Microeconomics: Analysis of Demand, Supply and Equilibrium Concepts

VerifiedAdded on 2022/09/11

|14

|2654

|13

Essay

AI Summary

This essay provides a comprehensive overview of microeconomic principles, focusing on the concepts of demand, supply, and market equilibrium. It begins with a formal definition of microeconomics and its role in understanding the behavior of individual economic agents and firms. The essay then delves into the core concepts of demand, including the law of demand, its assumptions, and the various determinants that influence it, such as price, income, tastes and preferences, and the prices of related goods. Similarly, the essay explores the concept of supply, covering the law of supply, its assumptions, and the factors that determine supply, including price, expectations about future prices, the nature of the good, cost of inputs, and technology. Finally, the essay discusses the mechanism of equilibrium, illustrating how the interaction of demand and supply forces leads to a stable market equilibrium, where the quantity demanded equals the quantity supplied. The essay also highlights the properties of market equilibrium and the role of price in achieving it.

Running head: MICROECONOMICS

Microeconomics

Name of the Student

Name of the University

Course ID

Microeconomics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MICROECONOMICS

Introduction

Microeconomics refers to the division of economics that discusses behavior of individual

or firms in their decision making concerned with allocation of limited resources to meet the ends

and interaction between firms and individuals. One objective of studying microeconomics to

understand the mechanism of market which establishes relative price of goods and services and

allocate scarce resources for alternative uses. Microeconomics describes the conditions that

enable free market to allocate resources efficiently (Pindyck & Rubinfeld, 2015). Moreover, it

also shows the condition of market failure, a situation where free market fails to make efficient

allocation of resources. The basics of market mechanism is based on fundamental concepts of

demand and supply. Demand in the market reflects behavior of buyers while supply captures

behavior of sellers. Different agents participate in the market to maximize their own satisfaction.

The behavior of individual agents in the free market maximizes social welfare. Efficient

allocation is achieved where market reaches equilibrium through mutual interest of buyers and

sellers. In the free market, a stable equilibrium is achieved by interaction between supply and

demand (Fine, 2016). The essay discusses microeconomics concepts of demand, supply and

equilibrium mechanism. The essay first describes formal definition of demand and supply, law of

demand and supply, various determinants of demand and supply and then discusses the

mechanism of equilibrium.

Demand

Demand refers to an economic principle which signifies desire of a consumer to buy

different goods and services supported by purchasing power and willingness to pay given price

of the certain good or service. Individual demand implies demand of a single consumer. Market

Introduction

Microeconomics refers to the division of economics that discusses behavior of individual

or firms in their decision making concerned with allocation of limited resources to meet the ends

and interaction between firms and individuals. One objective of studying microeconomics to

understand the mechanism of market which establishes relative price of goods and services and

allocate scarce resources for alternative uses. Microeconomics describes the conditions that

enable free market to allocate resources efficiently (Pindyck & Rubinfeld, 2015). Moreover, it

also shows the condition of market failure, a situation where free market fails to make efficient

allocation of resources. The basics of market mechanism is based on fundamental concepts of

demand and supply. Demand in the market reflects behavior of buyers while supply captures

behavior of sellers. Different agents participate in the market to maximize their own satisfaction.

The behavior of individual agents in the free market maximizes social welfare. Efficient

allocation is achieved where market reaches equilibrium through mutual interest of buyers and

sellers. In the free market, a stable equilibrium is achieved by interaction between supply and

demand (Fine, 2016). The essay discusses microeconomics concepts of demand, supply and

equilibrium mechanism. The essay first describes formal definition of demand and supply, law of

demand and supply, various determinants of demand and supply and then discusses the

mechanism of equilibrium.

Demand

Demand refers to an economic principle which signifies desire of a consumer to buy

different goods and services supported by purchasing power and willingness to pay given price

of the certain good or service. Individual demand implies demand of a single consumer. Market

2MICROECONOMICS

demand of a commodity indicates total quantity of the commodity demanded by all consumer in

the market.

Law of demand

The law of demand formally presents a relationship of price with quantity demanded of a

good. The law states that given all other factors affecting demand a growth in price of a good

lowers quantity demanded of the good and vice versa (Moulin, 2014). The law of demand

therefore suggests an inverse association between quantity demanded and price. That is demand

changes in the opposite path of price.

Assumption of law of demand

The basic assumptions behind law of demand are as follows

i)Tastes and preferences of buyers stay constant.

ii) There are no changes in income of consumers

iii) There is no change in custom rules.

iv) The good which is to be used should not confer any distinction on the buyers (Rader, 2014).

v) The commodity concerned should not have any substitutes.

vi) Price of other related products should remain constant.

vii) Quality of the product should remain fixed.

viii) Habits of the buyers remain constant.

demand of a commodity indicates total quantity of the commodity demanded by all consumer in

the market.

Law of demand

The law of demand formally presents a relationship of price with quantity demanded of a

good. The law states that given all other factors affecting demand a growth in price of a good

lowers quantity demanded of the good and vice versa (Moulin, 2014). The law of demand

therefore suggests an inverse association between quantity demanded and price. That is demand

changes in the opposite path of price.

