Management Accounting Systems and Reporting for Business Decisions

VerifiedAdded on 2023/01/09

|15

|3786

|66

Report

AI Summary

This report offers a comprehensive analysis of management accounting, focusing on its principles, systems, and practical applications within Dell Inc. The introduction defines management accounting and distinguishes it from financial accounting, highlighting its role in providing financial and non-financial details for internal decision-making. The report then delves into the specifics of management accounting systems, including job costing, inventory management, and price optimization systems. Furthermore, the report examines the use of management accounting reporting, such as budget reports, accounts receivables, job cost reports, and inventory reports, providing insights into how these reports aid in organizational control, planning, and decision-making. The analysis includes the distinct roles of management accounting users like top-level management and policy makers. The report emphasizes how Dell Inc. can leverage management accounting for effective financial and operational management. Overall, the report provides a valuable understanding of how management accounting supports strategic planning and operational efficiency within a business context, using Dell Inc. as a case study.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting ............................................................................................................3

TASK 2............................................................................................................................................5

Management accounting system and its internal systems ..........................................................5

TASK 3............................................................................................................................................6

Use of management accounting reporting...................................................................................6

TASK 4............................................................................................................................................8

Definition and calculations ........................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting ............................................................................................................3

TASK 2............................................................................................................................................5

Management accounting system and its internal systems ..........................................................5

TASK 3............................................................................................................................................6

Use of management accounting reporting...................................................................................6

TASK 4............................................................................................................................................8

Definition and calculations ........................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

There are a number of accounting approaches in financing that are being applied in their

activities by company organizations. The word Management Accounting (MA) may be explained

as a kind of accounting methodology by providing financial and non - financial details in which

internal reports are generated. This method is commonly used for businesses engaged in

industrial operations. The project report is based on Dell incorporation which operates its

operations in the process of making personal computers. This company is a leading in the aspect

of computer manufacturing and selling. In current time company is facing issue which is that

they are unable to know whether they should personal computers or not. For this purpose,

different types of tasks are covered under project report. The report covers information about

Management accounting systems (MAS), reports as well as some calculations are also carried

out.

TASK 1

Management accounting

Definition of MA:

MA is also known as systematic accounting which can be described as a method of supplying the

managers with financial details which resources while making decisions. MA is utilized

primarily by the organization’s management department, so that is the one aspect that renders it

distinct from financial reporting (Azudin and Mansor, 2018 ). Through this phase, tax

information and documentation including payroll, annual balance sheets are exchanged with the

management team committee by operational budget. This accounting approach is completely

different from financial accounting (FA) due to serval reasons which are mentioned further. It

can be applied in the Dell computer corporation so that they manage their financial and non-

financial information in a systematic manner.

How MA is distinct with FA.

There is numerous variation between both accounting methods because each of them is being

applied in a specific manner in operations of companies. Below difference between both

accounting is mentioned in such manner:

Basis MA FA

Information Under this form of accounting, In FA, only those transactions’

There are a number of accounting approaches in financing that are being applied in their

activities by company organizations. The word Management Accounting (MA) may be explained

as a kind of accounting methodology by providing financial and non - financial details in which

internal reports are generated. This method is commonly used for businesses engaged in

industrial operations. The project report is based on Dell incorporation which operates its

operations in the process of making personal computers. This company is a leading in the aspect

of computer manufacturing and selling. In current time company is facing issue which is that

they are unable to know whether they should personal computers or not. For this purpose,

different types of tasks are covered under project report. The report covers information about

Management accounting systems (MAS), reports as well as some calculations are also carried

out.

TASK 1

Management accounting

Definition of MA:

MA is also known as systematic accounting which can be described as a method of supplying the

managers with financial details which resources while making decisions. MA is utilized

primarily by the organization’s management department, so that is the one aspect that renders it

distinct from financial reporting (Azudin and Mansor, 2018 ). Through this phase, tax

information and documentation including payroll, annual balance sheets are exchanged with the

management team committee by operational budget. This accounting approach is completely

different from financial accounting (FA) due to serval reasons which are mentioned further. It

can be applied in the Dell computer corporation so that they manage their financial and non-

financial information in a systematic manner.

How MA is distinct with FA.

There is numerous variation between both accounting methods because each of them is being

applied in a specific manner in operations of companies. Below difference between both

accounting is mentioned in such manner:

Basis MA FA

Information Under this form of accounting, In FA, only those transactions’

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

included information about monetary and

non-monetary transactions are

included.

information is contained which is

related to monetary transactions.

Compulsory This accounting is not essential for

companies to implement even they

are listed in any stock exchange.

