Defined Benefit Plan Analysis: Investment Choice and Superannuation

VerifiedAdded on 2022/11/25

|10

|2898

|350

Report

AI Summary

This report examines defined benefit plans, investment choice plans, and superannuation within the context of the tertiary sector and Hewlett-Packard. It explores the different types of superannuation plans available to employees, including investment choice plans and defined benefit plans, detailing their characteristics and how they operate. The report delves into the factors that tertiary sector employees consider when deciding between these plans, such as financial security, age, employee mobility, historical performance, information levels, gender, and sense of security. Furthermore, it analyzes the significance of the time value of money and tax implications in the decision-making process, highlighting how these factors influence investment choices. The conclusion emphasizes the importance of offering beneficial investment options to attract and retain employees in the tertiary sector, suggesting that defined benefit plans can be a suitable choice for creating investment value and fostering consistent investment habits. The report also references various academic sources to support its findings.

DEFINED BENEFIT PLAN

Module Number-

[DATE]

Hewlett-Packard

Module Number-

[DATE]

Hewlett-Packard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................2

Different plans of Superannuation.........................................................................................................2

Investment choice plan......................................................................................................................2

Defined benefit plan..........................................................................................................................3

Factors considered by tertiary sector employees in deciding whether to place their superannuation

contributions in the Defined Benefit Plan or the Investment Choice Plan.............................................3

Issues relating to the concept of the time value of money, taxes etc., might be important in this

decision-making process........................................................................................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Introduction...........................................................................................................................................2

Different plans of Superannuation.........................................................................................................2

Investment choice plan......................................................................................................................2

Defined benefit plan..........................................................................................................................3

Factors considered by tertiary sector employees in deciding whether to place their superannuation

contributions in the Defined Benefit Plan or the Investment Choice Plan.............................................3

Issues relating to the concept of the time value of money, taxes etc., might be important in this

decision-making process........................................................................................................................5

Conclusion.............................................................................................................................................6

References.............................................................................................................................................7

Introduction

With the changes in time, each and every employee need to strengthen their

investment options to increase the available return on capital employed. However, there are

several investment options which could be used by employees to increase their return on

investment such as tertiary investment option, defined benefit plan, superannuation

investment option. It is considered that tertiary sector is successfully fulfilling the servicing

needs of the people. Service requirement and its fulfilment is left with no gap these days. The

tertiary sector is satiating the needs of the people in every possible way as this sector is

working out in this provision. This way the economy is no longer facing the problem related

to consumer demand related to high quality. The development of an economy is determined

by the fact that whether the primary and secondary sectors of the economy are moving

towards the tertiary sector. Financial institutions, schools, restaurants, transportation and

salon are some of the basic examples of tertiary sector.

The sector also has employees who are called tertiary sector employees that work in different

fields that get to business running. Such employees are benefitted as well as they get some

rewards in addition to the basic salary that they get. The benefits are in cash or maybe in

kind. There is superannuation contribution as well which lets their future get better and

secure exactly like pension fund. Both the parties that is the employee as well as the

employer make contribution to this amount and it keeps on increasing. This creates a sense of

financial security amongst the employees as a small contribution done today can help in

saving their future. However, the contributions vary differently in different economies.

Different plans of Superannuation

The following are the different options of investments that are used in the tertiary sector for

their employees to help secure their future. However, the selection of the particular

investment option is based on the available return on investment and associated risk with the

investment plans (Bae, et al. 2018).

Investment choice plan

This plan makes sure that the employees invest the amount in an investment portfolio. The

deduction is done on a fixed percentage of the salary of the employee and there is no other

With the changes in time, each and every employee need to strengthen their

investment options to increase the available return on capital employed. However, there are

several investment options which could be used by employees to increase their return on

investment such as tertiary investment option, defined benefit plan, superannuation

investment option. It is considered that tertiary sector is successfully fulfilling the servicing

needs of the people. Service requirement and its fulfilment is left with no gap these days. The

tertiary sector is satiating the needs of the people in every possible way as this sector is

working out in this provision. This way the economy is no longer facing the problem related

to consumer demand related to high quality. The development of an economy is determined

by the fact that whether the primary and secondary sectors of the economy are moving

towards the tertiary sector. Financial institutions, schools, restaurants, transportation and

salon are some of the basic examples of tertiary sector.