Assumption of law of demand

The basic assumptions behind law of demand are as follows

i)Tastes and preferences of buyers stay constant.

ii) There are no changes in income of consumers

iii) There is no change in custom rules.

iv) The good which is to be used should not confer any distinction on the buyers (Rader, 2014).

v) The commodity concerned should not have any substitutes.

vi) Price of other related products should remain constant.

vii) Quality of the product should remain fixed.

viii) Habits of the buyers remain constant.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MICROECONOMICS

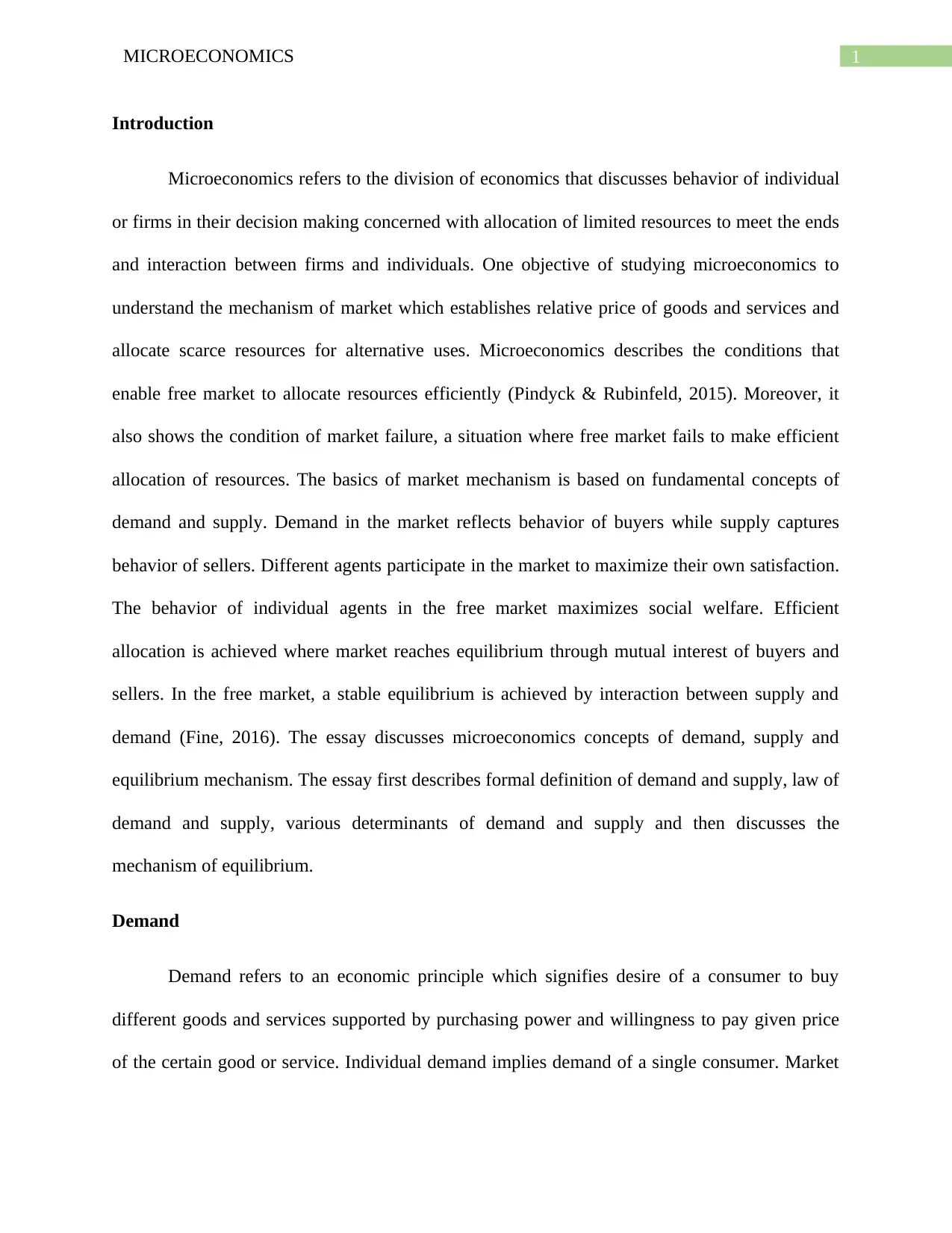

The law of demand operates under the above mentioned assumptions. Changes in any of

the assumptions lead to violation of the law (Currie, Peel & Peters, 2016). Based on the law of

demand, demand curve of a good slopes downward.