FA is mandatory for those companies

which are listed in any specific stock

exchange.

Outcome In MA, internal reports are

produced in accordance of need of

business.

Under FA, various types of financial

statements are prepared including

P&L, balance sheet etc.

Auditing It is not essential that internal

reports produced under this

accounting need to be audited.

While in this accounting, it is

necessary to do auditing of prepared

financial statement before presenting

to stakeholders.

Users of MA information:

As per the above discussion, this can be inferred that MA is mainly useful for internal

stakeholders because they utilize key information form it. Below some key users of this

accounting are mentioned in such manner:

Management department- In a particular company, management department is one of the

key department whose responsibility is to manage all tasks and activities in an effective

manner. In order to do so they need key information which can be derived via internal

reports produced under MA. In the context of Dell company, they use this information for

better decision making.

Top level management- the management accounting is also used by the top level people

of management for taking the correct and right future decisions for the company (Bedford

and Speklé, 2018). The management accounting contains the financial information about

the company, the top level people review these information and data and then they

evaluates the financial and management soundness of the businesses.

Policy makers: The people who forms the policies or rules for the organisation also needs

the management accounting information. In this actual information and the statistical data

is been analysed and evaluated by these people so that they can make the objectives and

goals for the company in a appropriate manner.

non-monetary transactions are

included.

information is contained which is

related to monetary transactions.

Compulsory This accounting is not essential for

companies to implement even they

are listed in any stock exchange.

FA is mandatory for those companies

which are listed in any specific stock

exchange.

Outcome In MA, internal reports are

produced in accordance of need of

business.

Under FA, various types of financial

statements are prepared including

P&L, balance sheet etc.

Auditing It is not essential that internal

reports produced under this

accounting need to be audited.

While in this accounting, it is

necessary to do auditing of prepared

financial statement before presenting

to stakeholders.

Users of MA information:

As per the above discussion, this can be inferred that MA is mainly useful for internal

stakeholders because they utilize key information form it. Below some key users of this

accounting are mentioned in such manner:

Management department- In a particular company, management department is one of the

key department whose responsibility is to manage all tasks and activities in an effective

manner. In order to do so they need key information which can be derived via internal

reports produced under MA. In the context of Dell company, they use this information for

better decision making.

Top level management- the management accounting is also used by the top level people

of management for taking the correct and right future decisions for the company (Bedford

and Speklé, 2018). The management accounting contains the financial information about

the company, the top level people review these information and data and then they

evaluates the financial and management soundness of the businesses.

Policy makers: The people who forms the policies or rules for the organisation also needs

the management accounting information. In this actual information and the statistical data

is been analysed and evaluated by these people so that they can make the objectives and

goals for the company in a appropriate manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Management accounting system and its internal systems

Management accounting consists of company's internal financial information which been

used by the managers so that they can make the good future decisions about the company. These

management accounting information can only be used by the internal team of the company, this

factor makes management accounting system very much different from the financial accounting.

Through the information or statistical data provided to the internal team, they analyse and

evaluate it so that they can make the future decision accordingly. Through these information or

data the organisation can better control there operations, make the appropriate plans and keep the

actions or work at the desired directions. Management accounting system involves many other

systems like:

Job costing systems: In job accounting system the organisation estimates the cost which is

related to a specific work or job. In this the cost get accumulate which can get incurred in the

performance of a particular activity. This would help the organisation in knowing the cost which

this particular activity would going to take. For example, in the case with Dell company, the

organisation can estimate the cost for the activities which they are conducting. The separate cost

can get incurred for production activity (Botes and Sharma, 2017). In that cost the organisation

can evaluate the total cost which the company is incurring in the production activity. If the

company believes that too much cost is getting in their production department or activity, then

they will analyse the department activities and take out the areas where they can reduce the costs.

Inventory management systems: In inventory management system, there is a full record about

inventories about the stocks available with the company. It is the combination of technology in

which the organisation stores and saves the information about the inventories. Such technology is

very much useful for the organisation as it helps it having easy maintenance for the same. In the

company dell, the inventory management system has been used in maintaining the stocks or the

inventory which the company has with itself. These information may include the number for

finished goods, unfinished goods, raw materials which the company has, orders in process in the

like. Through this information the company can make the corrective decisions about the

inventory. This would also enable the company, Dell, in taking the corrective measures and

actions in regard with inventories. Through the adoption of inventory system the company, Dell,

can forecast about their inventory, it will also help in making the better decisions about the

Management accounting system and its internal systems

Management accounting consists of company's internal financial information which been

used by the managers so that they can make the good future decisions about the company. These

management accounting information can only be used by the internal team of the company, this

factor makes management accounting system very much different from the financial accounting.

