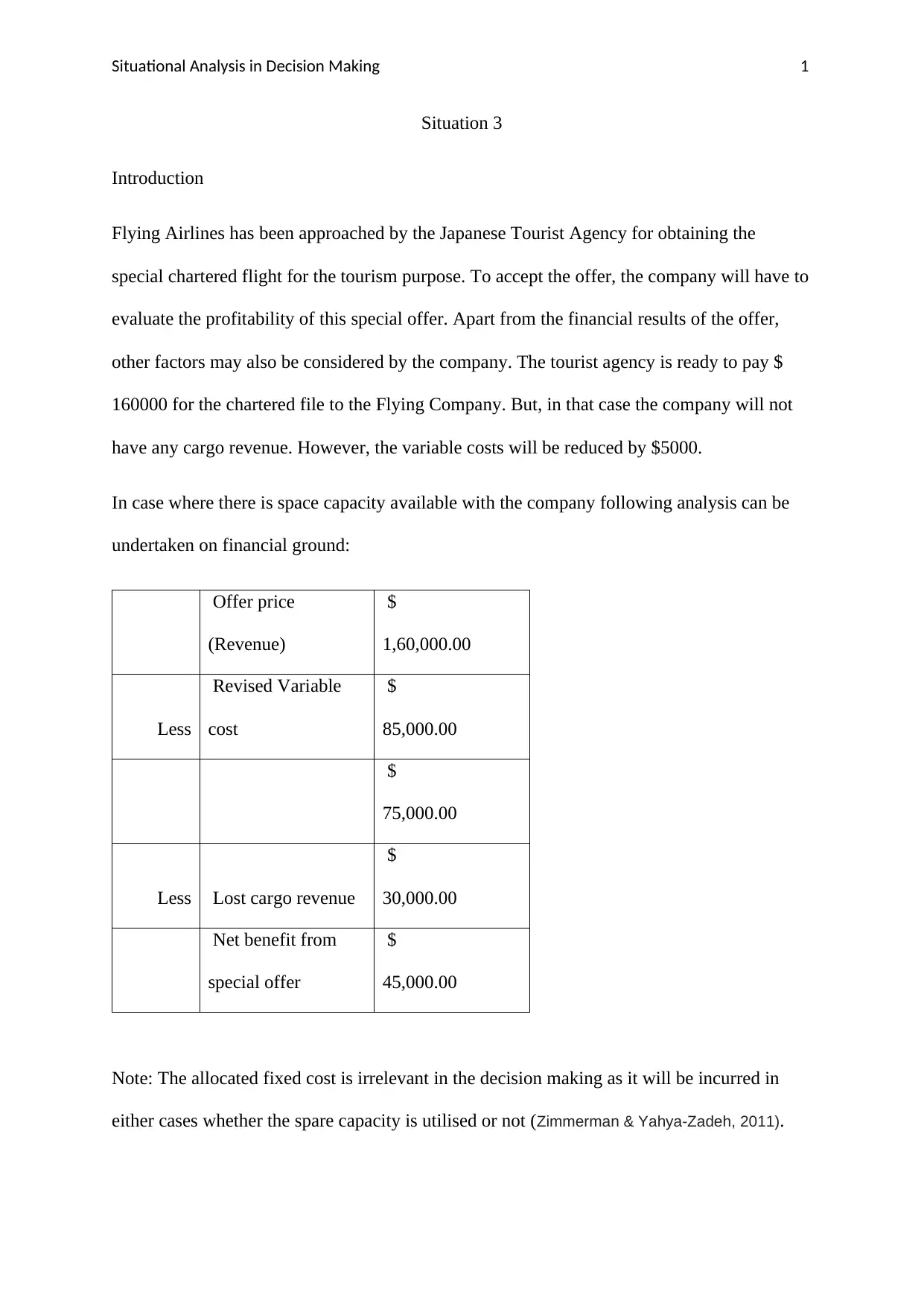

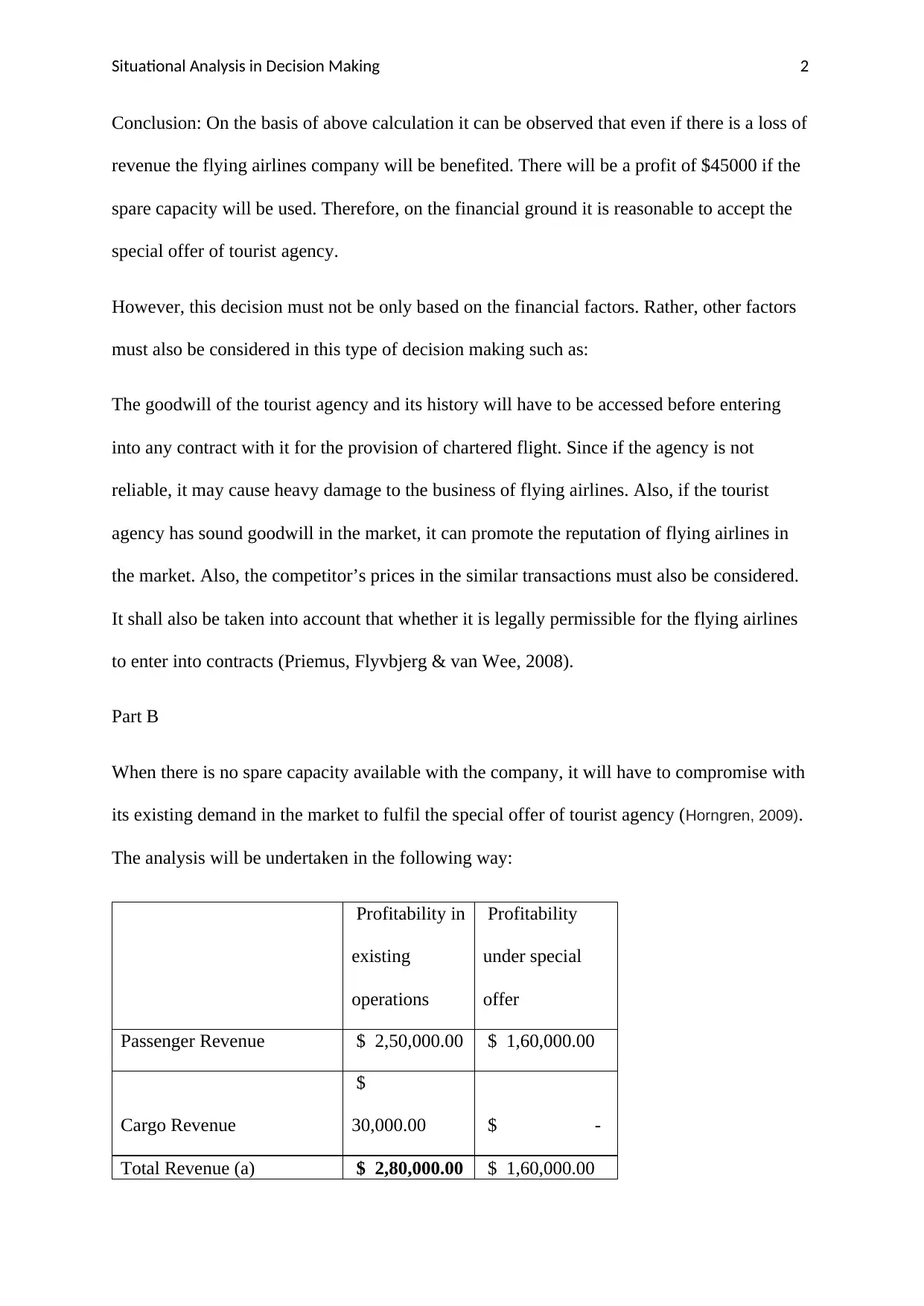

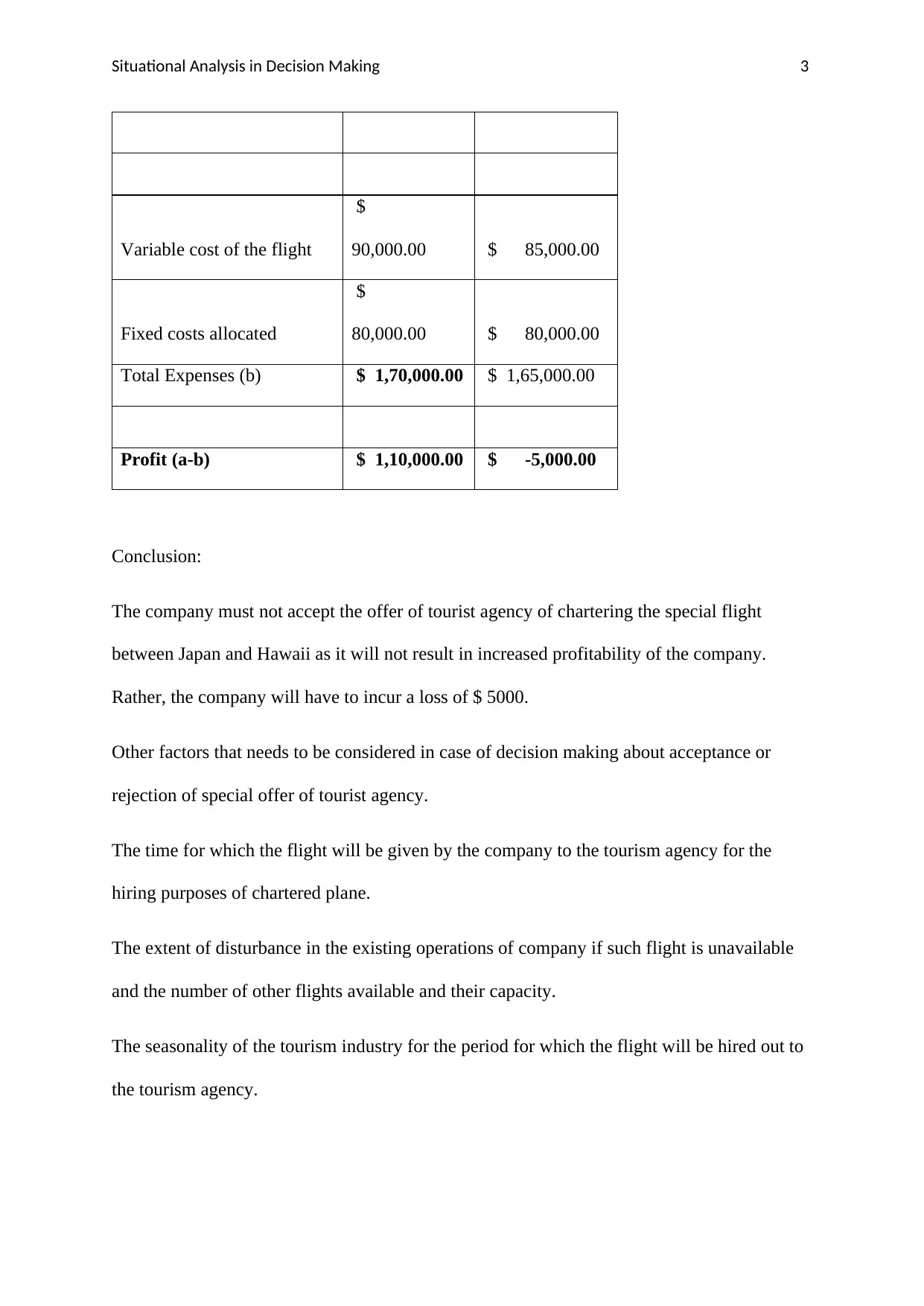

This case study explores the decision-making process for Flying Airlines regarding a special chartered flight offer from a Japanese Tourist Agency. The assignment analyzes the profitability of the offer under two scenarios: when spare capacity is available and when it is not. The financial analysis includes revenue, variable costs, and lost cargo revenue, leading to conclusions about whether to accept the offer based on financial grounds. The study emphasizes the importance of considering non-financial factors like the tourist agency's reputation and competitor pricing. When there is no spare capacity, the analysis shows a potential loss, leading to a recommendation against accepting the offer. The assignment also highlights additional factors to consider, such as the flight duration, impact on existing operations, and seasonality of the tourism industry. The analysis utilizes concepts from management accounting and cost accounting to guide decision-making.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.