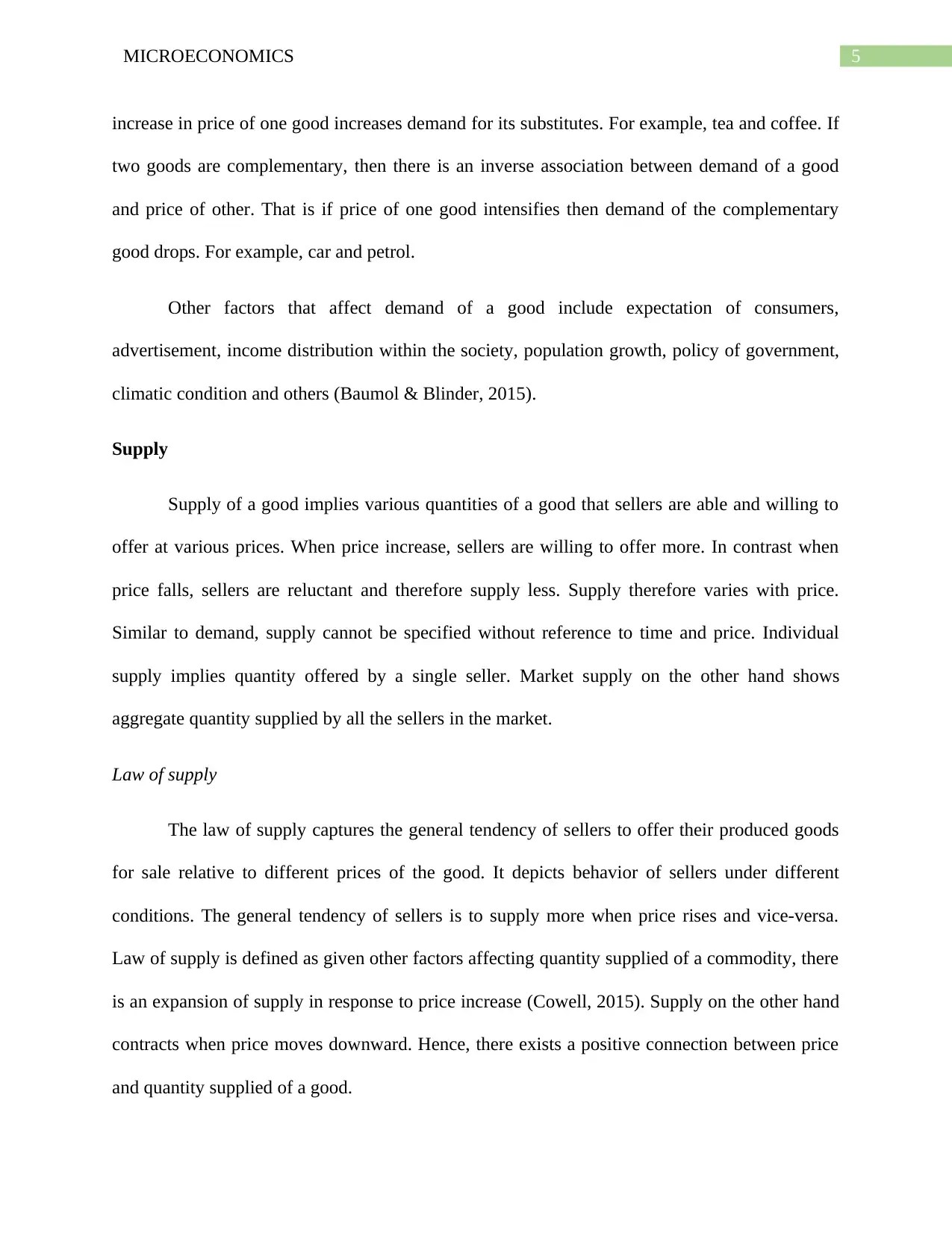

Figure 1: Demand curve

In the above figure, the downward sloping line DD shows the demand curve of a

particular good. Corresponding to a price of P1, quantity demanded of the good is Q1. Now, if

price increases from P1 to P2, quantity demanded of the good decreases from Q1 to Q2.

Various determinants of demand

Demand of a particular commodity is influenced by several factors. Size of the impact of

each of the factors on demand is determined by nature of the good. Factors affecting demand of a

commodity is discussed below

Price

The law of demand operates under the above mentioned assumptions. Changes in any of

the assumptions lead to violation of the law (Currie, Peel & Peters, 2016). Based on the law of

demand, demand curve of a good slopes downward.

Figure 1: Demand curve

In the above figure, the downward sloping line DD shows the demand curve of a

particular good. Corresponding to a price of P1, quantity demanded of the good is Q1. Now, if

price increases from P1 to P2, quantity demanded of the good decreases from Q1 to Q2.

Various determinants of demand

Demand of a particular commodity is influenced by several factors. Size of the impact of

each of the factors on demand is determined by nature of the good. Factors affecting demand of a

commodity is discussed below

Price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MICROECONOMICS

The first most important determinant of demand is price of the product. Price of a

produce largely influences its demand. As suggested by law of demand price has an inverse

association with demand (McKenzie & Lee, 2016). Holding all other factors constant, demand

increase as price falls and decreases as price surges.

Income

After price, income is considered as one of the most important factors influencing

demand. Income by influencing affordability or purchasing power of people affects demand. The

relation between demand and income depends on the nature of the product. For a normal good

income has a positive influence on demand. That is demand increases with increase in income

and demand falls with decline in income. The case however is different for inferior goods.