Through the information or statistical data provided to the internal team, they analyse and

evaluate it so that they can make the future decision accordingly. Through these information or

data the organisation can better control there operations, make the appropriate plans and keep the

actions or work at the desired directions. Management accounting system involves many other

systems like:

Job costing systems: In job accounting system the organisation estimates the cost which is

related to a specific work or job. In this the cost get accumulate which can get incurred in the

performance of a particular activity. This would help the organisation in knowing the cost which

this particular activity would going to take. For example, in the case with Dell company, the

organisation can estimate the cost for the activities which they are conducting. The separate cost

can get incurred for production activity (Botes and Sharma, 2017). In that cost the organisation

can evaluate the total cost which the company is incurring in the production activity. If the

company believes that too much cost is getting in their production department or activity, then

they will analyse the department activities and take out the areas where they can reduce the costs.

Inventory management systems: In inventory management system, there is a full record about

inventories about the stocks available with the company. It is the combination of technology in

which the organisation stores and saves the information about the inventories. Such technology is

very much useful for the organisation as it helps it having easy maintenance for the same. In the

company dell, the inventory management system has been used in maintaining the stocks or the

inventory which the company has with itself. These information may include the number for

finished goods, unfinished goods, raw materials which the company has, orders in process in the

like. Through this information the company can make the corrective decisions about the

inventory. This would also enable the company, Dell, in taking the corrective measures and

actions in regard with inventories. Through the adoption of inventory system the company, Dell,

can forecast about their inventory, it will also help in making the better decisions about the

inventories, it will increases the transparency into the operations which would increase the

reliability. Apart from this, the inventory management system also helps the Dell company in

maintaining a good relationship with suppliers, vendors, other partners and so on. Through this

system the organisation can easily have a track upon their inventories, suppliers, deliveries and

the like. The company from this can keep an record about where the product has been delivered

and at what time. This will reduce the chances for dislocating or lost of a product. Inventory

management system would also enable the company in satisfying the needs for the customers in

a more effective manner by providing the products to them at time and having the proper

availability of the same.

Price optimisation system: The price optimisation system is the mathematical program which

analyse the demand of the customers at various prices. It has been said that the demand of the

commodity increases when the price for the same gets decrease, it theory applies to normal

goods. This system enables the organisation in predicting the demand into the targeted market

when the company would be setting a specified price for the product. As in the case with Dell,

the company in predicting the demand for their products they they sells their products at a

specified prices (Järvinen, 2016). This technique is very helpful for the company as it enables the

company in tailoring its price or the cost for the offered product according to the targeted group

or customers. In this system the Dell company makes the correct decisions regrading the prices

for the product which they are offering to their customers.

TASK 3

Use of management accounting reporting

Organisation has various types of accounting reporting and some of them are as follows:

Budget report: The budget report is the report through which the actual performance is

compared with the budget which is set as projections. These budget help in assuring that the

present performance or the actions are going in relation with the projected budget. These budgets

are prepared so that the organisation can make the assumptions about the resources which they

would be needing during the project or financial year. These reports are related with the

financials of the organisation, it can be possible for them that the projected assumptions can get

differ from the actual performance (Lachmann, Trapp and Trapp, 2017). But the company should

reliability. Apart from this, the inventory management system also helps the Dell company in

maintaining a good relationship with suppliers, vendors, other partners and so on. Through this

system the organisation can easily have a track upon their inventories, suppliers, deliveries and

the like. The company from this can keep an record about where the product has been delivered

and at what time. This will reduce the chances for dislocating or lost of a product. Inventory

management system would also enable the company in satisfying the needs for the customers in

a more effective manner by providing the products to them at time and having the proper

availability of the same.

Price optimisation system: The price optimisation system is the mathematical program which

analyse the demand of the customers at various prices. It has been said that the demand of the

commodity increases when the price for the same gets decrease, it theory applies to normal

goods. This system enables the organisation in predicting the demand into the targeted market

when the company would be setting a specified price for the product. As in the case with Dell,

the company in predicting the demand for their products they they sells their products at a

specified prices (Järvinen, 2016). This technique is very helpful for the company as it enables the

company in tailoring its price or the cost for the offered product according to the targeted group

or customers. In this system the Dell company makes the correct decisions regrading the prices

for the product which they are offering to their customers.