The sector also has employees who are called tertiary sector employees that work in different

fields that get to business running. Such employees are benefitted as well as they get some

rewards in addition to the basic salary that they get. The benefits are in cash or maybe in

kind. There is superannuation contribution as well which lets their future get better and

secure exactly like pension fund. Both the parties that is the employee as well as the

employer make contribution to this amount and it keeps on increasing. This creates a sense of

financial security amongst the employees as a small contribution done today can help in

saving their future. However, the contributions vary differently in different economies.

Different plans of Superannuation

The following are the different options of investments that are used in the tertiary sector for

their employees to help secure their future. However, the selection of the particular

investment option is based on the available return on investment and associated risk with the

investment plans (Bae, et al. 2018).

Investment choice plan

This plan makes sure that the employees invest the amount in an investment portfolio. The

deduction is done on a fixed percentage of the salary of the employee and there is no other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

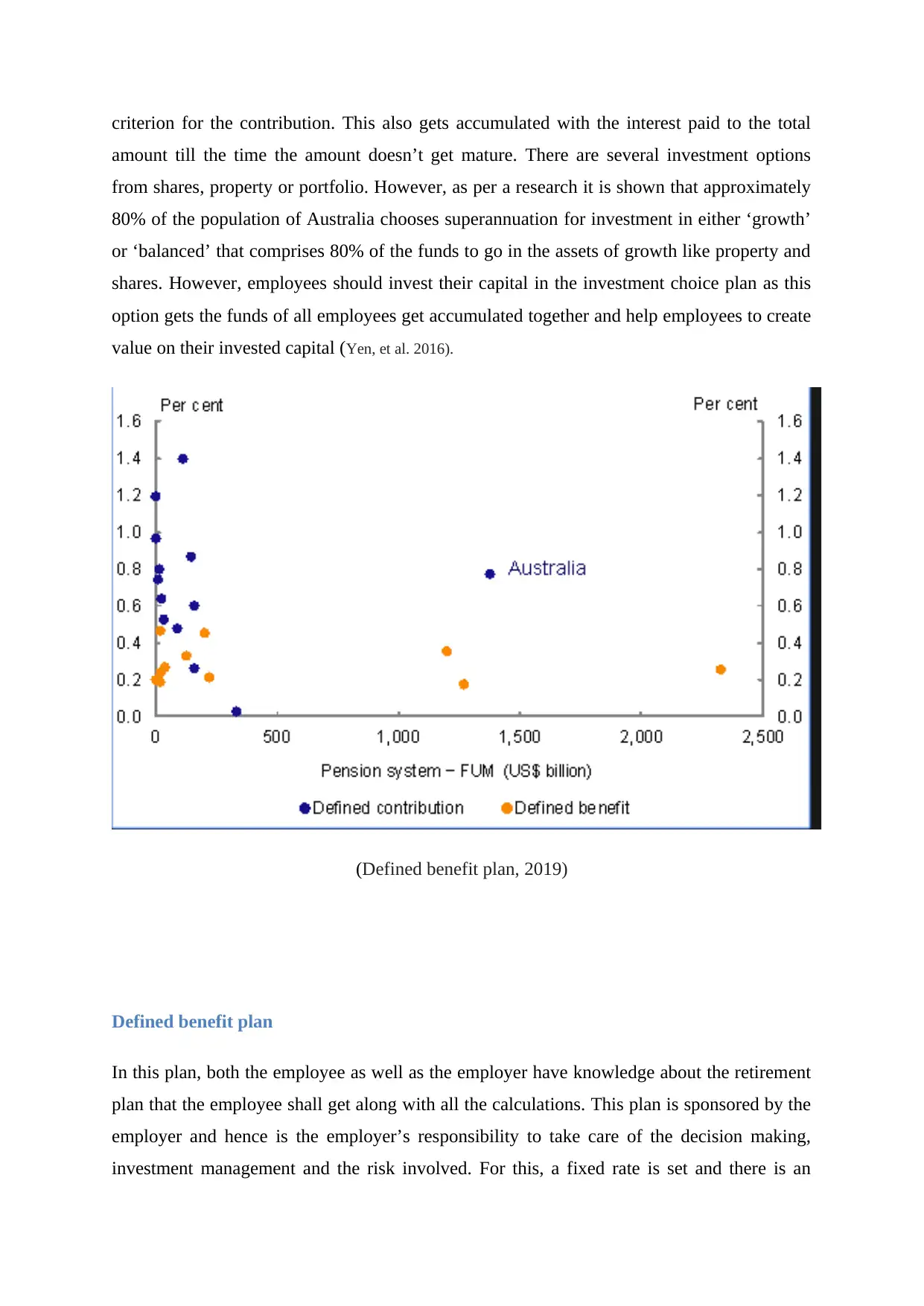

criterion for the contribution. This also gets accumulated with the interest paid to the total

amount till the time the amount doesn’t get mature. There are several investment options

from shares, property or portfolio. However, as per a research it is shown that approximately

80% of the population of Australia chooses superannuation for investment in either ‘growth’

or ‘balanced’ that comprises 80% of the funds to go in the assets of growth like property and

shares. However, employees should invest their capital in the investment choice plan as this

option gets the funds of all employees get accumulated together and help employees to create

value on their invested capital (Yen, et al. 2016).

(Defined benefit plan, 2019)

Defined benefit plan

In this plan, both the employee as well as the employer have knowledge about the retirement

plan that the employee shall get along with all the calculations. This plan is sponsored by the

employer and hence is the employer’s responsibility to take care of the decision making,

investment management and the risk involved. For this, a fixed rate is set and there is an

amount till the time the amount doesn’t get mature. There are several investment options

from shares, property or portfolio. However, as per a research it is shown that approximately

80% of the population of Australia chooses superannuation for investment in either ‘growth’

or ‘balanced’ that comprises 80% of the funds to go in the assets of growth like property and

shares. However, employees should invest their capital in the investment choice plan as this