Demand for inferior goods fall with an increase in income while demand increases with fall in

income.

Taste and preferences

One primary factor directing demand of a good is the tastes and preferences. Tastes and

preferences of consumers play a vital role in determining demand. There are again several

factors that influence tastes and preferences. These factors are life styles, buying habits, living

standard, age, sex, religious value, customs and fashion trend (Kreps, 2019). With change in any

of the mentioned factors tastes and preference change and demand changes accordingly.

Price of related products

Demand of a commodity not only influenced by its own demand but also by variation in

prices of related goods. Related goods can be either substitutes or complementary. When two

goods are substitutes then demand of a good is positive related with price if other. That means,

The first most important determinant of demand is price of the product. Price of a

produce largely influences its demand. As suggested by law of demand price has an inverse

association with demand (McKenzie & Lee, 2016). Holding all other factors constant, demand

increase as price falls and decreases as price surges.

Income

After price, income is considered as one of the most important factors influencing

demand. Income by influencing affordability or purchasing power of people affects demand. The

relation between demand and income depends on the nature of the product. For a normal good

income has a positive influence on demand. That is demand increases with increase in income

and demand falls with decline in income. The case however is different for inferior goods.

Demand for inferior goods fall with an increase in income while demand increases with fall in

income.

Taste and preferences

One primary factor directing demand of a good is the tastes and preferences. Tastes and

preferences of consumers play a vital role in determining demand. There are again several

factors that influence tastes and preferences. These factors are life styles, buying habits, living

standard, age, sex, religious value, customs and fashion trend (Kreps, 2019). With change in any

of the mentioned factors tastes and preference change and demand changes accordingly.

Price of related products

Demand of a commodity not only influenced by its own demand but also by variation in

prices of related goods. Related goods can be either substitutes or complementary. When two

goods are substitutes then demand of a good is positive related with price if other. That means,

5MICROECONOMICS

increase in price of one good increases demand for its substitutes. For example, tea and coffee. If

two goods are complementary, then there is an inverse association between demand of a good

and price of other. That is if price of one good intensifies then demand of the complementary

good drops. For example, car and petrol.

Other factors that affect demand of a good include expectation of consumers,

advertisement, income distribution within the society, population growth, policy of government,

climatic condition and others (Baumol & Blinder, 2015).

Supply

Supply of a good implies various quantities of a good that sellers are able and willing to

offer at various prices. When price increase, sellers are willing to offer more. In contrast when

price falls, sellers are reluctant and therefore supply less. Supply therefore varies with price.

Similar to demand, supply cannot be specified without reference to time and price. Individual

supply implies quantity offered by a single seller. Market supply on the other hand shows

aggregate quantity supplied by all the sellers in the market.

Law of supply

The law of supply captures the general tendency of sellers to offer their produced goods

for sale relative to different prices of the good. It depicts behavior of sellers under different

conditions. The general tendency of sellers is to supply more when price rises and vice-versa.

Law of supply is defined as given other factors affecting quantity supplied of a commodity, there

is an expansion of supply in response to price increase (Cowell, 2015). Supply on the other hand

contracts when price moves downward. Hence, there exists a positive connection between price

and quantity supplied of a good.

increase in price of one good increases demand for its substitutes. For example, tea and coffee. If

two goods are complementary, then there is an inverse association between demand of a good

and price of other. That is if price of one good intensifies then demand of the complementary

good drops. For example, car and petrol.

Other factors that affect demand of a good include expectation of consumers,

advertisement, income distribution within the society, population growth, policy of government,

climatic condition and others (Baumol & Blinder, 2015).

Supply

Supply of a good implies various quantities of a good that sellers are able and willing to

offer at various prices. When price increase, sellers are willing to offer more. In contrast when

price falls, sellers are reluctant and therefore supply less. Supply therefore varies with price.

Similar to demand, supply cannot be specified without reference to time and price. Individual

supply implies quantity offered by a single seller. Market supply on the other hand shows

aggregate quantity supplied by all the sellers in the market.

Law of supply

The law of supply captures the general tendency of sellers to offer their produced goods

for sale relative to different prices of the good. It depicts behavior of sellers under different

conditions. The general tendency of sellers is to supply more when price rises and vice-versa.

Law of supply is defined as given other factors affecting quantity supplied of a commodity, there

is an expansion of supply in response to price increase (Cowell, 2015). Supply on the other hand

contracts when price moves downward. Hence, there exists a positive connection between price

and quantity supplied of a good.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MICROECONOMICS

Assumption of law of supply

The operation of law of supply is based on some assumptions. The assumptions behind

law of supply are given as follows

i)Income of buyers of the good remain unchanged

ii) The technique of production remains fixed

iii) The transportation cost remains unchanged

iv) There is no change in production cost (Mankiw, 2014).

v) The scale of production is assumed to be fixed at the given time.

vi) There is no speculation in the market.

vii) There is no change in price of other goods produced.

ix) There is no change in government policy.