TASK 3

Use of management accounting reporting

Organisation has various types of accounting reporting and some of them are as follows:

Budget report: The budget report is the report through which the actual performance is

compared with the budget which is set as projections. These budget help in assuring that the

present performance or the actions are going in relation with the projected budget. These budgets

are prepared so that the organisation can make the assumptions about the resources which they

would be needing during the project or financial year. These reports are related with the

financials of the organisation, it can be possible for them that the projected assumptions can get

differ from the actual performance (Lachmann, Trapp and Trapp, 2017). But the company should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

try to bring up their operations within that specific budget set. This also enable the organisation

in reviewing the cost. The budget report has these following four things and these are as:

Budget: These refers to the budget in which prepared by the organisation at the starting of the

period. In this the company by taking the past trends and current objectives projects the budget

for this particular period.

Actual: The this actual factor the business puts the actual cost which it has incurred from its

operations.

Over budget: In this over budget column, the difference between the budget and actual budget is

been specified. How much amount the actual budget is greater than the specified budgets.

Percentage of budget: This column will tell about the how much percentage the budgets has

been utilised.

Every department prepare its own budgets according to the activities they are performing. Then

these budgets get presented later to the top level management and then get discussed.

Account receivables: Account receivables refers to the amount of invoices which the

organisation has not received from the customers. These are the amount for which the customers

are yet to pay (Leotta, Rizza and Ruggeri, 2017). The account receivables are shown at the asset

side for the balance sheet. These are taken as an asset as its amount is owned by the company

itself. These come into the category of current assets as they converts in cash within a year and

so. They are the legally forcible claims which the company can take from the customers. The

company's accountant keeps the record for the amount which are related with account

receivables. These receivables also increases the company's liquidity which is very much

beneficial for the company to meet the demand for cash.

Job cost report: The job cost report is the report which is concerning about the cost about which

has incurred in performing a particular job. The organisation has to perform all the activities and

to perform the activities, the organisation incurred the cost for performing it. The job cost report

helps the company in ascertaining the cost which has spend in performing a particular task. In

this report the organisation can watch the status about how much amount has been spent and how

much has been taken as a the budget. Through this the company has ascertain and compare the

cost for performing the activity. If the cost for performing the activity is above the stated budget

than the controlling actions must be taken by the company and bring the cost to a projected

amount.

in reviewing the cost. The budget report has these following four things and these are as:

Budget: These refers to the budget in which prepared by the organisation at the starting of the

period. In this the company by taking the past trends and current objectives projects the budget

for this particular period.

Actual: The this actual factor the business puts the actual cost which it has incurred from its

operations.

Over budget: In this over budget column, the difference between the budget and actual budget is

been specified. How much amount the actual budget is greater than the specified budgets.

Percentage of budget: This column will tell about the how much percentage the budgets has

been utilised.

Every department prepare its own budgets according to the activities they are performing. Then

these budgets get presented later to the top level management and then get discussed.

Account receivables: Account receivables refers to the amount of invoices which the

organisation has not received from the customers. These are the amount for which the customers

are yet to pay (Leotta, Rizza and Ruggeri, 2017). The account receivables are shown at the asset

side for the balance sheet. These are taken as an asset as its amount is owned by the company

itself. These come into the category of current assets as they converts in cash within a year and

so. They are the legally forcible claims which the company can take from the customers. The

company's accountant keeps the record for the amount which are related with account

receivables. These receivables also increases the company's liquidity which is very much

beneficial for the company to meet the demand for cash.

Job cost report: The job cost report is the report which is concerning about the cost about which

has incurred in performing a particular job. The organisation has to perform all the activities and

to perform the activities, the organisation incurred the cost for performing it. The job cost report

helps the company in ascertaining the cost which has spend in performing a particular task. In

this report the organisation can watch the status about how much amount has been spent and how

much has been taken as a the budget. Through this the company has ascertain and compare the

cost for performing the activity. If the cost for performing the activity is above the stated budget

than the controlling actions must be taken by the company and bring the cost to a projected

amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory report: In this report the organisation prepares the report about the inventory which

they have with them. The report tell the department about the current status with regard to

inventory. So that they can take the decisions making accordingly. As in the case with Dell

company the organisation through the inventory report would get to know about the transaction

which has been done yet by the company, the amount of inventory which has been stored into the

warehouse, the goods or products that are in work in progress category and so on (Malina, 2017).

From this the company can analyse the area or activity which is over loading and which has

shortages.

The company uses all these budgets into their structures or processes. Dell performs the

inventory budget to analyse the activities related to inventories, the job cost report in which the

dell company analyse the cost incurred by performing a particular job so and take the corrective

measures when the company thinks that the cost expenditure is greater than the projected amount

(Mokhtar and et. al., 2016). Dell company also maintains the account receivables in which they

sells the products to the customers in the view to receive the amount in the future.