option gets the funds of all employees get accumulated together and help employees to create

value on their invested capital (Yen, et al. 2016).

(Defined benefit plan, 2019)

Defined benefit plan

In this plan, both the employee as well as the employer have knowledge about the retirement

plan that the employee shall get along with all the calculations. This plan is sponsored by the

employer and hence is the employer’s responsibility to take care of the decision making,

investment management and the risk involved. For this, a fixed rate is set and there is an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actuary who investigates the contribution rate on a regular basis and any deficiency is rate is

met by the employer itself. The benefit is calculated as per the defined benefit plan

considering many factors including the age of the employee at the retirement, salary and

years of service of the employee (Ryland, 2010). The payment made to the employee is done

in various methods like lump sum, pension, or both (Lee, et al. 2017).

Factors considered by tertiary sector employees in deciding whether to place their

superannuation contributions in the Defined Benefit Plan or the Investment Choice

Plan

The decision to invest in different plans of superannuation for the Defined Benefit Plan or

Investment Choice Plan is not an easy one for the employees of the tertiary sector. Since

everything comes with uncertainty, these plans also have uncertainty involved and for the

same reason there are many factors that are considered to take a decision. However, these

factors change along with the economic changes. They are discussed below:

Financial security: It gets the employees who make the decision to invest in superannuation

plan the financial stability that they require. People who are financially sound opt for

investment choice plan and those having limited earning go for defined benefit plan.

Therefore, the financial stability of a person is assessed so that their risk is lowered in the

investment plan opted (Serrasqueiro, 2016).

Age of Employee: Those employees who are young are more into investing in the investment

choice plan. The period between the investment tenure and the age of the retirement is large

for young employees and hence these employees can use the market movements in a positive

manner so that they get the maximum benefit (Vilkinas, 2014). The time incurred to make the

changes in the portfolio they have invested in is quite high and hence the stagnant nature of

any portfolio can be avoided by them. On the contrary to this, the employees having higher

age depends on the retirement benefits. They don’t prefer investment choice plan as they

have less choices in the portfolio and in the risk assumed (Josa-Fombellida, López-Casado, and

Rincón-Zapatero, 2018).

Employee Mobility: There are employees who switch jobs more often as compared to others.