When the above mentioned assumptions hold, supply of a good move in the same

direction of price. Because of the operation of law of supply, supply curve of a good is positively

sloped. This is shown in figure 2

Assumption of law of supply

The operation of law of supply is based on some assumptions. The assumptions behind

law of supply are given as follows

i)Income of buyers of the good remain unchanged

ii) The technique of production remains fixed

iii) The transportation cost remains unchanged

iv) There is no change in production cost (Mankiw, 2014).

v) The scale of production is assumed to be fixed at the given time.

vi) There is no speculation in the market.

vii) There is no change in price of other goods produced.

ix) There is no change in government policy.

When the above mentioned assumptions hold, supply of a good move in the same

direction of price. Because of the operation of law of supply, supply curve of a good is positively

sloped. This is shown in figure 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MICROECONOMICS

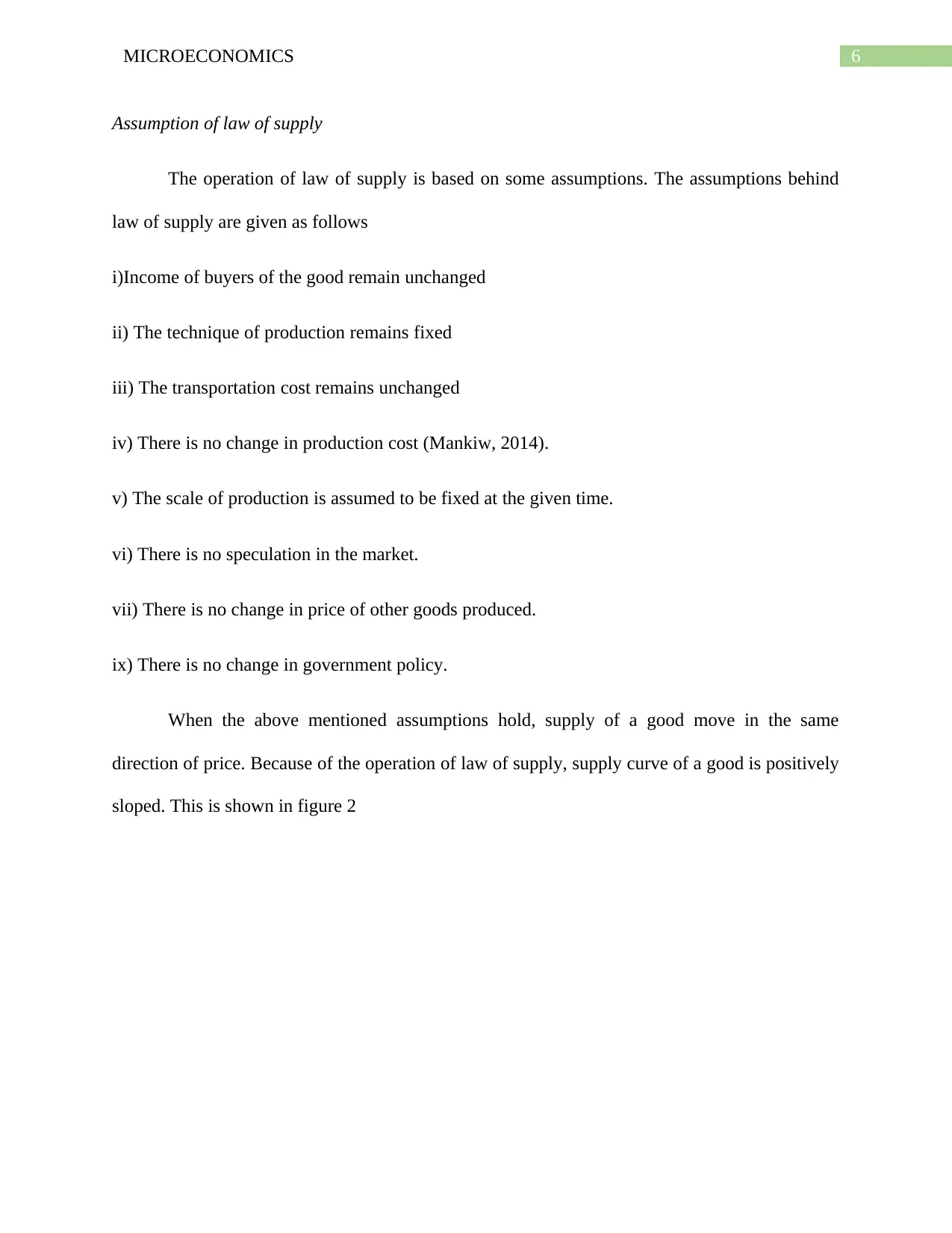

Figure 2: Supply curve

In figure 2, SS shows supply curve of a commodity. At price P*, quantity supplied of the

commodity is Q*. As price increases to P* to P1, quantity supplied grows from Q* to Q1.

Various determinants of supply

Various factors affecting supply of a commodity ate known as determinants of supply

(Cowen & Tabarrok, 2015). The important determinants of supply are as follows

Price

The most vital factor determining supply is price of a product. A larger quantity of good

is supplied at a high price while a smaller amount of good is supplied corresponding to a lower

price.