TASK 4

Definition and calculations

Direct materials: Direct materials are the materials which are brought by the company to

make or complete their finished product. The Materials which have been brought by the

company does not used into the production process, rather it directly gets attached to the main

project to finish the actual product. All these are the tangible products which the company

brought up from the other company or party and then they attached or use it in making the

finished product. Dell company purchases the RAM and software from intell and microsoft, here

the company has buy the raw materials i.e. RAM and software to make a finished product which

is laptop (Nørreklit, 2017). The company goes for direct materials because they lack in

producing all these products or materials by themselves. Though purchasing the product or raw

material from other party adds up to the cost for company but a single company cannot produces

all the things or materials by itself.

Direct labour: It refers to the cost which is associated with the wages or salaries of the

labour that works for production department. The cost for the labour is directly added to the total

they have with them. The report tell the department about the current status with regard to

inventory. So that they can take the decisions making accordingly. As in the case with Dell

company the organisation through the inventory report would get to know about the transaction

which has been done yet by the company, the amount of inventory which has been stored into the

warehouse, the goods or products that are in work in progress category and so on (Malina, 2017).

From this the company can analyse the area or activity which is over loading and which has

shortages.

The company uses all these budgets into their structures or processes. Dell performs the

inventory budget to analyse the activities related to inventories, the job cost report in which the

dell company analyse the cost incurred by performing a particular job so and take the corrective

measures when the company thinks that the cost expenditure is greater than the projected amount

(Mokhtar and et. al., 2016). Dell company also maintains the account receivables in which they

sells the products to the customers in the view to receive the amount in the future.

TASK 4

Definition and calculations

Direct materials: Direct materials are the materials which are brought by the company to

make or complete their finished product. The Materials which have been brought by the

company does not used into the production process, rather it directly gets attached to the main

project to finish the actual product. All these are the tangible products which the company

brought up from the other company or party and then they attached or use it in making the

finished product. Dell company purchases the RAM and software from intell and microsoft, here

the company has buy the raw materials i.e. RAM and software to make a finished product which

is laptop (Nørreklit, 2017). The company goes for direct materials because they lack in

producing all these products or materials by themselves. Though purchasing the product or raw

material from other party adds up to the cost for company but a single company cannot produces

all the things or materials by itself.

Direct labour: It refers to the cost which is associated with the wages or salaries of the

labour that works for production department. The cost for the labour is directly added to the total

cost. If the work performed by an employee is nit related to the production activity then it would

be considered under the indirect cost head. Some companies calculate the cost through:

Hourly basis : In which the total hour a worker as work gets taken account and then cost is

calculated.

Days basis : In this the organisation calculates the cost for labour on the bases of days he has

worked (Nuhu, Baird and Appuhamilage, 2017).

Unit produced: In this the company calculates the cost for labour according to the unit he has

produced.

The company dell follows the day basis in which the organisation gives the wages or the

salaries to their employees on the basis of days they have worked.

Direct overhead: These are the cost which gets incurred during the process of

production such as electricity, space for carrying out the production activity, water, and the like.

All such costs do get adds up in the calculation of total costs. These cost are very much stable

and constant as they does not get change with any change into the volume of production

outcomes.

Fixed overhead: Fixed overheads are the costs which are stable and constant to the

company (Otley, 2016). There cost are very much stable irrespective to the level for production.

Some of these costs are rent, depreciation caused to the fixed assets, salaries to the production

managers, supervisors, amount specified as insurances, taxes and so on. These are the cost which

are fixed for the company. Dell company have to pay for these cost irrespective to the volume of

their production.

Product cost: The cost which get into the production of the product is known as Product

cost. The product costs include the cost for materials, labour costs, costs for factory overhead and

so on. The actual selling price of a product can only get ascertain after adding up all the cost

associated in producing one unit of product. After adding up all the costs, the actual selling price

of a product is ascertain. The after sales services which the company provides to the customers

also get included into the product cost. The product cost gets included into the financial

statements under the head of manufacturing overheads.

Period cost: They are the cost which are indirect in nature as they are not related to the

production activity (Qian, Hörisch and Schaltegger, 2018). They are shown in the income

be considered under the indirect cost head. Some companies calculate the cost through:

Hourly basis : In which the total hour a worker as work gets taken account and then cost is

calculated.

Days basis : In this the organisation calculates the cost for labour on the bases of days he has

worked (Nuhu, Baird and Appuhamilage, 2017).

Unit produced: In this the company calculates the cost for labour according to the unit he has

produced.

The company dell follows the day basis in which the organisation gives the wages or the

salaries to their employees on the basis of days they have worked.

