Holmes Institute Audit and Compliance: Deloitte-Navistar Case Study

VerifiedAdded on 2023/03/23

|6

|1467

|34

Report

AI Summary

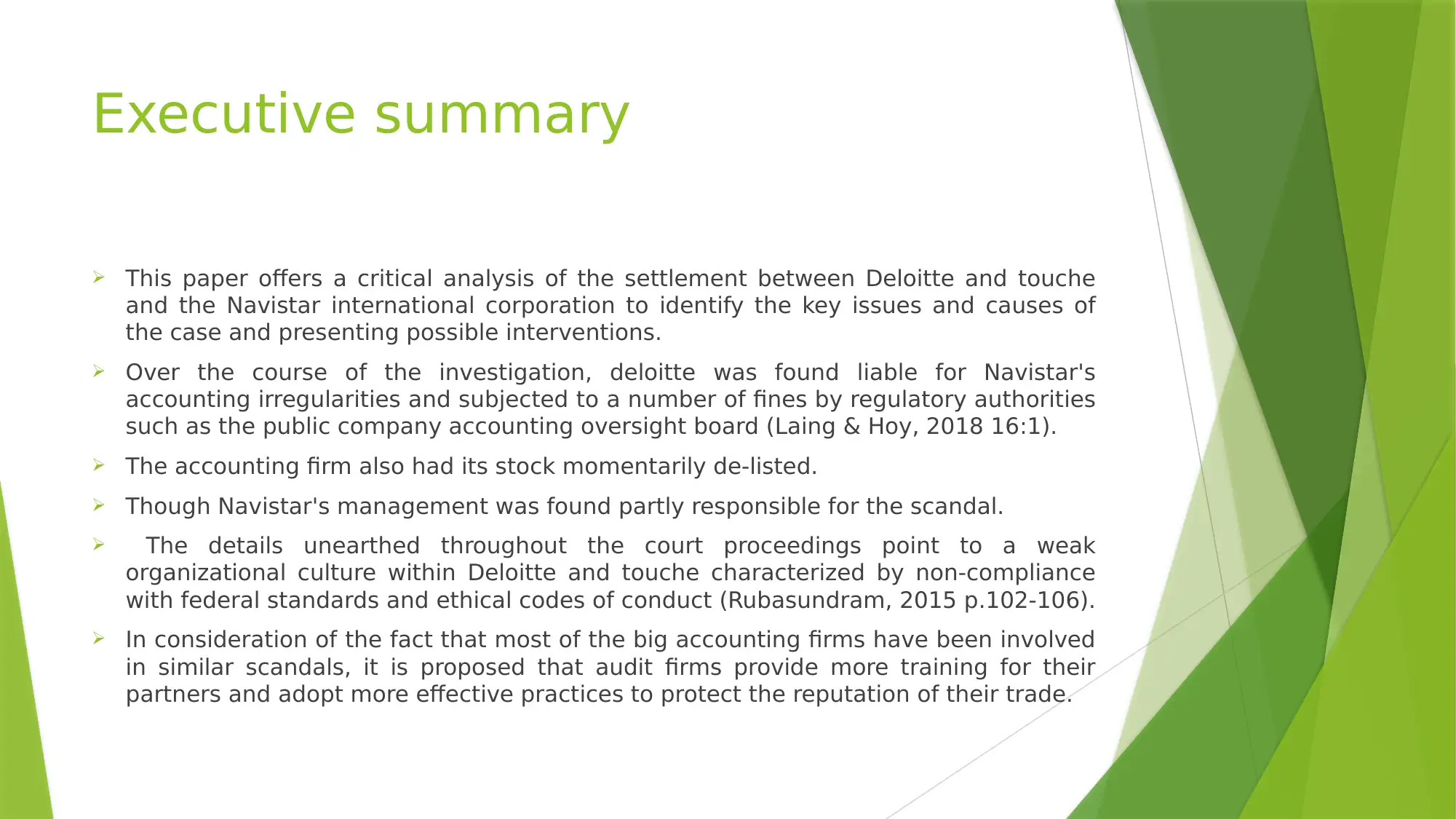

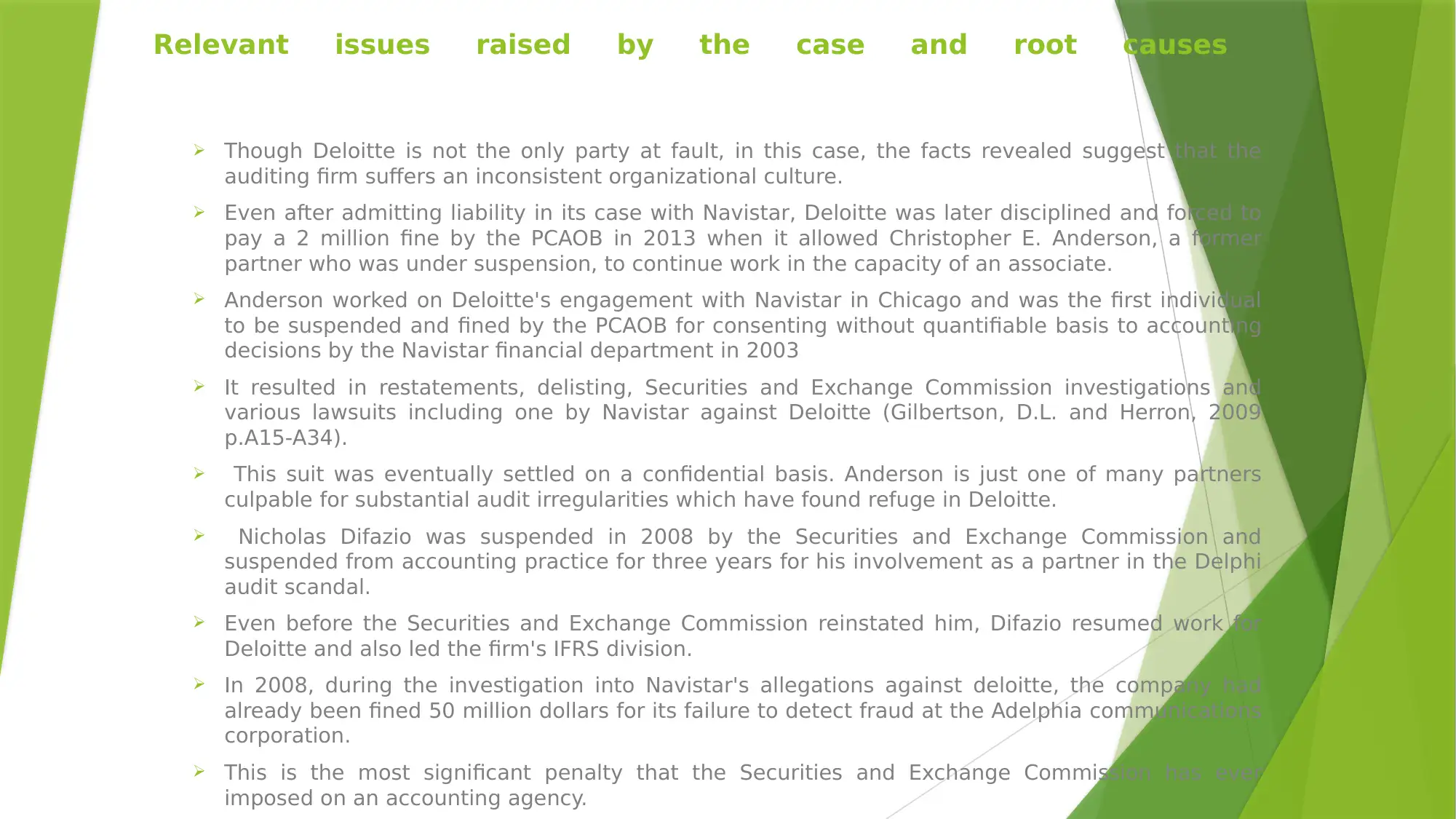

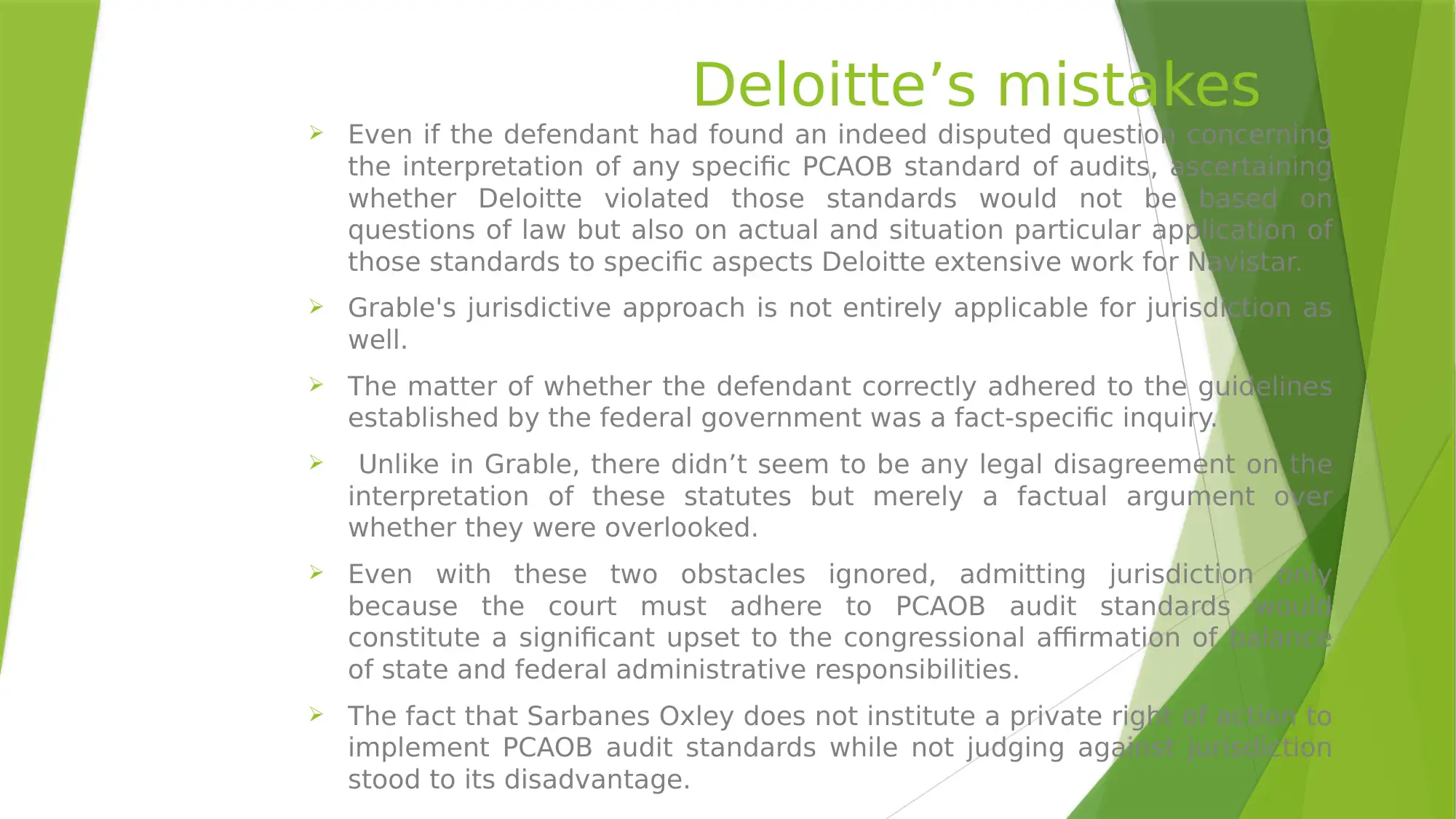

This report provides a critical analysis of the settlement between Deloitte & Touche and Navistar International Corporation. It identifies the key issues and root causes of the case, focusing on Deloitte's liability for Navistar's accounting irregularities and the resulting fines and reputational damage. The analysis delves into the weak organizational culture within Deloitte, highlighting non-compliance with federal standards and ethical codes of conduct. The report examines the specific events, including Navistar's restatement of revenues, delisting from the New York Stock Exchange, and the involvement of key individuals like Christopher E. Anderson and Nicholas Difazio in audit irregularities. Furthermore, it evaluates Deloitte's mistakes in adhering to PCAOB audit standards and the legal arguments involved. The report concludes by proposing interventions such as enhanced auditor training and the adoption of more effective practices to protect the reputation of audit firms and ensure professional integrity. The study emphasizes the need for process-based reviews, internal auditor training, and the use of quality control and statistical tools in auditing practices.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.