Expectation about future price

Supply of a good is influenced by expectation of sellers about future price. When sellers

expect price will increase in future, they will reduce current supply to sell a higher quantity in

Figure 2: Supply curve

In figure 2, SS shows supply curve of a commodity. At price P*, quantity supplied of the

commodity is Q*. As price increases to P* to P1, quantity supplied grows from Q* to Q1.

Various determinants of supply

Various factors affecting supply of a commodity ate known as determinants of supply

(Cowen & Tabarrok, 2015). The important determinants of supply are as follows

Price

The most vital factor determining supply is price of a product. A larger quantity of good

is supplied at a high price while a smaller amount of good is supplied corresponding to a lower

price.

Expectation about future price

Supply of a good is influenced by expectation of sellers about future price. When sellers

expect price will increase in future, they will reduce current supply to sell a higher quantity in

8MICROECONOMICS

future (Nicholson & Snyder, 2014). In contrast, if seller expect price to be lowered in future they

will try to sell as much as possible at present resulting in an increase in current market supply.

Nature of the good

Supply varies depending on nature of the good. For perishable good supply is very

inelastic since entire stock of such good has to be disposed of within a very short time span

irrespective of its price. Supply in contrast is very elastic for goods that can be stored for a

relatively longer period.

Cost of inputs

Various factors inputs are used in producing a particular good. Supply varies with

changes in cost of inputs. If cost of inputs increases, there is an increase in production cost which

lowers supply (Blad & Keiding, 2014). When cost of factor inputs decreases, production cost

decreases as well resulting in an increase in supply.

Technology

The technique of production is a crucial determinant of supply. Use of advanced

technology increases productivity of different factor inputs causing an expansion of supply.

Improvement in technology through continuous innovation greatly influences supply of the

commodity (Mahanty, 2014).

In addition to above discussed factors other factors leading to a change in supply of a

commodity include natural condition, transportation cost and condition of transportation, policy

of government and others.

Equilibrium mechanism

future (Nicholson & Snyder, 2014). In contrast, if seller expect price to be lowered in future they

will try to sell as much as possible at present resulting in an increase in current market supply.

Nature of the good

Supply varies depending on nature of the good. For perishable good supply is very

inelastic since entire stock of such good has to be disposed of within a very short time span

irrespective of its price. Supply in contrast is very elastic for goods that can be stored for a

relatively longer period.

Cost of inputs

Various factors inputs are used in producing a particular good. Supply varies with

changes in cost of inputs. If cost of inputs increases, there is an increase in production cost which

lowers supply (Blad & Keiding, 2014). When cost of factor inputs decreases, production cost

decreases as well resulting in an increase in supply.

Technology

The technique of production is a crucial determinant of supply. Use of advanced

technology increases productivity of different factor inputs causing an expansion of supply.

Improvement in technology through continuous innovation greatly influences supply of the

commodity (Mahanty, 2014).

In addition to above discussed factors other factors leading to a change in supply of a

commodity include natural condition, transportation cost and condition of transportation, policy

of government and others.