Direct overhead: These are the cost which gets incurred during the process of

production such as electricity, space for carrying out the production activity, water, and the like.

All such costs do get adds up in the calculation of total costs. These cost are very much stable

and constant as they does not get change with any change into the volume of production

outcomes.

Fixed overhead: Fixed overheads are the costs which are stable and constant to the

company (Otley, 2016). There cost are very much stable irrespective to the level for production.

Some of these costs are rent, depreciation caused to the fixed assets, salaries to the production

managers, supervisors, amount specified as insurances, taxes and so on. These are the cost which

are fixed for the company. Dell company have to pay for these cost irrespective to the volume of

their production.

Product cost: The cost which get into the production of the product is known as Product

cost. The product costs include the cost for materials, labour costs, costs for factory overhead and

so on. The actual selling price of a product can only get ascertain after adding up all the cost

associated in producing one unit of product. After adding up all the costs, the actual selling price

of a product is ascertain. The after sales services which the company provides to the customers

also get included into the product cost. The product cost gets included into the financial

statements under the head of manufacturing overheads.

Period cost: They are the cost which are indirect in nature as they are not related to the

production activity (Qian, Hörisch and Schaltegger, 2018). They are shown in the income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statements of the company for that particular accounting period. Some of the examples may

include marketing expenses, selling expenses and etc.

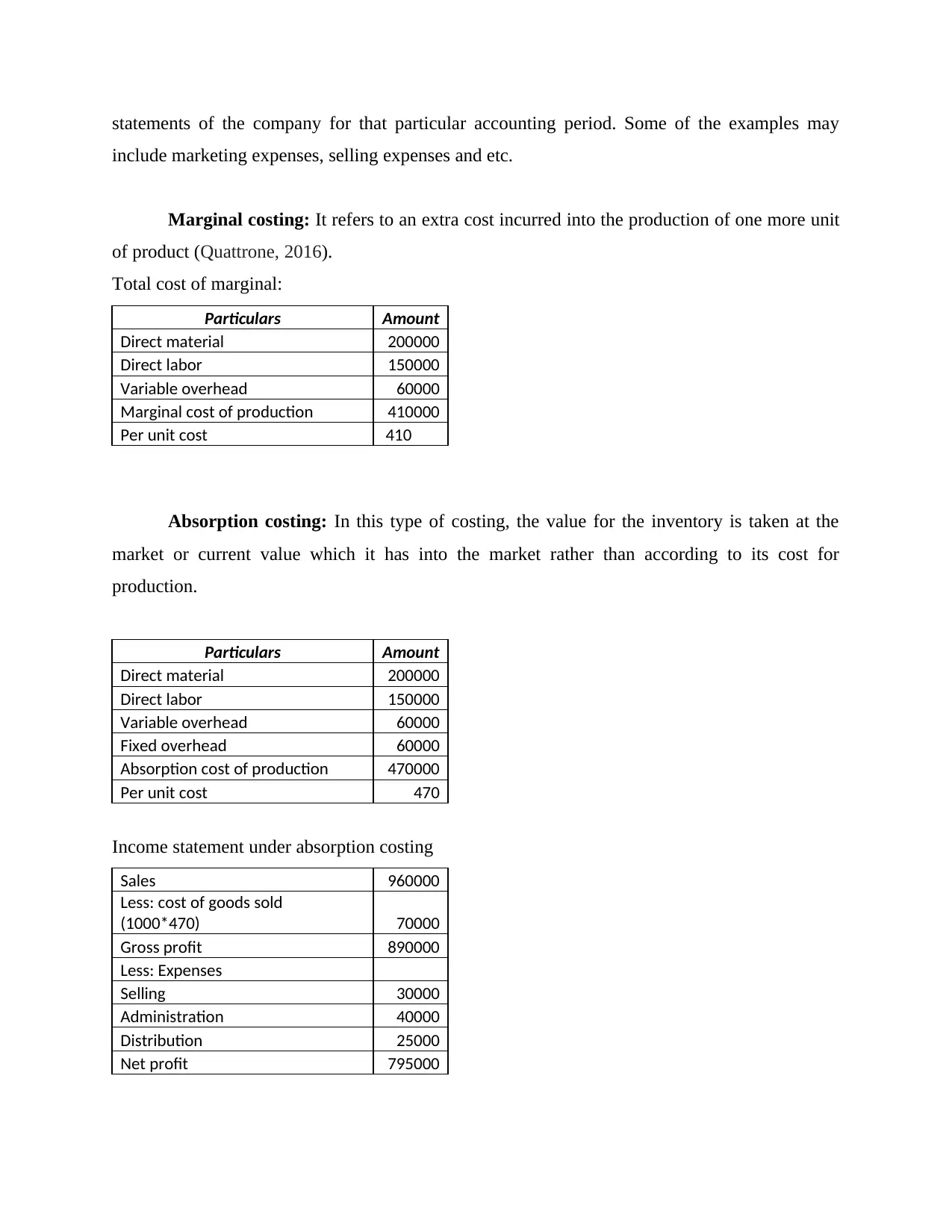

Marginal costing: It refers to an extra cost incurred into the production of one more unit

of product (Quattrone, 2016).