Such employees invest in investment choice plan as this option gets the funds of all

employees get accumulated together and is however invested as per the wish of the

employee. The plans of the investment choice is a preferable for the fact that the defined

met by the employer itself. The benefit is calculated as per the defined benefit plan

considering many factors including the age of the employee at the retirement, salary and

years of service of the employee (Ryland, 2010). The payment made to the employee is done

in various methods like lump sum, pension, or both (Lee, et al. 2017).

Factors considered by tertiary sector employees in deciding whether to place their

superannuation contributions in the Defined Benefit Plan or the Investment Choice

Plan

The decision to invest in different plans of superannuation for the Defined Benefit Plan or

Investment Choice Plan is not an easy one for the employees of the tertiary sector. Since

everything comes with uncertainty, these plans also have uncertainty involved and for the

same reason there are many factors that are considered to take a decision. However, these

factors change along with the economic changes. They are discussed below:

Financial security: It gets the employees who make the decision to invest in superannuation

plan the financial stability that they require. People who are financially sound opt for

investment choice plan and those having limited earning go for defined benefit plan.

Therefore, the financial stability of a person is assessed so that their risk is lowered in the

investment plan opted (Serrasqueiro, 2016).

Age of Employee: Those employees who are young are more into investing in the investment

choice plan. The period between the investment tenure and the age of the retirement is large

for young employees and hence these employees can use the market movements in a positive

manner so that they get the maximum benefit (Vilkinas, 2014). The time incurred to make the

changes in the portfolio they have invested in is quite high and hence the stagnant nature of

any portfolio can be avoided by them. On the contrary to this, the employees having higher

age depends on the retirement benefits. They don’t prefer investment choice plan as they

have less choices in the portfolio and in the risk assumed (Josa-Fombellida, López-Casado, and

Rincón-Zapatero, 2018).

Employee Mobility: There are employees who switch jobs more often as compared to others.

Such employees invest in investment choice plan as this option gets the funds of all

employees get accumulated together and is however invested as per the wish of the

employee. The plans of the investment choice is a preferable for the fact that the defined

benefit plan works with the opening of several defined benefit plans for each employer the

employee works for. This helps in segregating the benefits to the employees.

Historical Performance of the Plans: Each plan is based on the observation on how different

plans have worked in the past and hence is decided which superannuation fund to invest in.

The performance is checked by the plans with the recent records, for example a year or a

quarter is compared, and the results are checked. This helps in making a decision as one can

check the changes in the return based on the capital invested by them. To add on, it has been

found that approximately 60% to 80% of the Australian employees takes investment choice

plan as their superannuation investment option (Korzynski, 2013).

Level of information available with the employees: The difference between the current

market performance and the expected market performance based on different employees have

an effect on the investment decisions of the employees. Those who are well-versed with the

movement of the market are the ones who choose investment choice plan in general. This is

because of the fact that they have vast knowledge that helps them gain higher interest on their

income. At the contrary, employees having less information go for the defined benefit plan.

Gender: The gender also plays a vital role in the life of the employees to choose their

superannuation fund. It is often observed that women have more risk than men and hence

they choose high risk investment plan if they fetch higher interest. Women have a habit of

saving and hence are seen to be choosing a plan that involves lesser risk. However, this may

also vary on various factors like how they are in their personal as well as professional life.

Sense of Security: There are people who don’t want to take a lot of risk and hence want to

stay secured. It has been seen that such people usually opt defined benefit plan as there is risk

and uncertainty attached with the investment choice plans. The investment choice plan on the

contrary depends on the movement of the market and hence the sense of security is put at

stake (Review, 2015).

No matter there are many constraints and factors that one has for the investment, it also

depends on the personal life and interest of the employees as well (Lin, MacMinn, and Tian,

2015).

Issues relating to the concept of the time value of money, taxes etc., might be important

in this decision-making process

Time value of money and taxes in an economy are also important factors that play a role in

the investment choice plan or defined benefit plan in superannuation investment (Kio, 2015).

However, tax deduction is the key imperative factor for the employees who are having high

employee works for. This helps in segregating the benefits to the employees.

Historical Performance of the Plans: Each plan is based on the observation on how different

plans have worked in the past and hence is decided which superannuation fund to invest in.

