Financial Analysis Report: Dell's Laptop Manufacturing Plant Project

VerifiedAdded on 2023/03/17

|8

|1340

|66

Report

AI Summary

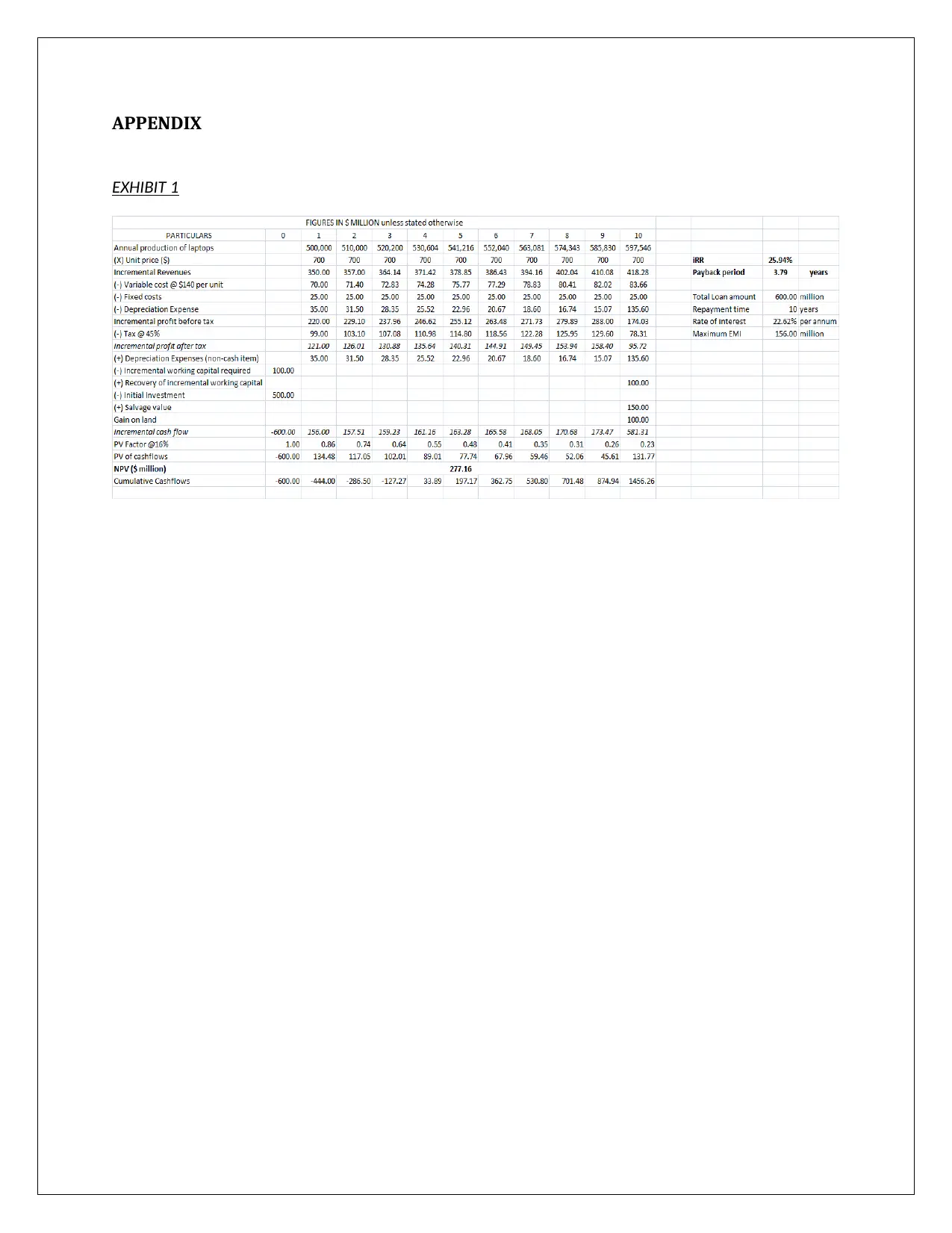

This report presents a comprehensive financial analysis of Dell's proposed laptop manufacturing plant, evaluating its feasibility using capital budgeting techniques. The analysis includes calculations of depreciation, cash flows, Net Present Value (NPV), Internal Rate of Return (IRR), and payback period. The report assesses the project's viability under different scenarios, including the impact of debt financing and interest rates. It also examines the company's policy of using a uniform cost of capital across all projects, highlighting its potential shortcomings. Furthermore, the report considers the implications of a new requirement that project inflows should service debt repayments. The findings indicate that the project is financially viable, provided the interest rate on borrowing does not exceed a certain threshold. The report concludes with recommendations for the company, emphasizing the need for a risk-adjusted cost of capital and flexibility in project selection.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.