Total cost of marginal:

Particulars Amount

Direct material 200000

Direct labor 150000

Variable overhead 60000

Marginal cost of production 410000

Per unit cost 410

Absorption costing: In this type of costing, the value for the inventory is taken at the

market or current value which it has into the market rather than according to its cost for

production.

Particulars Amount

Direct material 200000

Direct labor 150000

Variable overhead 60000

Fixed overhead 60000

Absorption cost of production 470000

Per unit cost 470

Income statement under absorption costing

Sales 960000

Less: cost of goods sold

(1000*470) 70000

Gross profit 890000

Less: Expenses

Selling 30000

Administration 40000

Distribution 25000

Net profit 795000

include marketing expenses, selling expenses and etc.

Marginal costing: It refers to an extra cost incurred into the production of one more unit

of product (Quattrone, 2016).

Total cost of marginal:

Particulars Amount

Direct material 200000

Direct labor 150000

Variable overhead 60000

Marginal cost of production 410000

Per unit cost 410

Absorption costing: In this type of costing, the value for the inventory is taken at the

market or current value which it has into the market rather than according to its cost for

production.

Particulars Amount

Direct material 200000

Direct labor 150000

Variable overhead 60000

Fixed overhead 60000

Absorption cost of production 470000

Per unit cost 470

Income statement under absorption costing

Sales 960000

Less: cost of goods sold

(1000*470) 70000

Gross profit 890000

Less: Expenses

Selling 30000

Administration 40000

Distribution 25000

Net profit 795000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

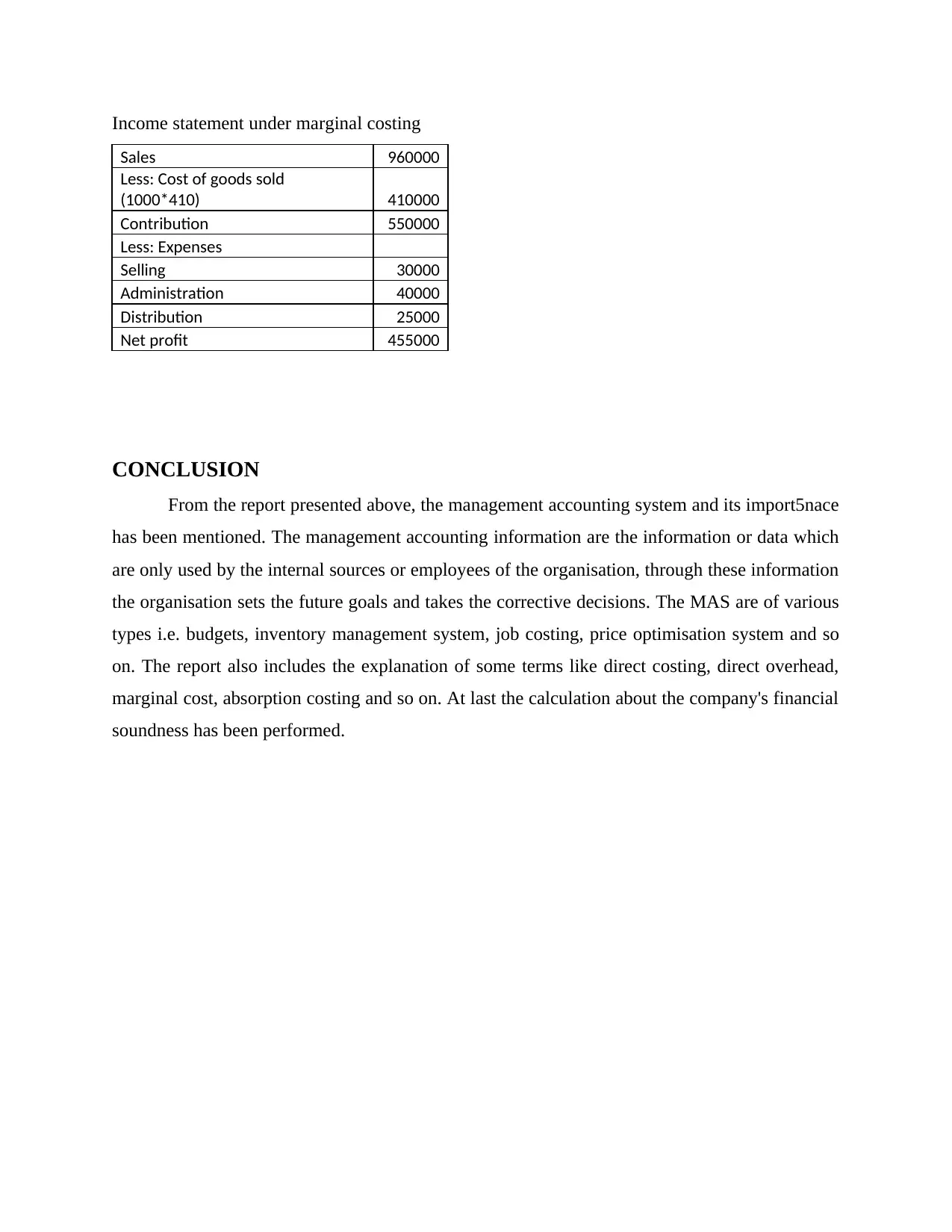

Income statement under marginal costing

Sales 960000

Less: Cost of goods sold

(1000*410) 410000

Contribution 550000

Less: Expenses

Selling 30000

Administration 40000

Distribution 25000

Net profit 455000

CONCLUSION

From the report presented above, the management accounting system and its import5nace

has been mentioned. The management accounting information are the information or data which

are only used by the internal sources or employees of the organisation, through these information

the organisation sets the future goals and takes the corrective decisions. The MAS are of various

types i.e. budgets, inventory management system, job costing, price optimisation system and so

on. The report also includes the explanation of some terms like direct costing, direct overhead,

marginal cost, absorption costing and so on. At last the calculation about the company's financial

soundness has been performed.

Sales 960000

Less: Cost of goods sold

(1000*410) 410000

Contribution 550000

Less: Expenses

Selling 30000

Administration 40000

Distribution 25000

Net profit 455000

CONCLUSION

From the report presented above, the management accounting system and its import5nace

has been mentioned. The management accounting information are the information or data which

are only used by the internal sources or employees of the organisation, through these information

the organisation sets the future goals and takes the corrective decisions. The MAS are of various