The performance is checked by the plans with the recent records, for example a year or a

quarter is compared, and the results are checked. This helps in making a decision as one can

check the changes in the return based on the capital invested by them. To add on, it has been

found that approximately 60% to 80% of the Australian employees takes investment choice

plan as their superannuation investment option (Korzynski, 2013).

Level of information available with the employees: The difference between the current

market performance and the expected market performance based on different employees have

an effect on the investment decisions of the employees. Those who are well-versed with the

movement of the market are the ones who choose investment choice plan in general. This is

because of the fact that they have vast knowledge that helps them gain higher interest on their

income. At the contrary, employees having less information go for the defined benefit plan.

Gender: The gender also plays a vital role in the life of the employees to choose their

superannuation fund. It is often observed that women have more risk than men and hence

they choose high risk investment plan if they fetch higher interest. Women have a habit of

saving and hence are seen to be choosing a plan that involves lesser risk. However, this may

also vary on various factors like how they are in their personal as well as professional life.

Sense of Security: There are people who don’t want to take a lot of risk and hence want to

stay secured. It has been seen that such people usually opt defined benefit plan as there is risk

and uncertainty attached with the investment choice plans. The investment choice plan on the

contrary depends on the movement of the market and hence the sense of security is put at

stake (Review, 2015).

No matter there are many constraints and factors that one has for the investment, it also

depends on the personal life and interest of the employees as well (Lin, MacMinn, and Tian,

2015).

Issues relating to the concept of the time value of money, taxes etc., might be important

in this decision-making process

Time value of money and taxes in an economy are also important factors that play a role in

the investment choice plan or defined benefit plan in superannuation investment (Kio, 2015).

However, tax deduction is the key imperative factor for the employees who are having high

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount of income in their invested capital. Nonetheless, the benefit of tax deduction is

calculated as per the defined benefit plan considering many factors including the age of the

employee at the retirement, salary and years of service of the employee and applicable rule

and regulation for the investment purpose. These factors are discussed below:

Taxes: Taxation is a system that lets the people of the economy pay a certain amount to the

government on their income, be it any benefit they get on the retirement. There are

exceptions as well where no taxes are to be paid to the employees on the retirement benefit

they get ("Let the voluntary sector help", 2012). This includes the incapacity of employees to

perform, or the death of the employee and many more. In all the other situations, the tax is

always deducted on the retirement benefit paid to the employees. In defined benefit plan, the

tax is limited to the benefit which is limited to the contribution of the employee accumulated

for the working tenure (Krishnan, Cumbie, and Ice, 2017)

But, in the investment choice plan, the amount contributed in the plan is invested by the

employee in a portfolio. This keeps on adding to the fund in terms of interest. Thus, tax is to

be paid as a contribution on the income earned by the investment and the interest. Due to this,

many choose defined benefit plan (Kaiako pono, 2010).

Time value of money: It is the capability of money to raise its value so that its future worth

is more. This is because the value of rupee today is more than the future as there is inflation

and hence the value drops. Thus, the investment today has to compensate the fall of value.

Therefore, investment choice plan is a good idea as it increases the value of superannuation

fund (Cohen, 2013). However, defined benefit plan leads to stagnancy of the amount and no

benefit added. This is the imperative factor to assess the value on the invested capital and

helps investors to assess the present value of the cash inflow which they will receive after a

certain period of time (Cobb, 2015).

Recommendation/Conclusion

This concludes that the development of any economy is judged by the efficient shift it gets

from the different sectors like primary and secondary to the tertiary. Thus, to motivate

employees to get into this sector, it is important that they get certain benefits that help them

incline towards working in this sector (Chomik and Piggott, 2016). The investors have to

choose only those options that get them better value for their money. Now in the end, it could

be inferred that defined benefit plan is the best suitable option for the tertiary employees to

calculated as per the defined benefit plan considering many factors including the age of the

employee at the retirement, salary and years of service of the employee and applicable rule

and regulation for the investment purpose. These factors are discussed below:

