Managerial Finance: Dell Inc. Plant Project Evaluation Report - ACC511

VerifiedAdded on 2022/11/23

|14

|1925

|492

Report

AI Summary

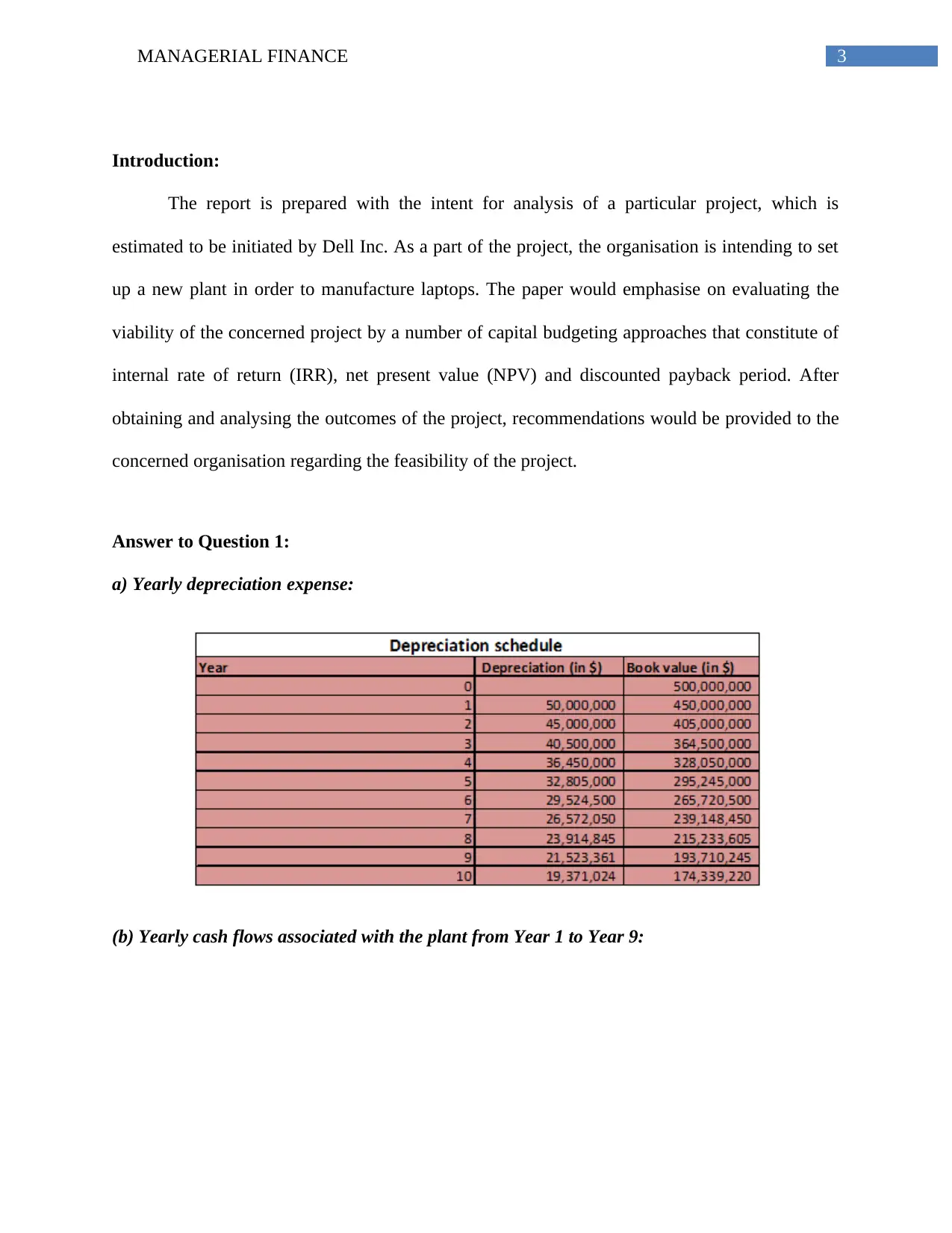

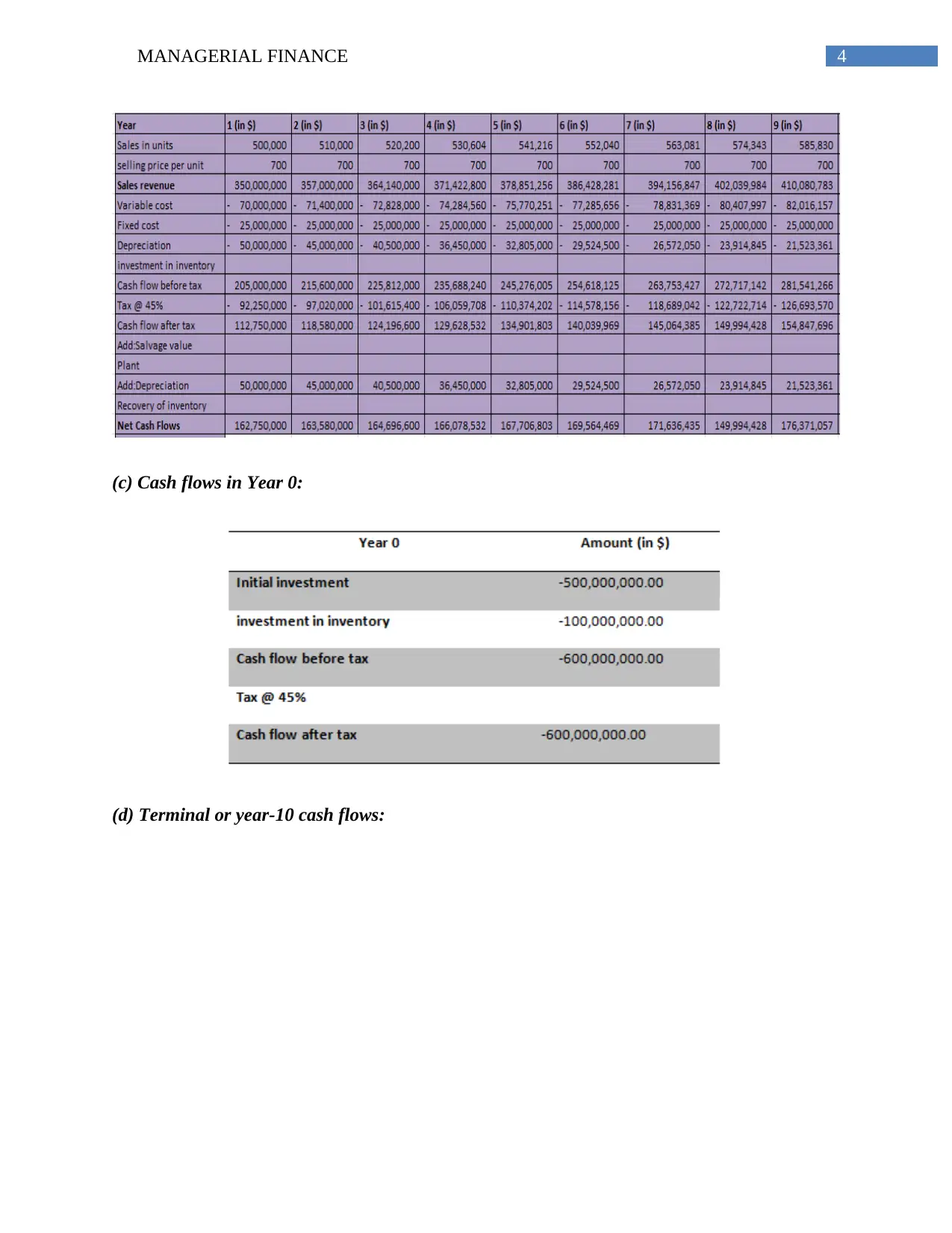

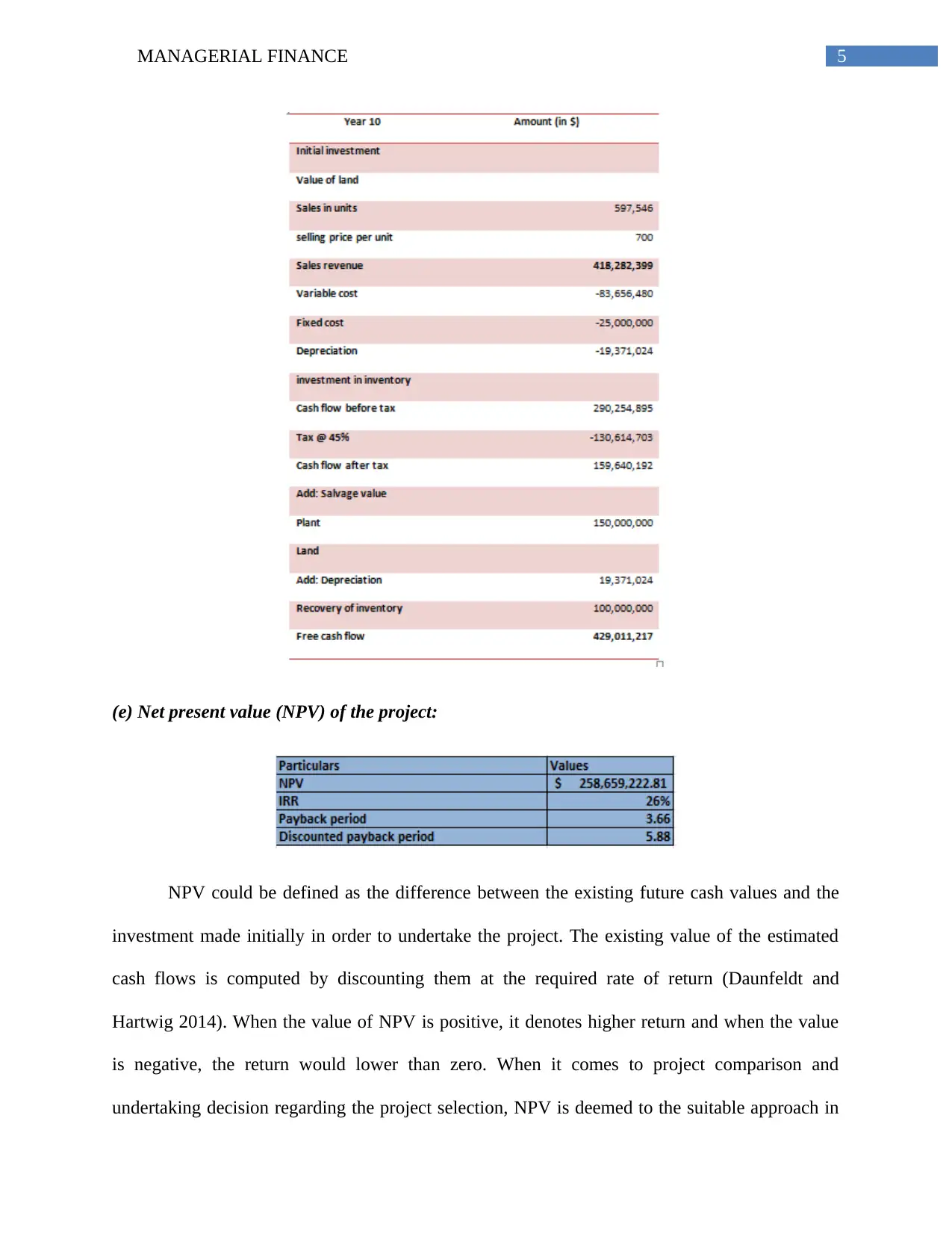

This report evaluates a proposed project for Dell Inc., specifically the establishment of a new laptop manufacturing plant. The analysis employs capital budgeting techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), and payback period, to assess the project's financial viability. The report calculates yearly depreciation, cash flows, and terminal values to determine the project's profitability. The NPV is found to be positive, the IRR exceeds the cost of capital, and the payback period is within the economic life of the project, suggesting that the project is acceptable. The report also emphasizes the importance of using risk-adjusted discount rates, rather than a uniform rate, for different projects. The report also addresses the financial aspects of securing a bank loan and the potential pros and cons associated with it. The conclusion recommends that Dell Inc. proceed with the project, while also considering the specific risks associated with the project when setting the discount rate.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.