types i.e. budgets, inventory management system, job costing, price optimisation system and so

on. The report also includes the explanation of some terms like direct costing, direct overhead,

marginal cost, absorption costing and so on. At last the calculation about the company's financial

soundness has been performed.

REFERENCES

Books and Journals

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

Bedford, D. S. and Speklé, R. F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Botes, V. L. and Sharma, U., 2017. A gap in management accounting education: fact or fiction.

Pacific Accounting Review.

Järvinen, J. T., 2016. Role of management accounting in applying new institutional logics.

Accounting, Auditing & Accountability Journal.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp.42-58.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership construction

in family firms. Qualitative Research in Accounting & Management.

Malina, M. A. ed., 2017. Advances in management accounting. Emerald Group Publishing.

Mokhtar and et. al., 2016. Corporate characteristics and environmental management accounting

(EMA) implementation: evidence from Malaysian public listed companies (PLCs).

Journal of Cleaner Production. 136. pp.111-122.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Nuhu, N. A., Baird, K. and Appuhamilage, A. B., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research.31. pp.45-62.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner Production.

174. pp.1608-1619.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?

Management Accounting Research. 31. pp.118-122.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management accounting

adaptability. International Journal of Accounting and Information Management.

Books and Journals

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

Bedford, D. S. and Speklé, R. F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Botes, V. L. and Sharma, U., 2017. A gap in management accounting education: fact or fiction.

Pacific Accounting Review.

Järvinen, J. T., 2016. Role of management accounting in applying new institutional logics.

Accounting, Auditing & Accountability Journal.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp.42-58.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership construction

in family firms. Qualitative Research in Accounting & Management.

Malina, M. A. ed., 2017. Advances in management accounting. Emerald Group Publishing.

Mokhtar and et. al., 2016. Corporate characteristics and environmental management accounting

(EMA) implementation: evidence from Malaysian public listed companies (PLCs).

Journal of Cleaner Production. 136. pp.111-122.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Nuhu, N. A., Baird, K. and Appuhamilage, A. B., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research.31. pp.45-62.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner Production.

174. pp.1608-1619.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?

Management Accounting Research. 31. pp.118-122.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management accounting

adaptability. International Journal of Accounting and Information Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.