Taxes: Taxation is a system that lets the people of the economy pay a certain amount to the

government on their income, be it any benefit they get on the retirement. There are

exceptions as well where no taxes are to be paid to the employees on the retirement benefit

they get ("Let the voluntary sector help", 2012). This includes the incapacity of employees to

perform, or the death of the employee and many more. In all the other situations, the tax is

always deducted on the retirement benefit paid to the employees. In defined benefit plan, the

tax is limited to the benefit which is limited to the contribution of the employee accumulated

for the working tenure (Krishnan, Cumbie, and Ice, 2017)

But, in the investment choice plan, the amount contributed in the plan is invested by the

employee in a portfolio. This keeps on adding to the fund in terms of interest. Thus, tax is to

be paid as a contribution on the income earned by the investment and the interest. Due to this,

many choose defined benefit plan (Kaiako pono, 2010).

Time value of money: It is the capability of money to raise its value so that its future worth

is more. This is because the value of rupee today is more than the future as there is inflation

and hence the value drops. Thus, the investment today has to compensate the fall of value.

Therefore, investment choice plan is a good idea as it increases the value of superannuation

fund (Cohen, 2013). However, defined benefit plan leads to stagnancy of the amount and no

benefit added. This is the imperative factor to assess the value on the invested capital and

helps investors to assess the present value of the cash inflow which they will receive after a

certain period of time (Cobb, 2015).

Recommendation/Conclusion

This concludes that the development of any economy is judged by the efficient shift it gets

from the different sectors like primary and secondary to the tertiary. Thus, to motivate

employees to get into this sector, it is important that they get certain benefits that help them

incline towards working in this sector (Chomik and Piggott, 2016). The investors have to

choose only those options that get them better value for their money. Now in the end, it could

be inferred that defined benefit plan is the best suitable option for the tertiary employees to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

create value on their investment. It helps to develop consistent investment habit out of their

earned salary. Nonetheless, tertiary sector employees who are having high amount of

income in their business process should be more indulged in taking the investment options

which will give them higher amount of tax deduction.

earned salary. Nonetheless, tertiary sector employees who are having high amount of

income in their business process should be more indulged in taking the investment options

which will give them higher amount of tax deduction.

References

Ako Aotearoa. (2010). Kaiako pono. 2nd ed, Wellington: [N.Z.].

Bae, S. U., Hur, H., Min, B. S., Baik, S. H., Lee, K. Y., and Kim, N. K. (2018). Which

Patients with Isolated Para-aortic Lymph Node Metastasis Will Truly Benefit from Extended

Lymph Node Dissection for Colon Cancer?. Cancer research and treatment: official journal

of Korean Cancer Association, 50(3), 712.

Chomik, R., and Piggott, J. (2016). Australian Superannuation: The Current State of Play.

Australian Economic Review, 49(4), 483-493.

Cobb, J. A. (2015). Risky business: The decline of defined benefit pensions and firms’

shifting of risk. Organization Science, 26(5), 1332-1350.

Cohen, M. (2013). Superannuation retirement balances: A surprising outcome. Australasian

Journal on Ageing, 33(4), E41-E45.

Josa-Fombellida, R., López-Casado, P., and Rincón-Zapatero, J. P. (2018). Portfolio

optimization in a defined benefit pension plan where the risky assets are processes with

constant elasticity of variance. Insurance: Mathematics and Economics, 82, 73-86.

Kio, S. (2015). Extending social networking into the secondary education sector. British

Journal of Educational Technology, 47(4), 721-733.

Korzynski, P. (2013). Employee motivation in new working environment. International

Journal Of Academic Research, 5(5), 184-188.

Krishnan, V. S., Cumbie, J., and Ice, R. (2017). Defined benefit plans vs. defined

contribution plans: An evaluation framework using random returns. 47(4), 721-733

Lee, J., Chen, Y. J., Wu, M. H., Chang, C. L., Chen, T. C., Chen, J. R., and Yang, Y. C.

(2017). PO-0712: Benefit of semi-extended field radiotherapy in patients with locally

advanced cervical cancer. Radiotherapy and Oncology, 123, S373-S374.

Let the voluntary sector help. (2012). Primary Health Care, 22(6), 3-3.

Ako Aotearoa. (2010). Kaiako pono. 2nd ed, Wellington: [N.Z.].