Equilibrium mechanism

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MICROECONOMICS

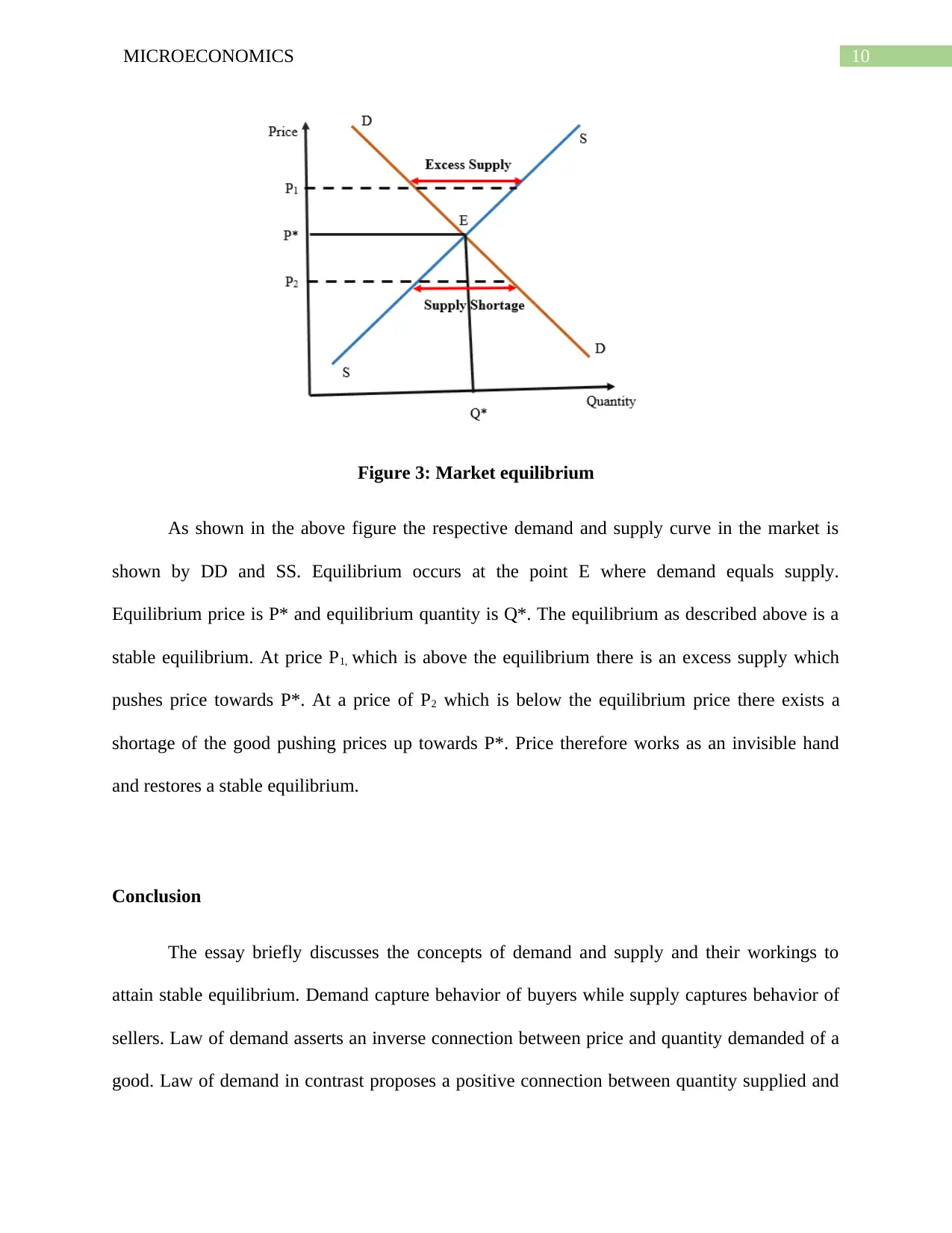

After discussing various aspects related to demand and supply, the concept of equilibrium

can be discussed. Economic equilibrium refers to a balanced condition where supply and demand

forces match. If there are no external forces, then equilibrium values of variable remain constant.

In a free market, equilibrium corresponds to the point where market quantity supplied of the

commodity equals quantity demanded (Stoneman & Bartoloni, 2018). At this equilibrium, a

stable price is achieved by competition between buyers and sellers group and quantity demanded

by the buyers are exactly same as the quantity supplied by the seller. The price determined in the

free market is called fee market price and does not change unless there is a change in either

demand or supply. The quantity corresponding to equilibrium is called the equilibrium quantity

or market clearing quantity. There are three fundamental properties of market equilibrium which

are given as follows

The behavior of agents participating in the market remain consistent

Neither of the agents have any incentive to change its behavior

Market equilibrium is the result of a dynamic process and is stable (Dixit, 2014).

The free market equilibrium satisfies all the three properties. The process of equilibrium

attainment in a market is shown in the following figure

After discussing various aspects related to demand and supply, the concept of equilibrium

can be discussed. Economic equilibrium refers to a balanced condition where supply and demand

forces match. If there are no external forces, then equilibrium values of variable remain constant.

In a free market, equilibrium corresponds to the point where market quantity supplied of the

commodity equals quantity demanded (Stoneman & Bartoloni, 2018). At this equilibrium, a

stable price is achieved by competition between buyers and sellers group and quantity demanded

by the buyers are exactly same as the quantity supplied by the seller. The price determined in the

free market is called fee market price and does not change unless there is a change in either

demand or supply. The quantity corresponding to equilibrium is called the equilibrium quantity

or market clearing quantity. There are three fundamental properties of market equilibrium which

are given as follows

The behavior of agents participating in the market remain consistent

Neither of the agents have any incentive to change its behavior

Market equilibrium is the result of a dynamic process and is stable (Dixit, 2014).

The free market equilibrium satisfies all the three properties. The process of equilibrium

attainment in a market is shown in the following figure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MICROECONOMICS