Bae, S. U., Hur, H., Min, B. S., Baik, S. H., Lee, K. Y., and Kim, N. K. (2018). Which

Patients with Isolated Para-aortic Lymph Node Metastasis Will Truly Benefit from Extended

Lymph Node Dissection for Colon Cancer?. Cancer research and treatment: official journal

of Korean Cancer Association, 50(3), 712.

Chomik, R., and Piggott, J. (2016). Australian Superannuation: The Current State of Play.

Australian Economic Review, 49(4), 483-493.

Cobb, J. A. (2015). Risky business: The decline of defined benefit pensions and firms’

shifting of risk. Organization Science, 26(5), 1332-1350.

Cohen, M. (2013). Superannuation retirement balances: A surprising outcome. Australasian

Journal on Ageing, 33(4), E41-E45.

Josa-Fombellida, R., López-Casado, P., and Rincón-Zapatero, J. P. (2018). Portfolio

optimization in a defined benefit pension plan where the risky assets are processes with

constant elasticity of variance. Insurance: Mathematics and Economics, 82, 73-86.

Kio, S. (2015). Extending social networking into the secondary education sector. British

Journal of Educational Technology, 47(4), 721-733.

Korzynski, P. (2013). Employee motivation in new working environment. International

Journal Of Academic Research, 5(5), 184-188.

Krishnan, V. S., Cumbie, J., and Ice, R. (2017). Defined benefit plans vs. defined

contribution plans: An evaluation framework using random returns. 47(4), 721-733

Lee, J., Chen, Y. J., Wu, M. H., Chang, C. L., Chen, T. C., Chen, J. R., and Yang, Y. C.

(2017). PO-0712: Benefit of semi-extended field radiotherapy in patients with locally

advanced cervical cancer. Radiotherapy and Oncology, 123, S373-S374.

Let the voluntary sector help. (2012). Primary Health Care, 22(6), 3-3.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lin, Y., MacMinn, R. D., and Tian, R. (2015). De-risking defined benefit plans. Insurance:

Mathematics and Economics, 63, 52-65.

Review, T. (2015). Tax Review. Pittsburgh Tax Review, Journal of tax deduction 12(2).

Ryland, P. (2010). Investment. Superannuation retirement balances: A surprising outcome.

47(4), 721-733

Serrasqueiro, Z. (2016). Investment determinants: high-investment versus low-investment

Portuguese SMEs. Investment Analysts Journal, 46(1), 1-16.

Vilkinas, T. (2014). Leadership provided by non-academic middle-level managers in the

Australian higher education sector: the enablers. Tertiary Education and Management, 20(4),

320-338.

Yen, T. C., Lai, C. H., Ma, S. Y., Huang, K. G., Huang, H. J., Hong, J. H., ... and Chang, T.

C. (2016). Comparative benefits and limitations of 18 F-FDG PET and CT-MRI in

documented or suspected recurrent cervical cancer. European journal of nuclear medicine

and molecular imaging, 33(12), 1399-1407.

Defined benefit plan, 2019, details and comparison available at

http://fsi.gov.au/publications/interim-report/04-superannuation/efficiency/ accessed on 20.05.2019

Mathematics and Economics, 63, 52-65.

Review, T. (2015). Tax Review. Pittsburgh Tax Review, Journal of tax deduction 12(2).

Ryland, P. (2010). Investment. Superannuation retirement balances: A surprising outcome.

47(4), 721-733

Serrasqueiro, Z. (2016). Investment determinants: high-investment versus low-investment

Portuguese SMEs. Investment Analysts Journal, 46(1), 1-16.

Vilkinas, T. (2014). Leadership provided by non-academic middle-level managers in the

Australian higher education sector: the enablers. Tertiary Education and Management, 20(4),

320-338.

Yen, T. C., Lai, C. H., Ma, S. Y., Huang, K. G., Huang, H. J., Hong, J. H., ... and Chang, T.

C. (2016). Comparative benefits and limitations of 18 F-FDG PET and CT-MRI in

documented or suspected recurrent cervical cancer. European journal of nuclear medicine

and molecular imaging, 33(12), 1399-1407.

Defined benefit plan, 2019, details and comparison available at

http://fsi.gov.au/publications/interim-report/04-superannuation/efficiency/ accessed on 20.05.2019

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.