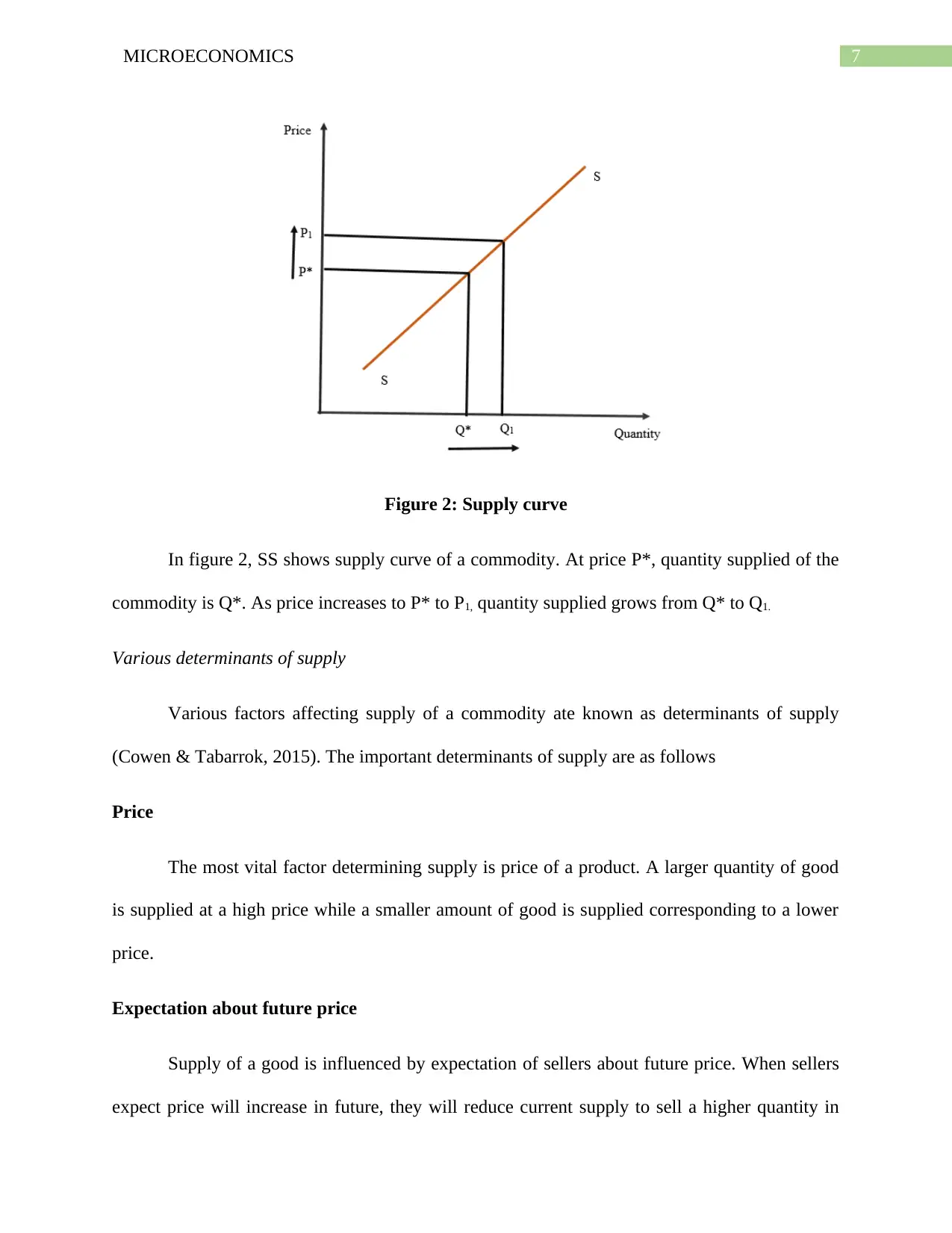

Figure 3: Market equilibrium

As shown in the above figure the respective demand and supply curve in the market is

shown by DD and SS. Equilibrium occurs at the point E where demand equals supply.

Equilibrium price is P* and equilibrium quantity is Q*. The equilibrium as described above is a

stable equilibrium. At price P1, which is above the equilibrium there is an excess supply which

pushes price towards P*. At a price of P2 which is below the equilibrium price there exists a

shortage of the good pushing prices up towards P*. Price therefore works as an invisible hand

and restores a stable equilibrium.

Conclusion

The essay briefly discusses the concepts of demand and supply and their workings to

attain stable equilibrium. Demand capture behavior of buyers while supply captures behavior of

sellers. Law of demand asserts an inverse connection between price and quantity demanded of a

good. Law of demand in contrast proposes a positive connection between quantity supplied and

Figure 3: Market equilibrium

As shown in the above figure the respective demand and supply curve in the market is

shown by DD and SS. Equilibrium occurs at the point E where demand equals supply.

Equilibrium price is P* and equilibrium quantity is Q*. The equilibrium as described above is a

stable equilibrium. At price P1, which is above the equilibrium there is an excess supply which

pushes price towards P*. At a price of P2 which is below the equilibrium price there exists a

shortage of the good pushing prices up towards P*. Price therefore works as an invisible hand

and restores a stable equilibrium.

Conclusion

The essay briefly discusses the concepts of demand and supply and their workings to

attain stable equilibrium. Demand capture behavior of buyers while supply captures behavior of

sellers. Law of demand asserts an inverse connection between price and quantity demanded of a

good. Law of demand in contrast proposes a positive connection between quantity supplied and

11MICROECONOMICS

price. Some important determinants of demand are price, income, price of related goods, tastes

and preference and others. Some factors affecting supply of a good include price, nature of good,

technology, cost of inputs and others. Finally, a stable equilibrium is achieved where market

demand and market supply matches.

price. Some important determinants of demand are price, income, price of related goods, tastes

and preference and others. Some factors affecting supply of a good include price, nature of good,

technology, cost of inputs and others. Finally, a stable equilibrium is achieved where market

demand and market supply matches.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.